COIN - Block: Downside Risk Outweighs Upside Potential - Better Alternatives Exist

2023-09-25 14:00:00 ET

Summary

- Block's stock has fallen 82% since reaching an all-time high in August 2021 and is now trading around $50.

- The company has faced challenges including a damning report about its business practices and the departure of its CEO.

- The absence of a share buyback program raises concerns about the company's capital allocation strategy and its ability to compete in the financial transaction services sector.

- We believe SQ is currently a sell.

Introduction

Block ( SQ ) reached an all-time high on August 2nd, 2021, at $289 and has since fallen 82% and is now trading around the $50 mark.

Overall, SQ has been through a tough time since the highs of 2021, having posted its first year with a net income loss since 2018. SQ has been through its fair share of problematic events in the past year.

The most memorable might be the damning report from Hindenburg Research which claim that Block was willing to "facilitate fraud against consumers and the government, avoid regulation, dress up predatory loans and fees as revolutionary technology, and mislead investors with inflated metrics." - Hindenburg found that between 40% - 75% of the users on Cashapp were either fake, involved in fraud or multiple accounts tied to a single person. Not a good look for SQ.

More recently, SQ's CEO decided to step down effectively on October 2nd, seemingly out of nowhere. Jack Dorsey has, therefore, been appointed CEO for the time being. Dorsey has a mixed history as CEO of publicly listed companies and is perhaps best known for his time as CEO of Twitter (now X). During his time at Twitter, the stock provided a cumulative return of approximately 12% for shareholders.

Although these events have caused the stock to fall considerably in the past six months, we believe SQ has a decent amount of downside. This article will discuss some of SQ's more notable acquisitions, their overall valuation, and how they stack up against their peers.

Many Well-Known Companies Under The Block Umbrella

Block has made a wide array of acquisitions that are supposed to bolster and diversify its business while also providing decent synergies within the company.

Stitch Labs Inc.

Founded in 2011, Stitch Labs specializes in operations management software, offering solutions encompassing inventory and order management, channel coordination, and fulfillment services. Their notable collaboration with SQ in May 2014 allowed SQ's mobile payment users to efficiently oversee inventory, invoices, and shipping via the Stitch Labs platform. In July 2020, SQ made the significant move to acquire Stitch Labs to make their services payment to their customers. However, the latter continued to provide its products until the spring of 2021, albeit not accepting new customers .

Weebly Inc.

Weebly is a global platform simplifying website, blog, and online store development. With a presence serving millions of businesses and powering over 50 million sites worldwide, Weebly was an attractive prospect. SQ's acquisition of Weebly in May 2018, valued at approximately $272.5 million in cash and stock, aimed to integrate Weebly's web-building tools with SQ's in-person and online offerings. This was meant to create synergy for businesses wanting to use SQ's payment solutions and build an online presence. This move was meant to broaden SQ's international customer base and establish a new recurring revenue stream.

Verse Technologies Inc.

Verse Technologies pioneered mobile peer-to-peer (P2P) payment solutions. Their mobile payment app simplifies money transfers, facilitates payment requests, and enables balance transfers to bank accounts. SQ's acquisition of Verse in June 2020, estimated between $33.8 million and $56.3 million, marked a significant expansion for SQ, particularly in Europe, including Spain, France, Germany, and Italy. As an independent business, SQ supported Verse's continued expansion throughout Europe, ensuring product, customer, and operations continuity.

Eloquent Labs

Eloquent Labs, a startup founded in 2016 by prominent natural language processing researchers, specializes in conversational AI services. Their AI-driven software replaces live chat customer support agents for e-commerce companies. In May 2019, SQ acquired Eloquent Labs to leverage its AI technology to enhance messaging services within SQ's payments ecosystem. This acquisition demonstrated SQ's dedication to advancing AI technology, further underscored by its acquisition of Dessa , a Canadian tech company specializing in emerging AI technologies, in February 2020.

Third Party Trade LLC

Founded in 2015, Third Party Trade provides an API platform for constructing financial applications related to investing. Although public details about the acquisition were limited, Michael Giles (CEO of Third Part Trade LLC) confirmed the sale to SQ on his LinkedIn page. He began working full-time for SQ in February 2019, and Third-Party Trade was rebranded as Cash App Investing LLC, perhaps the most well-known product in SQ's product line. In October 2019, SQ introduced free stock trading on its Cash App, marking a significant development following the acquisition.

A Lack Of Fundamental Catalysts

Our article covering PayPal ( PYPL ) discussed their shifting focus on share buybacks in recent years. We wanted to do the same with SQ for consistency, and SQ and PYPL are very close competitors.

Here is the thing: SQ has never initialized a share buyback program in its history. Block's choice to steer clear of share buybacks as a means of giving back to its shareholders raises some valid concerns. Share buybacks are a recognized method for companies to use their surplus cash to buy back their shares from the stock market.

This process typically results in a reduction in the total number of shares outstanding, which can potentially lead to an increase in the company's EPS and, consequently, its stock price. It also sends a positive signal to investors that the company is optimistic about its future growth prospects. By not considering this strategy, Block may miss an opportunity to enhance shareholder value and convey a favorable message to its investors.

With the company's stock currently trading around $45, there's a strong argument for Block to contemplate initiating a share buyback program. Repurchasing shares could be reasonable at this price point, as it can contribute to a higher stock price in the long run. This would benefit shareholders who have demonstrated confidence in the company's performance. Additionally, in a market environment where investors closely monitor how companies allocate their capital, a well-executed buyback program can be a strategic move to boost investor trust and loyalty.

Block's substantial cash balance of over $6.4B highlights the feasibility of implementing a share buyback program. This significant cash reserve gives the company the financial means to carry out such a strategy without jeopardizing its operations or future growth plans. It's worth noting that while returning value to shareholders through dividends is another standard method, share buybacks offer a more adaptable approach, allowing the company to respond to changing circumstances and market dynamics.

Investors may be banking on additional growth in a highly competitive sector like financial transaction services without plans for share buybacks. In this dynamic market, sustaining growth can be challenging, given the fierce competition from established players and new entrants. With share buybacks off the table, investors are likely looking for strong indicators that the company has a solid plan for expanding its operations, increasing its customer base, and diversifying its revenue streams. Demonstrating a clear and effective growth strategy becomes pivotal as investors seek reassurance that the company can thrive and deliver returns in a market that continually demands innovation and adaptability.

Financials and Valuation

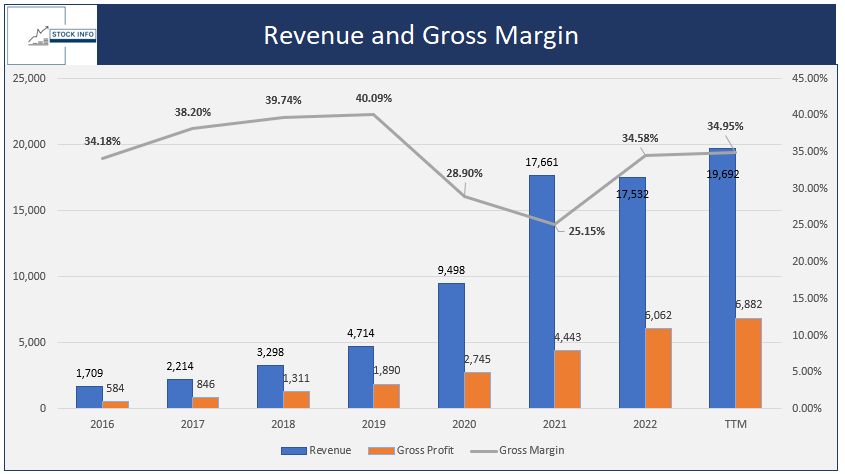

The significant decline in share price is not directly related to SQ's earnings. They still made about $17.5B in revenue in 2022, and their TTM is currently around $19.7B.

That is a 5-year revenue CAGR of almost 43%, which is highly impressive. Their gross margin has increased since 2021 but is still below its high of just over 40% in 2019.

{kind=link}

While investors should note that SQ's gross margin was 40% in 2019, it declined in 2020 mainly due to the consequences of COVID-19. While Block's gross margin may be improving, the recent change in CEO and overall pressure it has faced after the Hindenburg report could hit its top line.

In addition, SQ's free cash flow has taken a massive hit in the past year. From Q2 2022 - Q4 2022, the company reported a negative free cash flow as low as -$518M in Q2 2022. Although they went cash flow positive in recent quarters, it's far from consistent enough to entice investors. Over a trailing twelve-month period, SQ has an FCF of $321.65M, which gives an FCF yield of 1.17%, which is relatively subpar.

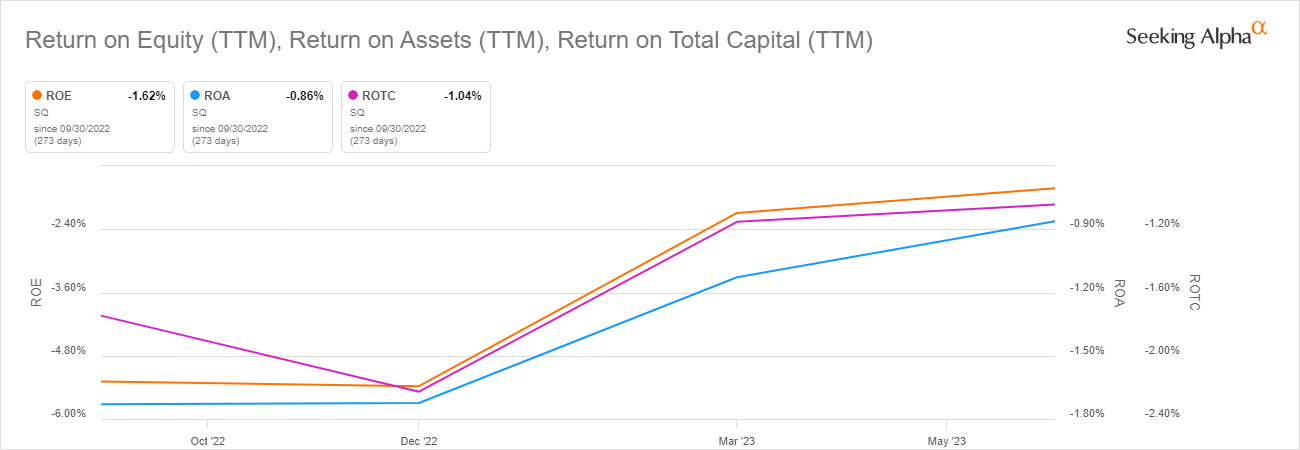

Suppose we look at different profitability factors, namely RoE, RoA, and ROTC, all in TTM. SQ currently has a negative Return on equity, assets, and total capital in TTM. As for their FCF, these metrics do not stand out as indicators of a sound investment. Although it has been improving over the last few quarters, there is no real sign of any significant improvements in its profitability.

{kind=link}

We believe that for SQ to become an exciting investment opportunity, its free cash flow must stay positive and preferably stand increasing. In addition, they must become more profitable. As opposed to PayPal, SQ simply cannot compete on these metrics. Hence, we believe there are better alternatives in the industry.

If we look at how SQ has been priced compared to its peers in the last month, it is clear that in terms of price to free cash flow, SQ is severely overpriced. The company trades at almost four times the P/FCF of Adyen and almost five times as much as PYPL.

Ycharts

Historically, SQ has always traded significantly higher P/FCF than its peers. It seems somewhat unreasonable that SQ trades at such a high valuation compared to its peers. Thus, we believe the correction this stock has experienced in the past few months is justified.

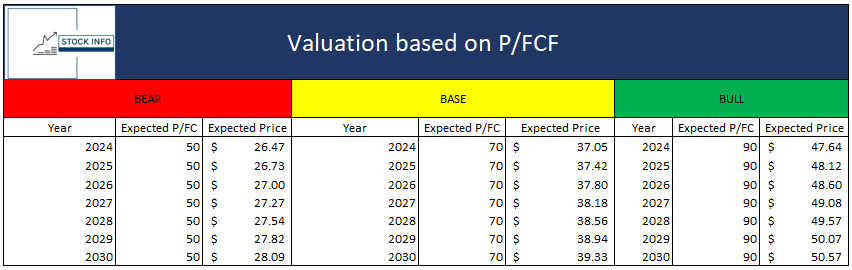

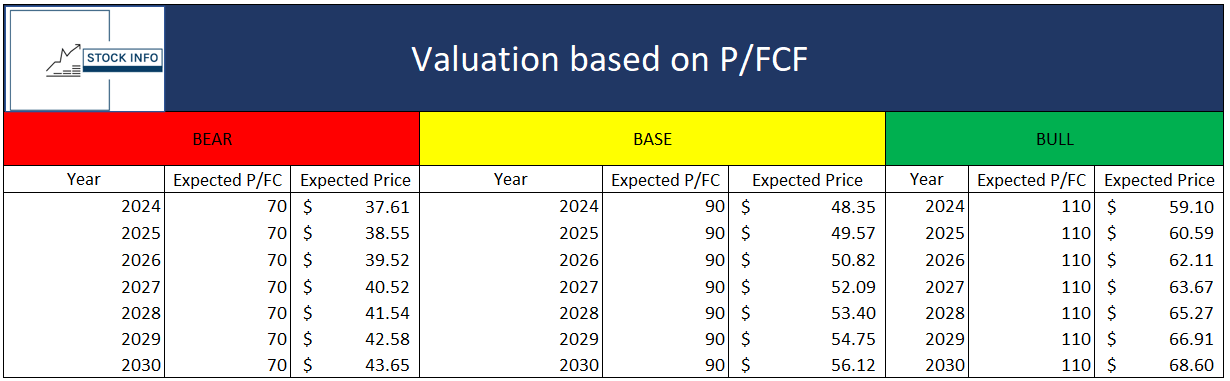

With that being said, there is a real possibility the stock could go even lower. Our valuation model based on P/FCF assumes different P/FCF ratios for a bear, base, and bull scenario for SQ. In addition, we will assume a relatively conservative 1% growth in FCF, mainly because SQ's FCF has been fluctuating significantly throughout the years. Therefore, we wish to keep it relatively constant. Moreover, we will use the TTM FCF for this valuation, assuming that SQ will not buy back any shares.

{kind=link}

The results of our model suggest that even in a base case, SQ is still trading approximately $7 above the expected 2024 price, assuming the stock will trade at a P/FCF of 70. Assuming a bullish case, the stock would be valued around its current market price. It should be noted that we are not assuming any decline in FCF or growth for any year in this model. If SQ's FCF contracts, valuations according to our model would only result in a lower expected price.

To summarize, we believe that SQ's high P/FCF may be unjustifiably high compared to its peers. Using a P/FCF ratio slightly closer to its peers shows that SQ is still overvalued relative to its current price.

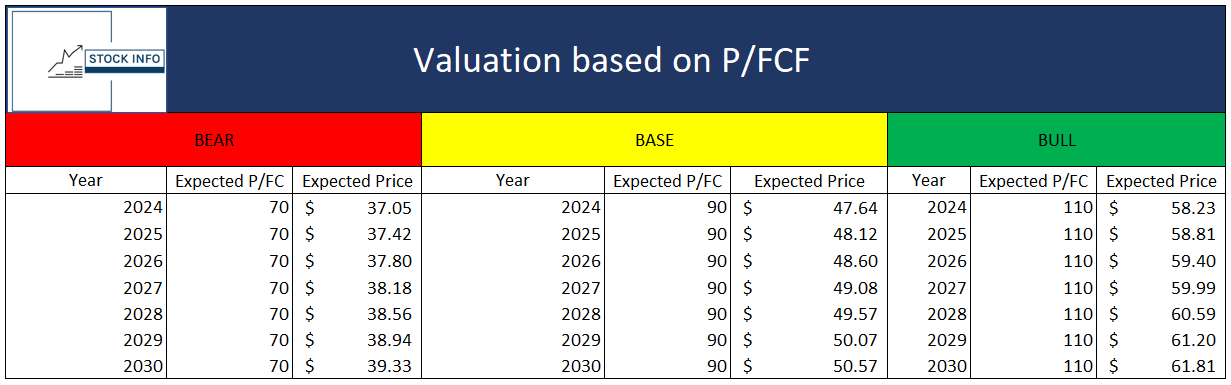

As you can see in the chart below, the valuation model based on P/FCF isn't looking bright even if we raise the expected P/FCFs in each of the cases. The model below still assumes overall FCF growth of 1% per year.

{kind=link}

Last but not least, we will also give you a model that assumes a 1.5% share repurchase each year, in addition to the FCF growth of 1% per year. This results in the following model.

{kind=link}

Even when taking this into consideration, the stock is still looking rather expensive when looking at its free cash flow.

Peers

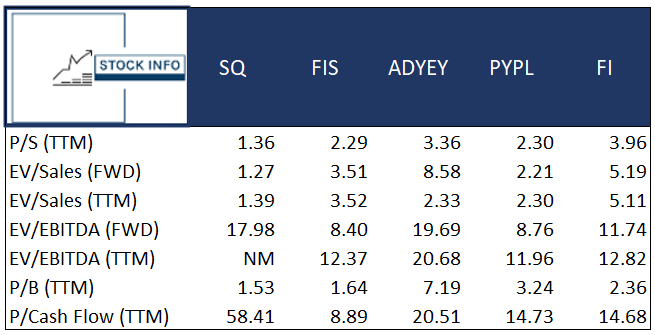

Looking at how Block compares several valuation metrics to its peers, valuation looks somewhat better for SQ.

{kind=link}

Firstly, SQ displays a relatively modest P/S ((TTM)) ratio of 1.36, significantly below that of ADYEY (3.36), PYPL (2.30), and FI (3.96). This implies that SQ's stock is conservatively valued at its sales and could be undervalued on this metric compared to its peers.

Similarly, SQ's EV/Sales ((FWD)) ratio of 1.27 stands out as notably lower than FIS (3.51), ADYEY (8.58), and FI (5.19). This suggests that investors may have a relatively moderate outlook on SQ's future sales potential, leading to a comparatively lower enterprise value.

When examining SQ's P/B ((TTM)) ratio, which currently sits at 1.53, it becomes apparent that SQ's stock price relies less on its book value per share compared to ADYEY (7.19), PYPL (3.24), and FI (2.36). This could mean investors are more confident in SQ's capacity to generate future earnings rather than focusing on the company's tangible assets.

On the flip side, SQ's EV/EBITDA ((FWD)) ratio of 17.98 appears significantly higher when contrasted with ADYEY (19.69) and FI (11.74). This implies that investors are willing to pay a premium for the expected future earnings of SQ before factoring in interest, taxes, depreciation, and amortization.

Lastly, SQ's P/Cash Flow ((TTM)) ratio of 58.41 significantly surpasses those of FIS (8.89), ADYEY (20.51), PYPL (14.73), and FI (14.68), indicating heightened expectations regarding the company's cash flow potential.

Overall, SQ appears to hold its ground against peers, boasting lower P/S and EV/Sales ratios. However, investors appear willing to invest at a premium for the anticipated future earnings of SQ, as indicated by its higher EV/EBITDA ((FWD)) ratio.

The notably elevated P/Cash Flow ((TTM)) ratio implies optimistic forecasts regarding cash flow. Ultimately, while SQ's valuation metrics depict undervaluation and investor confidence, a comprehensive assessment of the company's financial stability, competitive positioning, and growth potential is essential before forming a definitive judgment regarding its investment attractiveness.

Technical Analysis

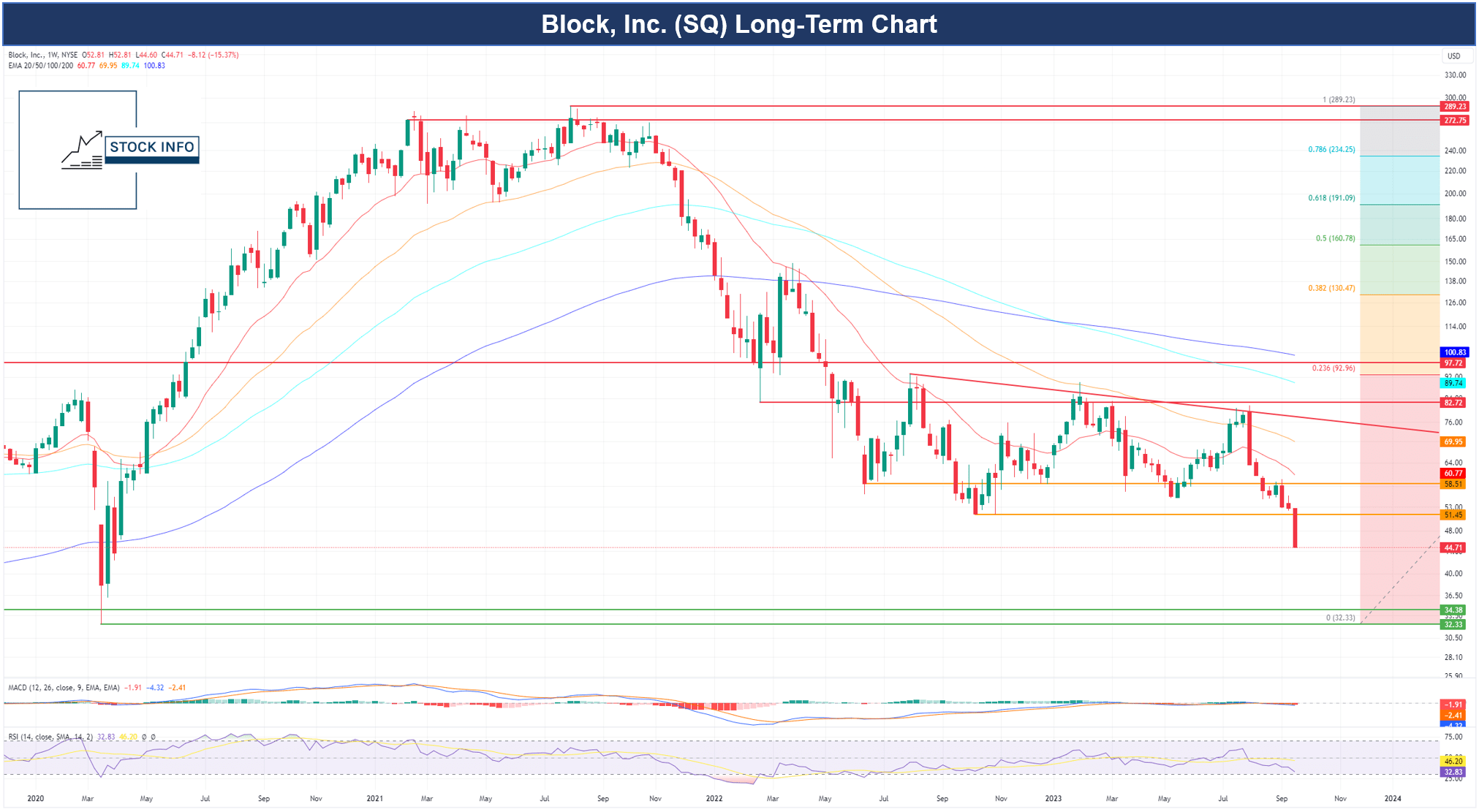

If we look at the technicals for SQ, it is clear that the company was grappling with a challenging week, experiencing a notable decline of nearly 15% in its stock price over a short period. This adds to the overall drop of over 40% since the start of August, raising concerns among investors.

A particularly worrying aspect is that the stock has fallen below a critical support level to $51.45, a price point last seen in October. Optimistic investors hope that SQ can bounce back and regain this vital support level soon. However, there's a real risk that the stock might continue to drop, possibly reaching a price range between $38 and $40 before finding support.

Even more concerning, if the $38 level doesn't hold, there's a possibility that the stock could drop to its lowest point in 2020, around $32 per share. This presents a challenge for investors who have confidence in the stock's stability.

Looking at the EMAs, the stock is trading below all of its EMAs on the chart below. This shows the immense bearish pressure currently put on the stock. For the stock to find a significant upside, it would have to break through all EMAs and, most importantly, get above the 200 EMA. If we look at the chart, the stock broke below the 200 EMA back at the beginning of 2022, whereafter this exact EMA became a resistance for the stock. This break-and-base behavior is what investors would want to see for SQ but to the upside.

Unfortunately, we do not see any signs of a significant move to the upside for SQ on a technical level in the short to medium term. We believe there is more downside risk rather than upside.

{kind=link}

Conclusion

In conclusion, Block has faced a challenging journey since its all-time high in August 2021, witnessing an 82% decline in its stock price, which now hovers around $50. The company grappled with several setbacks, notably the scathing report from Hindenburg Research, which raised concerns about its business practices and integrity. Additionally, the sudden departure of its CEO, Jack Dorsey's appointment as interim CEO, and his mixed track record further added uncertainty to the company's future. While these events have contributed significantly to the stock's decline in the past six months, there remains a looming possibility of further downside.

Block has made strategic acquisitions to diversify its business and create synergies, but questions linger about their impact and effectiveness. Moreover, despite a substantial cash reserve, the absence of a share buyback program raises concerns about the company's capital allocation strategy. Investors are left contemplating the company's growth prospects in a highly competitive financial transaction services sector. While valuation metrics suggest that SQ may be overpriced in terms of price to free cash flow compared to its peers, other metrics present a more nuanced picture. Ultimately, the stock's technical indicators indicate a bearish trend, with considerable downside risks in the short to medium term.

Investors in Block should proceed cautiously, considering the uncertainty surrounding the company's future, its ability to weather ongoing challenges, and the competitive landscape in the financial services industry. The stock's recent decline and questions about its valuation and strategic direction warrant careful evaluation before making investment decisions.

In addition, safer companies such as PayPal look to provide a better risk-to-reward, and we rate SQ a sell for these reasons.

For further details see:

Block: Downside Risk Outweighs Upside Potential - Better Alternatives Exist