BLMN - Bloomin' Brands: Foggy H2 Outlook With Waning Industry-Wide Traffic

2023-10-10 13:06:28 ET

Summary

- Bloomin' Brands had a satisfactory Q2, with lower traffic but a slight beat vs. its peer group, and a solid quarter out of Outback Brazil.

- Meanwhile, the company has held the line well on margins overall (albeit helped by pricing), with further gains from productivity and new equipment/tech.

- However, with industry-wide traffic worsening, the company rolling off price, and beef and labor inflation remaining sticky, the reward/risk setup isn't great looking into H2.

Just over a year ago, I wrote on Bloomin' Brands ( BLMN ), noting that while the stock was becoming more attractively valued, the ideal buy zone came in at $16.00 or lower. This ended up being an opportunity cost, with the stock bottoming out that week and enjoying a significant rally since then and never re-testing the $16.00 area low from June 2022. However, the stock has since pulled back sharply with the industry group, erasing over half of its year-to-date gain. Outside of industry-wide traffic that has continued to soften since July, Bloomin' is in the less favorable position of having higher relative commodity inflation with beef being a key ingredient on its menus vs. some brands like First Watch ( FWRG ) benefiting from deflation due to lower pork prices. In this update, we'll dig into how the BLMN is set up heading into H2 and whether the market has priced these headwinds into the stock.

Recent Results

Bloomin' Brands ("Bloomin'") released its Q2 results in August, reporting quarterly revenue of ~$1,153 million, a 2% increase from the year-ago period. The relatively low revenue growth compared to peers despite high single-digit pricing can be attributed to soft comp sales across its segments (excluding Outback Brazil which had a strong quarter), with Carrabba's performing the best with 3.5% comp sales year-over-year, followed by Outback, Bonefish Grill, and Fleming's at 0.6% growth, 0.5% growth, and [-] 2.5%, respectively. This was despite the bulk of these segments lapping negative easy comps that were negative in the year-ago period, with Outback, Carrabba's and Bonefish having two-year stacked comp sales growth of [-] 0.5%, 2.5%, and 0.6%, respectively.

Bloomin Brands Quarterly Revenue - Company Filings, Author's Chart

{kind=link}

On the surface, these results look disappointing and they were below my expectations, but Fleming's had a decent quarter given that it had to lap 6% comp sales (Q2-2022), and some of the traffic decline has been related to less discounting to drive sales vs. other brands that have got more promotional in casual dining. And on a positive note, the company noted that despite the sharp traffic declines seen across the board (negative 4.2% traffic growth for US businesses in Q2 2023), its US comp sales outperformed the industry average by 110 basis points, a minor win. And the company seems to be doing something right in terms of its guest experience, with it moving up from No. 6 to No. 1 on the ACSI Restaurant Study according to the company for casual dining brands. This is certainly a positive development, with consumers being more judicious where they spend.

Finally, digging into margins, the company reported restaurant-level margin improvement of 90 basis points in Q2 (16.4% vs. 15.5%), with its cost of sales dropping 200 basis points to 30.9%, helping to offset a 90 basis point increase in labor and a 20 basis point increase in other costs (higher utilities/advertising expenses). Bloomin' noted that the lower cost of sales was related to higher average check and cost savings and that it's seeing better table turns and improved productivity with its new kitchen technology/equipment. However, labor has remained sticky industry-wide due to wage inflation. The positive here is that Outback has done a better job than several brands regarding holding the line on margins, but this has been helped with higher menu prices, and price will roll off by ~300 basis points from H1 to H2.

Average Guest Check - Casual Dining Brands - Dine Brands Presentation

{kind=link}

Looking at the statistics above, which are stale and over 18 months old, we can see that Outback and Cheesecake Factory ( CAKE ) are two of the most expensive casual dining brands in the United States, and with Bloomin's Outback being a higher average check concept, it's not clear how much room on pricing there is until some less affluent customers are priced out or we see some trade down to other brands and or one less incremental visit to save money. So, although it's encouraging that the company has held the line as well as it has on margins, and other brands have done a decent job here as well, I don't think the average consumer can continue to absorb high single-digit pricing each year, and this could mean further margin compression next for the year group if brands (including Outback) have to be less aggressive on price and continue to deal with 5%-7% labor inflation to keep restaurants fully staffed and maintain retention.

Industry-Wide Trends

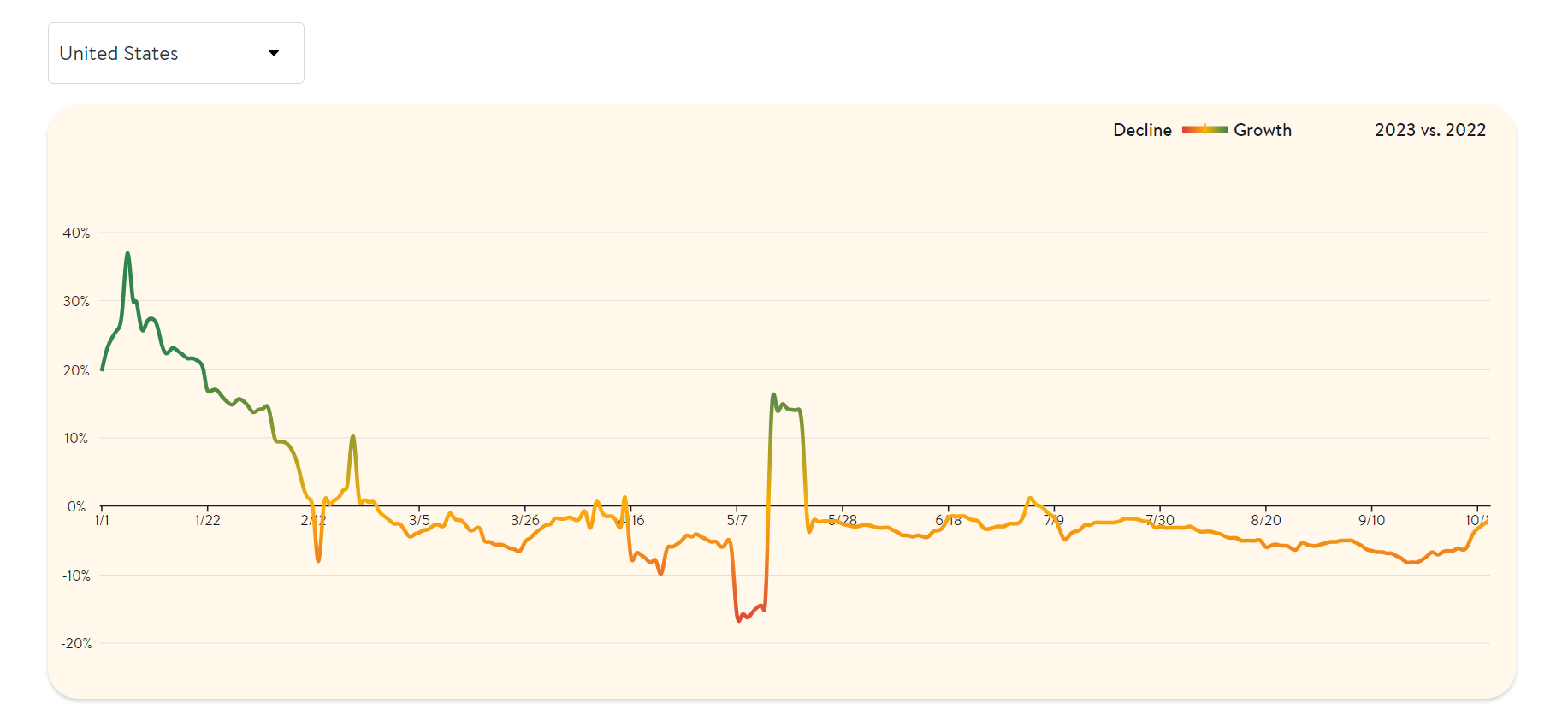

Moving over to industry-wide trends, the one positive has been the pullback in commodity prices, with Bloomin' calling out lower dairy and produce and other brands noting that pork and chicken also have cooled off vs. elevated pricing last year. In fact, Wholesale Food Prices were down year-over-year in August, a welcome departure from the double-digit inflation experienced last year. That said, Outback, like Texas Roadhouse ( TXRH ), will see an impact from higher beef costs, which has been a stubborn commodity that was still up over 15% in Q2 year-over-year. And with pricing rolling off, traffic worsening industry-wide and the impact of higher beef costs, it would surprise me if Bloomin' can deliver into the high end of its Q3 guidance of $0.41 to $0.46 in earnings per share unless this is accomplished with another quarter of aggressive share buybacks. Plus, while Q3 was rough for industry-wide traffic as highlighted below, Q4 isn't starting out any better and consumers are already tight with record credit card debt heading into an expensive holiday season.

US Seated Diners Growth - OpenTable

{kind=link}

Digging into the traffic component a little closer, the above chart highlights that traffic growth has been anemic this year, and while it started out strong after lapping Omicron (January 2022), it's been in a steady downtrend all year with the spikes in traffic becoming more and more muted. Meanwhile, traffic was sharply negative for all of Q3, clawed its way back through September but has turned lower again to start Q4. And comparing on a monthly basis, both casual dining and quick-service saw their worst traffic growth of the year in September, with the fact that quick-service was hit as well (typically a trade-down option and less sensitive) suggesting that consumer weakness could be worsening, with this being one category that has held up relatively well compared to casual dining.

To summarize, I think it's tough to be optimistic about a top or bottom line beat in Q3 or Q4 for Bloomin' - and outside of a recovery in the market as a whole, I don't see what the catalyst is for a much higher share price for BLMN if industry-wide Q3/Q4 results could be on track to disappoint. And while one could argue that expectations already are low because of the tough macro, we have seen a clear divergence in the positive commentary in Q2 Conference Calls on the start of Q3, which jives with the recovery in traffic from late June to late July. However, as the above chart shows and other traffic data highlights, this trend immediately rolled over, suggesting that this more upbeat commentary may have been different if the calls were two weeks later than late July/early August relative to how the rest of the quarter looks like it played out.

Valuation

Based on ~87 million shares and a share price of $23.40, Bloomin' Brands trades at a market cap of ~$2.03 billion and an enterprise value of ~$4.03 billion. This gives it one of the higher market caps among the casual dining group, well ahead of smaller peers like Red Robin ( RRGB ), BJ's Restaurants ( BJRI ), Dine Brands ( DIN ), and First Watch ((FWRG)). And following this steep correction, the stock also trades at one of the highest free cash flow yields in the industry group, trading at ~13.4x free cash flow based on its current EV even when using more conservative estimates of ~$300 million in FY2024. Not only is this one of the highest free cash flow yields in the sector, but the significant cash flow generation is allowing Bloomin' to aggressively buy back shares, with ~2% of its shares repurchased year-to-date alone, and nearly $100 million remaining under its current buyback program.

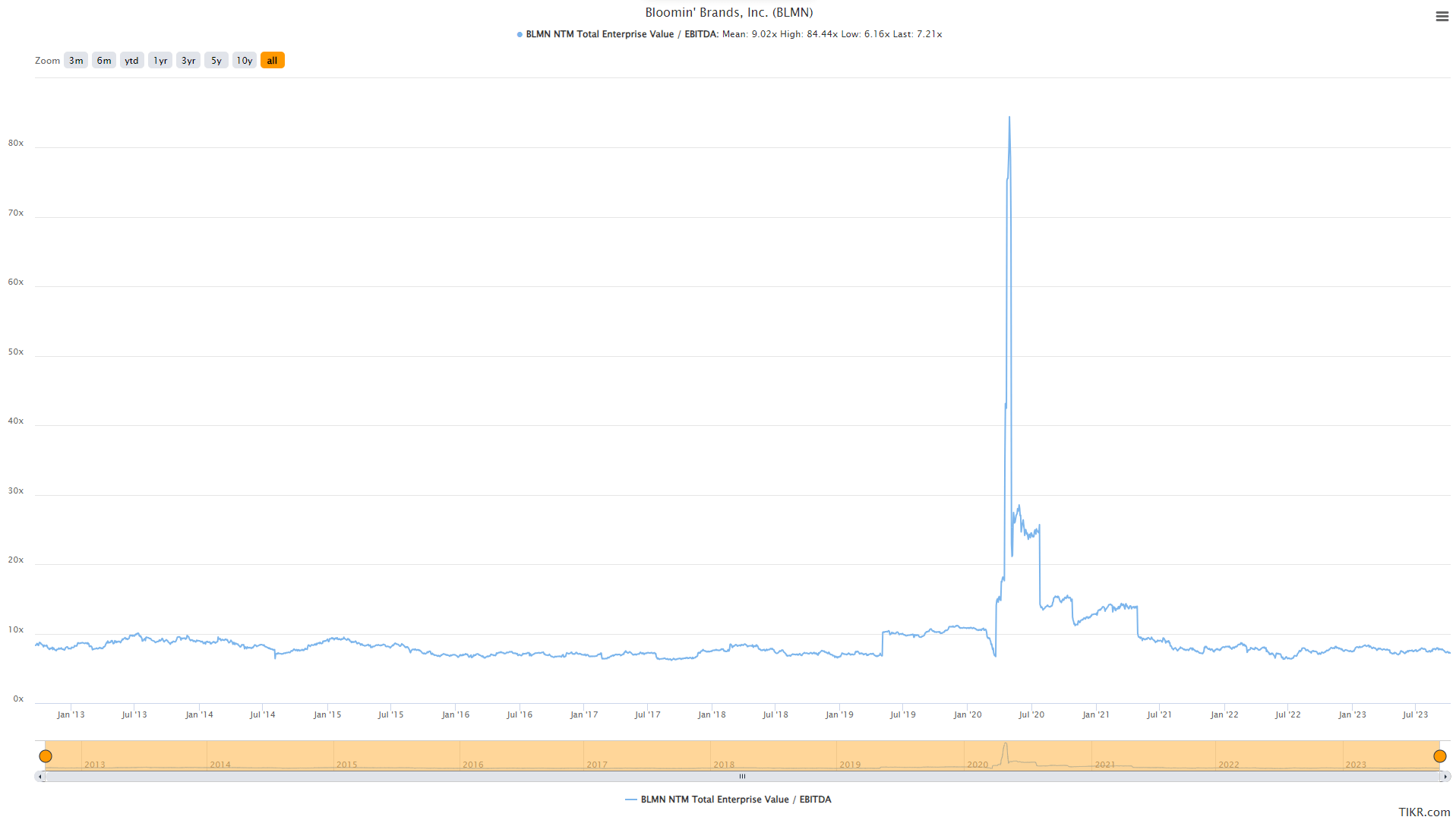

Bloomin Brands - Historical EV/EBITDA Multiple - TIKR.com

{kind=link}

Looking at the stock from an EV/EBITDA standpoint, the stock also has one of the more attractive multiples, trading at just ~7.1x EV/EBITDA on FY2024 estimates (~$560 million). This places it well below other casual dining names like BJ's Restaurants, Portillo's ( PTLO ), and First Watch at ~8.9x, ~16.0x and ~14.5x EV/EBITDA using FY2024 estimates, respectively. And although the discount is largely justified because of its lower unit growth and higher leverage ratios, 7.0x EV/EBITDA or lower is a very reasonable valuation compared to its historical multiple, with the stock trading at an average EV/EBITDA multiple of ~9.0x over the past decade, and typically bottoming out at ~6.0x EV/EBITDA or lower even in violent sell-offs. So, even if we adjust for the higher interest rate environment and its lower growth relative to its peer group, this is a very reasonable valuation.

Using what I believe to be a more conservative multiple of 7.5x EV/EBITDA and using FY2024 estimates of ~$560 million and ~86 million shares outstanding, I see a fair value for BLMN of $26.15. This points to a 12% upside from current levels, but I'm looking for a minimum 25% discount to fair value for mid-cap names to ensure a margin of safety. If we apply this discount to its estimated fair value, BLMN's ideal buy zone comes in at $19.60 or lower, suggesting that the stock has still not drifted into a low-risk buy zone despite its recent underperformance. Obviously, there's no guarantee that the stock heads back to these levels and a bounce short term would not surprise me with the stock down five out of the past six weeks, but this is the level I would need to become more interested, and where the stock would trade closer to a double-digit free cash flow yield on an EV/FCF basis.

Summary

Bloomin' Brands had a satisfactory quarter for its United States business and Outback Brazil had an impressive quarter (eight new units added), with the company noting that performance is exceeding expectations and that the system has room to double to 300 restaurants by 2028. However, we have seen a clear negative change in traffic since July and with the industry set up to potentially disappoint on the top and bottom line in H2, the reward/risk setup is not ideal, even if several names have come off their highs sharply. On a positive note, BLMN is one of the cheaper names; it outperformed traffic and it might be more immune than its peers. Still, with no clear margin of safety at $23.40 and the stock still above key support in the $20.00 - $21.00 region, I continue to see more attractive bets elsewhere in the market.

For further details see:

Bloomin' Brands: Foggy H2 Outlook With Waning Industry-Wide Traffic