FDIG - Block: Bitcoin Bloodbath But Gross Profits Are Strong

- Block has two powerful ecosystems with its Cash App and Merchant Payments Business.

- The company announced solid results for Q2, with a 29% increase in Gross Profit.

- Overall, Block revenue declined, but this was mainly due to the "Bitcoin Winter."

- The Block stock price fell on poor guidance and is now undervalued intrinsically and relative to historic multiples.

Block, Inc. (SQ), formerly known as Square, is a leading Fintech company which has built two ecosystems of products, its Square Merchant services and its Cash App. The company's Cash App Revenue has been decimated by the decline in Bitcoin Price and the subsequent "Bitcoin Winter" in trading. However, its Gross Profit has still grown strong, which is more important. Over 47 million accounts transacted on its Cash App in June and the company noticed strong retention patterns between those accounts that were connected with four or more other accounts. This means the company has discovered how to enhance the true "Network Effects" of the cash app ecosystem and thus generate long term retention.

However, tepid guidance and the upcoming "recession" have spooked investors, and the stock price has now plummeted by ~7% in after-hours trading. Given these factors, the stock is undervalued intrinsically and relative to historic multiples. Thus, let's break down its latest earnings report for the juicy details.

Poor Revenue, Strong Gross Profit

Block generated mixed financials for the second quarter of 2022. Total net revenue was $4.4 billion, which was actually down 6% mainly driven by the continued decline in Bitcoin revenue. Without Bitcoin, net revenue popped to $2.62 billion, up a rapid 34% year over year. In previous posts on Block, I spoke in detail about the revenue risk from the volatility of Bitcoin. Now it seems my thesis is playing out, as since the price of Bitcoin has plummeted, most retail investors are reluctant to trade. The good news for Block is that Bitcoin has never been a major profit driver, as the company doesn't have large margins on Bitcoin transactions. Therefore gross profit was actually up 29% year over year and up 47% on a three year CAGR basis.

{kind=link}

Gross Payment Volume ((GPV)) increased to $52.5 billion in the second quarter of 2022. This represented an increase of 23% year over year which was ok, but slower than prior years. International markets grew GPV strong, increasing it by 45% year-over-year vs 22% for U.S. markets.

Gross Payment Volume (Q2 Earnings report)

{kind=link}

Block's acquisition of Buy Now Pay Later ("BNPL") provider Afterpay is now fully integrated and contributed to $208 million in revenue and $150 million in Gross Profit.

Overall transaction-based revenue was $1.48 billion in the second quarter of 2022, up 20% year over year, with transaction-based gross profit edging by 10% year-over-year to $600 million. However, Blocks subscription and services-based business was the key growth driver, with revenue of $1.09 billion up a blistering 60% year-over-year. Gross profit for the segment was $882 million, up a rapid 56% year over year.

Square Merchant Products (Investor Day Presentation)

{kind=link}

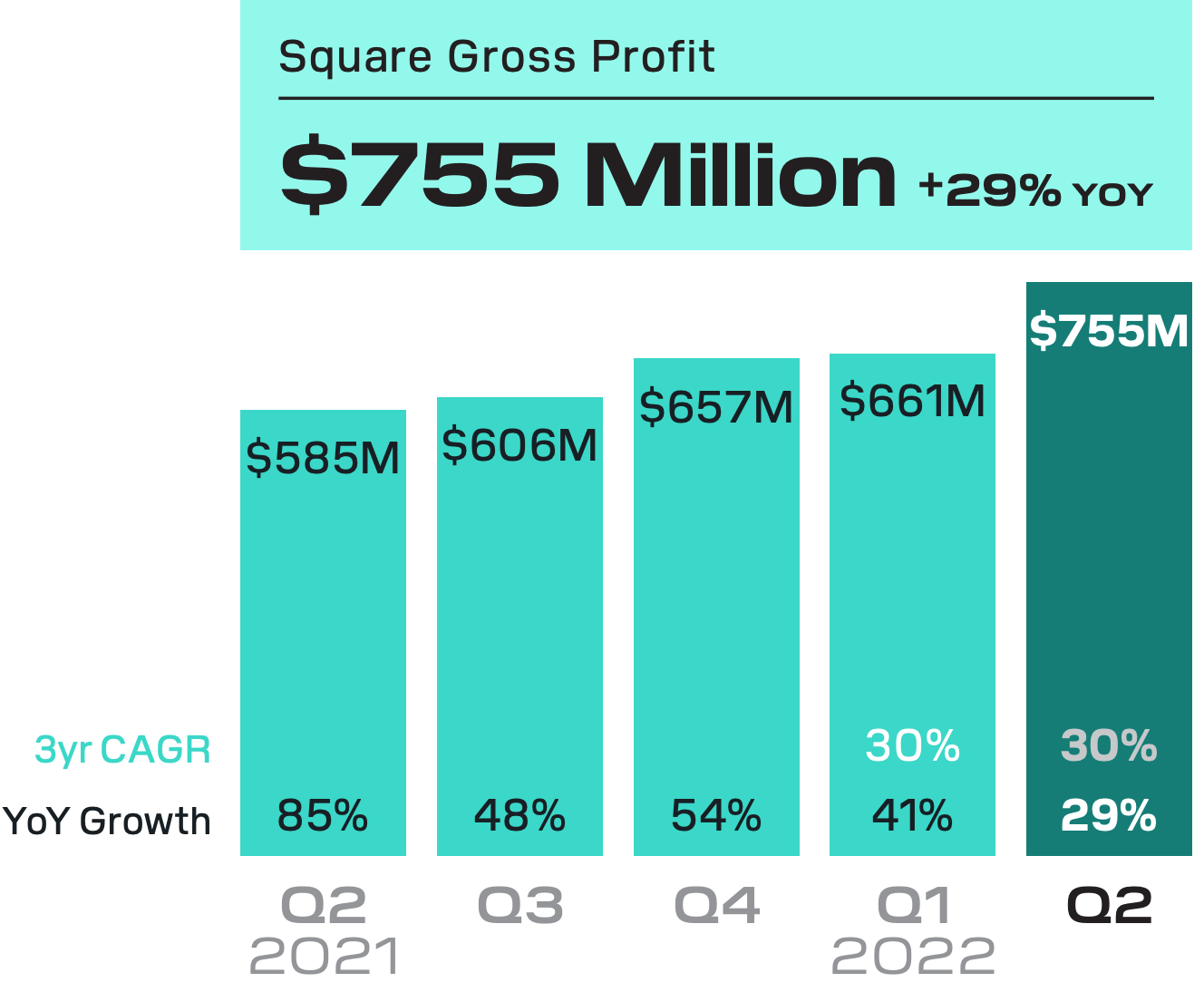

The merchant-focused side of Blocks business, "Square," generated $1.73 billion in revenue up a rapid 32% year over year. Gross profit also grew to $755 million, up 29% year over year. This growth was enhanced by strong subscription and services revenue, up a blistering 110% year over year, to $318 million. However, As "Square" makes the majority of its merchant revenue from transactions, this still makes up the majority of its $1.36 billion, which increased by 22% year over year. Interestingly, Square saw a lower percentage of debt card transactions, which started to "normalize" compared to pre-pandemic levels.

Block Gross Profit (Q2 Earnings Report)

{kind=link}

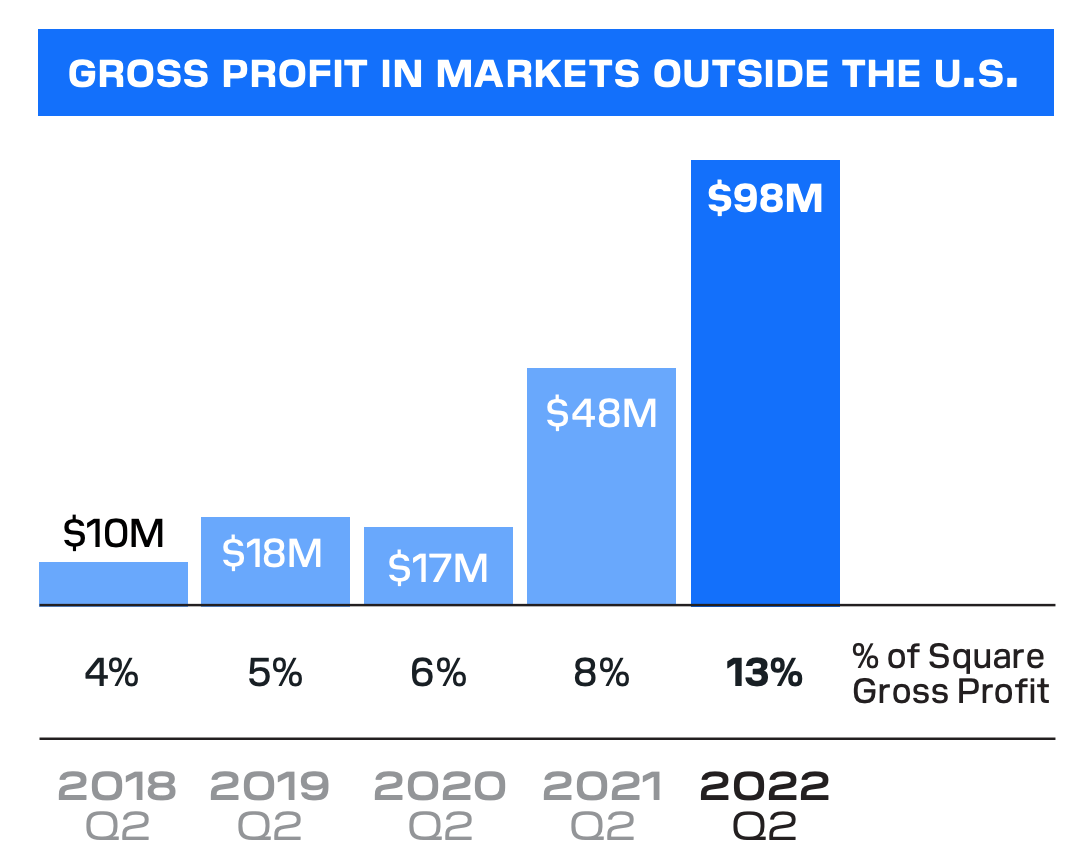

Block is executing well on its plans to expand internationally. The company launched 44 products across international markets in 2022, as they aim to enhance "product parity" across regions. For example, the Block launched Square Register in Ireland and France, in addition to Square Appointments in Japan and Instant Bank Transfers to enhance its Australian offering. These initiatives resulted in the percentage of Square's Gross Profit coming from outside of the U.S., jumping to 13% up from 8% in the prior quarter.

Square Gross Profit International (Q2 Earnings)

{kind=link}

Squares Software Subscriptions generated solid growth of 10% year over year to $48 million, while its Hardware Revenue (what the company makes from selling its Point of Sale terminals) increased by 10% year over year to $48 million. This was driven specifically from strong product growth of the "Square Register" and "Square Terminal."

Square Loans continued to grow strong, with loan originations jumping by 30% year over year to 122,000. This segment also benefited from $9 million of Paycheck Protection Program ((PPP)) loan support in the quarter.

Overall Profit and Loss

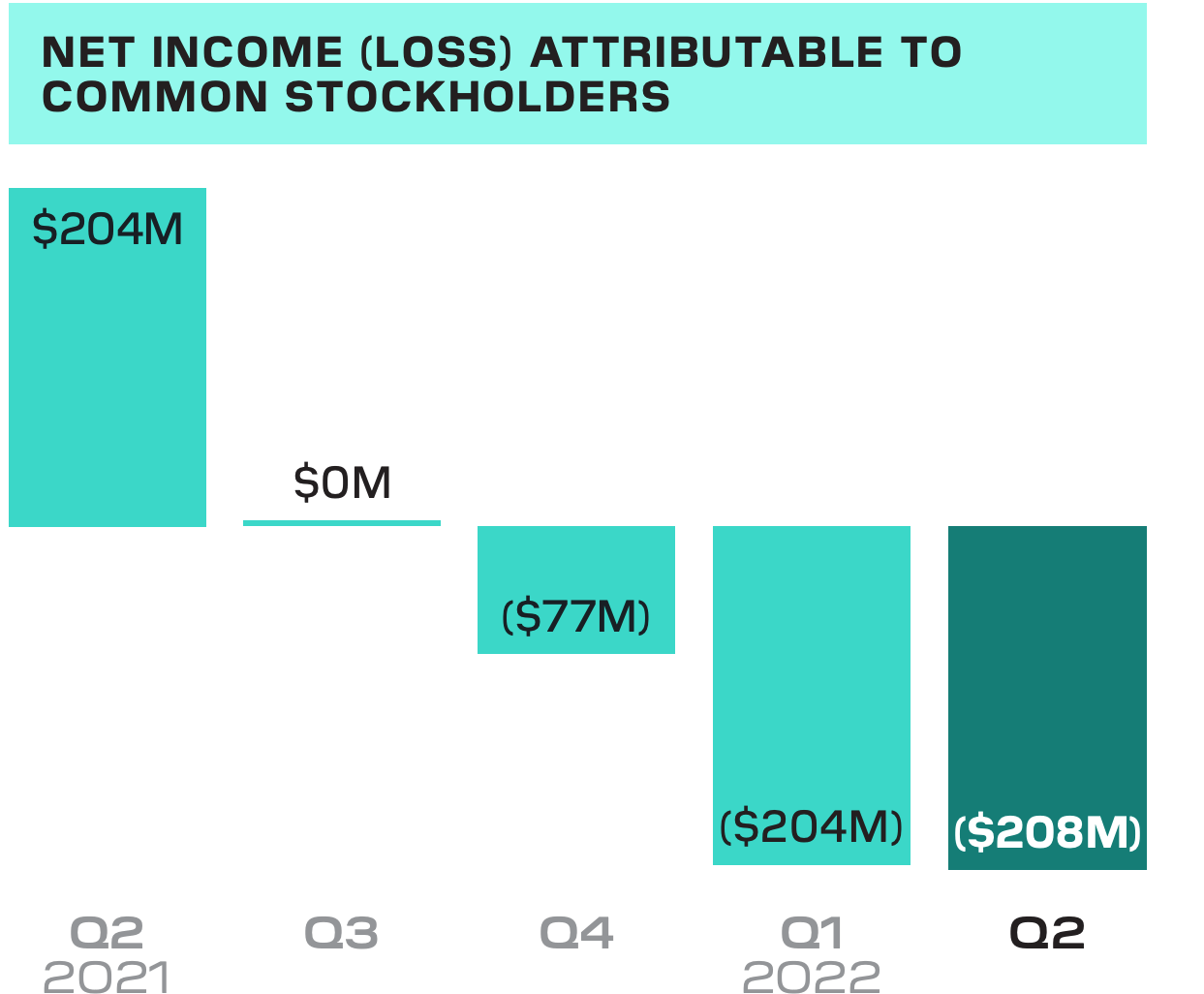

Bringing all the business segments together, Square generated a net loss of $208 million. This may not seem great, but it's good to keep in mind that $57 million of this was related to a $57 balance sheet adjustment of acquired intangible assets and $17 million in integration expenses. These were most likely related to the Afterpay acquisition. In addition, $36 million of this was related to a Bitcoin "impairment loss." Therefore, if we assume the prior items were "one off" expenses and exclude these items, Blocks net loss was $98 million.

Net Income Loss (Q2 Earnings report)

{kind=link}

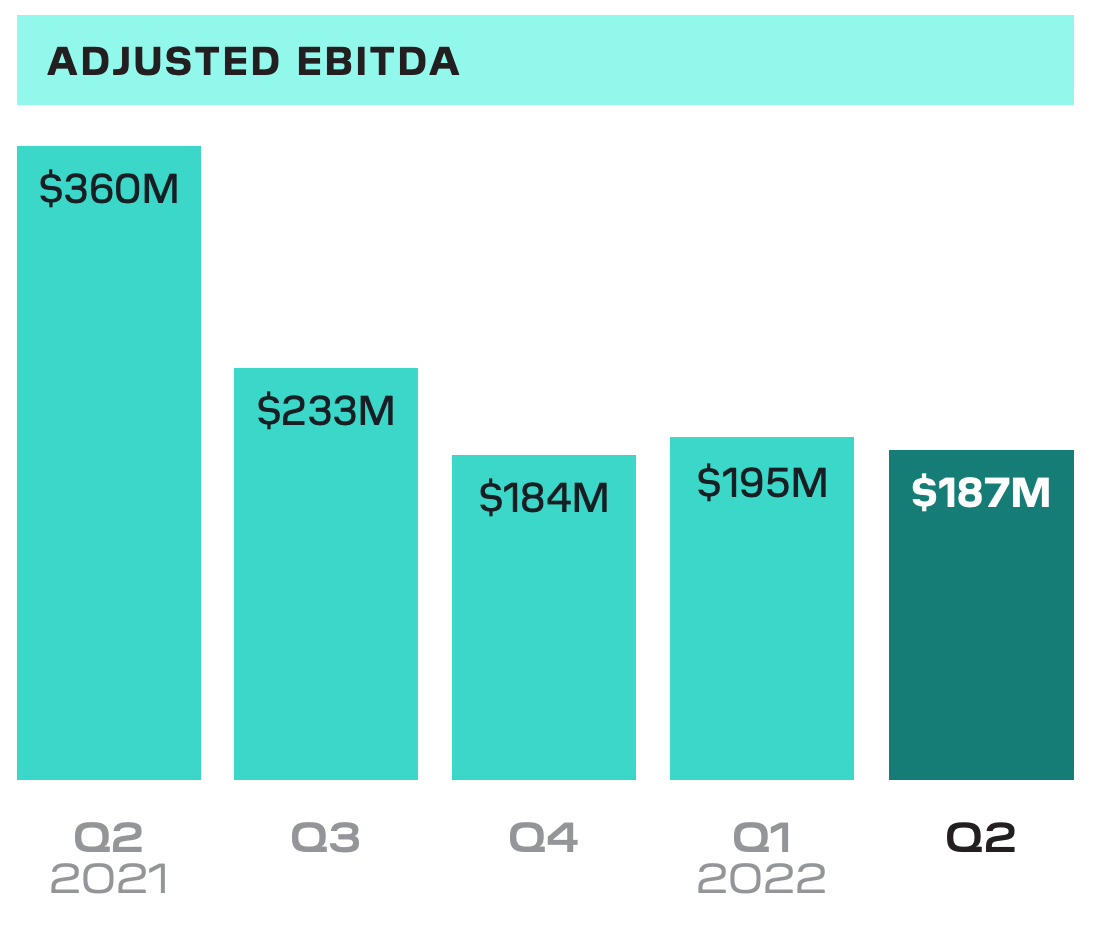

Blocks Adjusted EBITDA was $187 million in Q2/22, which was down from the $360 million produced in the second quarter of 2021. But, again, this was mainly due to higher operating expenses resulting from the Afterpay Acquisition and integrations.

Block EBIDTA (Q2 earnings report)

{kind=link}

Block has a solid balance sheet with $6.2 billion in cash, equivalents, restricted cash, and marketable debt securities, in addition to $600 million available from their revolving credit facility. Its total debt is fairly high at ~$5 billion, but I would deem this to be very manageable given the majority (~$4 billion) is long term debt.

Moving forward, management produced tepid guidance for the month of July. They forecast the growth rate in Gross Purchase Volume ((GPV)) to grow by 18% year over year, which is slower than the prior quarter rate.

Non-GAAP operating expenses are expected to increase by approximately $75 million compared to the second quarter of 2022. This includes costs across product development, sales and marketing, general and administrative expenses, and transaction, loan and consumer receivables losses. Thus, I imagine this muted guidance is why the stock actually declined by ~6% in after hours trading.

Advanced Valuation of Block

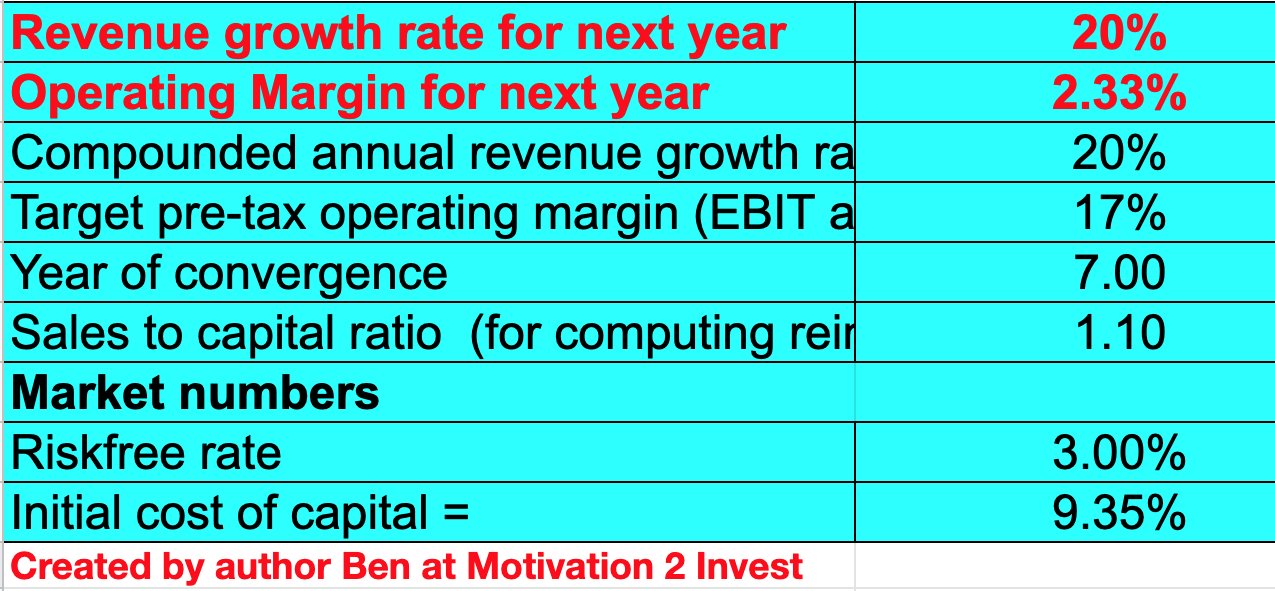

In order to value Block, I have plugged the latest financials into my advanced valuation model which uses the discounted cash flow ("DCF") method of valuation. I have optimistically forecasted revenue to grow by 20% over the next 2 to 5 years as the company continues to expand internationally and grow "upmarket" by targeting larger merchants such as with the 10 year SoFi Stadium partnership announced previously.

Block Stock Valuation (created by author Ben at Motivation 2 Invest)

{kind=link}

In addition, I have forecasted a 17% pre tax operating margin generated over the next 7 years as the company improves its marketing efficiencies and its "one-off expenses" start to become less common.

Block Stock Valuation 2 (created by author Ben at Motivation 2 Invest)

{kind=link}

Given these factors, I get a fair value for Block Stock of $110/share. The stock is currently trading at $89/share, and thus it is ~20% undervalued. As an extra datapoint, Block is trading at a Price to Sales Ratio = 2.6, which is approximately 66% cheaper than historic levels.

Risks

Consumer Spending Slowdown/Recession

As mentioned in my prior posts, high inflation squeezes the consumer with higher food and utility bill costs. The Fed is raising interest rates to firefight inflation. However, this squeezes the consumer with higher debt servicing costs. With less surplus income, consumers are likely to spend less. Block makes its revenue based on transaction volume, less volume equals less revenue. Although I believe this is only a temporary issue (until inflation subsides), it is a still a risk.

Final Thoughts

Block is a tremendous company which has built two diverse ecosystems of products with both its merchant services and cash app. The "Bitcoin Winter" has impacted Square's revenue, and continued volatility is expected moving forward. Despite this, Block's gross profit is still growing strong and they are executing well on their strategy to expand internationally and move upmarket. Thus, this stock could be a great long-term investment on the future of fintech. However, I would watch the technicals and wait for the stock to fall and hit support before entering.

For further details see:

Block: Bitcoin Bloodbath But Gross Profits Are Strong