PYPL - Block: Turnaround Underway

2024-01-16 18:01:02 ET

Summary

- Block stock recently doubled in just two months.

- Management expects GAAP operating profitability in 2024.

- They also hope to achieve the Rule of 40 by 2026.

- It looks like management has turned around the stock for good.

- Despite the recent rally, shares are still undervalued.

Introduction

I wrote a Block, Inc. ( SQ ) piece a few months ago, pointing out that the stock had sold off substantially, to a point where I felt that the bottom was near:

Following its huge selloff back to its Covid lows, Block stock now trades at a wide margin of safety with substantial upside potential as it trades near a major support level. Perhaps, this could be the bottom for the stock.

Not long later, the stock did indeed bottom, rallying 100% from its low of $40 to $80 in just two months.

As it turned out, a few catalysts fueled the rally, namely blowout earnings, a strong outlook, and the recent crypto surge.

And despite the recent rally, I believe shares are still attractive today - it seems that Block's turnaround story has only just begun, which should present more upside for the stock for years to come.

Growth

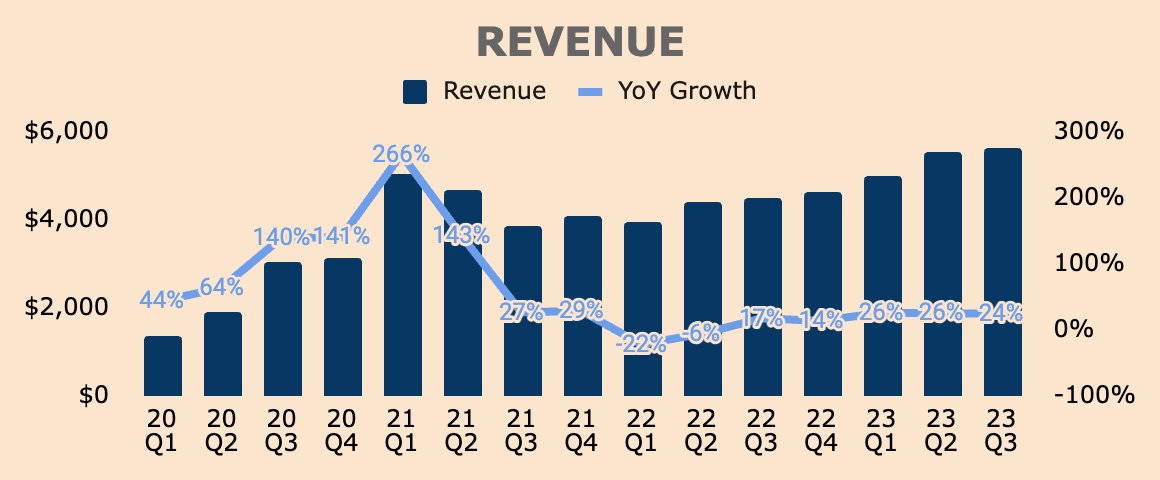

Looking at growth, Q3 Revenue grew 24% YoY to $5.6B, which happened to be a record high for the company. This also beat analyst estimates by $190M or 3.4%.

The strong performance was mainly driven by the continued growth of the Square and Cash App ecosystems, as well as the surge in Bitcoin Revenue, which was $2.4B in Q3, up by 37% YoY.

Given the fact that Bitcoin is highly volatile and unpredictable, I never liked how the company recognizes Bitcoin Revenue - it makes YoY comparisons particularly difficult.

{kind=link}

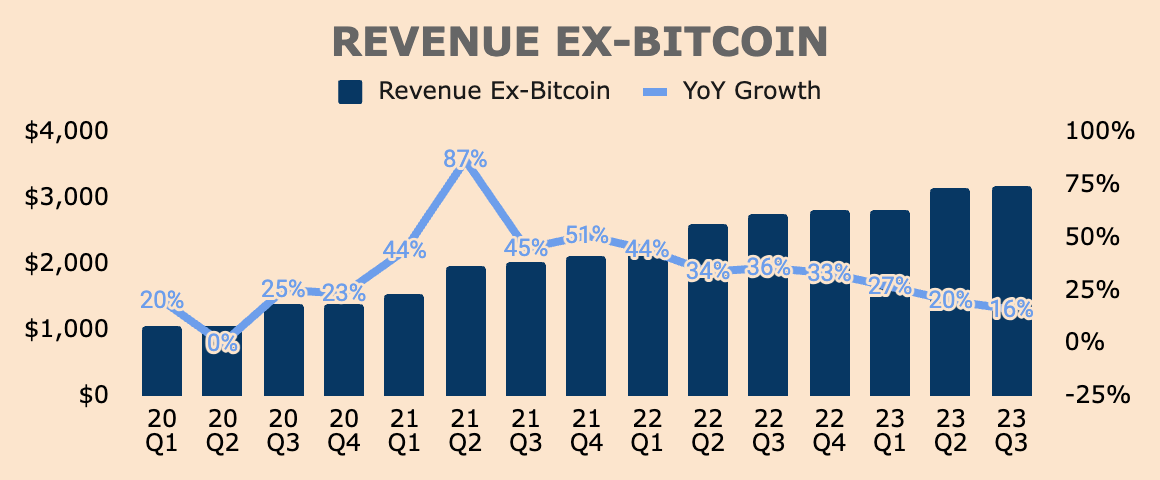

That said, I prefer to analyze the company's financials without the Bitcoin component. In Q3, Revenue Ex-Bitcoin was $3.2B, a 16% increase YoY. Despite the growth slowdown, this metric was also at a record high, which reflects Block's unique value proposition and strong execution.

{kind=link}

Growth was driven by a 10% YoY increase in Gross Payment Volume (GPV), which totaled $60.1B in Q3. If you haven't noticed, Revenue Ex-Bitcoin grew faster than GPV, implying better monetization rates across Block's product portfolio.

Below are a few metrics that I like to track to assess Block's overall monetization rate.

Author's Analysis

As you can see,

- Transaction Revenue as a percentage of GPV [A] has been declining gradually, down from 2.94% in Q1 of 2020 to 2.76% in Q3 of 2023. This metric is Square-dominant, which may mean that Square is losing its pricing power.

- Subscription and Services Revenue as a percentage of GPV [B] , on the other hand, has been improving over the last few years, up from 1.15% in Q1 of 2020 to 2.49% in Q3 of 2023. This metric is Cash App-dominant which suggests improved monetization for the segment.

- Add A and B together, you get the company's Ov erall Monetization Rate . As you can see, the metric is trending up nicely, up from 4.10% in Q1 of 2020 to 5.25% in Q3 of 2023. On a YoY basis, the metric is up 27 basis points.

A higher monetization rate is essential for long-term shareholder value creation and that is what Block has been able to demonstrate over the last few years.

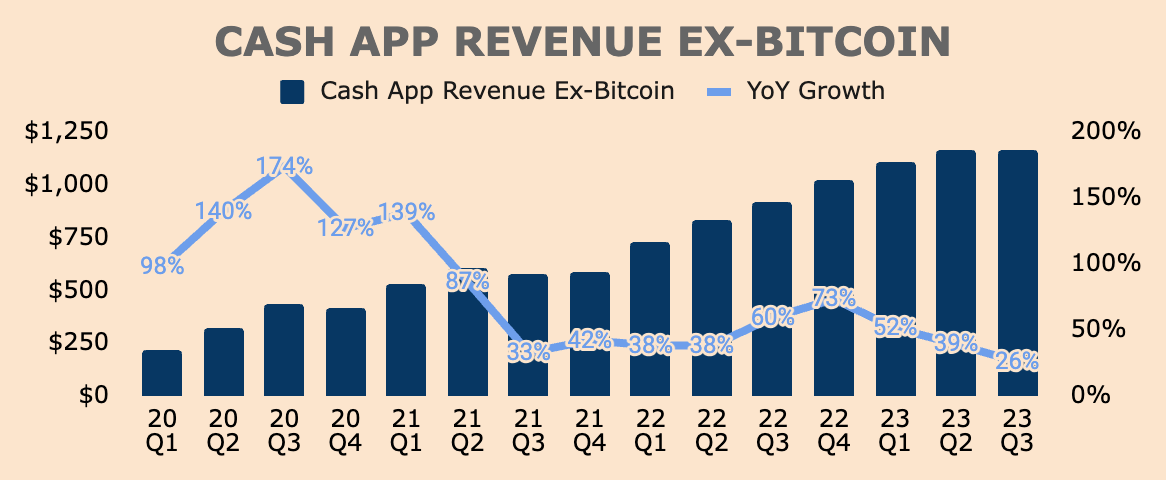

Looking closer at each segment, Cash App Revenue was $3.6B in Q3, up 34% YoY. Again, this included $2.4B of Bitcoin Revenue - Ex-Bitcoin, Cash App Revenue would have been $1.2B, up by 26% YoY. As you can see, growth is slowing down rapidly, which I expect to stabilize in the high teens in 2024.

{kind=link}

Regardless, growth in Cash App was due to $1.0B of Cash App Subscription and Services Revenue, which increased 29% YoY. This was bolstered by:

- Higher monetization rates as mentioned above.

- Monthly Transacting Actives of 55M, up 11% YoY.

- Cash App Pay Monthly Actives of over 2M, up 100% QoQ.

- Inflows of $62B, up 21% YoY.

On the other hand, Cash App Transaction Revenue was $121M in Q3, up only 2% YoY as Cash App GPV only grew by 1% YoY in the quarter, to $4.4B. This is not an issue since Transaction Revenue only makes up a small portion of Cash App Revenue, but it's definitely something to be aware of.

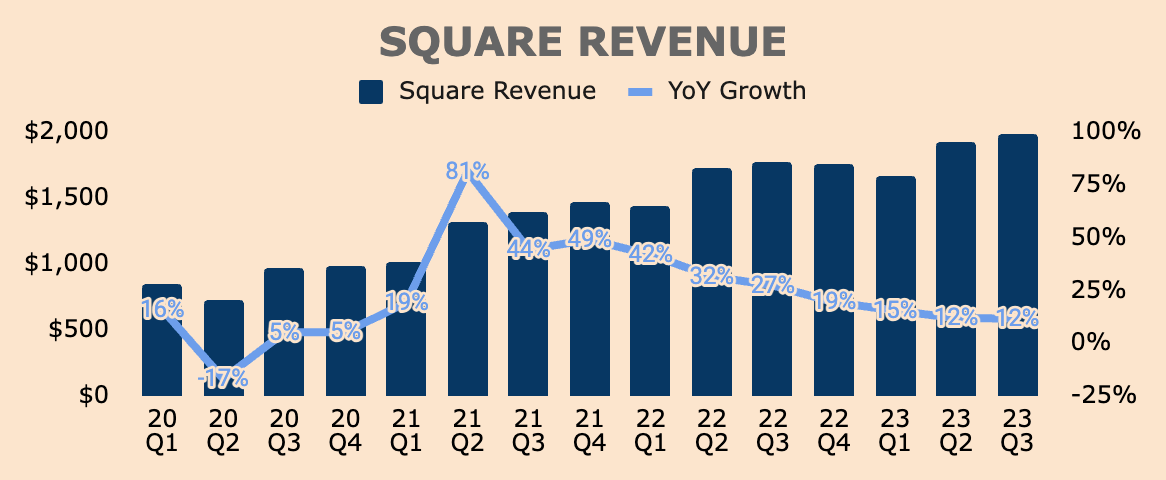

While Cash App GPV has been lagging, Square GPV grew 11% YoY to $55.7B. This was mainly driven by International Square GPV, which grew 28% YoY. On the other side, US Square GPV grew 9% YoY.

This consequently led to a 12% growth in Square Revenue in Q3, to nearly $2.0B. As you can see, it is a record-high for the segment as well.

{kind=link}

All in all, the Cash App and Square ecosystems continue to grow as fintech applications gain more adoption and legacy financial services fall out of favor.

The most important update is that Cash App continues to attract more users to the platform, amassing 55M Monthly Transacting Actives as of Q3, which could be further monetized.

As more users join the platform and as Overall Monetization Rates improve, Block's ecosystem of ecosystems will inevitably enjoy powerful network effects, which should drive robust growth and profitability moving forward.

Profitability

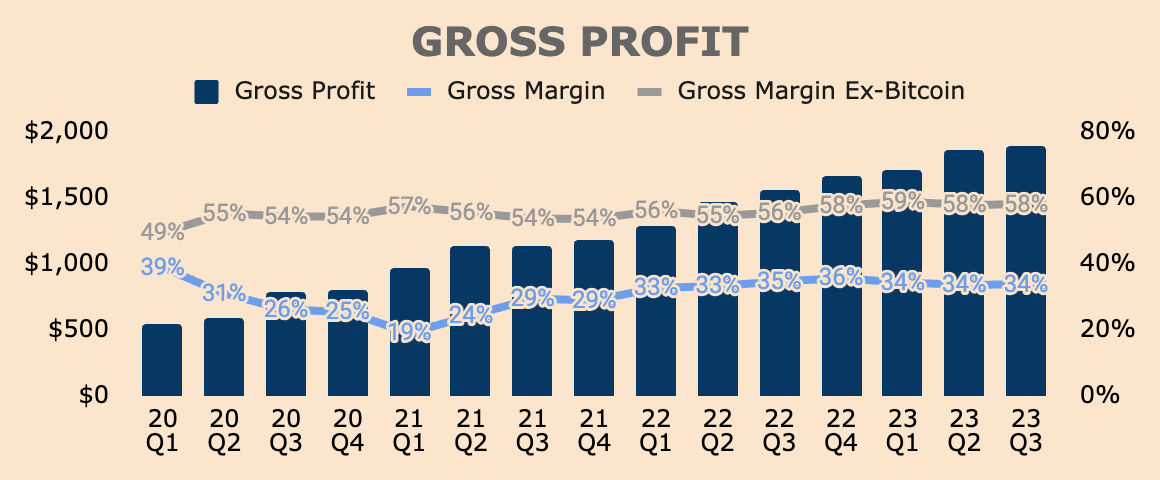

Turning to profitability, Q3 Gross Profit was $1.9B, up by 21% YoY. This represents a 34% Gross Margin.

I've also included Gross Margin Ex-Bitcoin, which removes Bitcoin Revenue and Cost of Bitcoin from the equation - excluding Bitcoin gives us a clearer view of how margins are trending.

That said, Q3 Gross Margin Ex-Bitcoin was 58%, a 200 basis point improvement YoY, demonstrating economies of scale within the Block ecosystem.

{kind=link}

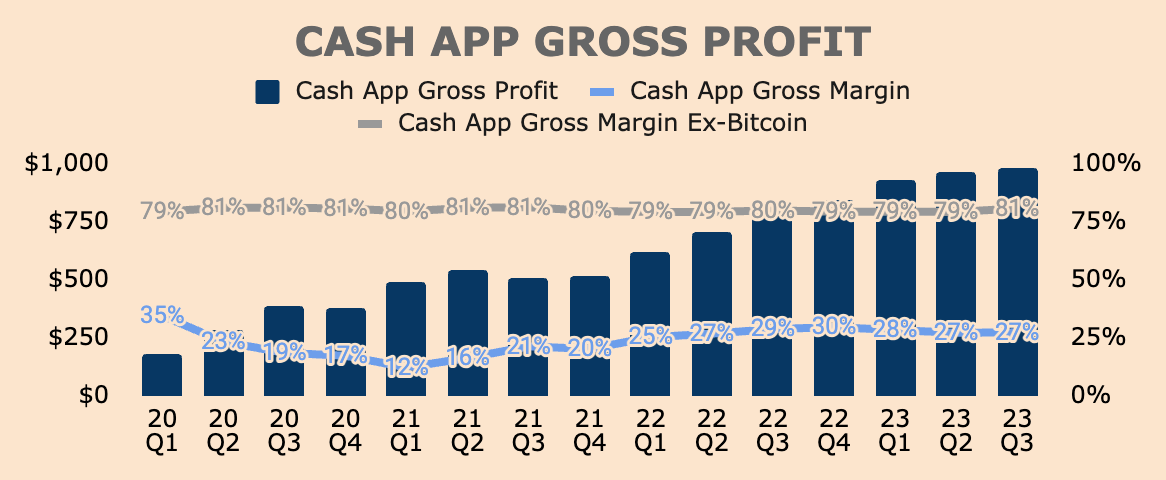

Breaking it down by segment, Q3 Cash App Gross Profit was $984M, which represents a Gross Margin of 27%. This doesn't look impressive at all, and this is because Bitcoin contributed 68% of Cash App Revenue while only producing 5% of Cash App Gross Profit.

{kind=link}

If we remove Bitcoin, we can see that Cash App is a very high-margin business, with a Gross Margin of 81% as of Q3. You can also see that Cash App maintained this high Gross Margin the entire time, which shows the durability of its business model.

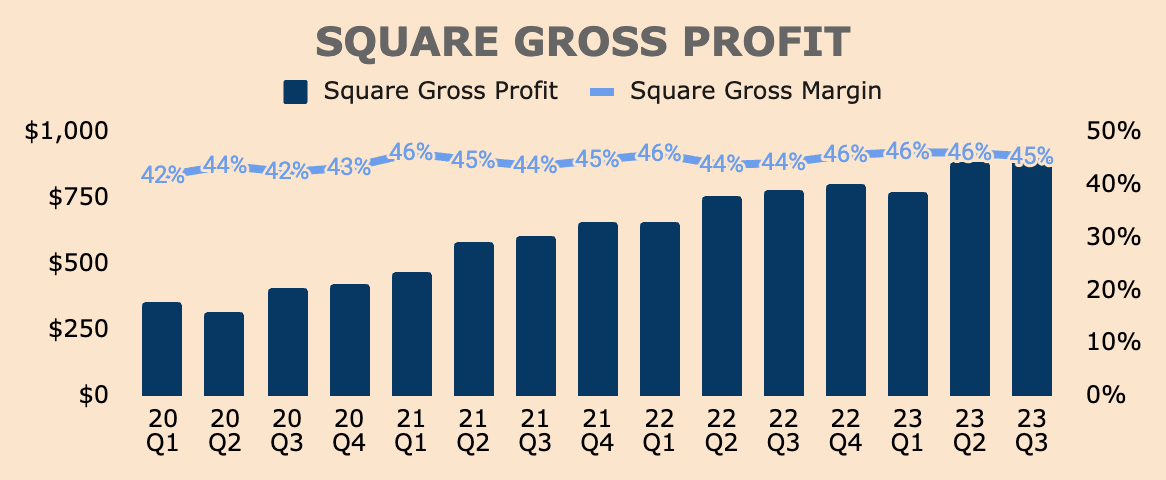

Moving on, Q3 Square Gross Profit was $899M, which represents a Gross Margin of 45%. As you can see, Square Gross Margin remained stable as well, which is great to see.

{kind=link}

Of important note, Square's Gross Profit growth of 15% was driven by:

- Gross Profit from vertical POS solutions like Square Appointments and Square for Restaurants, which grew 29% YoY.

- Gross Profit from banking products like Square Loans and Square Debit Card, which grew 20% YoY.

What this tells us is that businesses are looking for more specific payment software with integrated banking products and services to manage their cash inflows and outflows better. With Square's all-in-one hybrid payment platform, Gross Profit growth from these products should remain robust in the foreseeable future.

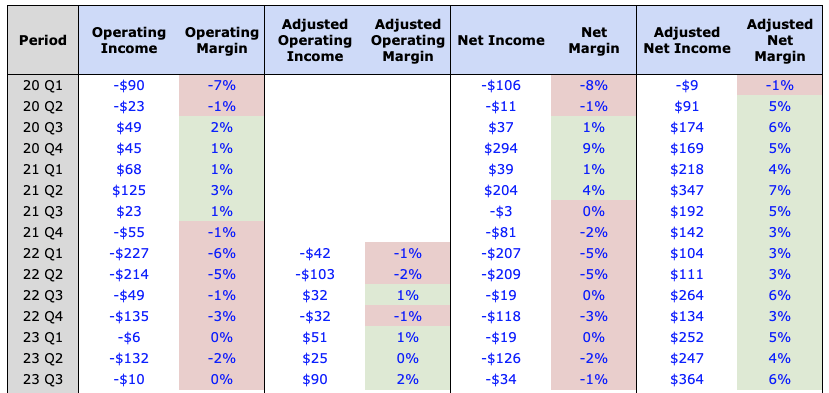

Moving down the income statement, Q3 Operating Income was $(10)M while Adjusted Operating Income was $90M.

In terms of the bottom line, Q3 Net Income was $(34)M while Adjusted Net Income was $364M.

{kind=link}

In my previous article, I mentioned that GAAP profitability would be a major catalyst for the stock, and judging by the significant sequential improvement in all four of these metrics, it looks like the market is pricing in GAAP Operating and Net Income profitability earlier than previously anticipated - thus the recent surge in the stock price.

In my opinion, GAAP Net Income profitability will be the next catalyst for the stock.

Whatever it is, there's no doubt GAAP Net Income profitability will happen in 2024, as the company focuses on "driving efficiencies to deliver long-term growth" and putting "an absolute cap" on the number of employees.

We are implementing an absolute cap on the number of people we have at our company. We expect to be a smaller team by the end of 2024 compared to where we are today. Our cap of 12,000 people compares to our current size of just over 13,000 people as of the end of the third quarter.

(COO and CFO Amrita Ahuja - Block FY2023 Q3 Earnings Call ).

That said, we can expect more layoffs in 2024, which should drive meaningful operating leverage, ultimately pushing the company toward GAAP profitability.

With the company ever-focused on delivering growth, managing headcount, and achieving profitability, it seems that management has turned the stock around for good.

Health

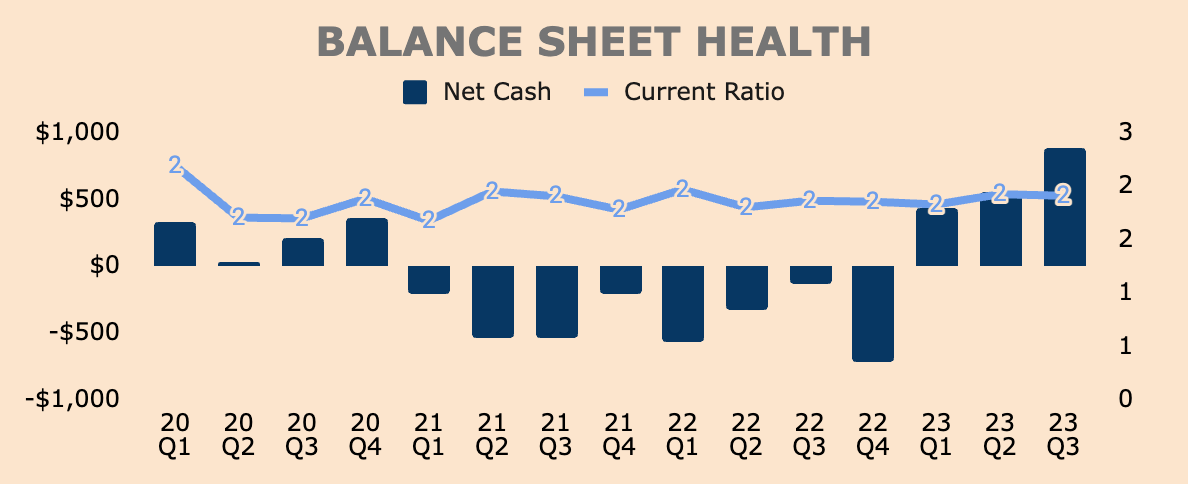

Block's balance sheet is getting stronger with each passing quarter.

In Q3, Block had $6.3B of Cash and Short-term Investments and $5.4B of Total Debt, which puts its Net Cash position at about $0.9B.

As you can see, Net Cash has been improving over the last few quarters as the company shifted its attention to cost savings and profitability. Moving forward, we should see Net Cash continue to build from here.

{kind=link}

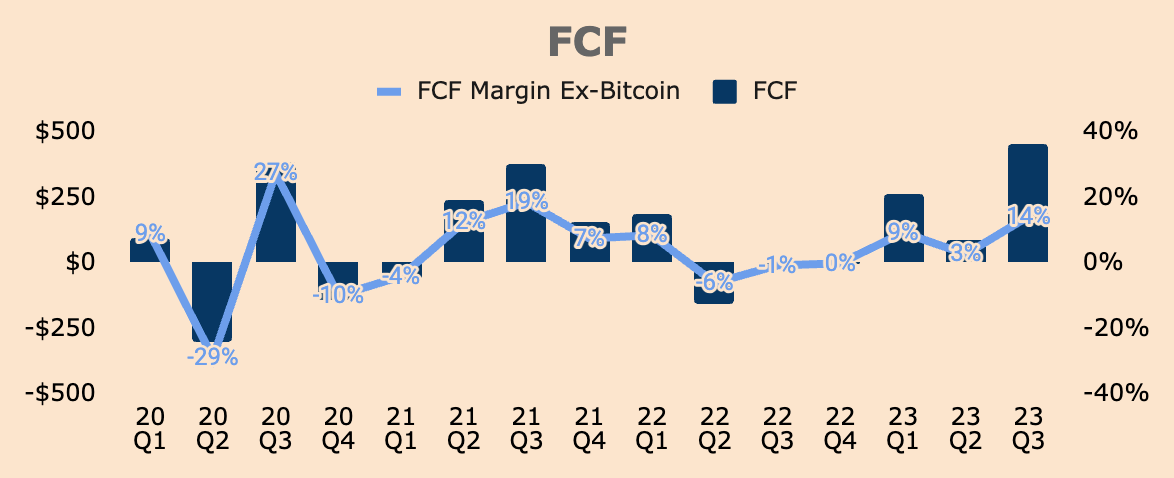

That's because Block is generating more and more cash. In Q3, Block produced a Free Cash Flow of $454M, which is an FCF Margin Ex-Bitcoin of 14%, up from (1)% last year.

{kind=link}

With robust FCF in place, Block will have more cash for expansion, debt repayment, as well as share buybacks, which the company recently announced.

On that last point, Block introduced a $1B buyback program, which should offset shareholder dilution from Stock-based Compensation - in Q3, shares outstanding increased by 3% YoY.

It's also great to know that the board authorized the buyback program on October 26 last year, which was very close to the low of $40 a share. Hopefully, the company bought back a decent amount of shares before the rally - kudos to management if they did.

Outlook

In terms of the outlook, management provided the following guidance:

{kind=link}

In Q4, management expects a Gross Profit of about $1,970M, which is about a 19% growth YoY. This is lower than Q3's growth of 21% so expect growth to slow down even more.

Nevertheless, Block expects to close the year with $7,449M of Gross Profit, which is up 24% YoY.

In addition, Q4 Adjusted Operating Income and Adjusted EBITDA are expected to be lower than Q3's figures, at $50M and $440M at the midpoint, respectively. As a reminder, GAAP Operating Income was still negative in Q3, which means GAAP profitability is unlikely in Q4.

On the bright side, management raised their full-year 2023 profit guidance:

- Adjusted Operating Income of $215M (raised by $190M).

- Adjusted EBITDA of $1,670M (raised by $170M).

Moving on, management expects a significant improvement in Adjusted Operating Income in 2024 to $875M, as the company focuses on "disciplined growth and pursuing cost efficiencies". For context, that is a 300% increase YoY. More importantly, management expects GAAP operating profitability in 2024.

Similarly, 2024 Adjusted EBITDA is expected to improve by nearly 50% YoY to $2.4B.

In other words, profitability is expected to accelerate in 2024.

At the same time, management laid out the following investment framework, which should drive long-term value for customers and shareholders.

We believe we will reach Rule of 40 in 2026, with an initial composition of at least mid-teens gross profit growth and a mid-20% Adjusted Operating Income margin .

Keep in mind that:

Adjusted Operating Income margin is defined by dividing Adjusted Operating Income over a given period by Gross Profit over the same period.

(Block FY2023 Q3 Shareholder Letter).

Given the trajectory of the business, Rule of 40 by 2026 is very much possible.

Note: Rule of 40 is an investment principle commonly used for software companies, and it states that the combined growth rate and profit margin of the company should equal or exceed 40%.

On growth, Block still has a long growth runway with "less than 5% penetrated against our $200B total addressable markets", which will expand over time as the company introduces new products and captures new demographics.

On profitability, management highlighted three key initiatives to boost profitability:

- Employee cap of 12,000, down from 13,000 currently.

- Reduce spend across corporate overhead areas.

- Gain operating leverage through scale and optimizing unit economics.

In short, the outlook given by management is very positive with growth expected to remain robust and profitability expected to accelerate through 2026, eventually reaching the Rule of 40.

Over the last few years, Block has always operated on shaky profitability with little to no improvement. Now, management has presented a definite path towards improved, sustained profitability, which should unlock value for shareholders.

No wonder the markets reacted so positively following Block's Q3 earnings releases.

Valuation

As you know, Block's stock rallied more than 100% from its bottom of $40 in October. We can list out a few reasons that catalyzed the sharp rebound:

- Strong earnings and outlook.

- Initiated a $1B buyback program.

- Broad market and Bitcoin rally since late October.

- Major technical support at $40.

- Valuation multiple was at an all-time low in October.

- Huge insider buy of $27.5M in November.

But with the stock now down more than 15% from its recent high of $80, is Block stock still a good buy here?

Let's take a look.

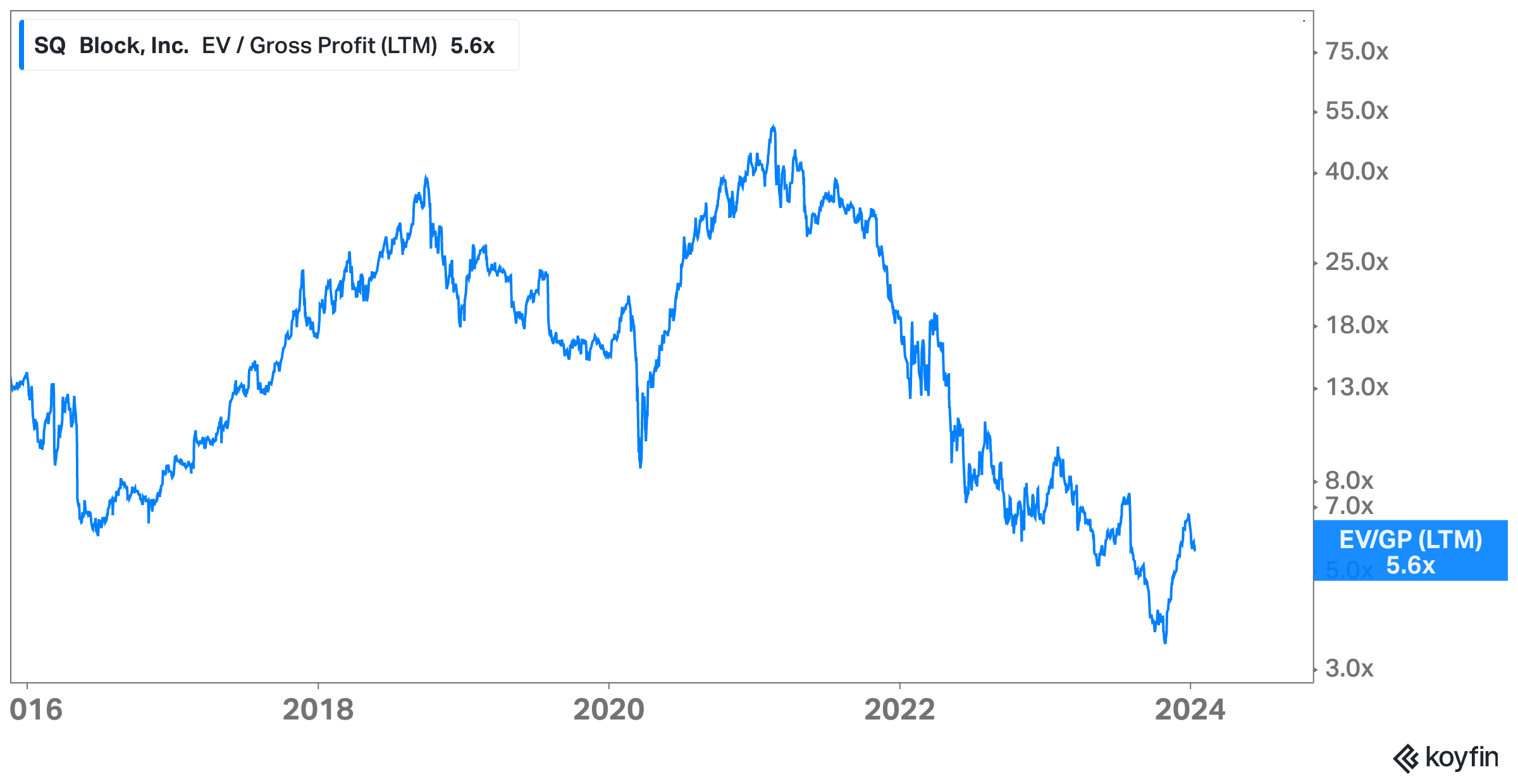

Based on an EV to Gross Profit multiple, Block still trades at depressed valuations. The company now has a multiple of 5.6x, which is way below its peak of 50.0x, IPO of 14.0x, and Covid lows of 8.6x, despite being a much larger and profitable company today.

So despite the recent rally, Block stock still looks cheap from a historical standpoint.

{kind=link}

High interest rates, soaring inflation, and slowing growth did contribute to multiple compressions, but look at the chart below. Block's fundamentals (Gross Profit) continue to improve while the stock is back to where it was five years ago.

This kind of divergence creates a wonderful buying opportunity.

Furthermore, with the recent pullback, Block's price action looks like an inverse head-and-shoulders, which is a bullish reversal pattern.

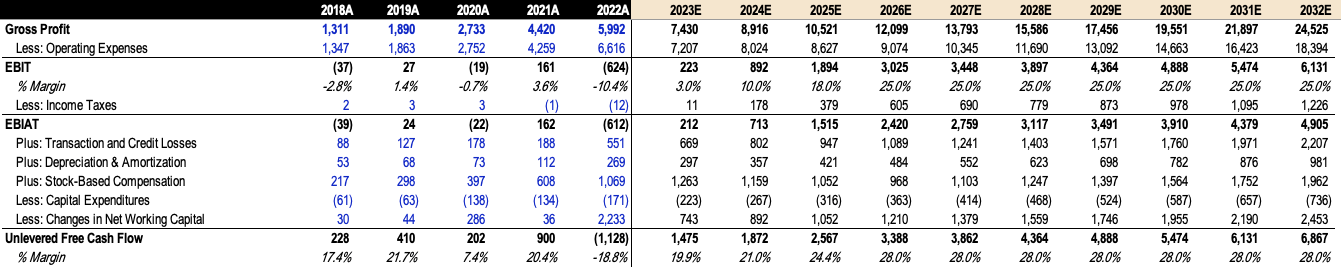

Taking a look at my DCF model, I've used Gross Profit as the topline, instead of Revenue. Doing so removes the volatile impact of Bitcoin Revenue.

That said, here are my key assumptions:

Management expects Gross Profit growth of 24% in 2023. By 2026, growth will drop to 15%, which is in line with management's of "at least mid-teens Gross Profit growth". For the remaining years, I will set a lower growth rate of 12%.

Management also guided for "a mid-20% Adjusted Operating Income margin". Again, keep in mind that Adjusted Operating Margin is calculated by taking Adjusted Operating Income and dividing it by Gross Profit. That said, I assume a 3% Operating Margin in 2023, which is what management guided, and by 2026, the Operating Margin should be about 25%.

Adding a Gross Profit growth of 15% and an Operating Margin of 25% yields a Rule of 40 by 2026.

{kind=link}

I assume a long-term FCF Margin (as a percentage of Gross Profit) of 28% for Block, which is slightly higher than the Operating Margin of 25%.

{kind=link}

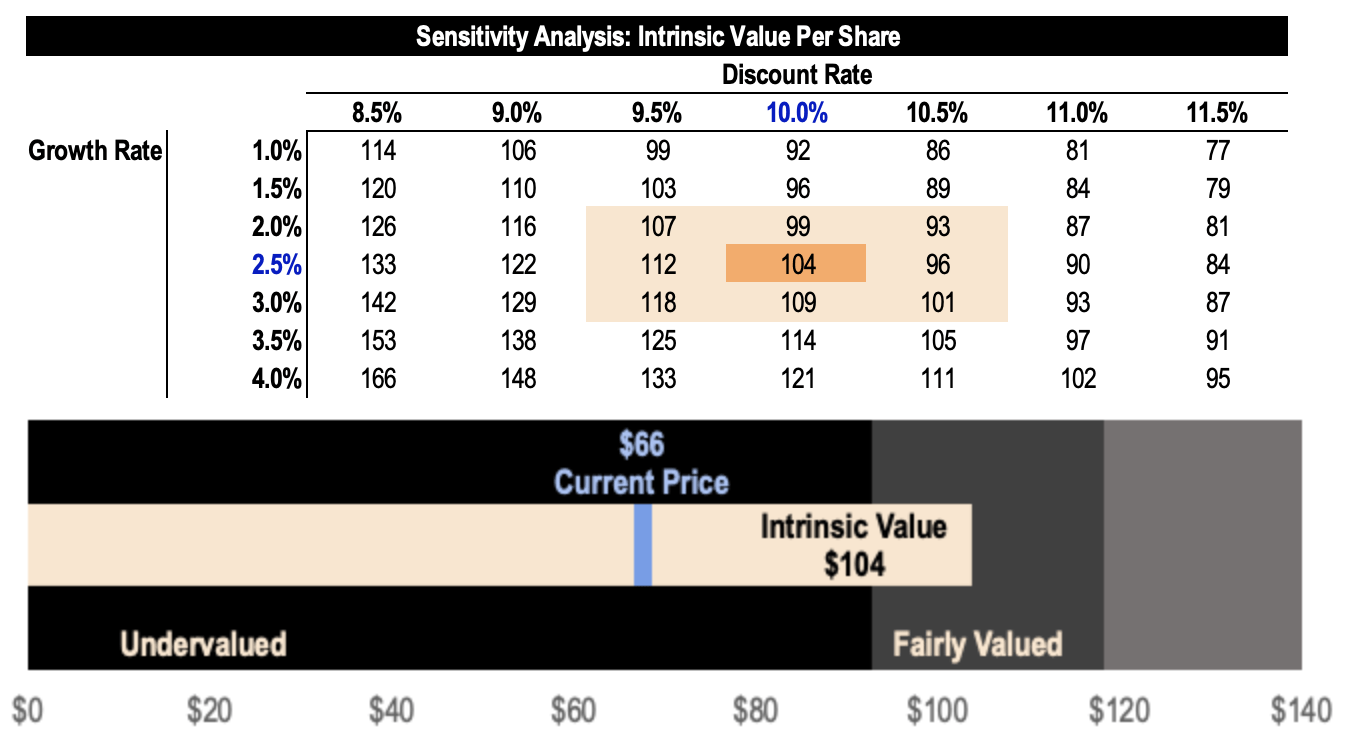

Using a perpetual growth rate of 2.5% and a discount rate of 10%, I arrive at an intrinsic value per share of $104 for Block, which represents an upside potential of 56% based on the current price of $66.

This is also higher than the average analyst price target of $79 a share.

{kind=link}

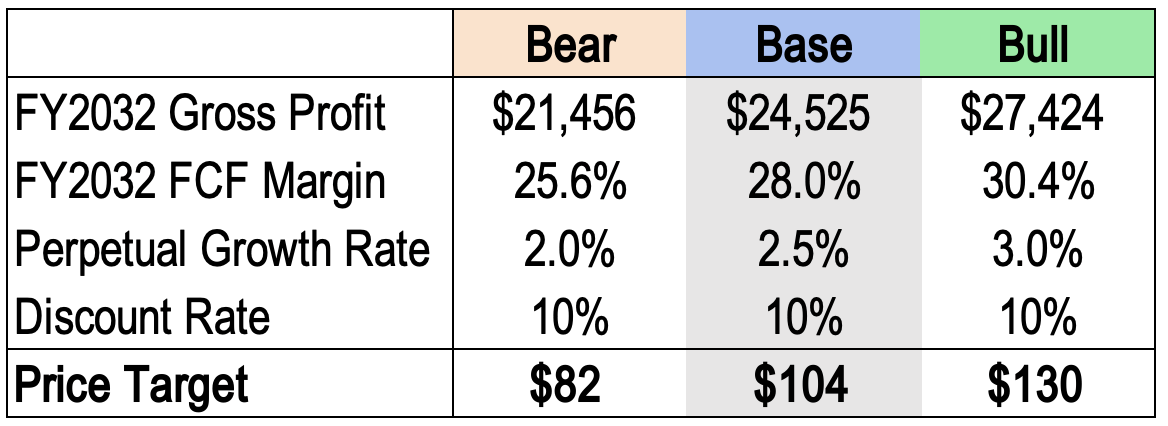

Here, I've also included my bear and bull cases. You can take a look below.

{kind=link}

In summary, I believe Block's stock is still undervalued.

Risks

The fintech industry is highly competitive. Payment processing services, in particular, may eventually be commoditized, which may put pressure on Square's transaction take rate, and ultimately profitability. Competition in this category includes PayPal Holdings, Inc. ( PYPL ) and Adyen N.V. ( OTCPK:ADYEY ).

At the same time, Cash App may lose market share to other digital wallet and banking solutions such as SoFi Technologies, Inc. ( SOFI ), Venmo, Zelle, Chime, Apple Pay ( AAPL ), and more, which could limit Cash App's growth.

Another risk to consider would be Bitcoin. If the price of Bitcoin falls, Block stock may likely fall as well.

Thesis

Block is at an inflection point.

Sentiment has been poor over the last few years. However, with management's Q3 update, sentiment has flipped to the upside.

Investors hated Block because of its lack of profitability. However, the tide has turned as management focuses on delivering profitability to unlock value for shareholders.

More specifically, the 12,000-employee cap and the Rule of 40 are major step changes as the company pursues growth in a disciplined and cost-effective manner.

Without a doubt, Block still has a long growth runway as it builds the financial ecosystem of tomorrow through two high-quality financial ecosystems: Square and Cash App.

Furthermore, with GAAP profitability on the horizon, Block's stock will likely soar higher from here.

That said, despite the sharp reversal in share price, the stock still looks undervalued - in my view, the turnaround story for Block has only just begun.

For further details see:

Block: Turnaround Underway