SQ - Block: Back To 'Square' One

2023-10-11 12:22:09 ET

Summary

- Block is building the financial ecosystem of tomorrow.

- The company is at the forefront of multiple financial megatrends.

- The commoditization of fintech applications is a major risk to the company.

- Block stock is now trading near its March 2020 lows - a major support.

Introduction

Fintech stocks have been beaten down to oblivion lately. What was once a much-loved emerging industry has turned into one of the most hated investment sectors.

Standing (perhaps "lying wounded on the floor" is a more accurate description) front and center during this bloodbath are none other than the three major modern payment processors: PayPal ( PYPL ), Adyen ( ADYEY ), and Block ( SQ ).

All three of these sold off violently following their most recent earnings report which begs the question: is it the right time to buy these stocks?

I covered both PayPal and Adyen recently:

But today, I want to zero in on Block.

That said, here's the main takeaway of my deep-dive write-up on Block:

Block stock is completing its round-trip as it trades close to its Covid lows.

Overvaluation, slowing growth, and competition are some of the reasons why the stock crashed so hard.

However, Block is building the financial ecosystem of tomorrow and is well-positioned for future growth as e-commerce, digital wallets, and digital banking continues to gain traction.

Following the selloff, Block stock looks undervalued, a good time to bet on this fintech fallen angel.

Company

The founding story of Block, formerly Square, began more than a decade ago when Twitter co-founder Jack Dorsey was fired from his CEO role in the social media company in 2008.

He returned to his hometown in St. Louis, Missouri, and reconnected with some of his childhood friends, one of whom was Jim McKelvey.

At that time, McKelvey was a glassblower and he made a living selling his glass artwork. The problem is that McKelvey can only accept cash as payment, and if a prospective buyer wanted to make a purchase with a credit card, he would have to respectfully decline.

That was an annoying problem and that meant a lot of sales lost. One time, McKelvey couldn't close a $2,000 deal as his business doesn't accept credit cards.

McKelvey soon realized that other small merchants would experience the same problem as he did. Coincidentally - more so, fortunately - the unemployed former Twitter CEO was in town to listen to McKelvey's complaint.

That's when both men came up with a solution to McKelvey's problem: to enable small businesses to accept card payments through their mobile phones.

In February 2009, Square was launched. Its first product was a headphone dongle with a swipeable credit card reader, fully compatible with iOS and Android.

Anyone can now accept card payments by plugging the reader into a phone or tablet and downloading the Square app. After swiping the card through the reader, the customer signs on the touchscreen to verify the payment. He or she then leaves her contact details and the payment receipt will be sent over via email or SMS.

This is a much more simple, intuitive, and user-friendly experience than the payment terminals offered by legacy processors like Verifone.

Pricing for the readers was even better: $0. In other words, merchants can test out this product free of charge. In exchange, merchants pay a small processing fee of around 2.75%.

Square Website

It was a brilliantly simple solution to a nagging issue - there was product-market fit and within a short period of time, product adoption exploded.

Over the years, Square continued to launch innovative products, enhancing its fleet of modern point-of-sale ((POS)) solutions.

Unlike PayPal and Adyen - which initially focused on online payment processing, - Square began its venture by focusing on POS processing.

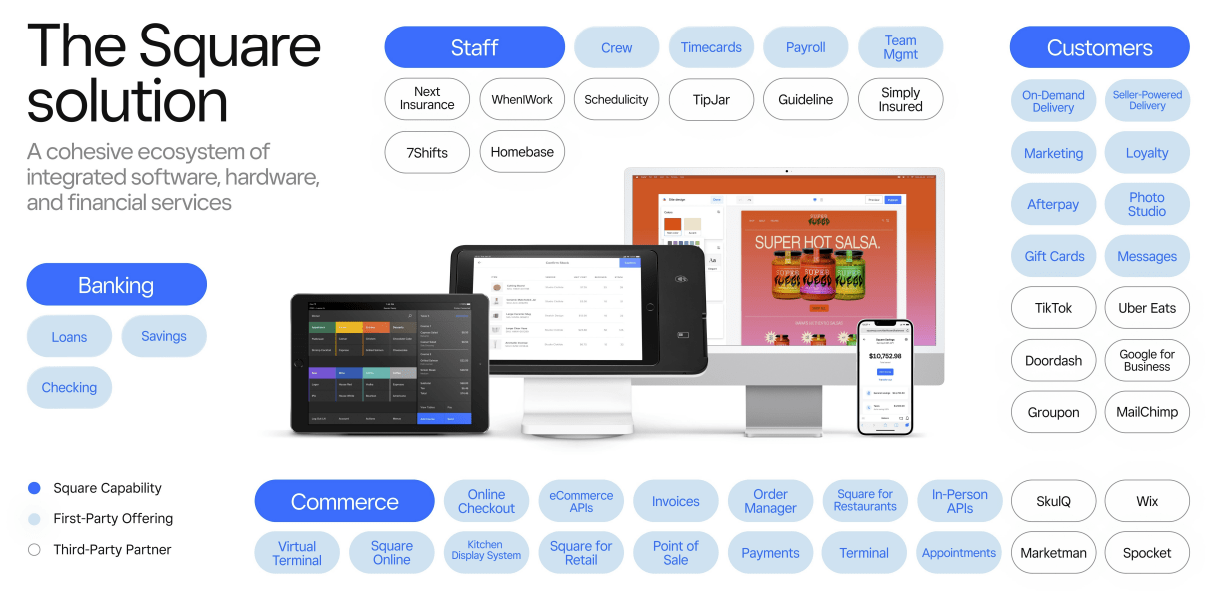

Today, Square offers a unified commerce ecosystem - combining software, hardware, and financial services - which provides sellers with all the tools they need for processing payments and growing their businesses.

The Square ecosystem consists of four key elements:

- Commerce : helps sellers process payments, track sales and inventory, as well as analyze transaction-level data. This also includes Square's POS hardware, Square Online to build a website and online store, and Square Appointments to integrate booking capabilities, among other things.

{kind=link}

- Customers : helps sellers grow their businesses by acquiring, engaging, and retaining customers. This includes Square Marketing to launch marketing campaigns, Square Loyalty to enroll customers in a loyalty program, as well as Customer Directory for customer relationship management.

- Staff : provides sellers the tools to streamline workforce management, including scheduling staff, communicating with team members, and paying employee wages.

- Banking : offer sellers banking services including small business loans ranging from $300 to $250K, checking and savings accounts to manage their finances, as well as spend their hard-earned money through a Square Debit Card.

In essence, the Square seller ecosystem, as shown below, provides sellers with an all-in-one platform to streamline business operations, including payment processing, customer engagement, workforce management, and financial management.

{kind=link}

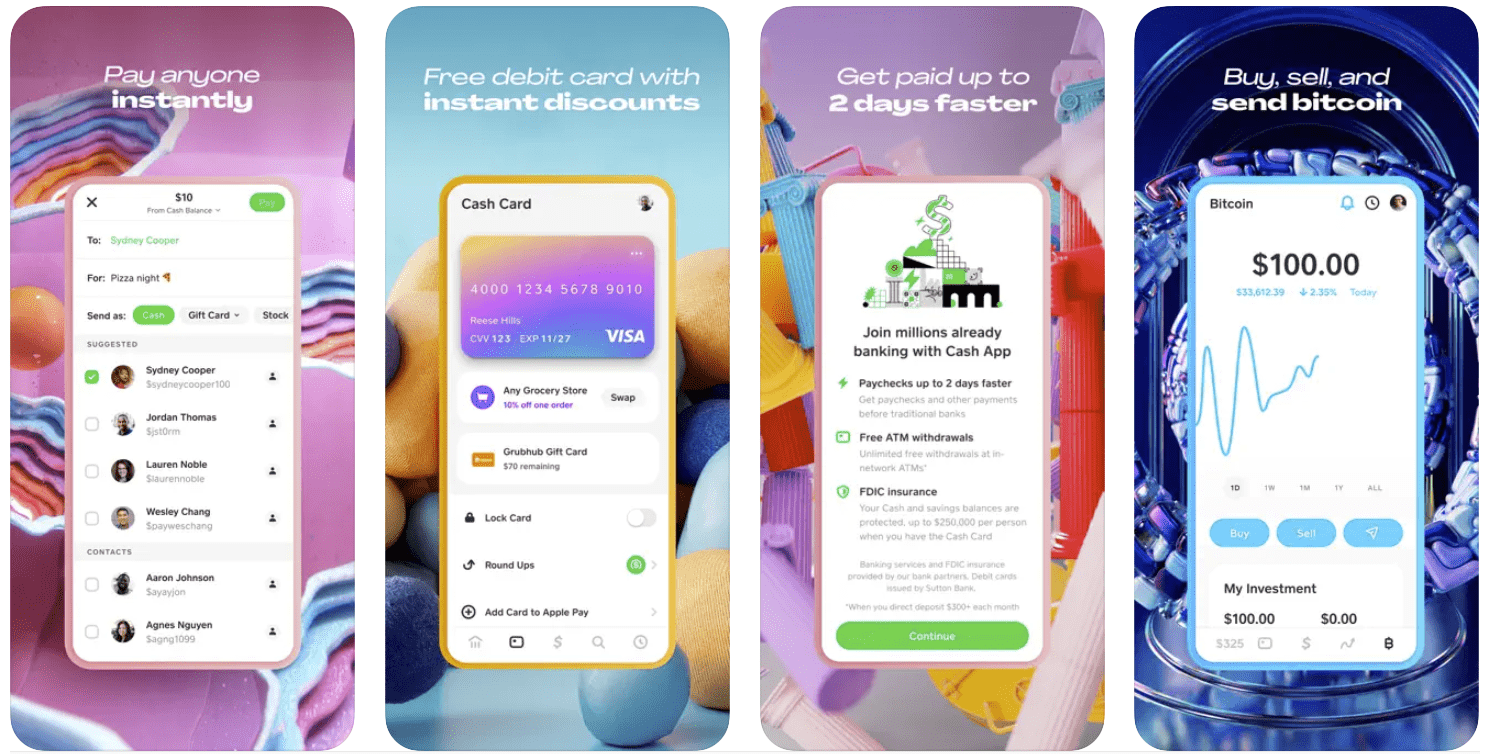

In 2013, Square launched its most important product to date: the Cash App - which represents the consumer ecosystem.

Cash App was originally launched as a peer-to-peer platform but has since grown into a digital banking offering for individuals to manage their finances.

With the Cash App, consumers get to:

- Send money to anyone instantly.

- Bank and spend with the Cash App debit card.

- Set aside money in a Savings account.

- Invest in stocks and crypto.

- Receive exclusive discounts through Cash Boost.

- Borrow up to $500 in a given month.

- File their taxes for free.

{kind=link}

Cash App was a huge success for Square as it brought in millions of users into the ecosystem. Its peer-to-peer payment network grew exponentially as users invited their friends, family, and colleagues into the platform.

While both the Square (seller) and Cash App (consumer) ecosystems were growing by the day, they were still operating as two siloed ecosystems.

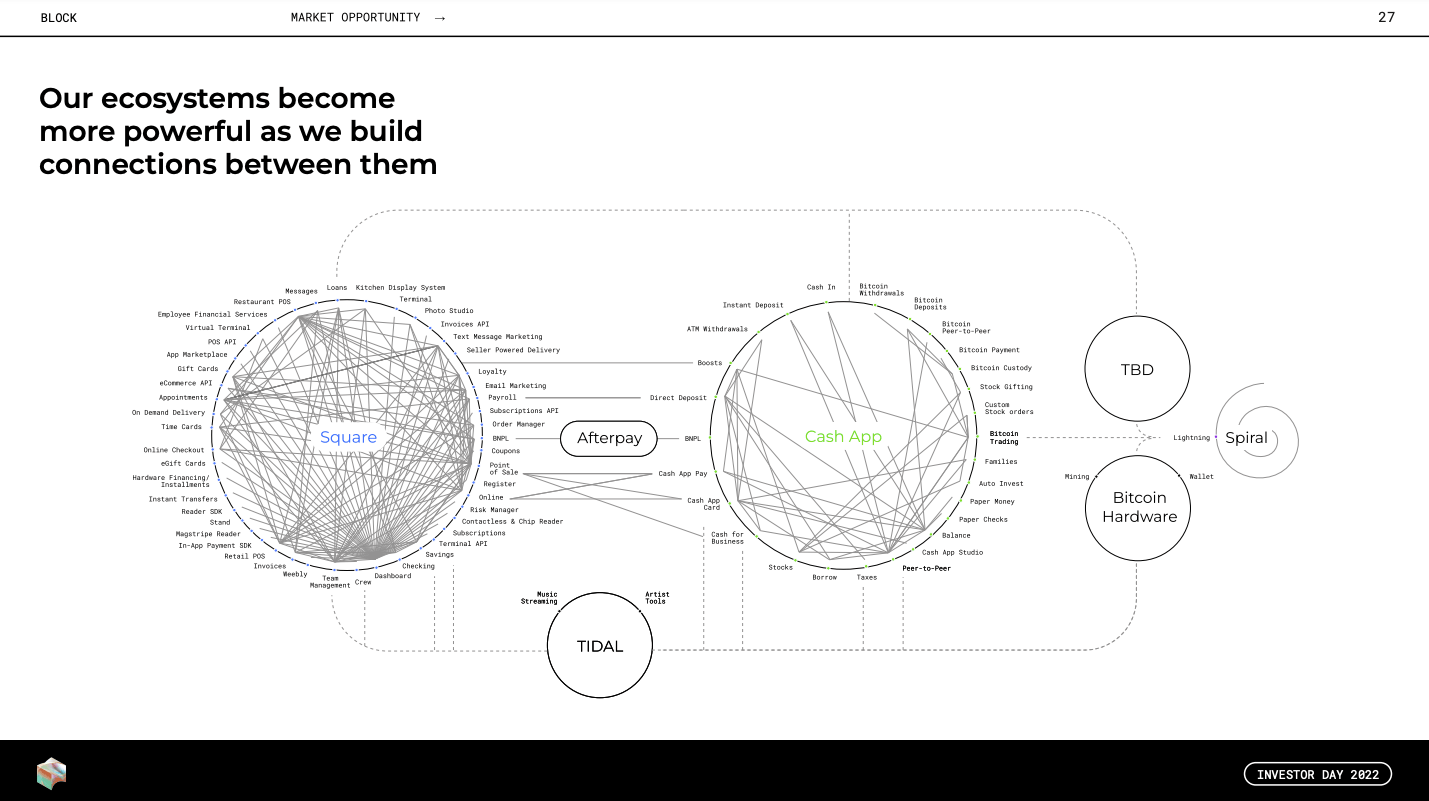

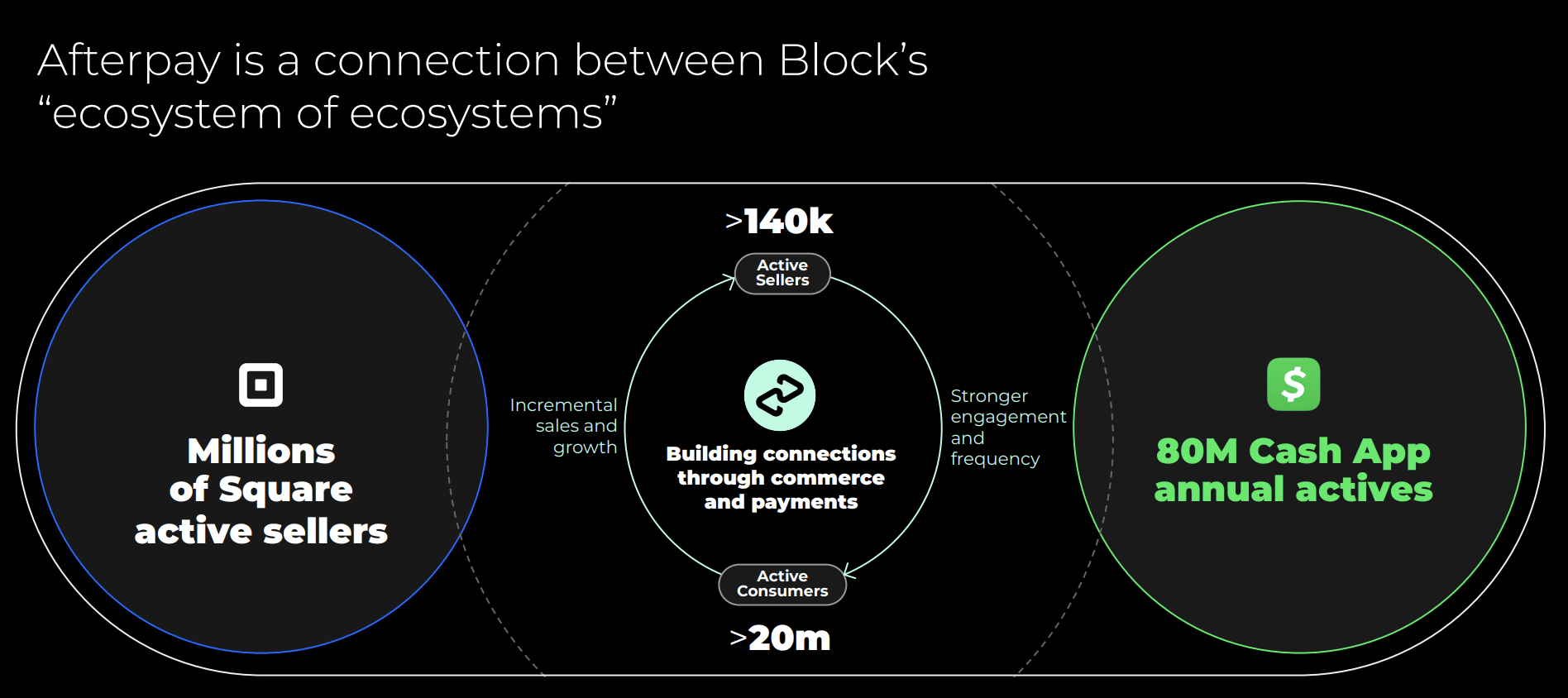

To unlock maximum value for both sellers and consumers, management needed to find a way to somehow connect the two ecosystems together - enter Afterpay.

In January 2022, Square completed the acquisition of the buy now, pay later platform, Afterpay, for $29B , which according to management, serves as the bridge between the Square and Cash App ecosystems.

It made a lot of sense since Afterpay has a marketplace business model that not only connects merchants and shoppers but also has the BNPL fintech application to it.

- Square + Afterpay : enables BNPL as a payment option.

- Cash App + Afterpay : bring commerce into Cash App.

Square, Cash App, and Afterpay: these are high-quality assets that could form the ultimate fintech ecosystem - the "ecosystem of ecosystems", so to speak.

{kind=link}

However, it's still too early to tell whether the Afterpay integration will bring to life management's grand vision of economic empowerment through its closed-loop financial system.

Block also has other products/projects but I won't discuss them much here:

- TIDAL : a global music streaming platform.

- TBD : an open-source platform focused on making the decentralized financial world accessible to everyone.

- Spiral : an independent, bitcoin-focused entity.

Nevertheless, Square changed its name to Block shortly after it announced its intent to acquire Afterpay. In essence, the new entity strives to build the ecosystem of ecosystems, with its all-in-one financial platform as the overarching foundation.

The name has many associated meanings for the company - building blocks, neighborhood blocks and their local businesses, communities coming together at block parties full of music, a blockchain, a section of code, and obstacles to overcome.

Moats

Based on my research and analysis, I identified three competitive moats for Block: brand, network effects, and switching costs.

Brand

Block has three popular financial apps with high ratings. As of this writing, here are their app ratings in the Apple App Store:

- Square : 389K reviews with 4.8/5.0 stars.

- Cash App : 5.5M reviews with 4.8/5.0 stars.

- Afterpay : 736K reviews with 4.9/5.0 stars.

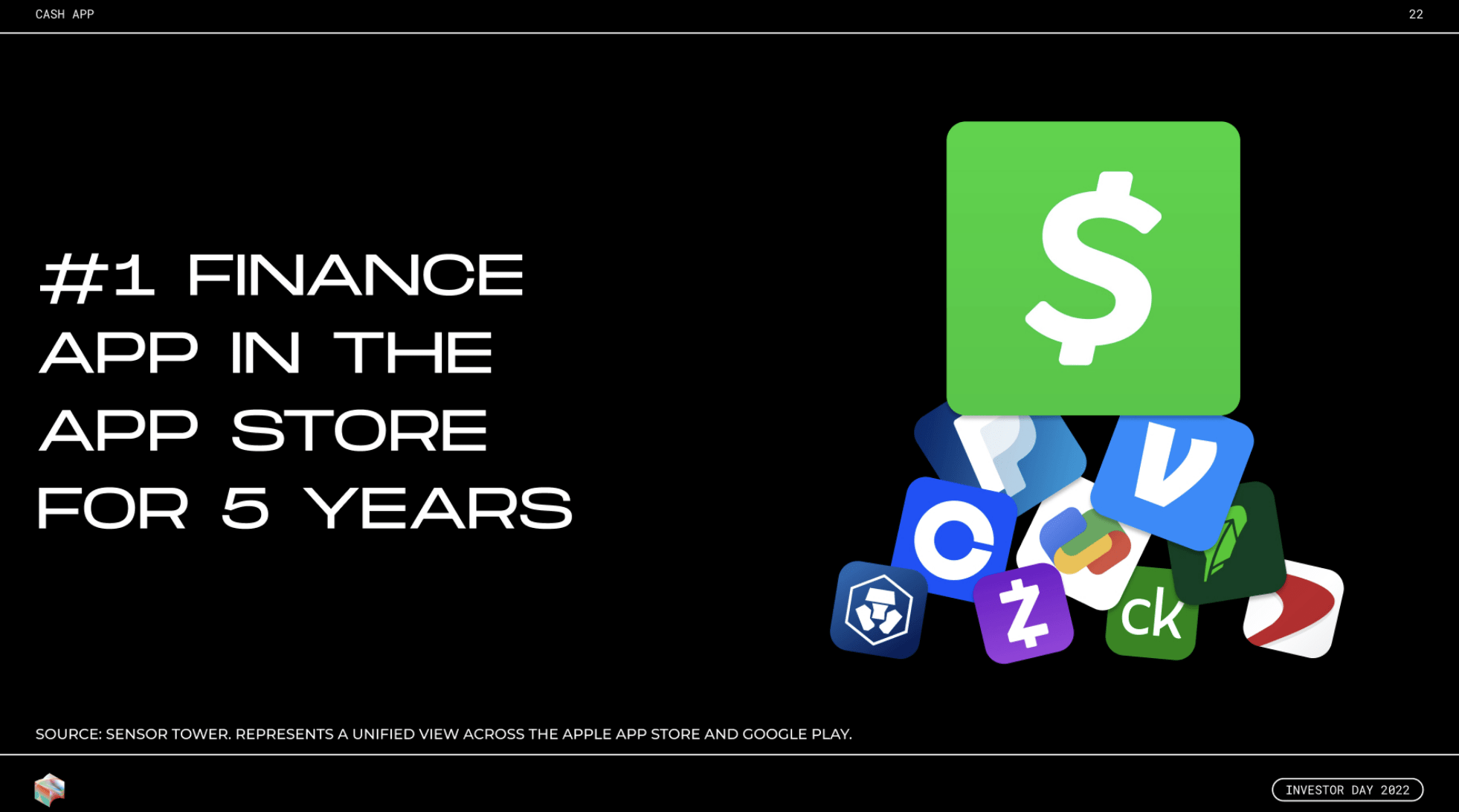

Cash App is also the #1 Finance App in the App Store for 5 years running, beating other well-known apps such as PayPal, Venmo, and Robinhood ( HOOD ).

{kind=link}

According to Gartner, Square is also regarded as the #1 Retail POS solution . The company's annual report also mentioned that Square has a net promoter score of 61 , which is more than double the average score for banking providers.

{kind=link}

In addition, Afterpay is a top three BNPL platform alongside Affirm ( AFRM ) and Klarna.

Without a doubt, Block possesses some of the strongest brands in the fintech space today.

Network Effects

Innovative financial products and strong brands enabled Block to attract a large and growing network of merchants and consumers.

- Square : 4M+ Sellers.

- Cash App : 54M Monthly Active Users.

- Afterpay : 144K+ Active Sellers and 20M+ Active Consumers.

Cash App is the fastest-growing app among the three as peer-to-peer transactions have powerful network effects whenever a consumer sends or requests money.

With the Afterpay integration, management hopes to connect the Square and Cash App ecosystems together, which could lead to powerful network effects as Block could gain incremental processing fees and cross-sell financial products at minimal cost.

For example, Cash App may offer users exclusive discounts when they transact with a Square-powered merchant, which encourages them to deposit even more money in Cash App. As you can tell, the money flows within Block's ecosystem of ecosystems, which maximizes revenue potential for the company. At the same time, cross-selling products like the Cash App debit card or Afterpay's BNPL offering becomes easier.

As more sellers and consumers join any of the three core Block apps, more money flows into the ecosystem and ultimately the higher payment volume the ecosystem processes. Combined with the social aspects of Cash App, the network effect gets even stronger.

{kind=link}

Switching Costs

Block's platforms have strong brands and huge networks, why would sellers or consumers leave the ecosystem?

Sellers already get a taste of Square's best-in-class POS solutions and payment processing capabilities, and now, they have greater reach due to Afterpay. As sellers utilize more of Square's offerings (i.e. using tools such as Square Invoices, Square Marketing, and Square Gift Cards), the more embedded they are in the Square ecosystem, thus leading to higher retention rates for Square as well as higher switching costs for these sellers.

Outside of pricing, I don't see any other reason for merchants to switch to another provider, which could mean a downgrade in terms of functionality and features.

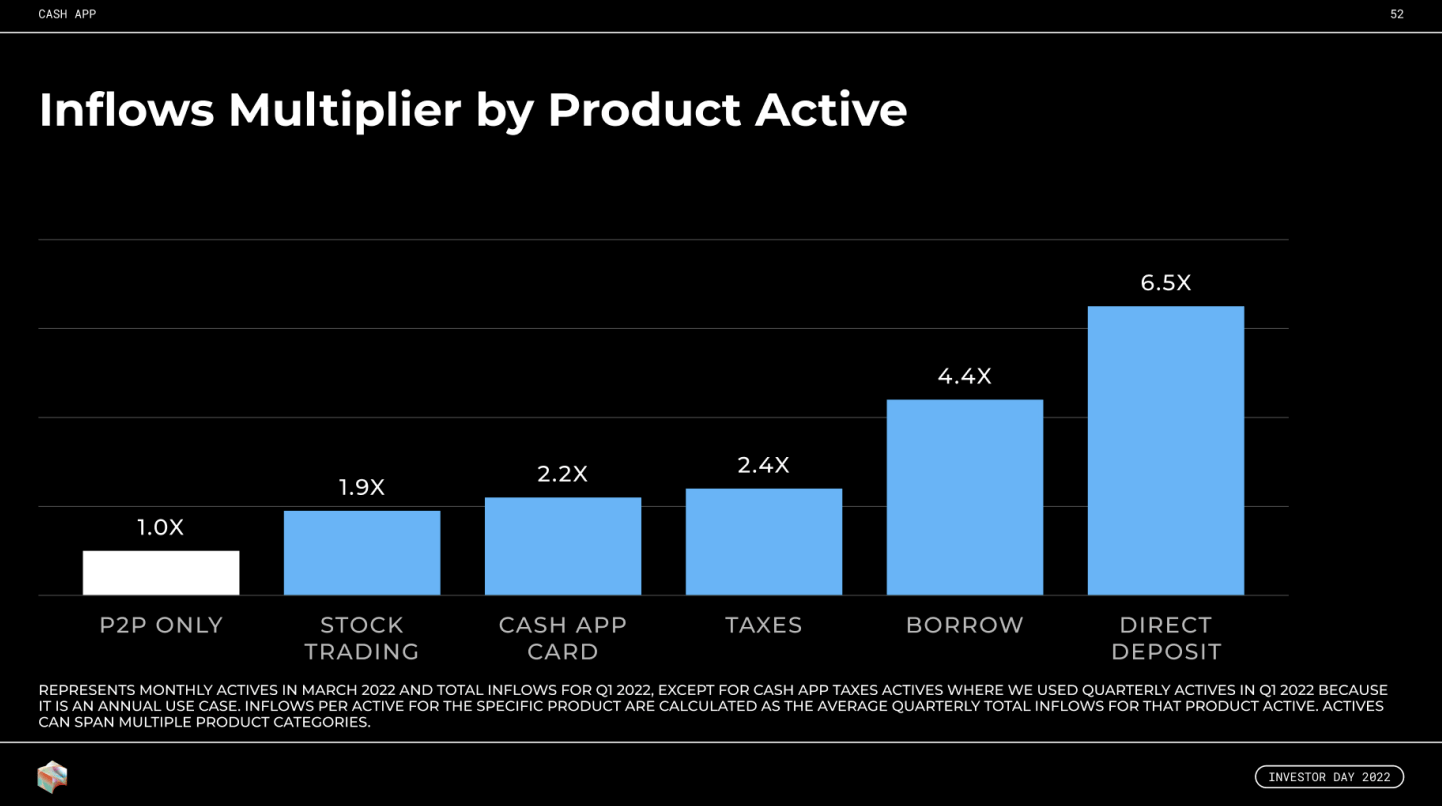

On the other hand, Cash App continues to introduce new offerings which lead to increasing inflows than P2P alone. In other words, as consumers use more products, the more funds they "invest" into the platform, which increases the stickiness of the platform.

{kind=link}

At the same time, the larger the network for a given user, the more likely that user stays on the platform. For instance, when a Cash App user has a network of 4 or more users, retention rates increase by at least 31 percentage points . In addition, it would be difficult for users to switch to another platform that their friends and families may not be using.

Growth

Let's now look at the company's financials.

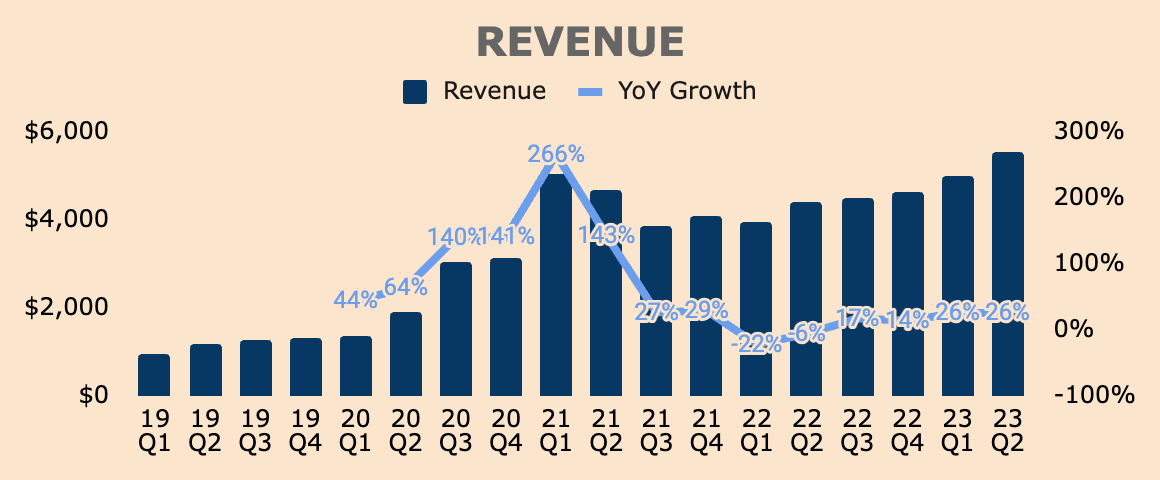

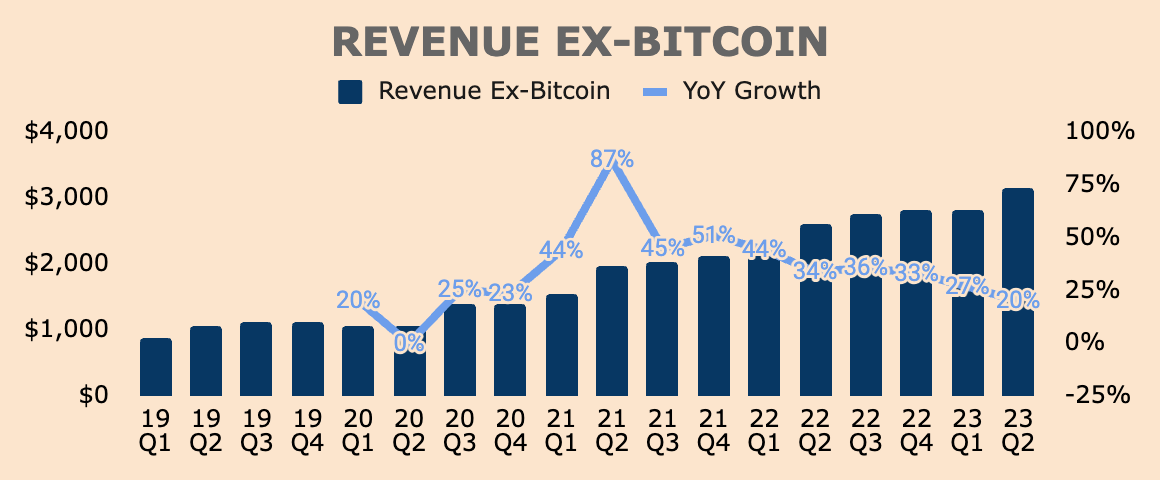

Q2 Revenue was $5.5B, up 26% YoY. This figure includes Bitcoin Revenue, which was $2.4B, up 34% YoY.

Keep in mind that Block recognizes the aggregate value of Bitcoin purchased by customers as Revenue, which is directly correlated to the market price of Bitcoin - this is one particular area that I don't like about Block's accounting since Bitcoin Revenue is volatile, unpredictable, and low-margin.

As you can see, Revenue growth has been volatile in the last few years largely due to the rise and drop in the value of Bitcoin in that time period.

{kind=link}

As such, removing Bitcoin out of the Revenue equation paints a clearer picture of the underlying performance of Block's ecosystem.

That said, Revenue Ex-Bitcoin in Q2 was $3.1B, up 20% YoY.

- Transaction-based Revenue was $1.6B, up 11% YoY, due to higher Gross Payment Volume ((GPV)) processed by Block, which was $59B in Q2, up 12% YoY.

- Subscription and Services-based Revenue was $1.5B, up 33% YoY, driven by Cash App and Afterpay.

As you can see growth has slowed down steadily over the last few quarters, likely due to the law of large numbers as well as weakening macro environment.

{kind=link}

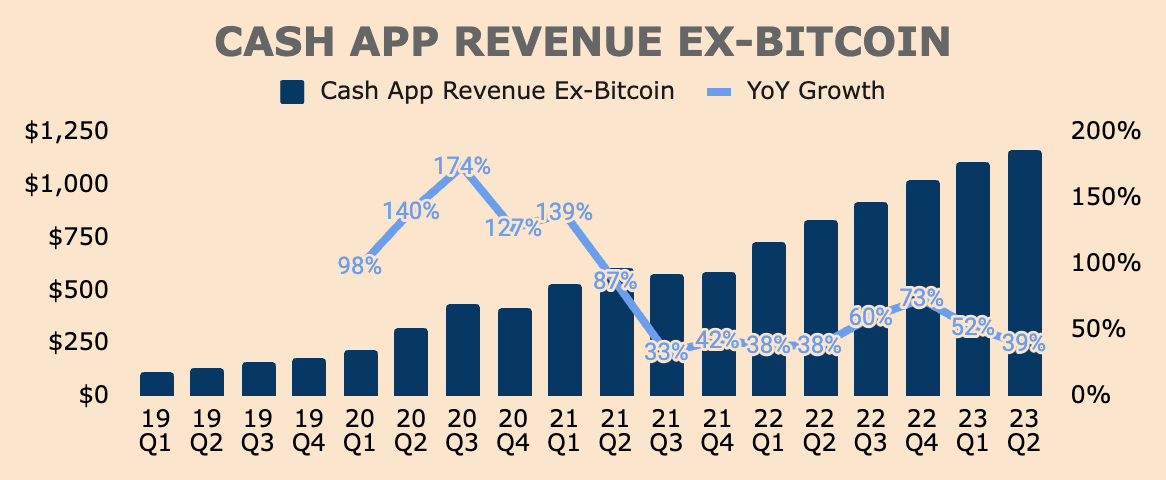

Let's take a closer look at growth by ecosystem. Keep in mind that the financial results from Afterpay have been distributed equally to the Cash App and Square segments.

That said, in Q2, Cash App Revenue was $3.6B and Cash App Revenue Ex-Bitcoin was $1.2B, up 36% and 39% YoY, respectively.

{kind=link}

Growth in Cash App was due to:

- Inflows of $62B, up 25% YoY.

- Cash App Business GPV of $4.9B, up 15% YoY.

- Monetization rates of 1.44%, up 16 basis points YoY.

Cash App Subscription and Services-based Revenue growth remained strong, increasing 43% YoY to just over $1B. This indicates that customers are using more of Cash App's financial services products such as Instant Deposit and Cash App Card, which means improved monetization and retention.

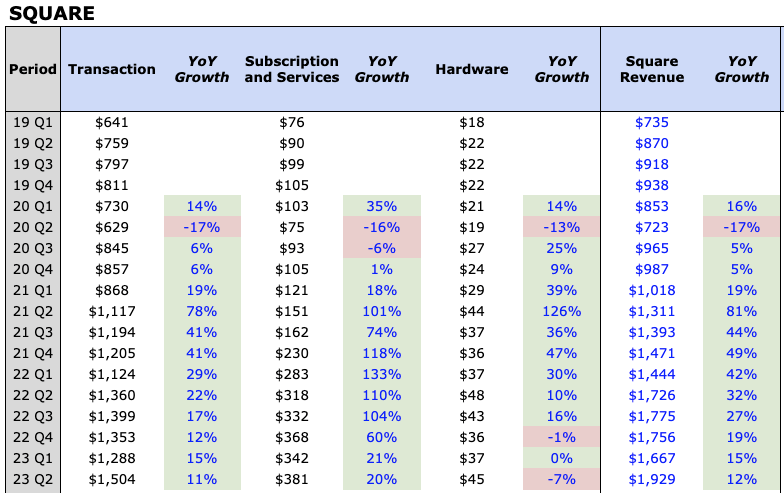

On the other hand, the Square ecosystem generated $1.9B of Revenue in Q2, up 12% YoY - a record for the segment.

{kind=link}

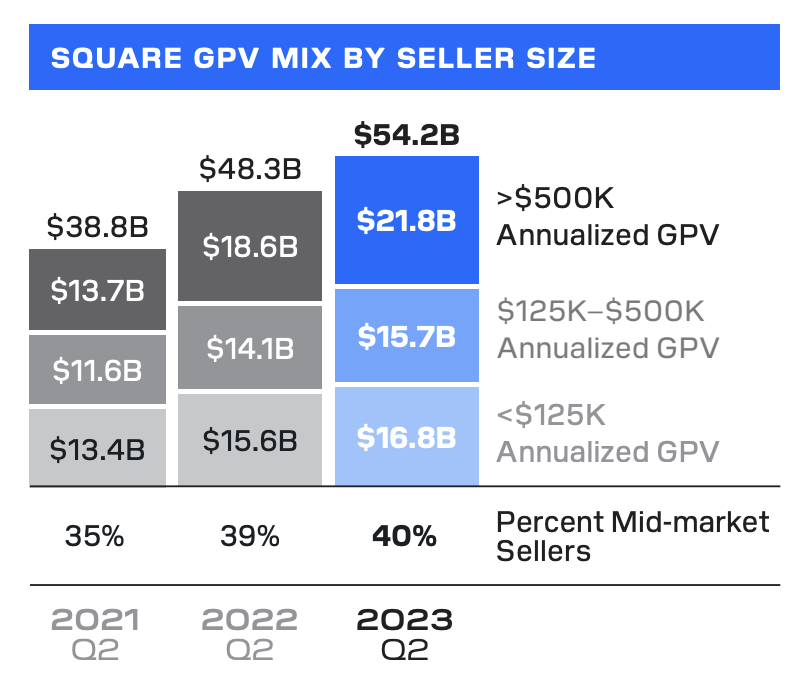

Growth was primarily due to Square GPV of $54B, up 12% YoY, with the international market growing 26% YoY, outpacing the US market's growth of 10% YoY.

As you can see above, both Transaction-based and Subscription and Services-based Revenue are slowing down significantly. If we look at Square GPV by seller size, we can see that the smaller sellers (<$125K Annualized GPV) are dragging the segment down, growing only 8% YoY. It's no surprise that the smaller sellers are under more pressure than their larger counterparts since they are more vulnerable to rising interest rates and high inflation.

Block FY2023 Q2 Shareholder Letter

{kind=link}

Nevertheless, the slowdown is concerning, which is probably why Square CEO Alyssa Henry left the company after 9+ years - Block Head Jack Dorsey will take over her role.

Regardless, Block continues to exhibit strong growth in a tough macro environment. While Square seems to be struggling, Square should maintain steady growth over the next few years as the company continues to dominate in POS technology, as well as benefit from the growth of modern payment processing.

In addition, Cash App is still growing rapidly as digital banking and wallet adoption continues to increase with each passing day.

With the integration of Afterpay, Block's ecosystem of ecosystems should unlock immense value as consumers and merchants engage and transact in Block's all-in-one, closed-loop payments network.

Profitability

In terms of profitability analysis, I'll do things differently. I'm going to show you Block's margins on a GAAP basis as well as margins excluding Bitcoin Revenue and Cost of Revenue as if the company does not offer Bitcoin trading on Cash App.

For instance, Gross Margin Ex-Bitcoin would be equal to Gross Profit Ex-Bitcoin divided by Revenue Ex-Bitcoin. This way we can truly see whether profitability is improving or not, without the volatile impacts of Bitcoin Revenue. As such, I will be focusing my attention on Ex-Bitcoin metrics.

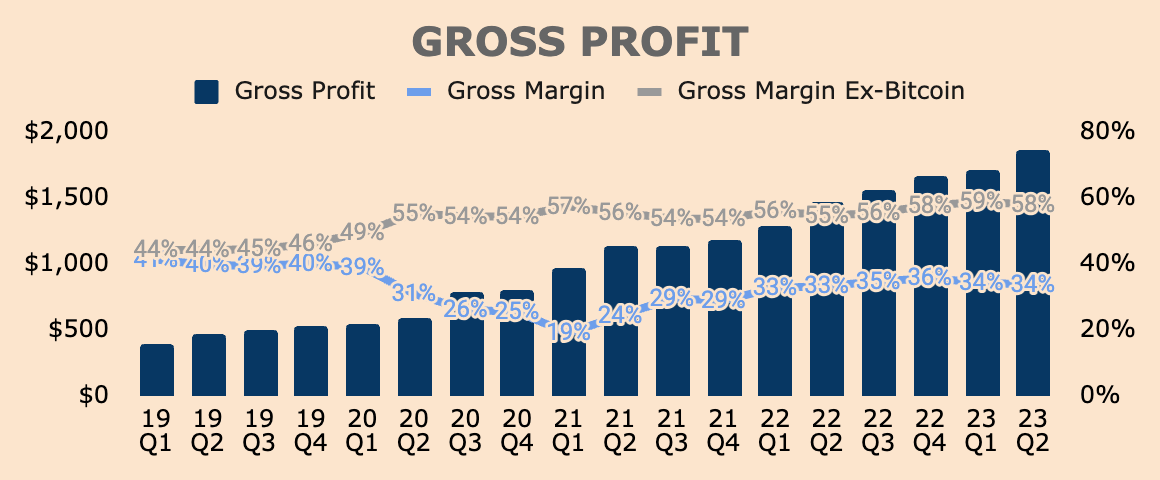

That said, Q2 Gross Profit was $1.9B, growing 27% YoY. This represents a 34% Gross Margin.

On the other side, Gross Profit Ex-Bitcoin was $1.8B, growing 28% YoY. This represents a Gross Margin Ex-Bitcoin of 58%.

As you can see, Gross Margin Ex-Bitcoin has been steadily improving over the last few quarters, which shows economies of scale within the business. If you focus solely on GAAP Gross Margins, you wouldn't be able to make the same conclusion.

{kind=link}

Gross Profit Ex-Bitcoin actually grew faster than Revenue Ex-Bitcoin (28% vs 20%) and this is due to two reasons.

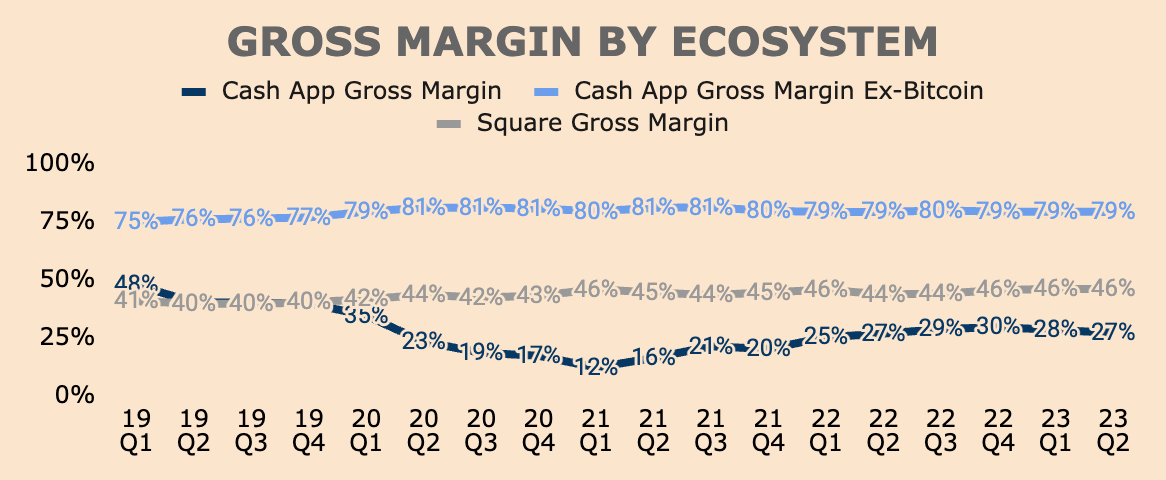

First, Cash App Revenue Ex-Bitcoin is growing faster than Square Revenue (39% vs 12%), contributing to Gross Margin Expansion. As you can see below, Cash App Gross Margin Ex-Bitcoin was 79% in Q2, which is much higher than Square's Gross Margin of 46%.

{kind=link}

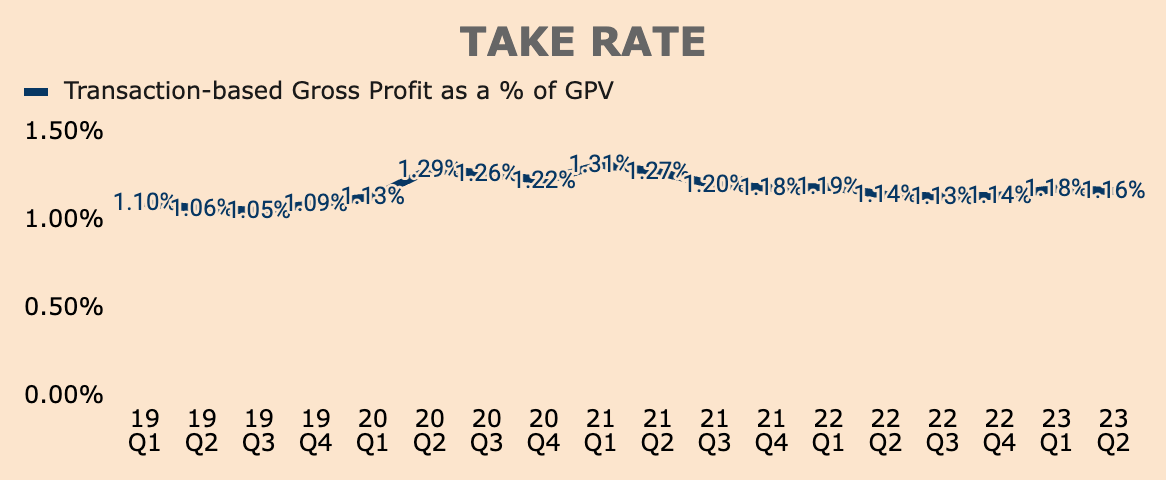

Second, Square also saw improved monetization as shown by the increase in Square Gross Margin as well as Transaction-based Gross Profit as a % of GPV - or Block's take rate.

{kind=link}

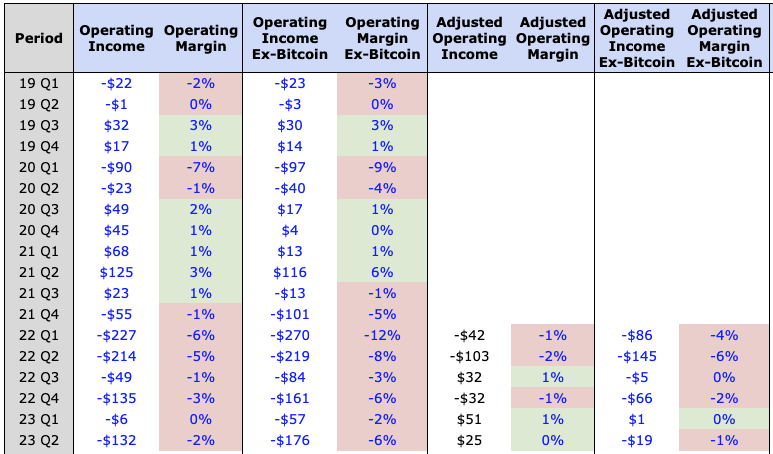

Moving on, Q2 Operating Income was $(132)M, which represents a (2)% Operating Margin.

Q2 Adjusted Operating Income was $25M, which excludes extraordinary items such as acquisition-related expenses, bitcoin impairment losses, and amortization. Do note that Adjusted Operating Income still includes Stock-based Compensation.

Regardless, the trend in operating profitability is pretty mixed as Operating Income improved YoY but declined QoQ. Hopefully, the company can return to GAAP operating profitability again soon.

{kind=link}

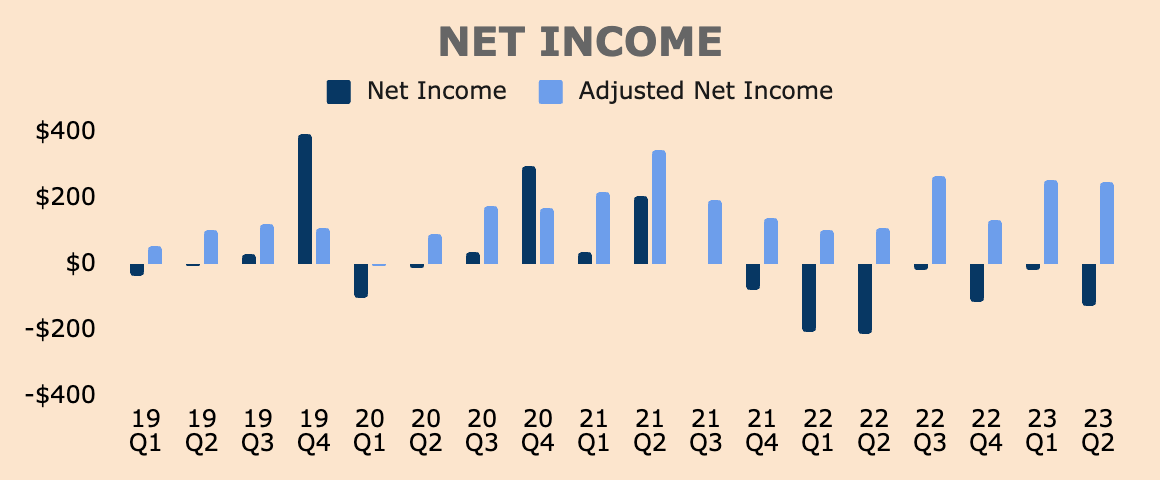

Finally, Q2 Net Income was $(126)M. Not much to talk about here but Block is still unprofitable on a GAAP basis, largely due to moderate SBC of $319M, which is about 10% of Revenue Ex-Bitcoin. Adding SBC and other non-cash and extraordinary items would yield an Adjusted Net Income of $247M in Q2.

{kind=link}

That said, Block seems to be gaining economies of scale as seen from the increasing Gross Margin Ex-Bitcoin. On the flip side, the company has yet to display operating leverage as Operating Income metrics remain negative and are showing little improvement.

In any case, GAAP profitability could be a major catalyst for the stock.

Health

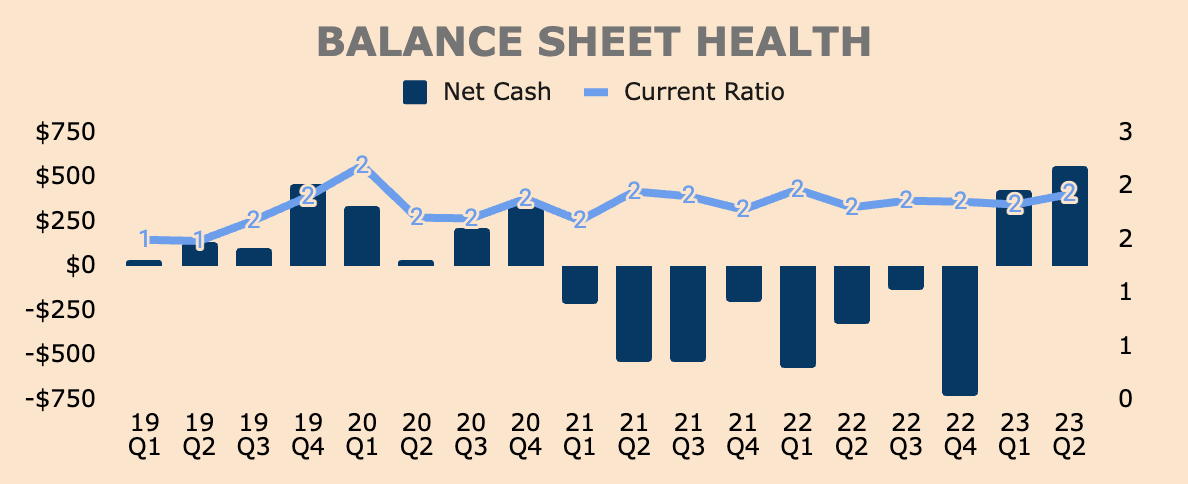

Turning to the balance sheet, Block has $5.9B of Cash and Short-term Investments with $5.3B of Total Debt, placing its Net Cash position to be about $0.6B as of Q2.

As you can see below, Block's Net Cash has been improving over the last few quarters as the company has been deleveraging its balance sheet, which is smart given the macro situation today.

{kind=link}

In terms of cash flow, Block produced $84M of Free Cash Flow in Q2. In the last twelve months, Free Cash Flow was $322M which is only a 3% FCF Margin against Revenue Ex-Bitcoin. Although not impressive, at least Block is not burning cash.

{kind=link}

Despite the cratering stock price, I don't see management announcing a share buyback program anytime soon - Net Cash is only $0.6B and the company is barely FCF positive.

Nevertheless, I would love to see FCF improve as the company scales further.

Outlook

In terms of outlook, management provided the following guidance.

Block FY2023 Q2 Shareholder Letter

{kind=link}

Management expects July 2023 Gross Profit to grow 21% YoY, which is quite a deceleration from Q2's growth of 27%. Split between the two ecosystems:

- Square Gross Profit to grow 15% YoY in July

- Cash App Gross Profit to grow 27% YoY in July

Management also added that Gross Profit growth is expected "to be relatively consistent through the third quarter" which is another way of saying that Q3 Gross Profit is expected to grow by 21% YoY.

Disappointing.

During the earnings call, management explained the reason for the slowdown:

The moderation in Gross Profit growth from the second quarter is primarily due to transaction margin compression as we lapse certain benefits from more favorable interchange economics last year .

(CFO Amrita Ahuja - Block FY2023 Q2 Earnings Call )

On the bright side, management raised their 2023 outlook on both Adjusted EBITDA and Adjusted Operating Income, by $140M for each figure. This reflects the company's "Gross Profit momentum" in Q2 as well as "expense discipline" in the first half of the year.

Block FY2023 Q2 Shareholder Letter

{kind=link}

With that in mind, the improved profitability guidance was still overshadowed by the slowing Gross Profit growth, which is probably why the stock tanked right after Q2 earnings results.

Whatever it is, Block still has a long growth runway ahead as digital wallet adoption increases and modern payment processing grows. According to Block, the company continues to expand its total addressable market ((TAM)) as it introduces more financial products and services into its ecosystem - Cash App and Square have a combined TAM of $190B.

{kind=link}

For one, US Retail Ecommerce Sales are expected to continue to grow to $1.6T by 2026, making up 20% of total retail sales. This should be a major tailwind for Square.

Insider Intelligence

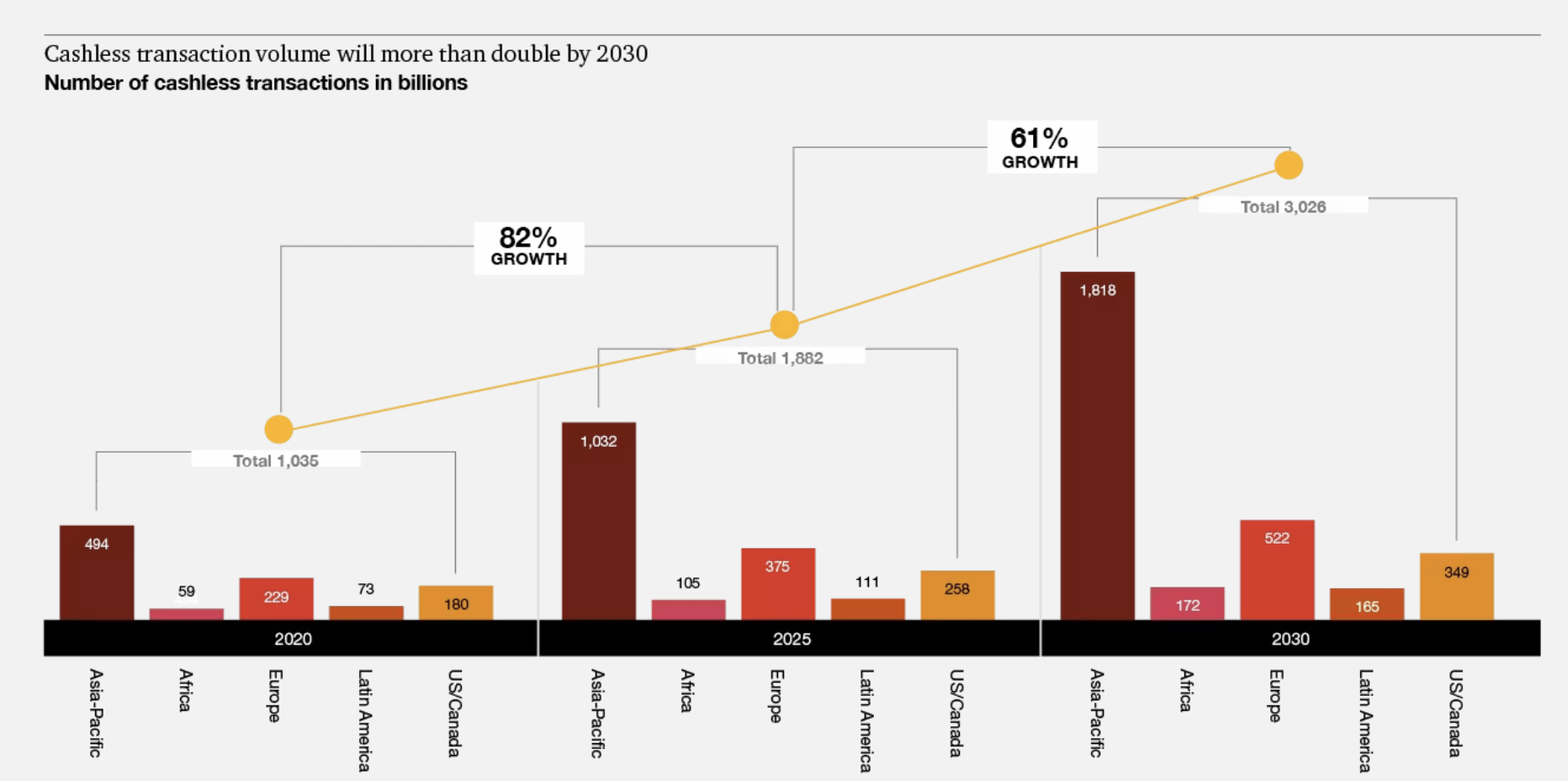

Furthermore, Cashless Transaction Volume is expected to increase by 200%+ from 1T transactions in 2020 to 3T transactions by 2030. This should boost the Cash App business, especially with its recent expansion of Cash App Pay.

{kind=link}

In dollars, Ark Invest estimated that global digital wallet TPV could surpass $40T by 2030. In addition, closed-loop transactions could account for more than 50% of digital wallet payments by 2030. Given Block's closed-loop ecosystem of ecosystems, Block stands to benefit immensely from this financial megatrend.

{kind=link}

Valuation

Since its August 2021 peak, Block stock has lost 80%+ of its value. The stock currently trades at just $46 a share, very close to its March 2020 lows of $32.

In other words, Block stock is back to square one (pun intended).

Today, the stock trades at just 3.8x EV to Gross Profit, its lowest multiple ever since the company went public, despite being a much larger and more profitable company.

{kind=link}

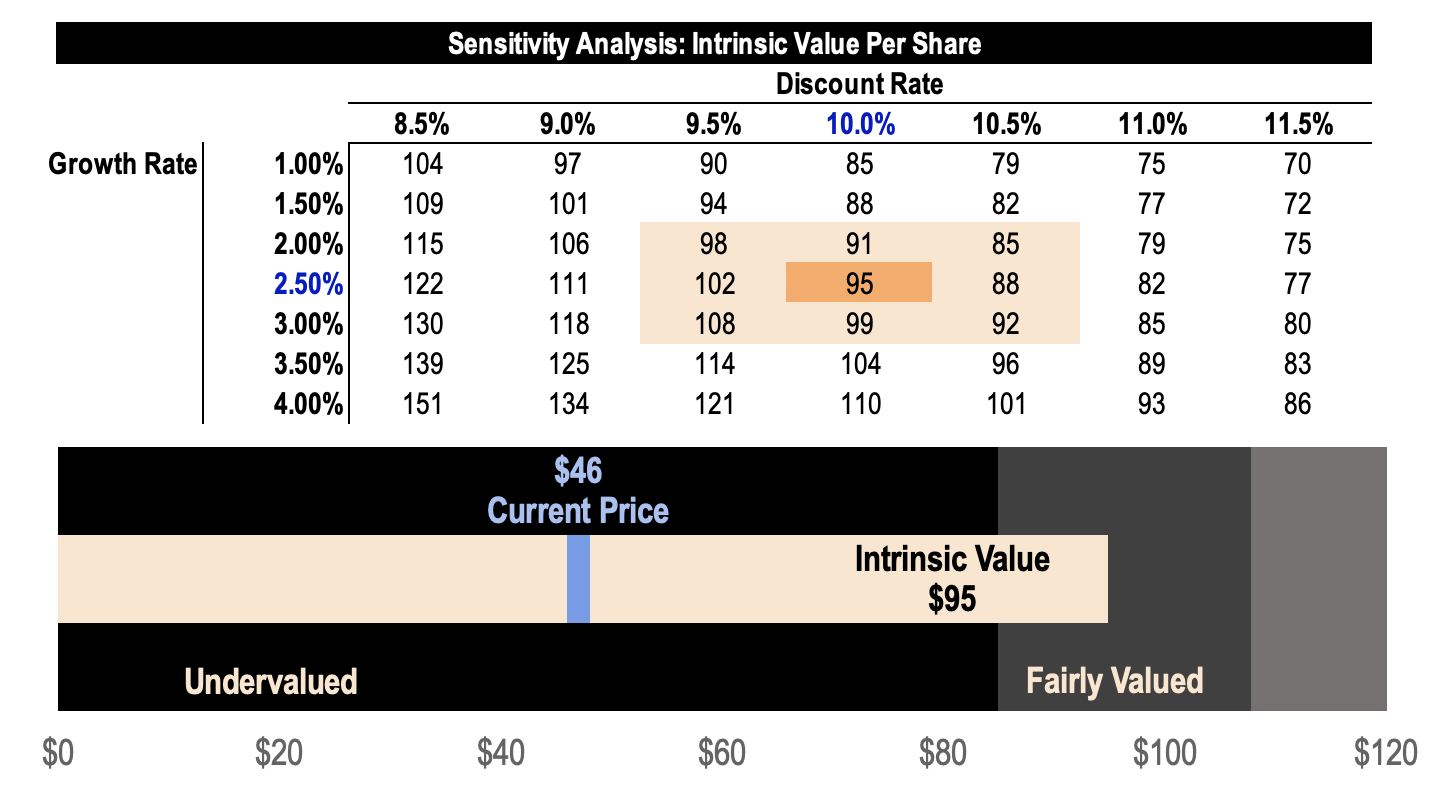

Let's take a look at my DCF model.

Again, I'm going to remove Bitcoin Revenue out of my projections. That said, here are my key assumptions:

- Revenue Growth Ex-Bitcoin : I'm assigning a conservative 20% growth in 2023 and then growth continues to slow down to just 10% by 2028 and beyond.

- Gross Margin Ex-Bitcoin : I expect margins to continue to improve due to the outsized growth of Cash App. As such, I expect Gross Margin Ex-Bitcoin to reach 60% by 2026 and beyond, up from 56% in 2022.

- Operating Margin Ex-Bitcoin : I also expect the company to gain operating leverage as it scales, expanding Operating Margins to 15% by 2028 and beyond.

{kind=link}

Based on all these assumptions, I arrive at a $35B Revenue Ex-Bitcoin by 2032, at a FCF Margin of about 17.6%.

{kind=link}

Using a discount rate of 10% and a perpetual growth rate of 2.5%, I arrive at a fair value estimate of $95 a share for Block, which is more than double the current price of $46.

As a reminder, this valuation does not include Bitcoin and the company's other crypto projects, which could unlock massive value if crypto and decentralized finance gain mass adoption.

{kind=link}

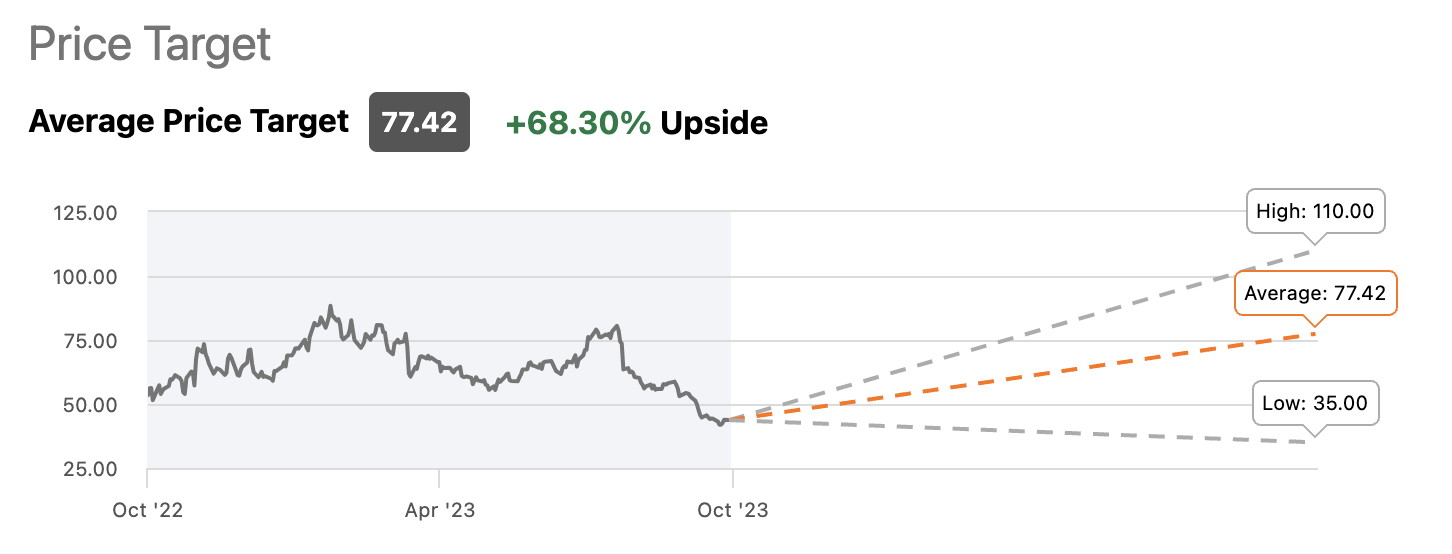

This is also higher than the average analyst price target of $77 a share. Notice that the lowest price target is $35 which is conveniently placed at the March 2020 lows.

{kind=link}

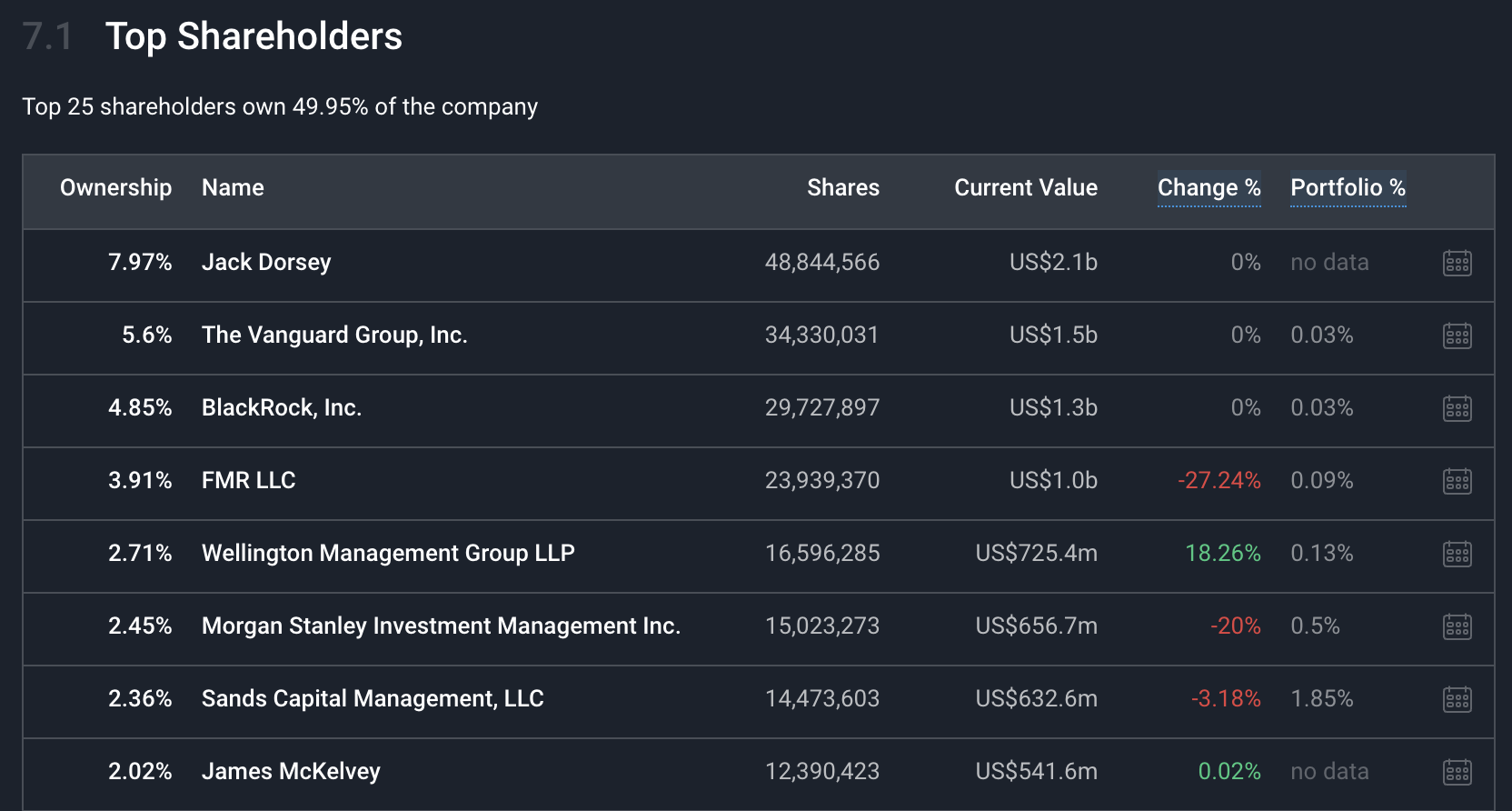

"Smart money" is piling into Block stock as well.

Fintel

More importantly, Block is still founder-led by Jack Dorsey, who by the way, is the largest shareholder - he owns ~8% of the company. It is also important to note that Jack Dorsey receives basically no compensation and no performance awards as CEO of the company (okay, I lied. He gets $2.75 in annual salary).

This means that the only way for him to get paid is to drive Block's stock price higher. The bad news is that Jack Dorsey has no salary in his pocket to buy shares of his company, which I think could be another major catalyst for the stock.

Nevertheless, Jack Dorsey has skin in the game and his financial incentives are very much aligned with long-term shareholders.

{kind=link}

That aside, the stock is back to square one, trading at its lowest valuation multiple and near major support at $35, which could signify a bottom for Block stock.

Risks

Competition

The biggest risk for Block is competition.

In its H1 update, Adyen mentioned price competition as one of the major reasons for the company's slowdown, sending the stock diving 30%+ after H1 earnings. Clearly, investors are concerned about a potential price war, which could negatively affect Square as well.

The eventual commoditization of payment processing services is a major thesis buster for investors and we're already seeing it happen in real time. As you can see, take rates among the big three fintech processors are all compressing.

If the trend continues, payment processors, including Block, could be in big trouble.

Author's Analysis

Not only that, but Cash App also faces tough competition from other digital wallet and banking solutions such as SoFi, Venmo, Zelle, Chime, Apple Pay, and more, which could limit Cash App's growth.

Afterpay Acquisition

Let's be real. Block overpaid for Afterpay, so much so that the $29B acquisition price tag is now larger than Block's market cap of $28B as of this writing. That's a serious case of shareholder value destruction.

The Afterpay Acquisition also brought in two additional risks:

- Failed synergies : the Afterpay integration into Square and Cash App may not bring the desired network effects that management is looking for. In other words, few people cross the Afterpay bridge, and thus, the Square and Cash App ecosystem continues to be siloed.

- Loan losses : Afterpay is a BNPL platform, which holds a substantial amount of loans in its balance sheet. This exposes Block to the risk of rising delinquencies and loan losses.

Bitcoin Proxy

Because of Block's accounting method, a large chunk of the company's Total Revenue consists of Bitcoin Revenue. If the price of Bitcoin craters, Block's overall Revenue will be dragged down as well, which may not look good for investors.

Thesis

To wrap up, Block is building an all-in-one financial ecosystem consisting of a best-in-class payments processing platform as well as a consumer-facing digital banking app, connected together through a BNPL marketplace.

Block's ecosystem of ecosystems possesses a strong brand, network effects, and switching costs moats, which should sustain further sales and earnings growth.

While growth has been slowing down, Block is at the forefront of multiple financial megatrends including e-commerce, digital wallets, and digital banking, which should drive growth and profits for years to come.

The company has a visionary leader, a growing ecosystem of ecosystems, and is also turning GAAP profitable.

Following its huge selloff back to its Covid lows, Block stock now trades at a wide margin of safety with substantial upside potential as it trades near a major support level. Perhaps, this could be the bottom for the stock.

The stock is back to square one, but the business is much larger, much stronger, and definitely much more capable of delivering its purpose of economic empowerment.

(While I'm bullish on SQ, I'm not buying the stock as I already have exposure to SQ through my investment in Marqeta ( MQ ), which powers the Cash App and Square Card).

For further details see:

Block: Back To 'Square' One