TOST - Block's Earnings Will Be Energized By AI (Rating Upgrade)

2024-01-04 21:20:12 ET

Summary

- Jack Dorsey is back as the head of Block and has outlined plans to turn the company's growth around and reach the Rule of 40 by 2026.

- Cost-cutting measures, including staff cuts, limiting stock-based compensation, and leveraging AI, will be implemented.

- I provide a buy recommendation for SQ with a price target of $92.48/share based on a P/S multiple of 2.12x eFY24 sales.

With Jack Dorsey back in the hot seat with Block ( SQ ), the market appears to be very optimistic on his plans to turn the company’s growth around and reach the Rule of 40 by 2026. In addition to striving for stronger topline growth, Dorsey outlined a number of cost-cutting measures that will be taking place, including cutting and capping staff at 12,000, limiting stock-based compensation, cutting overhead personnel, and leveraging AI across the sales & marketing and development process. Dorsey outlined in his letter to shareholders that once the Rule of 40 is achieved, the firm can return more of its earnings to shareholders. As of q3’23, Block initiated a $1b share repurchase program to offset dilution resulting from stock comp. Given the drive to improve operations and improve the business, I provide SQ a BUY recommendation with a price target of $92.48/share based on 2.12x eFY24 sales.

Operations

The party at Block is over and it is time to get down to business. As of q3’23, Jack Dorsey reemerged as the head of Block with the official title of “Block Head + Square Head” and has taken this position head on. With the goal in mind of reaching the Rule of 40 by 2026, Mr. Dorsey has his work cut out for him. Much of his initiative involves refocusing the firm, breaking down silos and integrating solutions, and flattening the corporate structure by reducing overhead. By integrating AI throughout their platform and product development lifecycle, Mr. Dorsey anticipates a faster development to deployment within the applications. Management emphasized a focus in their food & beverage and beauty verticals, both through sales tactics and product development. With the use of AI, management believes that they can better engage with sellers and potential sellers across the sales & marketing process.

In addition to operational cuts, Mr. Dorsey intends on getting stock-based compensation under control and limiting share dilution through a $1b share buyback program.

So, stock-based compensation in the fourth quarter, we expect to be relatively flat relative -- on an absolute dollar basis relative to the third quarter. And as I said on the call earlier, we expect to drive meaningful leverage on SBC over time starting in 2024. And here we'd measure it as stock-based compensation as a percentage of gross profit as we implement the absolute number cap on the number of people that we have at the company and look to drive operational leverage and efficiencies across our business.

{kind=link}

Corporate Reports

Looking at the firm’s cash flow statements, it’s clear that stock-based compensation holds a heavy weight on the firm’s ability to generate cash. Management discerned that q4’23 stock-based compensation will remain flat sequentially at around $345mm. 2024 stock-based compensation should reduce significantly as the firm seeks to reduce headcount by ~1,000 personnel from 13,000.

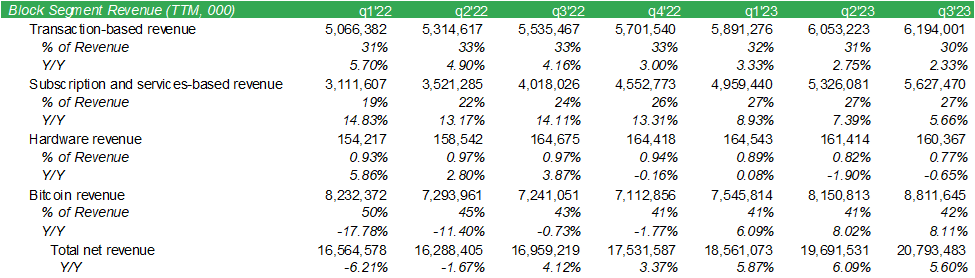

Looking through the segments on a trailing basis, the firm experienced overall growth in each segment other than hardware revenue, which fell by 65bps on a TTM basis. I do not believe this to be much of a concern given it accounts for less than 1% of total revenue; however, I do believe this could potentially be an early signal for future growth across the sellers software platform ecosystem used in conjunction with the hardware. Aside from hardware and bitcoin-related revenue, each segment experienced a slight decline in growth in q3’23. Though I believe it is too early to suggest that growth will stall in the coming fiscal year, overall growth rates have been in decline since q3’22, excluding the reemergence of bitcoin transactions on the platform.

{kind=link}

Corporate Reports

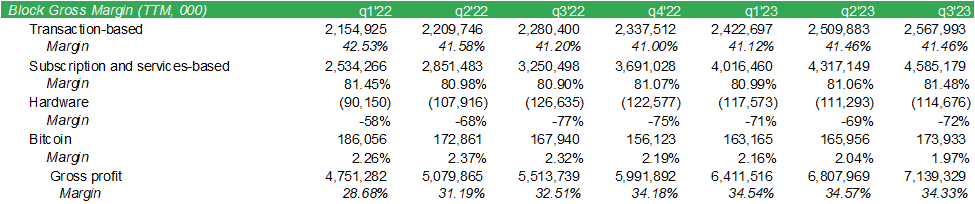

Despite the slight slowdown in growth, gross margins have experienced a slight decline with subscription- and service-based margins expanding to 81.48% and transaction-based margins remaining flat at 41.46%.

{kind=link}

Corporate Reports

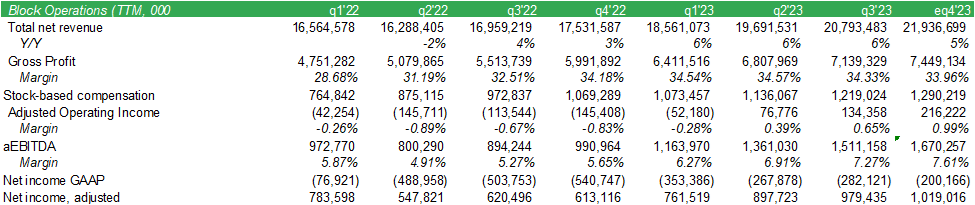

Overall operations strengthened in the quarter with aEBITDA reaching a 7.27% margin. Comparing GAAP and non-GAAP net income, it’s clear that management has been making strides in improving operational efficiency.

{kind=link}

Corporate Reports

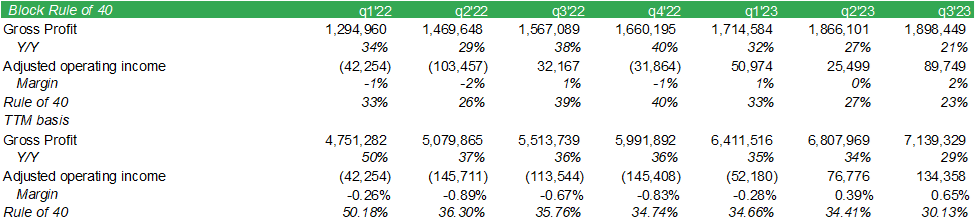

Because of where Block currently stands, it is difficult for me to envision the firm reaching the Rule of 40 by 2026, at least organically. Mr. Dorsey discerned that they’re calculating by the sum of gross profit growth and adjusted operating income margin. Given the sheer size, market penetration, and the competitive landscape in their industry verticals, achieving a 40% growth rate won’t be an easy task.

{kind=link}

Corporate Reports

With firms like Toast ( TOST ) and Shift4 Payments ( FOUR ) taking the restaurant industry and related hospitality industries by storm, either firm would either take market share with their competitively integrated front/back office applications, or potentially be rolled up into the Square ecosystem.

Comparing Toast and Square for restaurants, Square’s product lines are all offered at a lower price point, including the monthly software subscription fees. One of the values Toast has over Square is their bundling discount, when scaled, for their POS and Payroll software priced at $110/month +$4 per employee/month. Squares combined products would cost the seller $95/month + $6 per employee/month. In addition to this, Toast outpaces Square in transaction fees at 2.49% + $0.15 vs. Square’s fees of 2.60% + $0.10. Toast also offers 0% financing with $0 down with a fixed rate of payback per sale, similar to Square Capital’s offering.

Cash App experienced strong growth with the Cash App card reaching 22mm monthly actives as of q3’23. The segment originated over $900mm in short-term loans across more than 2mm monthly transactions. Block’s new app feature, Square Go, which was launched in August 2023, connected nearly half a million bookings in q3’23.

One of the offerings Block rolled out for Square customers is their AI-powered design applications , allowing them to use generative AI to automatically generate product descriptions, automate operations, and optimize workflows. I believe Square's generative AI-enabled applications will be a huge gamechanger for sellers as it can greatly reduce the time for most administrative tasks, such as updating a menu. This could also potentially sellers reduce costs in an already tight-margin business.

Block also launched a self-custody Bitcoin wallet , Bitkey in December 2023, giving users greater control over their digital currency. Whether this affects Block’s revenue growth from Bitcoin transactions is to be seen; however, providing users greater control over their digital currency may bolster new customer interests.

Looking ahead, management anticipates the firm to generate between $1,960-1,980mm in gross profit with aEBITDA coming in between $430-450mm for eq4’23. Assuming a constant 34% gross margin and using the midpoint for guidance, we can insinuate eFY23 revenue to come to $21,936mm. Applying these assumptions to management’s 2024 guidance, at $2,400mm in aEBITDA and assuming aEBITDA margin expands to 8%, we can expect ballpark $30b in revenue generation for eFY24, or a 37% increase to eFY23 total revenue. This may be a high estimate given the rate of margin expansion for aEBITDA, expanding by an average of 43bps sequentially since q3’22 when using the geometric mean. Even assuming a quarterly 35bps expansion rate, aEBITDA margins could be expected to reach as high as 9% by q4’24. With the assumed 9% aEBITDA margin, we can anticipate revenue to grow by 21% to $26,625mm for eFY24. This figure appears much more reasonable given the 25% growth rate between FY22 and eFY23. With the plan Jack Dorsey laid out in the earnings report, I believe Block can achieve this margin level, if not surpass it by q4’24.

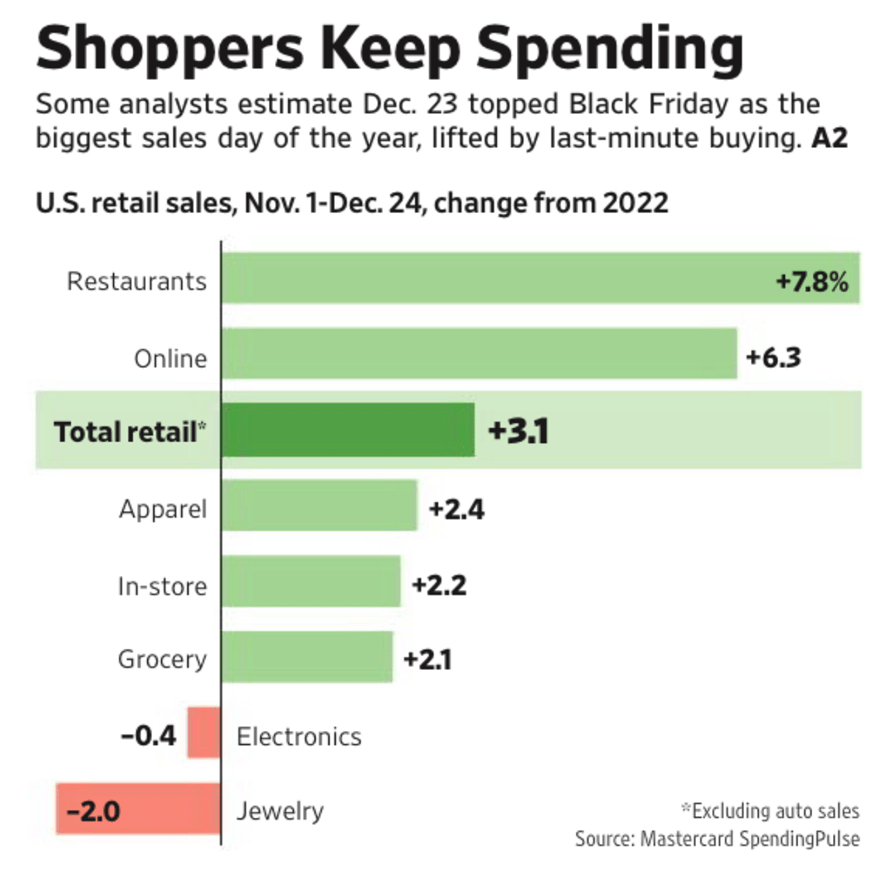

Lastly, there has been modestly conflicting data relating to consumer spending. Though timing is months apart, not enough has changed in the economy to deem either immaterial. The first was consumer spending data as compiled by Mastercard .

{kind=link}

Mastercard

What the chart suggests is that consumers remain resilient in spending net of electronics and jewelry.

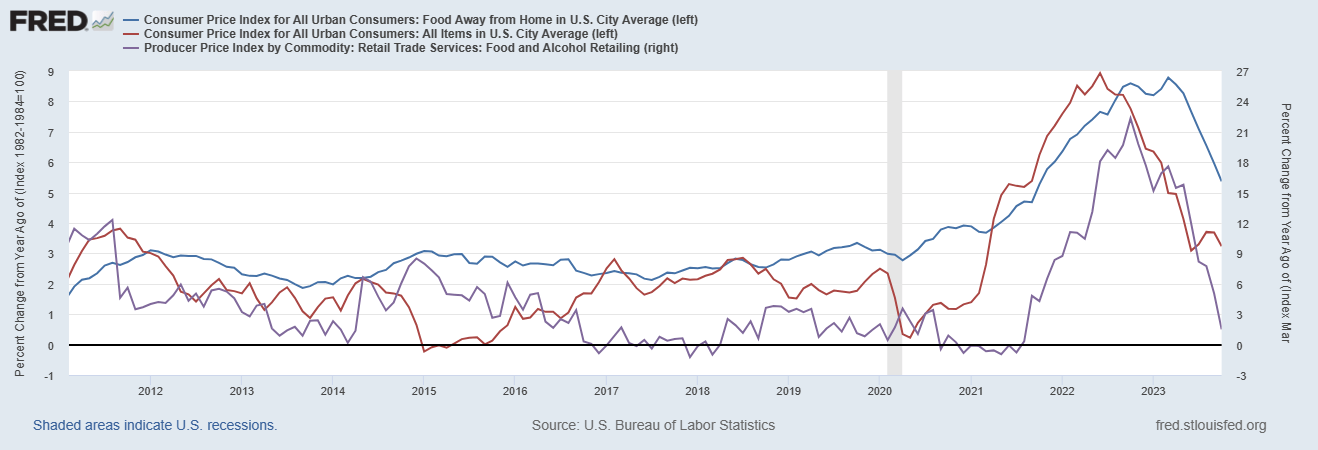

The next chart focuses solely on restaurant statistics and comes from DoorDash .

DoorDash

With restaurant inflation remaining elevated, my presumption would have been that consumers would cut back on eating out to a certain degree.

{kind=link}

Restaurant Inflation (FRED)

Considering the first chart, it is clear that consumers continued eating out during the last two months. Whether this increase was the result of higher frequency/volumes or inflationary pressures are not discussed, so there is no telling as to whether consumers are electively spending more by eating out more or being forced to spend more by eating out at the same frequency. Regardless of how consumer spending gets there, this will only impact Block if overall consumer spending drops off or if inflationary pressures force restaurants into bankruptcy.

Valuation

As I had discerned in my previous report covering Block , I insinuated that the firm is moving closer and closer to acting as a bank as opposed to a pure tech firm. I’ll be the first to admit my thesis at the time was more doomsday than what the economics called for. Though I do anticipate a decline in consumer spending, I believe I was much too early in reaching for a conclusion.

{kind=link}

Corporate Reports

Considering management’s eFY24 aEBITDA target and my margin assumptions, we can create a valuation table pulling forward eFY24 revenue for a price target of $92.48/share, providing us with 28% upside to the current price.

{kind=link}

Corporate Reports

On a peer comps basis, using the same peer group I had used in my initial analysis, we can come up with a slightly higher price target of $98.79/share when using a market cap weighted P/S multiple of 2.90x, calling for near-term margin expansion.

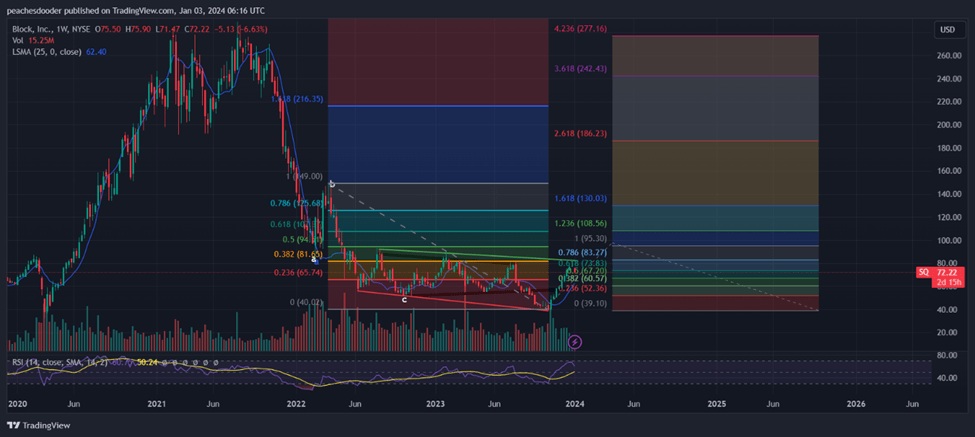

The technical chart tells a slightly different story with an elongated cycle down with declining peaks and bottoms.

{kind=link}

TradingView

If this recent up trend were the start to a new wave, we can expect shares to bounce back to $60/share in the near-term before rerouting to my price target of $98.79/share. This could also very well be a continuation of a down wave, leading to an even further downward trajectory, which was ballpark my initial price target of $30.17/share. The 14-day RSI puts SQ in overbought territory at 60.75, suggesting there may be more near-term selling.

Based on management’s estimates for eFY24 and the technicals, traders may be looking at SQ as a “show me” story in which they want to see the incremental actions take place before pushing the stock price up. Despite the near-term price trajectory, I believe the long-term margin-expanding story will provide growth for the business. I provide SQ with a BUY recommendation with a price target of $92.48/share.

For further details see:

Block's Earnings Will Be Energized By AI (Rating Upgrade)