SQ - Block: Squarely In My Crosshairs For An Undervalued Growth Stock

2023-11-17 06:58:22 ET

Summary

- Block Inc. is a fintech company that has seen its stock price drop by 80%, presenting a potential buying opportunity.

- The company's main business is Square + Cash App, which offers a cohesive commerce ecosystem and financial products for individuals.

- The stock is currently trading at a reasonable multiple for its growth rate, with strong revenue growth and a solid balance sheet.

- There's a large TAM of dated payment systems out there to replace and price growth is now far detached from fundamental revenue growth.

One of the gems of the fin-tech anti-bubble

I enjoy hopping around destroyed sectors and investment categories looking for quality companies under fire. Block, Inc. (SQ), is absolutely one of those. It is forming the same cross-section of fundamentals that led me to my investment and buy on Uber (UBER) stock back in April of this year. It's about 70% up since that article so I'm inclined to revisit this fundamental cross-section with Block Inc.

Down nearly 80%, I was never tempted to make a move on this stock during COVID when the thought process had everyone overly excited for all things tech due to a near non-existent risk-free rate. Boy have things changed. With the FED now holding rates between 5.25-5.5%, extra long duration, pre-GAAP profit darlings have been hammered. This play is now down 80%, has a lot of future growth potential, and trades at very reasonable multiples for its growth rate. Let's examine.

The business

From the 10K :

Square Ecosystem : Square offers a cohesive commerce ecosystem that helps our sellers start, run, and grow their businesses. We combine software, hardware, and financial services to create products and services that are cohesive, fast, self-serve, and elegant.

Cash App Ecosystem: Cash App provides an ecosystem of financial products and services to help individuals manage their money. Cash App's goal is to redefine the world's relationship with money by making it more relatable, instantly available, and universally accessible.

The meat of their business is Square + Cash App. If you haven't seen or interacted with the company's products to date, it is inevitable that one day you will.

Most recent quarter storyline

EPS of $0.55 beats by $0.09 | Revenue of $5.62B (24.40% Y/Y) beats by $182.83M

{kind=link}

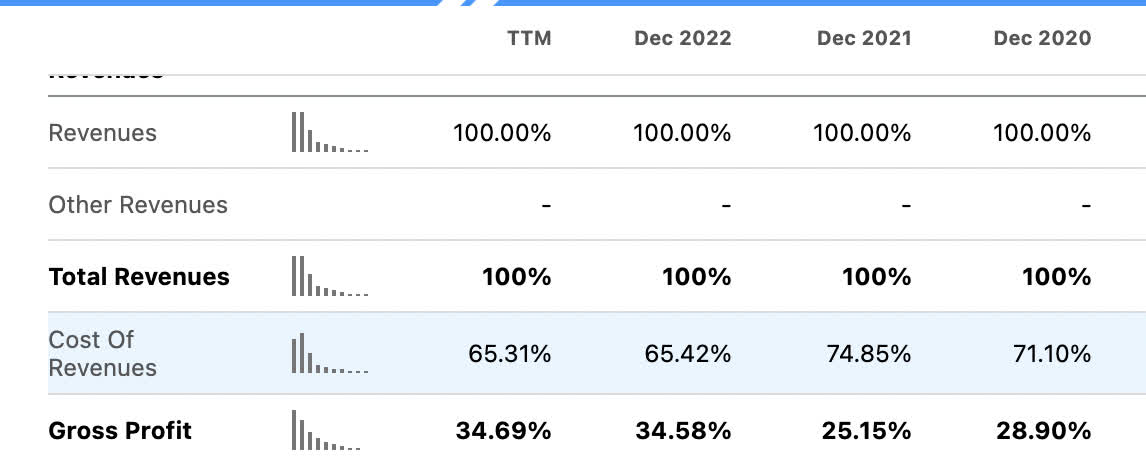

Gross profit continues to grow quarter by quarter, let's take a look at the gross margin trends:

{kind=link}

Highlighting the cost of revenue , the percentage continues to decline while revenue has been ascending. Gross profit margins have improved significantly since 2020. These are all positive trends that I picked up on in Uber's case study as well.

{kind=link}

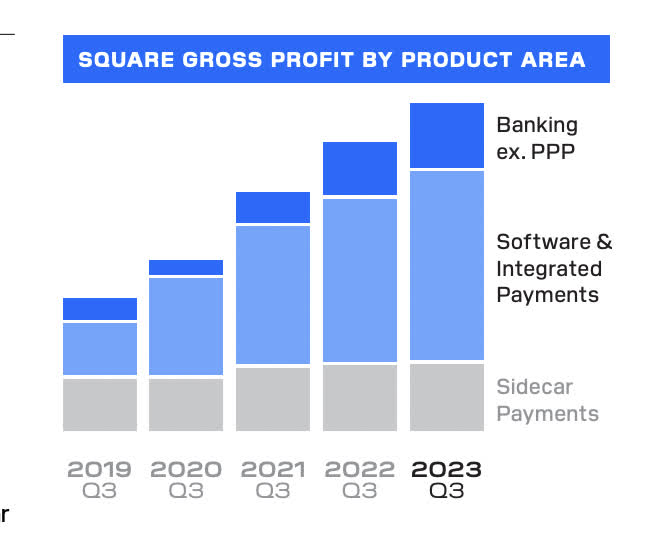

Block Inc. Q3 Investor Letter:

- Software and integrated payments include gross profit from in-person and online software that is monetized via embedded payments and/or monthly software subscription fees.

- Financial Services includes gross profit from Square Banking and instant transfers.

- Sidecar payments include gross profit from Square's Point of Sale app where sellers only use payments without using any software features.

The largest growth segment for Square is in software-integrated payments. More and more small, medium, and large businesses are adopting Square's point-of-sale hardware and integrating business management systems via subscription.

{kind=link}

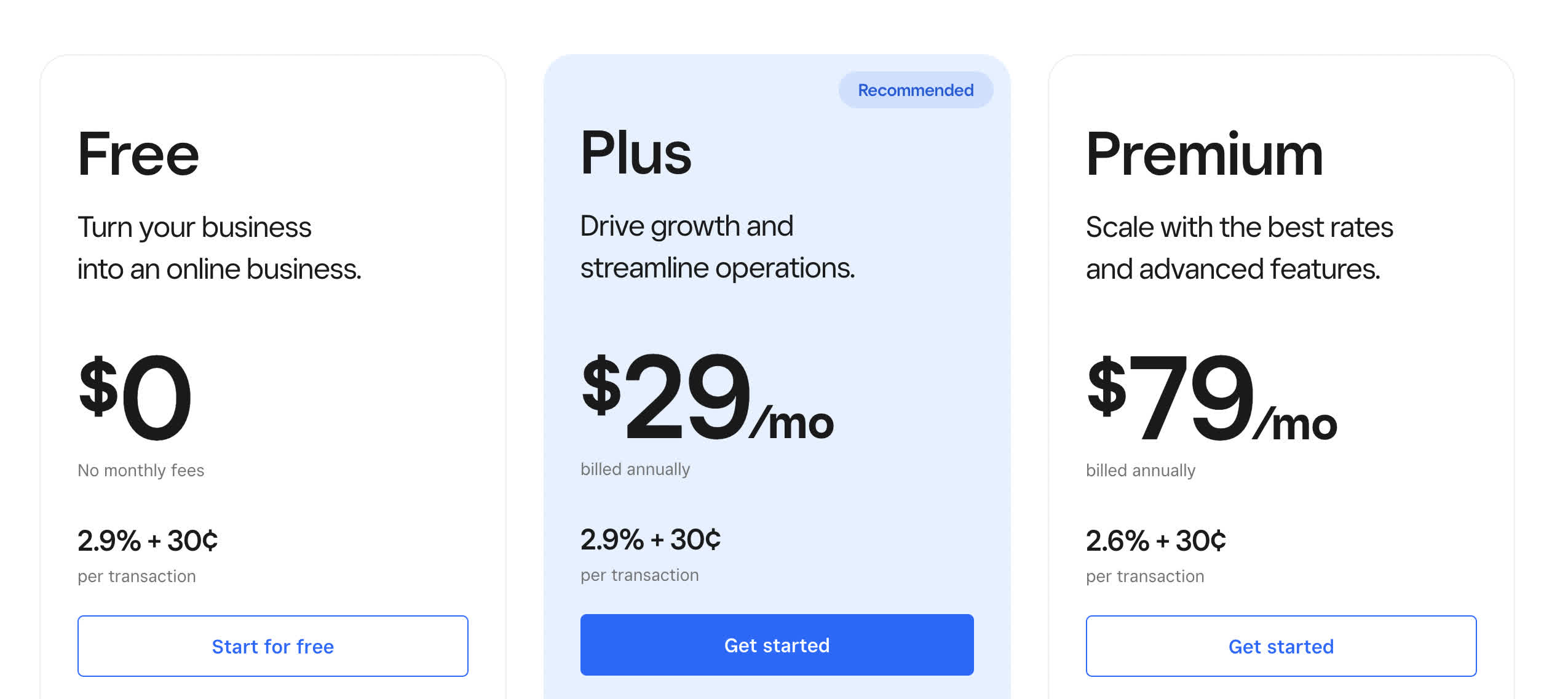

Examples of plans that can be monetized can be seen here. The software services are one monthly fee depending on service level and transactions are another fee. More gross payment volume is the key to revenue growth.

Block Inc. Q3 Investor Letter

Gross payment volume or GPV is up again this quarter. More volume, more users, and larger users of Square products will create more volume for which fees become accretive. The total addressable future market for electronic point-of-sale cash registers is by some estimations close to $20 Billion . With hardware only representing about $145 million of Block Inc.'s revenue, that's a lot of market to absorb. Yes, the hardware has negative margins, but generates more users, more transactions, more fees, and more software subscriptions.

The Chart

Firstly, the chart. Down 80% from the all-time high and now just barely entering value territory, it humbles and reminds me time and time again to be patient. Fundamentals eventually help form a bottom right where a stock should be when the mean reversion occurs. I have seen Block Inc.'s Square products everywhere when visiting small businesses and even some larger ones. They seem to be a perfect fit and replacement for the ancient IBM (IBM) cash registers of yore. Cheap, portable, and easy to set up. I love the prospects at this price.

Heat check

It's hard to track adjusted operating income as everyone's opinion of an adjustment may vary. Y Charts does not have a metric for it, but revenue growth is very suitable in this instance. My Peter Lynch "heat check" to track earnings or revenue growth against share appreciation over the last 10 years is a valuable tool. The growth lines traced one another, and then they didn't. With revenue up 2K% versus 333% share price appreciation, this divergence is a great place to seek out value.

James O'Shaughnessy

James O'Shaughnessy wrote a popular book on stock evaluation called 'What works on Wall Street'. In it, he found the following :

In the original edition of 'What works on Wall Street', O'Shaughnessy wrote that the single-best value factor was a company's price-to-sales ratio (P/S).

O'Shaughnessy used to run O'Shaughnessy Asset Management, LLC, an asset management firm that Franklin Templeton later acquired. Through his writing and research, he reviewed which fundamental premise was most indicative of value and support levels for a stock. He found that price-to-sales was even more effective in predicting value than price-to-earnings or other ratios. I can agree here depending on the stock.

In pre-GAAP profit growth names, I rely solely on this metric in identifying value. Revenue is the lifeblood of profit and the hardest thing to accumulate. If revenue growth is still occurring at reasonable price-to-sales ratios as was the case with Uber, then I am very interested.

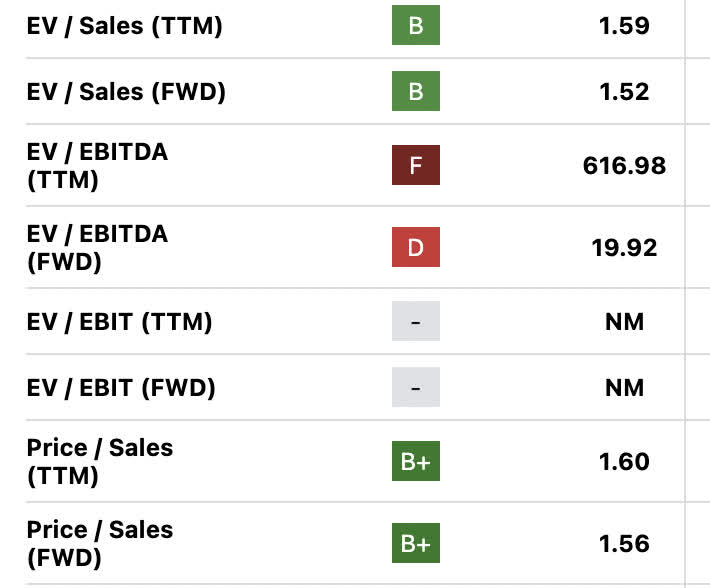

1.5 X Sales

{kind=link}

We can see both on an EV/Sales and price-to-sales basis that the company is trading at around 1.5 X. This and below was the baseline O'Shaughnessy pointed out to hunt for value. He later found that EV/Sales is a more accurate measure to account for debt in the capital stack or leverage to buy revenue. In the case of Block Inc., the two ratios are nearly identical and we have ongoing revenue growth.

{kind=link}

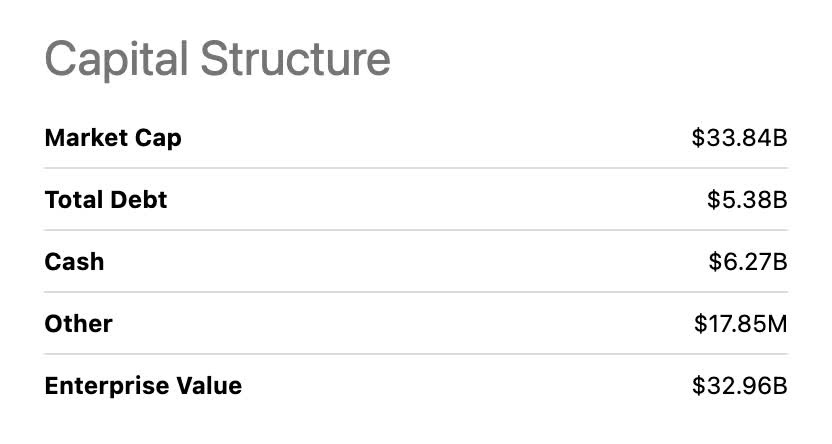

Cash is above debt. Market Cap is barely above Enterprise value. Since enterprise value is (debt+equity)- cash, the low amount of debt and relatively high amount of cash make the two values about the same. This is excellent because EV/Sales was found to be even more accurate than price-to-sales. This is an A+ balance sheet.

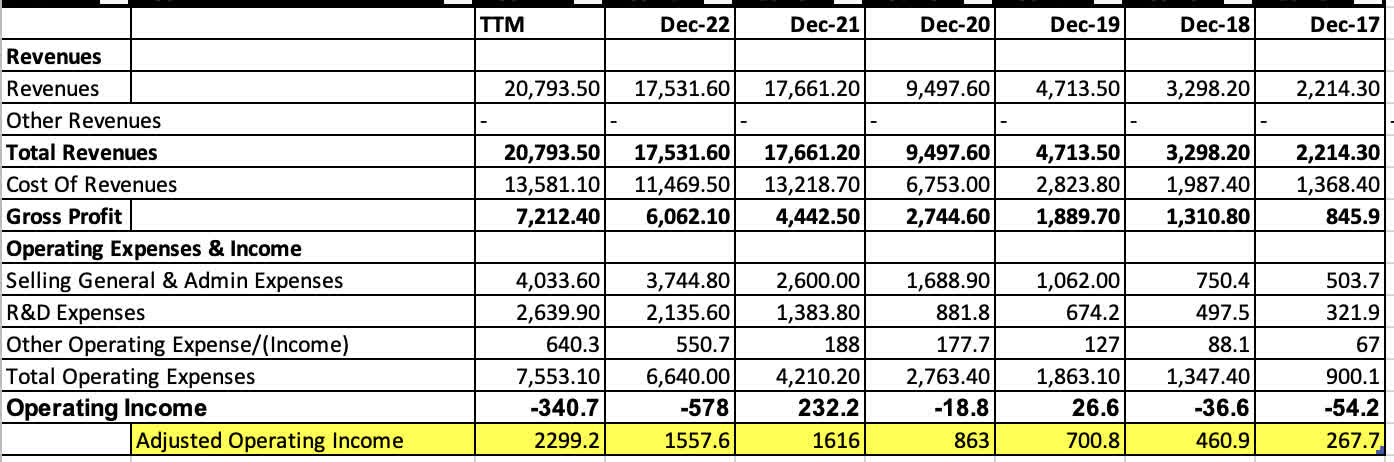

On an absolute basis, we do see a bit of a plateau in revenue growth TTM, but the past near-decade has been an absolute parabolic line. From $552 million at IPO to $17.53 Billion today.

{kind=link}

We currently sit at about 2018 prices on the stock. Let's drill down on revenue growth since then just for a visualization:

In this time clip, we have only a .71% share price appreciation versus 431.6% revenue growth. Very nice indeed.

The turn on adjusted operating profit

My Own Excel, Data From Seeking Alpha

{kind=link}

The way I like to look at an adjusted operating profit is the same way Nick Sleep and Qais Zakaria from the Nomad Partnership did , by adding back R&D to operating income. This doesn't work for all sectors, primarily pharmaceuticals, and semiconductors that need R&D constantly to meet the demand of their end users. As for intangible assets and tech companies, it's highly debatable which portion is necessary and which portion is nearly equivalent to retained earnings.

This is right out of the Jeff Bezos playbook where Amazon (AMZN) keeps spending enormous amounts on R&D as a tax shelter and a revenue growth mechanism. Big Tech can be way more profitable than they are. They just choose not to pay taxes and instead spend money on new ideas and product improvements which will generate even more revenue when you have great minds putting the capital to work. CEO Jack Dorsey is now fully focused after selling off Twitter and is a brilliant mind.

In this instance, Block Inc. has been profitable on this adjusted basis since 2015. They just never sold at a price-to-sales ratio that I like. Now that the two are being consummated, I'm starting to buy.

{kind=link}

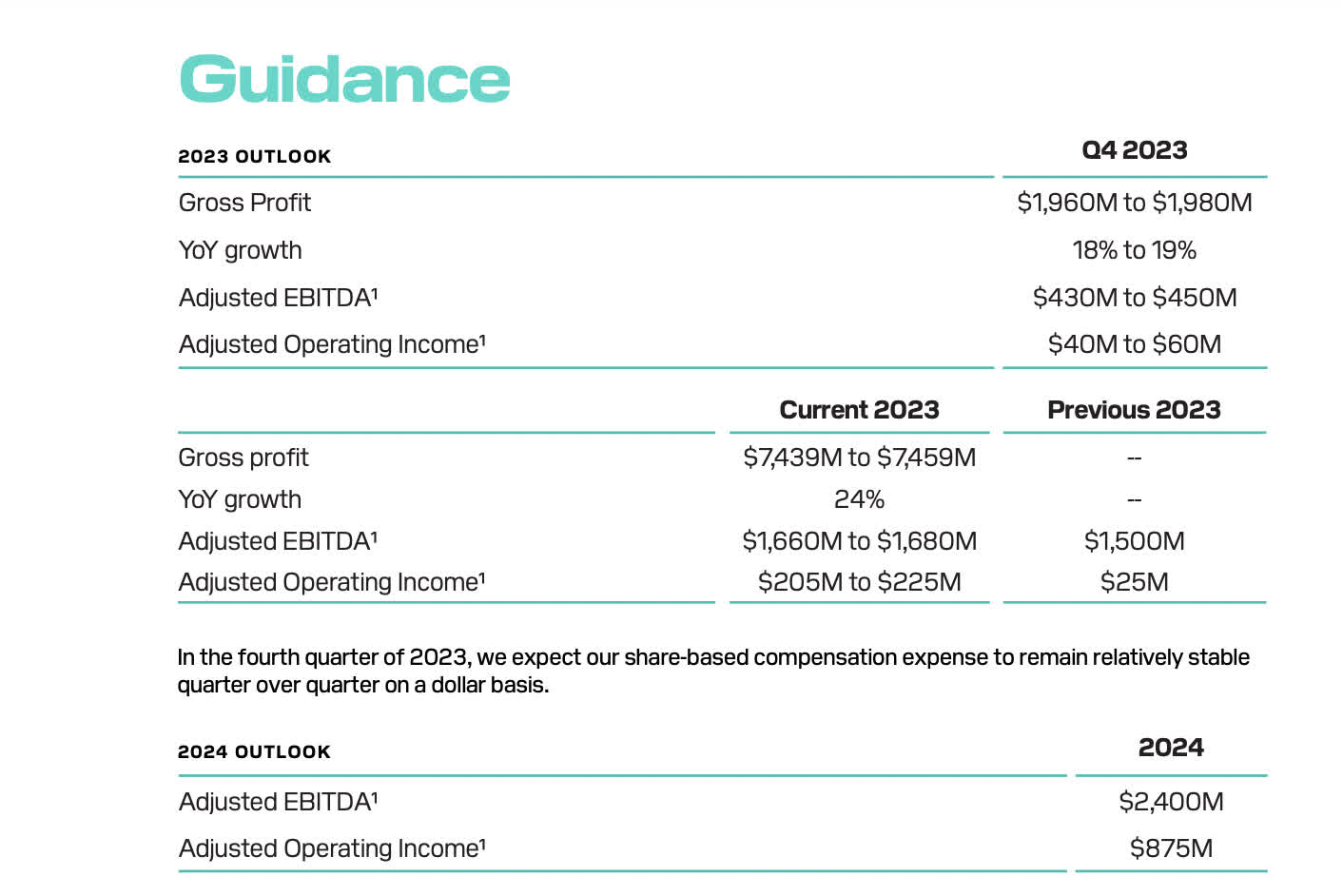

The forward guidance in adjusted EBITDA looks pretty close to what I came up with on a TTM basis for adjusted operating income backing out R&D. Uber's forward to current numbers also penciled out similarly when I did this comparison in my previous article on Uber . Running this exercise can be a pretty accurate way of preemptively anticipating adjusted EBITDA.

Conservative value

Looking at Forward guidance on Adjusted EBITDA at $2.4 Billion, the stock currently trades for around 14 X Forward numbers. Looking at the growth from the Excel sheet using the backed-out R&D method as a proxy, the 5-year average CAGR in adjusted operating income is 26.8%. Taming it down to a 25 multiple, which was another Peter Lynch PEG ratio guideline [don't go over 25 % growth assumptions], 25 X 2.4 Billion would get us a $60 Billion market cap. Divide that by shares outstanding of 614 million TTM and I get a fair price of $97.7 / a share . Almost a 2 X upside with a pretty conservative valuation.

Growth outlook

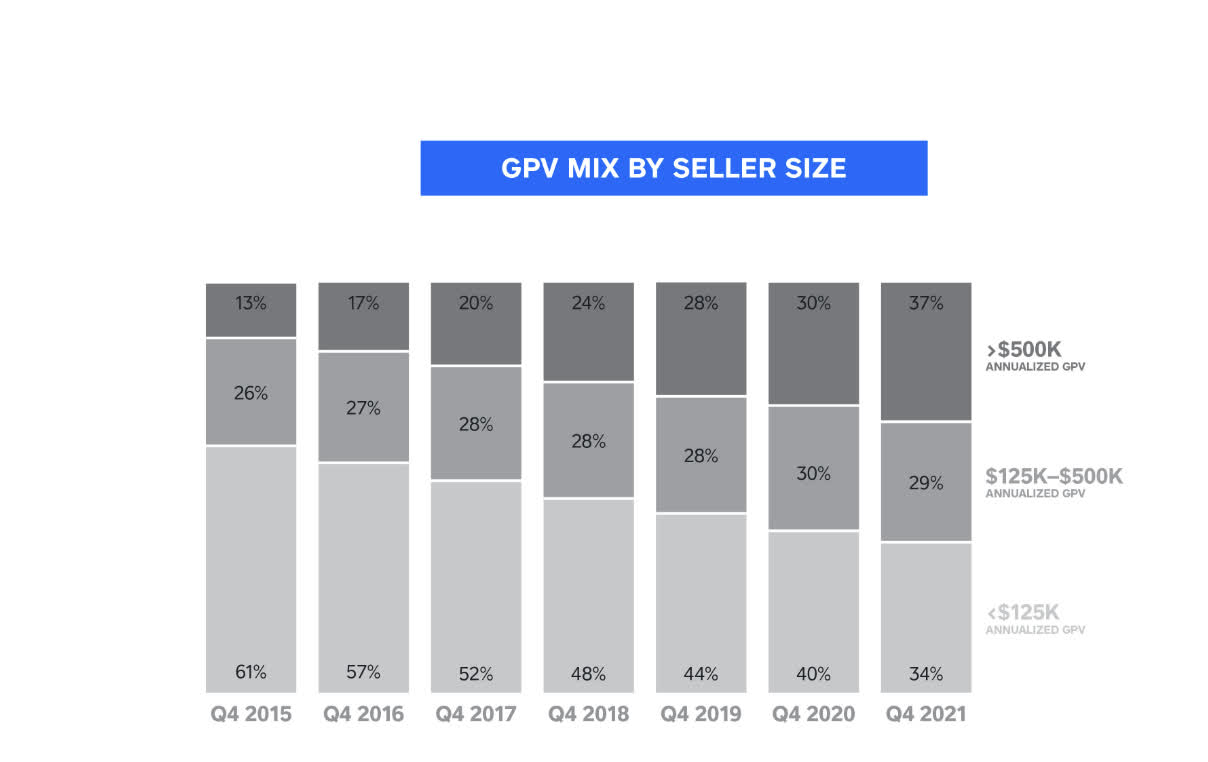

Seller size is growing

{kind=link}

Great illustration from the most recent 10K. The GPV per seller is increasing. Larger businesses, and larger payment volumes mean that Square especially is gaining a foothold in larger and larger businesses. The point of sale registers are becoming more and more ubiquitous. Competitor Clover has many that I bump into as well, but I notice far more Square point-of-sale registers at least in my neck of the woods.

Square points out that its main advantage over Clover is that they are a merchant of record and Clover is not :

Square is the merchant of record. This means we manage payment processing, chargebacks, and PCI compliance (without charging you hefty compliance fees). We even offer offline mode, so you can continue to take payments when your internet is temporarily unavailable.

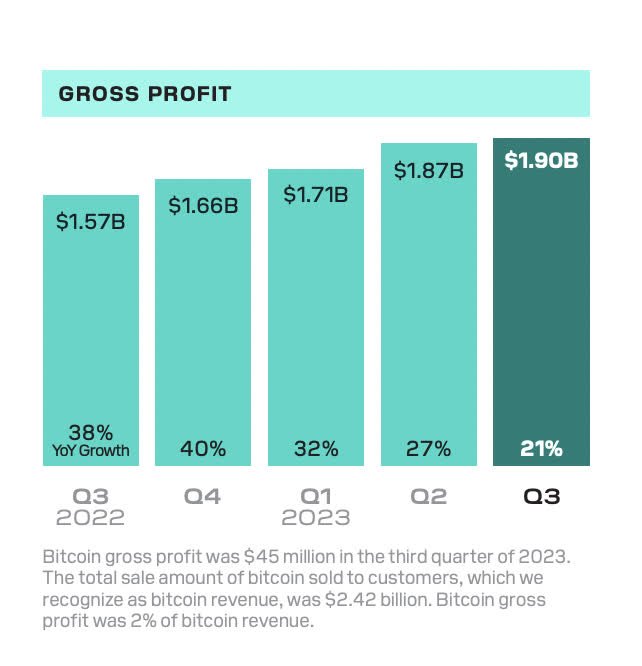

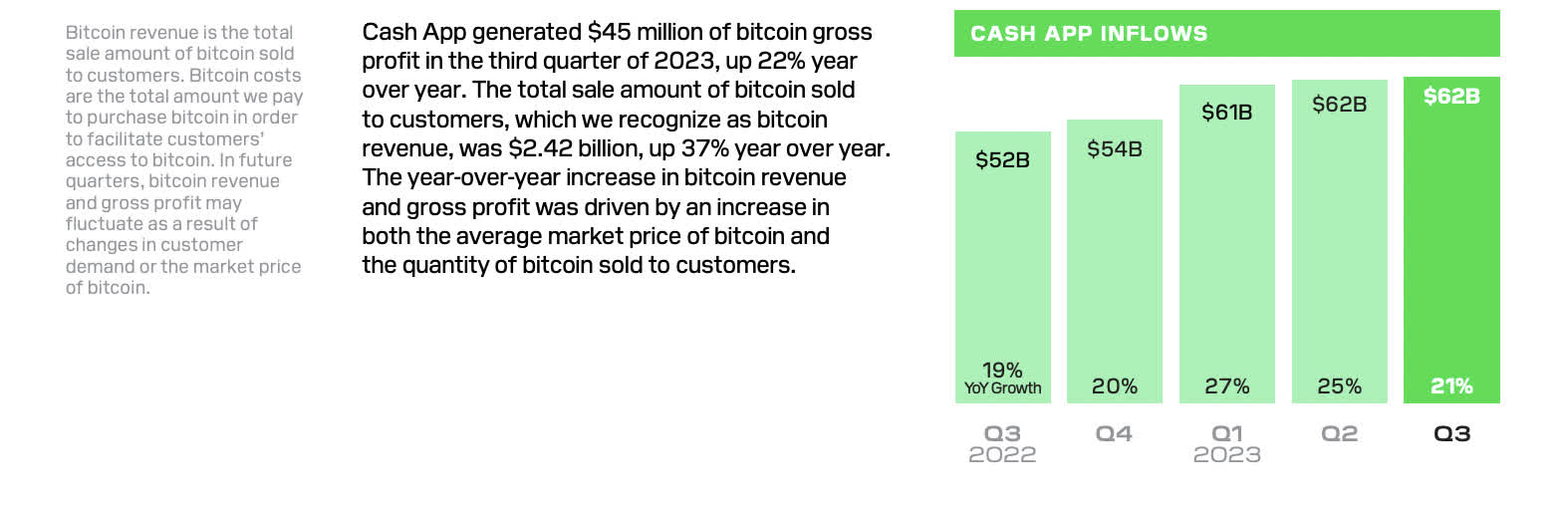

Cash app inflows continue to soar

{kind=link}

We can see as highlighted by the Q3 presentation, influxes in bitcoin-related revenue continue to soar. Although this business only has about a 2% margin, pulling new users and businesses into the cash app ecosystem can generate more fees that range from .5- 1.75% per transaction. More users more gross payment volume= more fees.

Risks

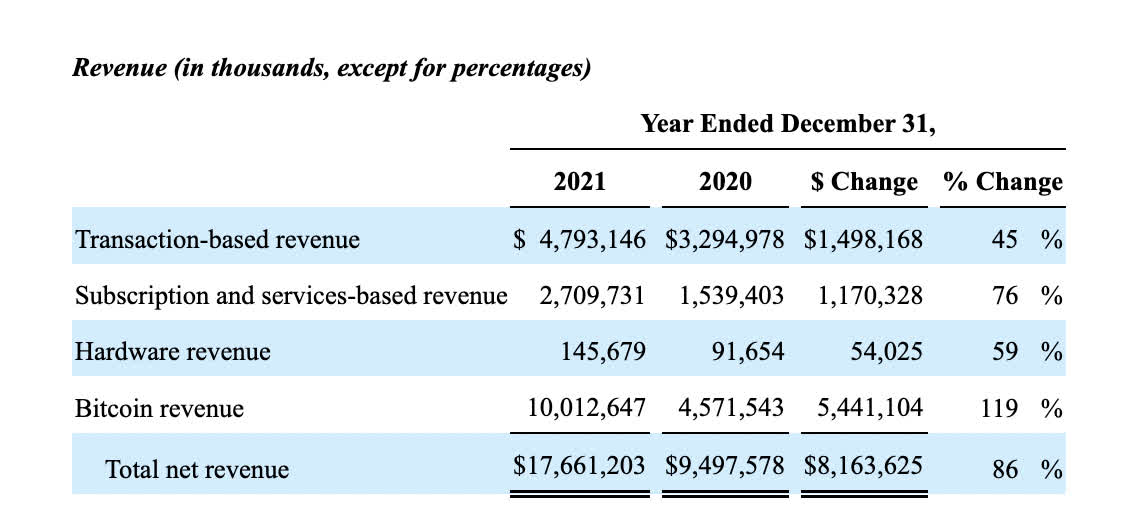

Revenue sources and growth

{kind=link}

The aforementioned bullish case on revenue growth is also highly tied to Bitcoin (BTC-USD). Very large increases in revenue growth are attributable to inflows of capital into cash apps to buy, sell, and transact Bitcoin. At this point with the coming soon spot Bitcoin ETF, Bitcoin is becoming an international non-nation state store of value and transact-able currency. I do not own any or transact with it, but at this point, crypto as a means of non-nation state-backed currency has its foothold. The store of value argument is another topic, but a wider and wider audience wants it as a means of transaction.

Should the SEC or other governmental bodies seek a way to ban or severely regulate Bitcoin and other cryptocurrencies, this could evaporate much of the revenue growth.

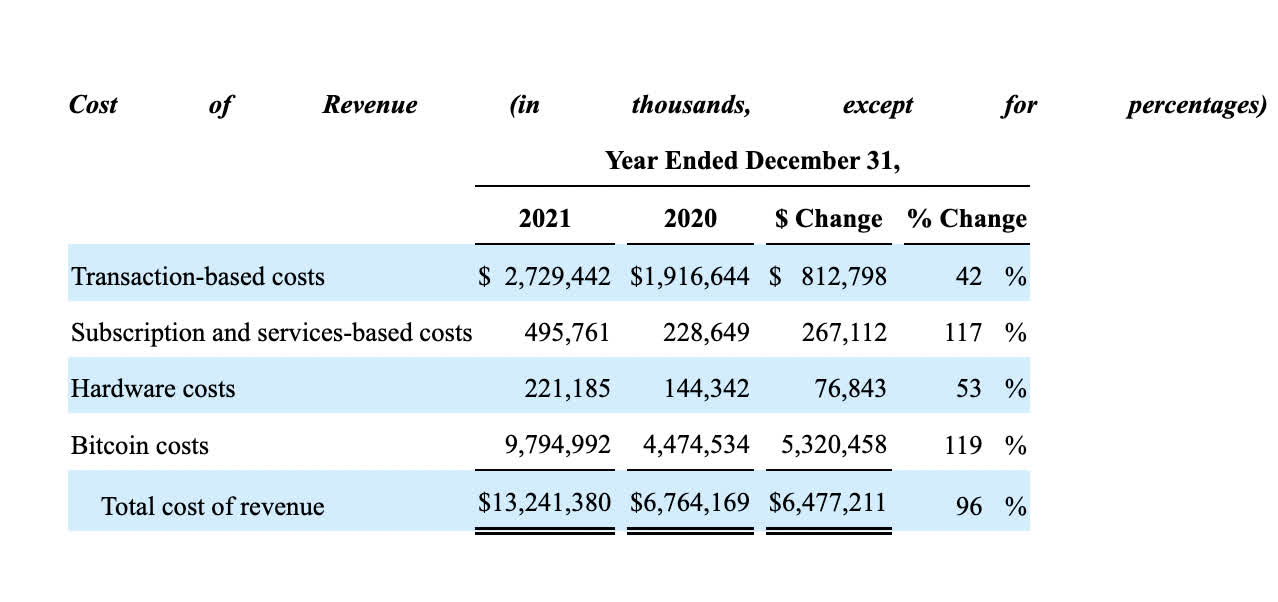

Cost of revenue

{kind=link}

Luckily when looking at the BTC business from a cost of revenue point of view, it is also their thinnest of margins across the sources of revenue. $9.8 Billion in costs versus $10 Billion in revenue is only about a 2% margin.

The main goal is to bring in capital and users as subscription-based services have the highest margins. These come mainly from the small business services through Square. Cash App also has a business account service that charges 2.75% on each received payment to a small business. Pulling in more users to the Square/Cash App ecosystem is the primary goal. The BTC users are a unique segment where there are not a lot of traditional competitors.

Conclusion

I am adding this along with PayPal Holdings (PYPL) to my active buying roster. Both have declined about 80% from their peaks and both are in a clear fin-tech anti-bubble. I still remember the days when analysts on CNBC were arguing why both of these should soon get back over their highs after a pullback in 2021.

What fundamental basis they were using, you got me. I guess when you focus on soundbites rather than fundamental historical analysis, which takes a lot of reading, analysis becomes myopic and limited to momentum. I have loved Block, Inc. here for a long time buy and hold. There's a large TAM of dated payment systems out there to replace and price growth is now far detached from fundamental revenue growth.

For further details see:

Block: Squarely In My Crosshairs For An Undervalued Growth Stock