TPVG - Blood In The Streets? I'm Collecting 15% On My Capital: TriplePoint Venture Growth

2023-12-07 07:35:00 ET

Summary

- When SVB collapsed, it created a void that needed to be filled.

- Venture capital lending can be extremely profitable when done correctly.

- I'm collecting 15% from TriplePoint Venture Growth as others flee the sector.

Co-authored by Treading Softly.

I've never been one to move with the crowd. My current lifestyle goes against many of the norms that were taught to me when I was a child. I grew up in a city. I wore modern clothing. I always had a pair of fresh sneakers on my feet. I had no pets or animals in my home.

Yet when I grew up, I ended up wearing boots, living in the country, and having plenty of animals on my homestead, where we try to live a sustainable lifestyle, not relying on the local grocery store.

So it should come as no surprise that when I approached the market, I also came with an independent mindset. Instead of following the crowd into growth investing, where I buy something hoping that its value will rise, so I can sell it to someone else in the future and unlock that money I earned. I instead bought investments that would pay me money simply to hold them - no more work needed.

At times, this counterintuitive method of generating strong income from the market by not having to sell has placed me at odds with those who want everyone to follow a uniform pattern. It reminds me of the tulip craze or the baseball card craze, where everyone attributed value to something that may not have that value otherwise, and convinced everyone else to attribute value to it too. The whole scheme fell apart when everyone realized that the arbitrary value within these pieces of paper or ungrown bulbs was a value that they were applying to it and not actual real-world value. Growth investors convince other growth investors that the investment is worthwhile driving up the price, but if all of those growth investors stopped being interested in those companies, the value would fall rapidly, and they'd be left with nothing to show.

This is a big difference from an income investor who's willing to invest for income and receive regular dividends. If the company I hold fails, I still have all of the dividends I've received from it to show as returns.

Today, I want to look at a company that invests in others for returns in a venture capital methodology. They earn money from interest as well as from potential capital gains. They continue to pay me outstanding income quarter after quarter.

Let's dive in!

A Time to be Greedy

TriplePoint Venture Growth ( TPVG ), yielding 15.2%, is a BDC (Business Development Company) that specializes in venture capital. This niche has been hit hard by the failure of Silicon Valley Bank which was very involved in venture capital, rising interest rates making capital more expensive for young companies, and a difficult environment for having an IPO. TPVG focuses on investing in companies that are preparing for a liquidity event in 1-2 years, and it hasn't been a great environment in 2023 for that strategy.

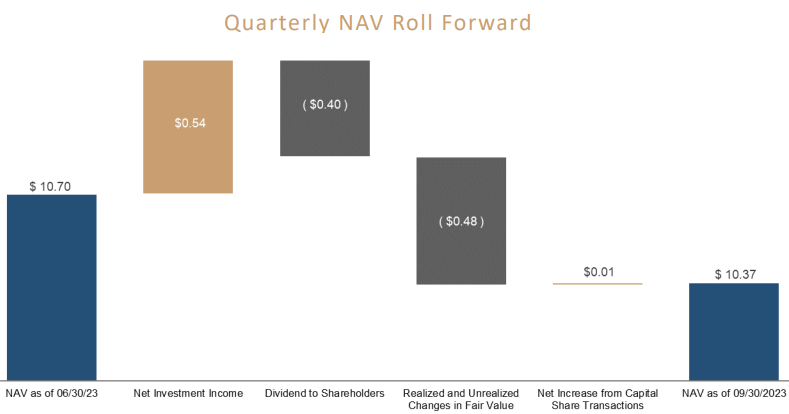

TPVG has seen several borrowers file for bankruptcy, and that has resulted in various loans being written off as losses. Book value has come under pressure, and that continued in Q3. Source

{kind=link}

Yet, note that TPVG earned far more net investment income than it paid in dividends. Despite some borrowers no longer paying, TPVG still out-earned the dividend by $0.14.

If you've read my writings, you know that I am always far more concerned about cash flow than I am about book value. TPVG is a good example of why. The realized losses on book value are lumpy. It will be large amounts in a quarter when a large portion of a loan is written off. However, from a cash flow perspective, one loan no longer paying isn't a big deal. That capital is "lost," but the $0.14 in NII in excess of the dividend made up for about 29% of the book value losses during the quarter. It will take time, but these excess earnings will help recover book value, and that is the plan stated by management when discussing the dividend on the earnings call :

"I think we have done some analysis on that and thinking about the impact on the overall coverage. Given the strength right now of the consistent coverage we've had, even if we bring back the incentive fee once the NAV stabilizes, we still see $0.40 as a solid number going forward, given the fully scaled up portfolio and the yields that are being generated and the level of fixed rate leverage we have, we think it bodes well for long-term coverage. Right now as far as maintaining that dividend, that's the strategy given the higher leverage ratio, it doesn't make sense right now to start looking at increasing dividend, but rather maintain the NAV."

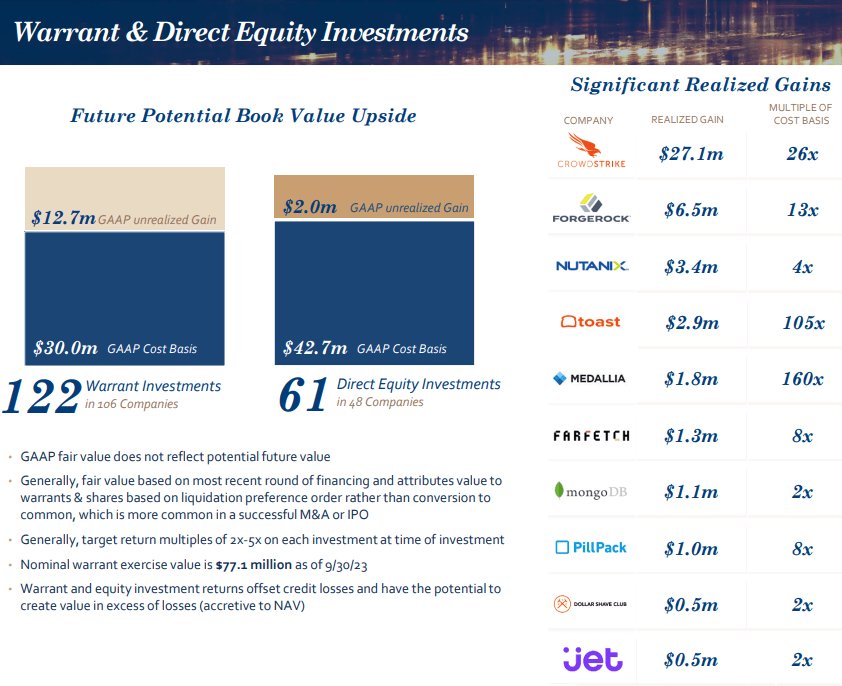

In addition to retaining capital, TPVG also has a portfolio of equity positions, which historically have seen monetization much larger than the carrying value.

{kind=link}

2023 has been a poor environment for monetizing private companies, which is quite commonly the case when the failure rate is high. However, the companies in TPVG's portfolio that aren't struggling in this difficult environment are also likely to be able to monetize when conditions improve and investors are once again bullish on new companies.

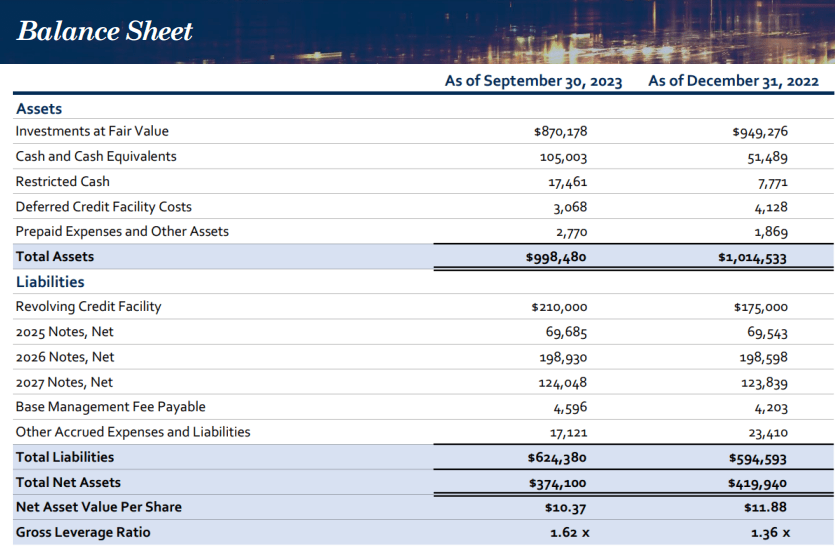

The bottom line is that TPVG will be able to recover from the loans that have defaulted. Our main concern is that TPVG controls its leverage levels. TPVG can recover NAV, but it is crucial that it is not forced into a situation where it needs to sell assets at poor prices to deleverage. Over the past year, TPVG's leverage has climbed, primarily due to the loss of asset value for the loans it wrote off.

{kind=link}

TPVG's leverage at the end of the quarter was 1.62x, this is slightly below the 1.67x the quarter before. However, it is important to note that TPVG is reporting its gross leverage (total liabilities/net assets), if we look at net leverage (subtracting cash from current debt), TPVG's net leverage for the quarter was 1.29x, down from 1.44x in Q2. Most BDCs will only report the net leverage number, which is also the metric that is used for legal leverage limitations. TPVG opted to draw down on its revolver in Q3 to ensure it has good liquidity, and management reported that it was repaid after the quarter ended.

In the near term, we expect that TPVG will continue to concentrate on managing their current portfolio and attempting to maximize recovery for the companies that defaulted. Additionally, TPVG will likely want to keep its leverage drifting down. However, as we go into 2024, TPVG should start expanding into new opportunities.

In the earnings call, CEO Labe outlines a material change in attitude among venture capitalists.

"For the deals getting done in today's market, the operational investment principles have changed. The emphasis is now on managing cash burn and demonstrating a projected path to profitability. As opposed to the guiding principle just 2 or 3 years ago, where venture investors sought growth at all costs."

This change from easy money for anything that promised growth, to a focus on positive cash flow, has shifted the dynamic for companies that rely on venture capital. Some of them will be able to evolve and deliver, and some won't. Creative destruction is occurring in the venture capital world. The companies that get through this difficult period and successfully pivot to cash flow positive companies will be able to IPO or otherwise be monetized for a premium. While TPVG is managing through a downswing right now, it will benefit when the pendulum swings back.

In the meantime, we have a rare opportunity to buy TPVG at a discount to book value.

Conclusion

When the market was frazzled by the collapse of Silicon Valley Bank and regional banking was being reviewed with a stricter eye, many strong companies were able to step in to fill that void. One of them was TPVG. While Silicon Valley Bank is back, advertising its business once more, it does not have the same gusto that it used to have; the same prestige is now tarnished because of what occurred. As traditional lenders and venture capitalists fail, alternatives are available to step up and fill that void. America is one of the greatest nations in the world for innovation. People are willing to take a bet for the chance of success because the country is so supportive and strong of those types of mindsets. I can support this innovative mindset and push while receiving outstanding income simultaneously. A win-win for me. It could be a win-win for you as well.

When it comes to your retirement, I don't want you to be worried about having to come up with innovative solutions to solve the question of your expenses. Instead, the solution is very simple. You need to have enough income to overwhelm your expenses and provide you with abundant income to be able to enjoy at your leisure. How do you achieve this? By owning investments that pay you outstanding levels of abundant income.

That's the beauty of my Income Method. That's the beauty of income investing.

For further details see:

Blood In The Streets? I'm Collecting 15% On My Capital: TriplePoint Venture Growth