BLMN - Bloomin' Brands: Buy For Now

Summary

- Bloomin' Brands saw a price uptick after its recent 2022 results, adding further share price momentum already seen since the start of 2023.

- The restaurant operator's revenues continue to grow, and its operating margins expanded in Q4 2022. Its outlook for both Q1 2023 and the year as a whole is positive too.

- With an attractive non-GAAP P/E ratio as well as forward P/E ratio, Bloomin' Brands stock is a buy for now.

Restaurant operator Bloomin' Brands, Inc. ( BLMN ) saw an over 8% jump in share price yesterday after the release of its full-year 2022 results yesterday. This adds to gains it had already started seeing in 2023, after a relatively weak last year. Year-to-date ((YTD)), BLMN stock is up by 34% as I write.

The next obvious question is whether Bloomin' Brands, Inc. can continue to reward shareholders with its price performance.

Above-average revenue growth

First, let's look at whether the Bloomin' Brands, Inc. price uptick is in line with its recent performance. Turns out, that its revenue growth of 7.1% year-on-year (YoY) is significantly higher than its compounded annual growth rate ((CAGR)) for the past 10 years of 0.7%. Arguably, its growth over the past decade is uninspiring . This is partly because of a big sag of 23.4% during the COVID-19 year of 2020. But even from 2015 to 2018, Bloomin' Brands stock saw declining revenues, and just about grew (by a small 0.3%) in 2019.

That seems to be in the past, though. Bloomin' Brands, Inc. bounced back with sharp growth in 2021 and continues the growth journey in 2022. Even if we take into consideration that at least some of the growth in 2022 was on account of the low base in the first few months of 2021, since the pandemic was very much around, the fact remains that the company has seen a decent 4.6% YoY growth in the fourth quarter of 2022 (Q4 2022) as well.

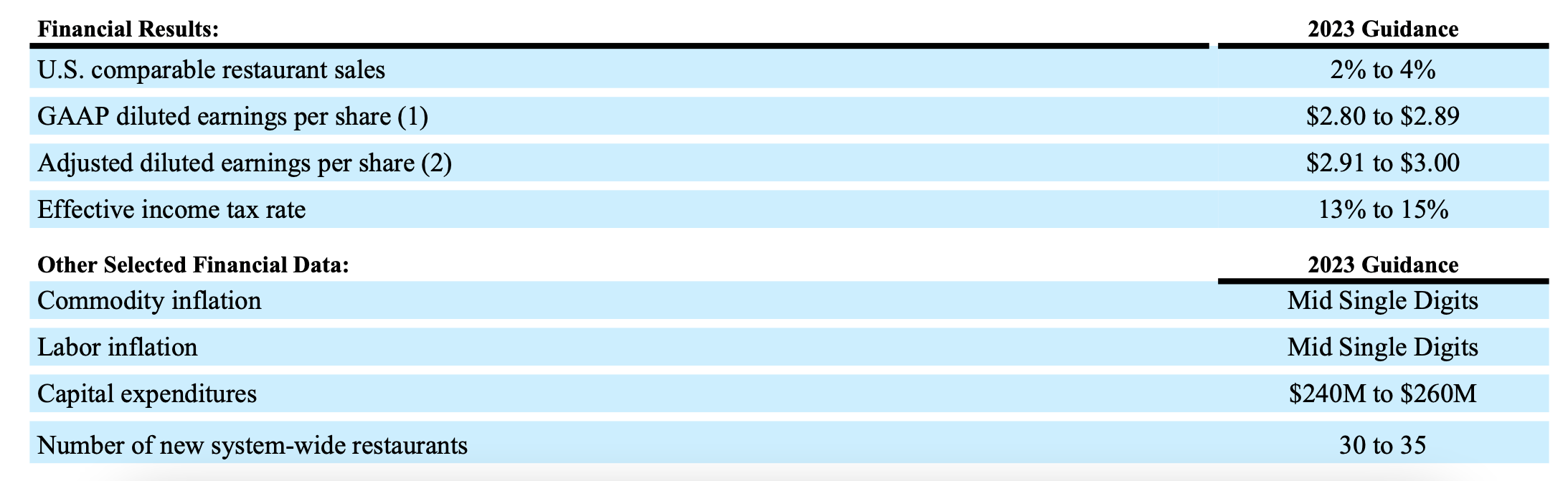

With this in mind, Bloomin' Brands' outlook of a 2% to 4% revenue growth for comparable restaurant sales in 2023, which makes up most of its revenues, sounds reasonable. It is also encouraging to keep its muted 10-year growth in mind, since the company seems to now be making progress.

Rise in operating income, net income declines

Bloomin' Brands, Inc.'s GAAP income from operations has also risen by 6.9% for 2022, and by an even higher 7.2% in Q4 2022. A slowing down in the cost of revenue increase, its big cost head, to 6.1% compared to a 22% increase in Q4 2021 contributed to an improvement in operating income. Bloomin' Brands unsurprisingly also saw margin expansion in the final quarter of 2022 to 7.7%. Its adjusted operating margin looks even better for Q4 2022 (see table below). Though, for the full year, it remained unchanged from 2021 at 7.5%. With CPI inflation now down to 6.4% YoY in the US , the lowest since October 2021, there's a likelihood that it can continue to see further margin improvement over the course of the year as the disinflation process continues.

{kind=link}

However, the company's net income declined to half the level it was at last year, largely on account of loss on extinguishment and modification of debt to the tune of around $108 million, up significantly from the $2 million last year, likely implying an increased cost of debt. It also recorded a loss on fair value adjustment of derivatives of $17.7 million, which wasn't there earlier.

Following this decline in net income, its basic earnings per share ((EPS)) fell to $1.15, less than half the $2.42 seen last year, while diluted EPS fell to $1.03 from $2 last year. Its adjusted diluted EPS didn't decline quite as much, coming in at $2.52, but it too has fallen from $2.7 in 2021.

It is encouraging, though, that the company expects significant improvement in EPS in 2023 (see table below). Diluted EPS is expected to come in between $2.8 and $2.9, while the adjusted counterpart is expected to rise to between $2.91 and $3.

{kind=link}

What's next for its share price?

This brings me to Bloomin' Brands, Inc.'s price-to-earnings (P/E) ratio. Its trailing twelve months ((TTM))P/E figure is at almost 26x , which is significantly higher than the 15.3x for the consumer discretionary sector.

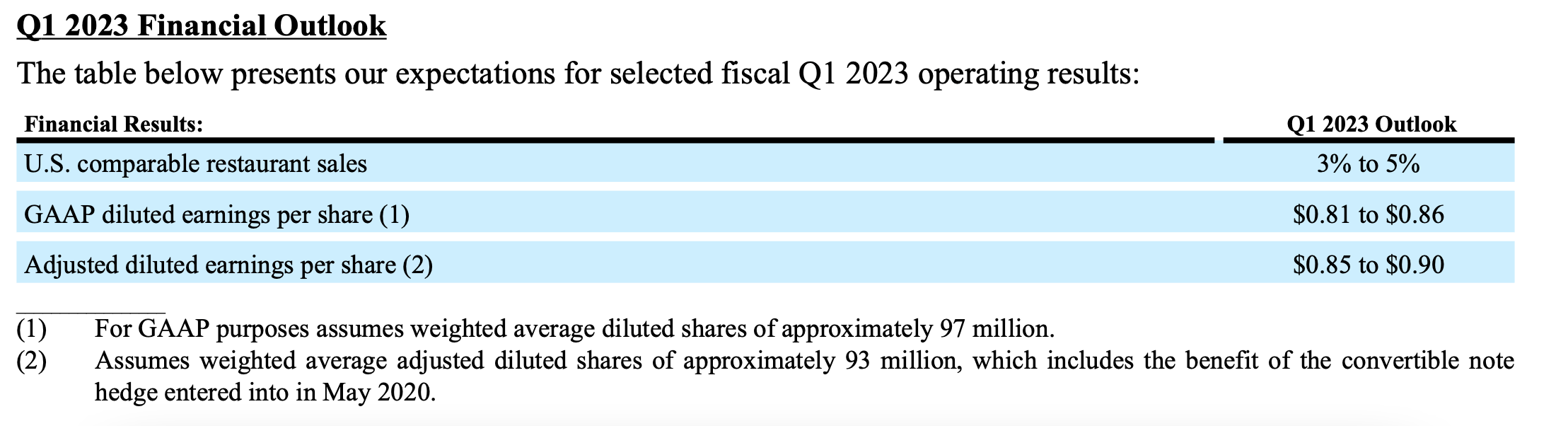

However, since its GAAP numbers have been affected negatively in the past year, here I am inclined to consider both its TTM Non-GAAP P/E as well as its forward P/E, going by its positive outlook. Both numbers look good. Its TTM Non-GAAP P/E is at 10.7x while the sector's P/E is at almost 12.1x. The forward GAAP P/E is also at 10.3x compared to 15.9x for the sector. This indicates that, at least in the short term, there could be a rise in its price. This is particularly so since BLMN provides an outlook on its Q1 2023 figures as well (see table below), which bodes well for both its revenue and EPS. Its diluted EPS is expected to grow by at least 11% YoY in this quarter, from $0.73 in Q1 2022.

{kind=link}

Some liquidity challenges

At the same time, I am not entirely certain if Bloomin' Brands, Inc. can continue to sustain the share price momentum it has seen in 2023 so far. This is because its growth is contingent upon improvements in economic conditions, and this year it is expected to slow down in the U.S., its main market. Further, its current ratio at 0.35x is far from ideal, indicating that it could be in a precarious place if things don't turn out as expected.

That said, the situation isn't entirely bad. Its debt ratio is at 0.65x, it could be worse. It's also positive on cash. The company's CFO, Chris Meyer commented in the earnings release that "Importantly, we continue to generate ample cash flow that will fund investments in our people and ongoing growth initiatives." BLMN also pays a dividend. It doesn't have the highest yield, at 2.08% , but it's a nice extra income from a stock nevertheless.

Short-term positive, medium-term uncertain

All in all, I think Bloomin' Brands, Inc. is headed in the right direction. The latest figures inspire confidence, as does its outlook. The improvement in operating profits and margin expansion in the last quarter of 2022 is notable at a time of high inflation. If the outlook for the U.S. economy were less certain and more positive, I would have little doubt that it's a buy. But since it's not and Bloomin' Brands, Inc.'s long-term growth is also low, I'm still cautious about the medium to long-term. For now, though, I am going for it as a Buy for the short term.

For further details see:

Bloomin' Brands: Buy, For Now