PYPL - Block: Can Management Execute On A Good Plan?

2024-01-08 02:48:17 ET

Summary

- Block's transaction revenues have seen a sharp decline, attributed to a fall in gross payment volumes, which is geared toward consumer activity in the Retail sector.

- The macros indicate mixed signals for top-line growth acceleration recovery in gross payment volumes, with Consumer Sentiment rebounding well but Retail Sales data underwhelming expectations.

- Block's has a good plan to layoff 1000 employees and improve workforce efficiency. My calculations reveal that this can right-size their employee productivity metrics vs peers and boost margins meaningfully.

- However can Dorsey's decentralized, non-hands-on leadership style engender the required employee productivity changes? I believe some proof of execution is required to gain confidence on this catalyst.

- Given that context, Block's 22% premium 1-yr fwd PE valuations vs its peers leave little margin of safety.

Thesis

I think Block ( SQ ) has a good plan to right-size their cost structure and pursue growth. I am bullish but waiting for some proof of execution momentum before initiating any buys. My 'Neutral/Hold' stance is after consideration of these key points:

-

The macros point to mixed signals for top-line recovery

-

Block's cost-cutting program can make its workforce efficiency more in-line with peers

-

Block is trading at a moderate premium vs its peers

Understanding Block's Business Drivers

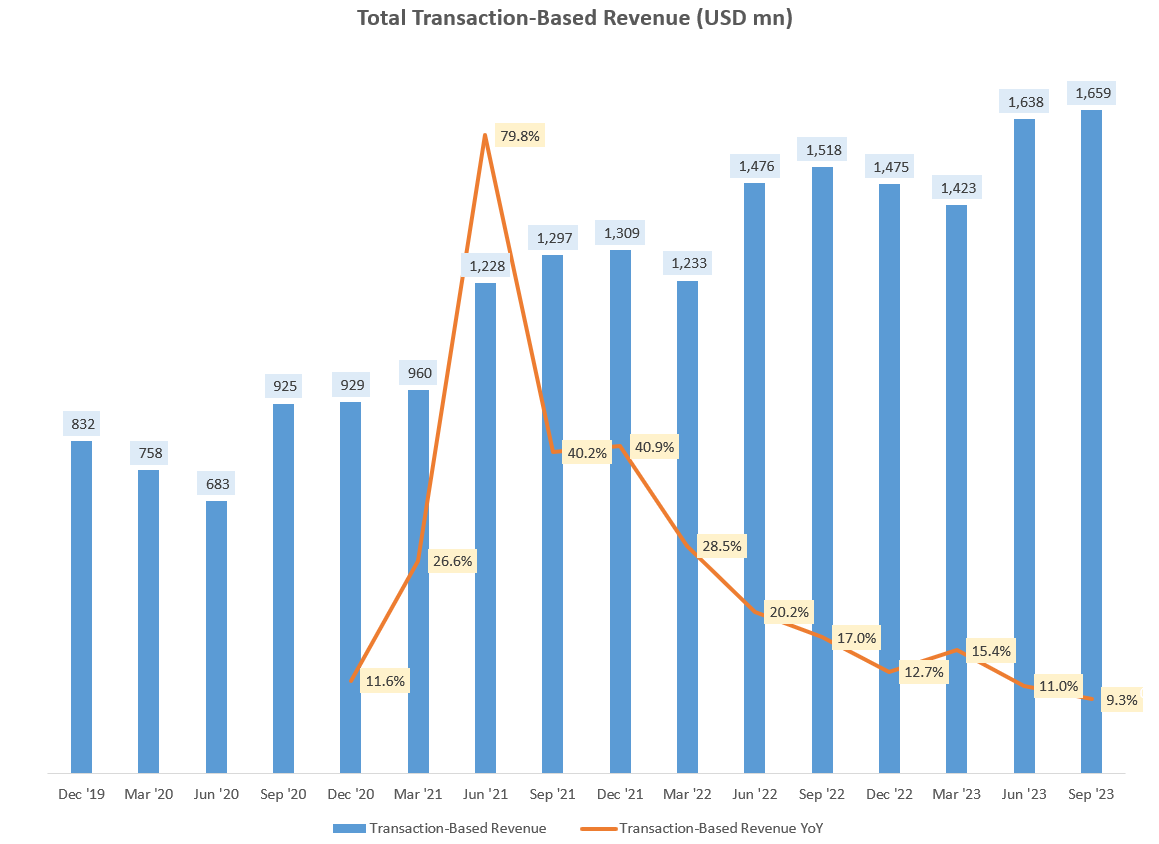

Total Transaction-Based Revenue (USD mn) (Company Filings, Author's Analysis)

{kind=link}

Block's transaction revenues have seen a sharp growth moderation from 40% YoY levels to sub-10% as of Q3 FY23 . Transaction revenue make up around 30% and 35% of the overall revenue and gross profit mix respectively. I would say it is the 2nd highest quality source of revenue after Subscription and Services (which is growing handsomely at a 25%+ YoY growth rate; no issues there).

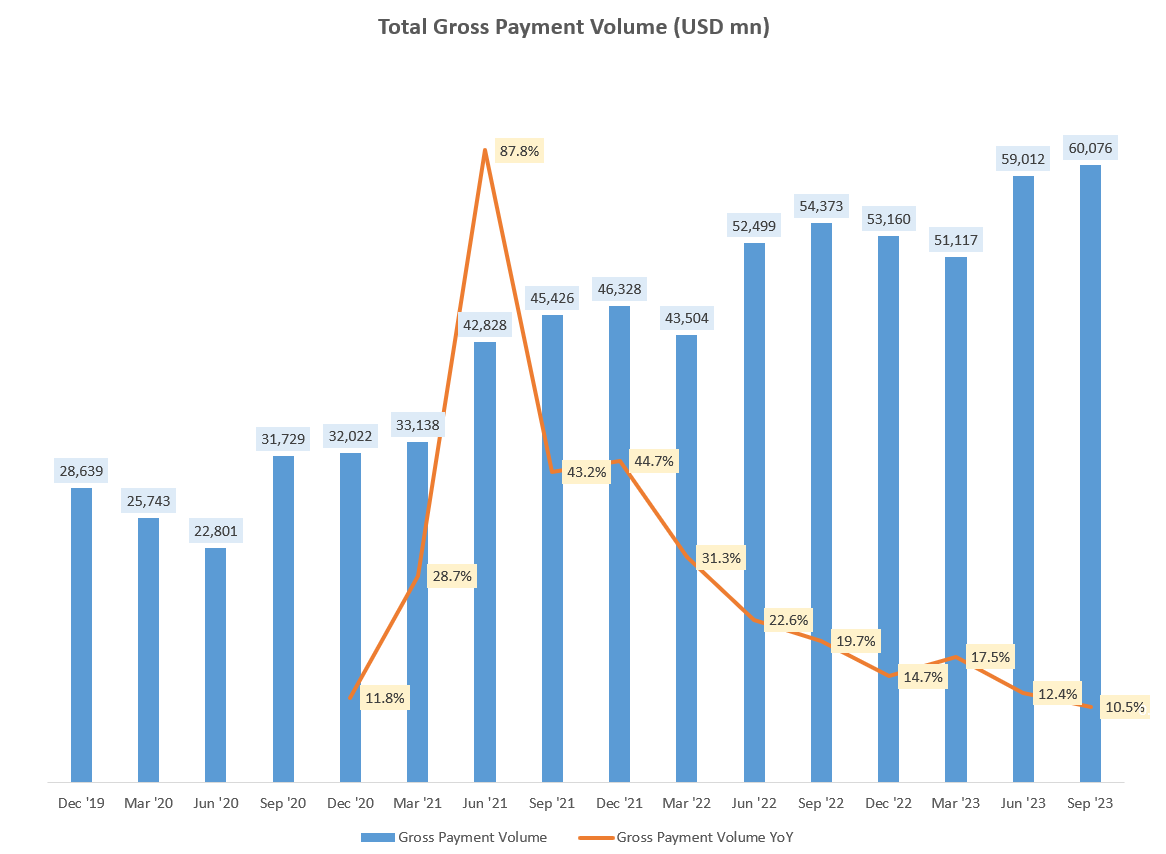

Total Gross Payment Volume (USD mn) (Company Filings, Author's Analysis)

{kind=link}

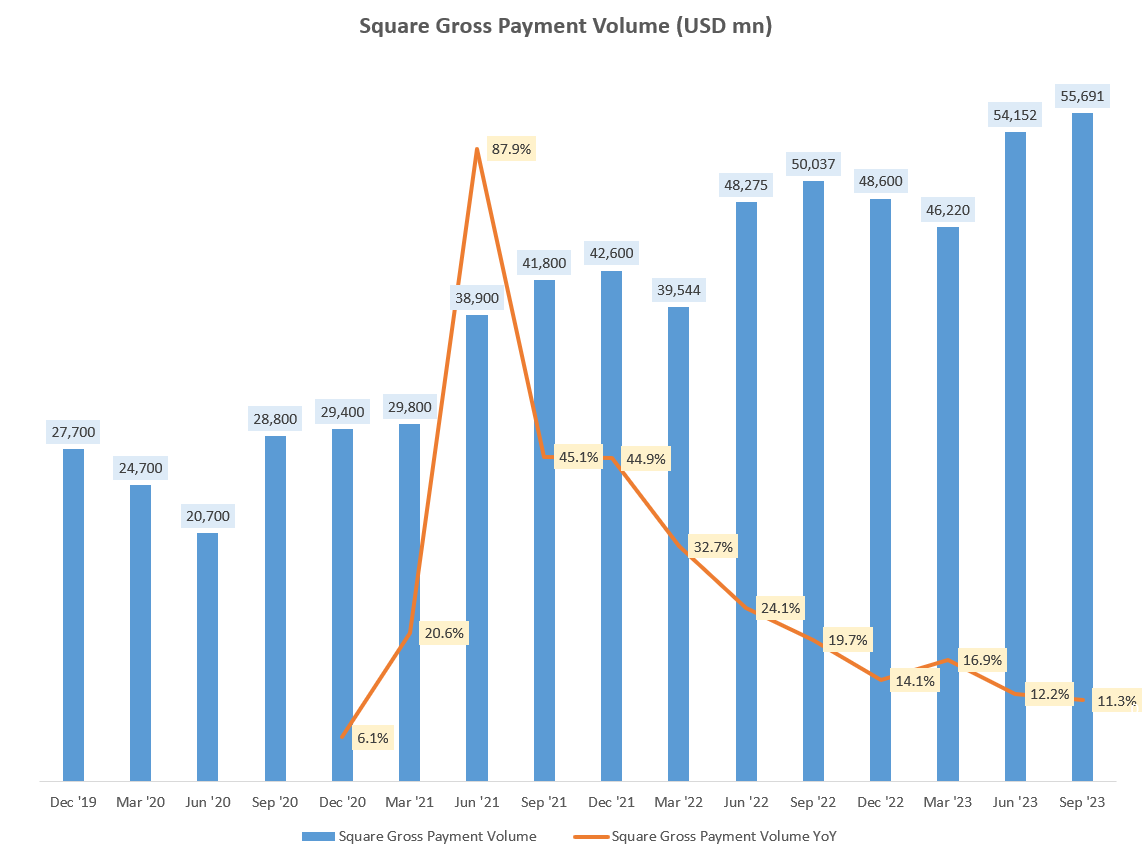

The steep deceleration in transaction revenue growth is attributed to total gross payment volumes (GPV), which has seen a similar fall from 30-40% YoY growth rates to around 10% levels as of the latest quarter. Transaction take rates have remained stable in the high 2.7-2.8% range. GPV growth has shown a similar decelerating profile in both the merchant-facing Square business (which makes up almost 93% of total GPV):

Square Gross Payment Volume (USD mn) (Company Filings, Author's Analysis)

{kind=link}

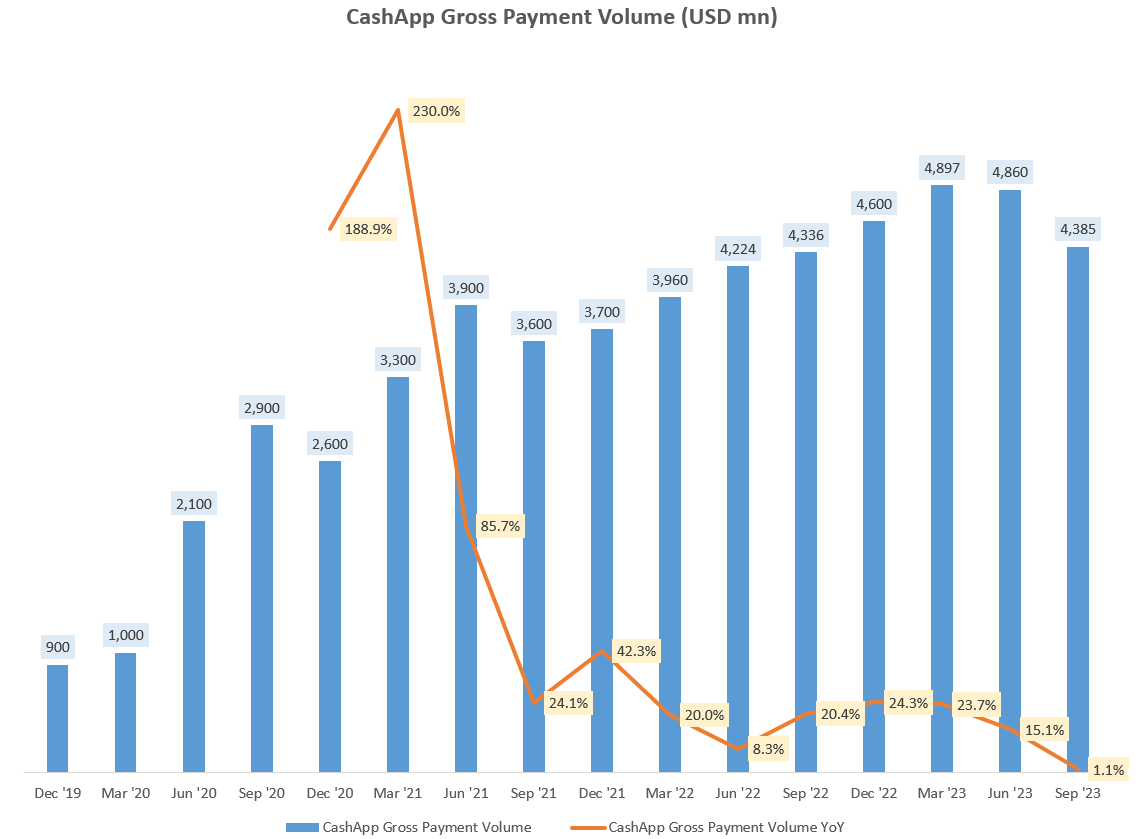

And also the consumer-facing CashApp business:

CashApp Gross Payment Volume (USD mn) (Company Filings, Author's Analysis)

{kind=link}

Block's 2021 Gross Payment Volume Mix (Statista, Author's Analysis)

As you can see above, almost 60% of Block's GPV is comprised of the food and beverage, beauty and other retail categories. The key point is that Block's GPV is very aligned to the performance of the US Retail sector, particularly the discretionary-spending side as they don't serve consumer staples categories such as groceries and gas . The data for this mix is a bit dated as it is from 2021. However, the mix and focus verticals for the company has not materially changed. For example, management recently highlighted:

We're going to prioritize two verticals, in particular, food and beverage. And also services such as beauty.

- Co-Founder Jack Dorsey in the Q3 FY23 earnings call

In fact, management has a strategy to go deeper within these focus verticals, targeting larger franchises:

Franchise and multi-entity sellers are key to our upmarket strategy as they generally use more products and generate greater gross profit than non-franchise sellers.

- Block's Q3 FY23 Shareholder letter

The macros point to mixed signals for top-line recovery

I believe US macroeconomic data releases such as Consumer Sentiment and Retail Sales give us leading indications of Block's GPV and Transaction Revenues outlook. Management has validated the idea that the macro trends affect their business in the latest earnings call:

Now we think the same-store growth, the slowdown there is relatively in line with broader macro trends across discretionary verticals... When you look at GPV per seller, this is where we believe the recent moderation we've seen has been macro-related .-- processing volumes at existing sellers were lower in the third quarter compared to the prior year. We believe it's macro-driven as the recent results of track directionally with other third-party spend indicators that we measure when we adjust for our mix of verticals given our greater mix of discretionary spend.

- COO and CFO Amrita Ahuja in the Q3 FY23 earnings call, Author's bolded highlights

US data is most relevant for Block because this geography is responsible for 93% of overall revenues.

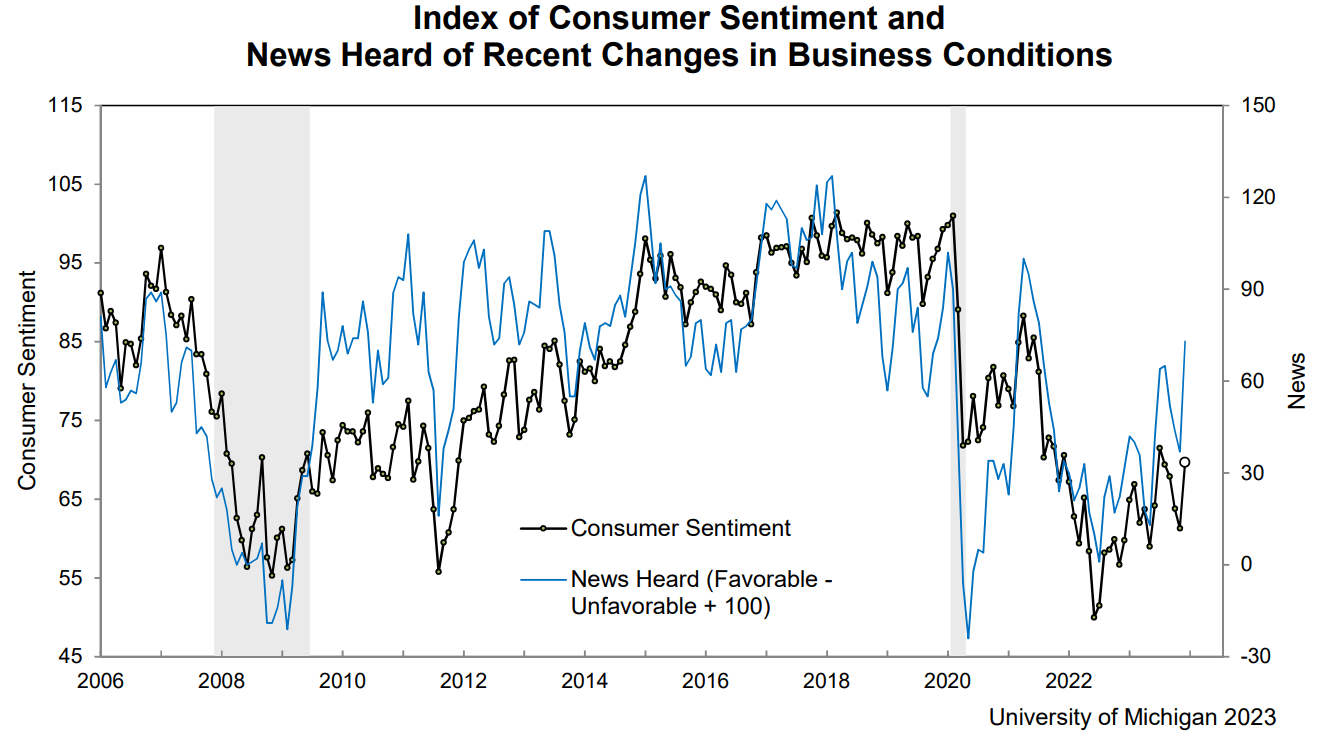

Index of Consumer Sentiment (University of Michigan Consumer Sentiment)

{kind=link}

Consumer Sentiment is clearly rebounding very strongly according to the University of Michigan Consumer Sentiment Index. In December 2023, it printed 69.7 compared to 61.3 in the month prior. Noteworthily, the index of Consumer Expectations also went up very strongly from 56.8 in November 2023 to 67.4 in December 2023. This indicates buoyant Consumer Activity, which is pertinent and bullish for Block as it is ultimately a B2C business (even its B2B Merchants business Square's activity is highly dependent on end-consumer behavior).

{kind=link}

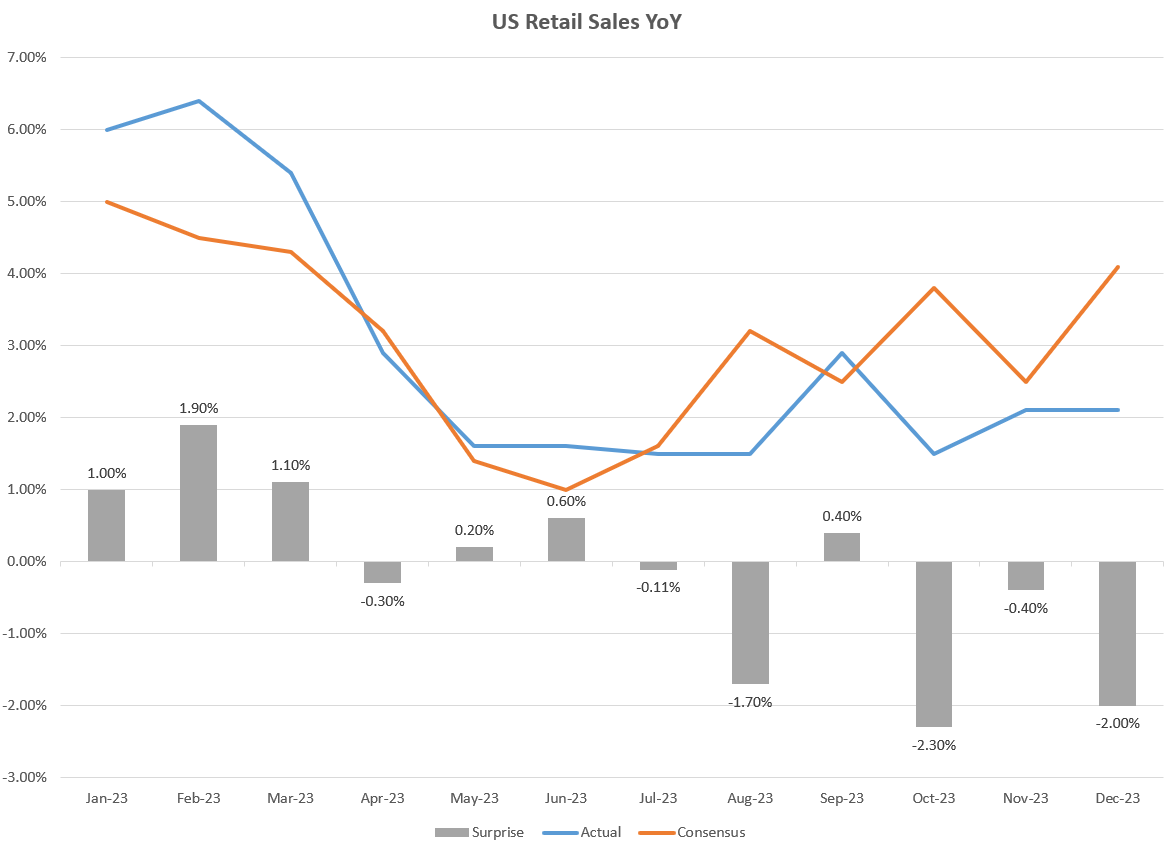

On the Retail Sales side however, despite consensus expectations expecting a meaningful growth rebound since H2 FY23 (which seems reasonable as Consumer Sentiment has been showing promise), actual results have for the most part fallen short, with 3 negative surprises in the last 5 months. On a YoY growth basis, US Retail Sales are chugging along at an underwhelming 2.00% as of December 2023. Therefore, this data does not paint an optimistic picture for Block's GPVs.

Overall, the macros are giving me mixed signals on the leading indicators of Block's GPV performance.

Block's cost-cutting program can make its workforce efficiency more in-line with peers

As I dug in through both the lens of Square and also our investment framework, I just found a lot of silos, a lot of redundancy, a lot of kind of a lack of desire for teams to work together.

- Cofounder and Square Head Jack Dorsey's assessment of the business in the Q3 FY23 earnings call

The numbers affirm Dorsey's observations:

Current Employee Productivity (USD) (Company Filings, Author's Analysis)

{kind=link}

Management revealed that Block currently has a bit more than 13,000 employees. In terms of employee productivity metrics, Block's opex (R&D and SG&A costs) per employee is consistently at least 100% higher than similar peers - Paypal ( PYPL ), Global Payments ( GPN ), Shift4 ( FOUR ) and Toast ( TOST ). As a small counterpoint, Block makes more revenue per employee too. However as you can see on the last row in the snapshot above, on a GAAP Gross Profit - Opex per employee basis, Block is consistently worse than all its peers except Toast, which still needs to transition toward profitability.

Block management has an aggressive cost-cutting plan to lay off 1,000 employees (7.7% of the total workforce):

Our cap of 12,000 people compares to our current size of just over 13,000 people as of the end of the third quarter. We believe constraining team size will enable us to be more effective in how we drive performance and service of our customers and accountability on our business strategies.

COO and CFO Amrita Ahuja in the Q3 FY23 earnings call, Author's bolded highlight.

Let's run some scenarios to get an idea of how this would affect the bottom-line. If Block managed to deliver Q3 FY23 with 12,000 employees instead of 13,000 that would result in a 66% Gross Profit - Opex per employee productivity metric. And whilst this would still be a bit worse than Paypal, it would compare a bit more favorably vs peers such as GPN and FOUR:

Employee Productivity with 1000 fewer employees (Company Filings, Author's Analysis)

{kind=link}

Under the same scenario, Block's EBIT margins would be +2.1% instead of -0.2% for the latest quarter:

Block EBIT Margins (Company Filings, Author's Analysis)

More importantly, the incremental YoY EBIT margins would be much healthier at close to 15%:

Block Incremental YoY EBIT Margin (Company Filings, Author's Analysis)

This is a much healthier margin profile for Block's kind of business. For context, PayPal's EBIT margin profile hovers around a similar 15-16% range. So I think management has the right intentions. And they are not doing something particularly unique. 2022 and 2023 already established a playbook for creating meaningful margin expansion via a rationalization of the workforce. For example, Elon Musk cut 80% of the workforce at Twitter without any major negative consequences. In his own words :

There were a lot of people that didn't seem to have a lot of value. I think that's true at many Silicon Valley companies. I think there is the possibility for significant cuts at other companies without affecting their productivity, in fact increasing their productivity.

Maybe Dorsey - founder and former head of Twitter - has picked up this playbook from Musk...

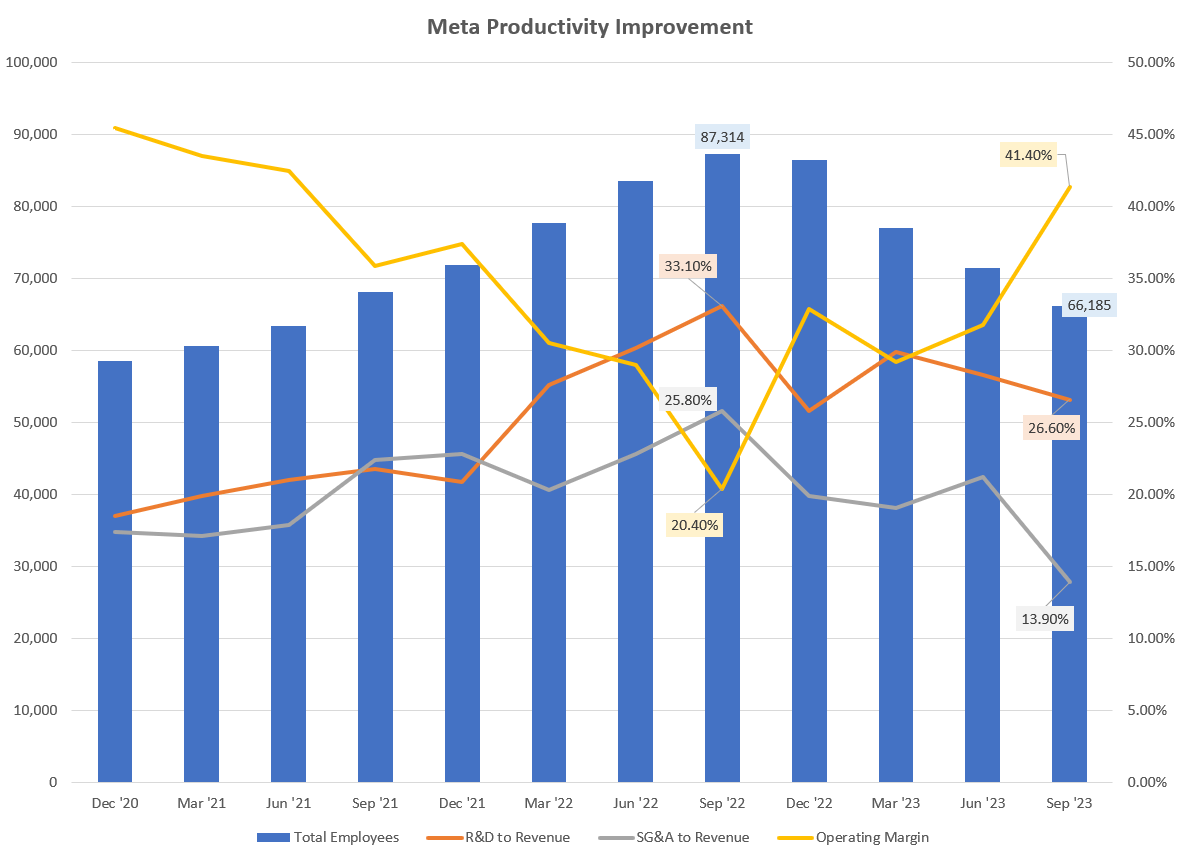

Other technology companies have successfully executed this strategy too, surprising many analysts ( including me ) as can been seen in Meta's ( META ) productivity improve success:

Meta Productivity Improvement (Company Filings, Author's Analysis)

{kind=link}

The only question then is whether Dorsey and co can play the same moves well to realize margin benefits via a leaner Block. One thing to note about Dorsey's leadership style is that he prefers decisions to be taken by his leadership group in a true decentralized fashion, which is a great fascination he holds given his focus on cryptocurrency and decentralized technologies. Dorsey apparently does not like decisions creeping its way to the top. However, some argue that it is precisely this leadership style that led to slack in his former company Twitter:

Every time he had to make a decision, he said he saw it as a “failure” of the business, preferring to allow staffers to thrash out ideas themselves. But it was this lack of steady hand and resulting indecision, his critics argue, that left Twitter plagued by slow innovation, briefly challenged by activist investor Elliott Management and ultimately vulnerable to Musk.

Has Dorsey adapted his style? Would Block's management be able to successfully make the company more productive? I think it's prudent to wait for some signs of proof here.

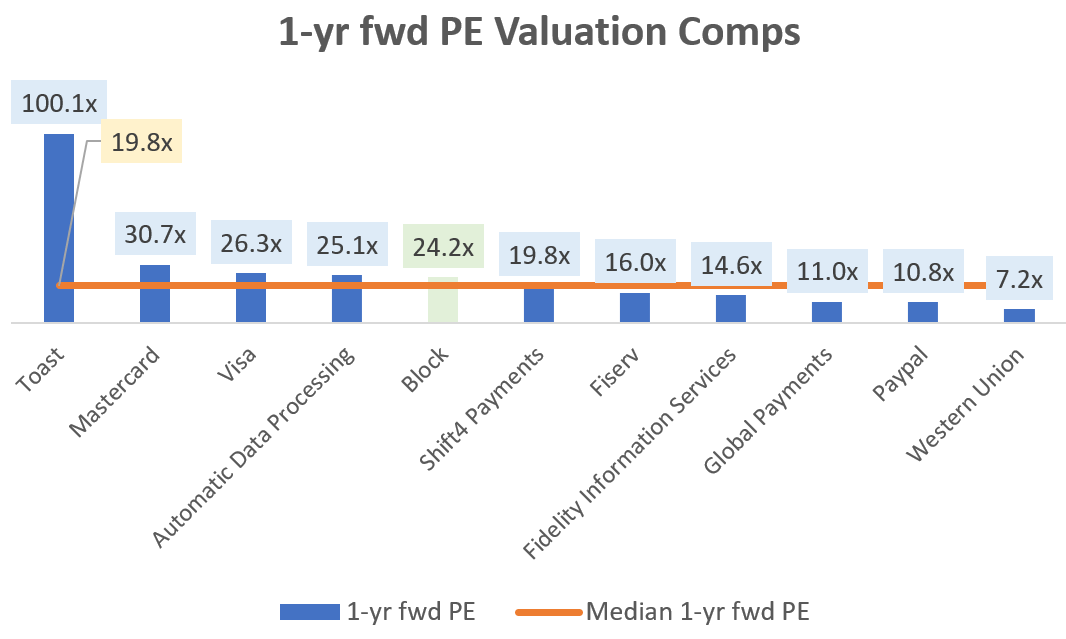

Block is trading at a moderate premium vs its peers

{kind=link}

Peerset includes Toast ( TOST ), Mastercard ( MA ), Visa ( V ), Automatic Data Processing ( ADP ), Shift4 Payments ( FOUR ), Fiserv ( FI ), Fidelity Information Services ( FIS ), Global Payments ( GPN ), PayPal ( PYPL ) and Western Union ( WU )

Block is currently trading at a 1-yr fwd PE of 24.2x; a 22% premium above the peer-group median of 19.8x. Given the unclear macro outlook for Block's top-line and my preference to wait for some proof of execution on management's ambitious cost-cutting plan, I deem this premium to lack a sufficient margin of safety for buys.

Takeaway & Positioning

The macro indicators on US Consumer Sentiment point towards a bullish outlook for Block. However, underwhelming US Retail Sales data undermine that view. As Block's transactions business (almost a third of overall revenues and gross profits) is linked to consumers and retail activity, this casts doubt on visibility of a growth re-acceleration.

On the costs and margins side, I believe management has the right plan to cut almost 8% of the workforce. My calculations reveal that this would dramatically change the employee productivity metrics to be more in-line with peers, and make GAAP-EBIT profitability more suitable for a solid fintech business. Block does not need to do anything new; Twitter and Meta have already provided a playbook and set the model for unlocking margin improvements via workforce rationalization. However, Dorsey is known to be a not-so-hands-on leader; which is necessary for driving transformative change . So I believe it is prudent to first wait and see some progress on Block's execution of its margin improvement goals to gain confidence on a successful turnaround.

Given this stance, Block's 22% premium valuations relative to the sector median's 1-yr fwd PE do not leave much margin of safety. Hence, I rate the stock a 'Neutral/Hold' for now.

How to interpret Hunting Alpha's ratings:

Strong Buy: Expect the company to outperform the S&P500 on a total shareholder return basis, with higher than usual confidence

Buy: Expect the company to outperform the S&P500 on a total shareholder return basis

Neutral/hold: Expect the company to perform in-line with the S&P500 on a total shareholder return basis

Sell: Expect the company to underperform the S&P500 on a total shareholder return basis

Strong Sell: Expect the company to underperform the S&P500 on a total shareholder return basis, with higher than usual confidence

For further details see:

Block: Can Management Execute On A Good Plan?