APRN - Blue Apron: How Much Longer Can It Keep Bleeding Red Ink?

Summary

- Shares of Blue Apron have shot up 60% year to date, barely saving the company from a de-listing.

- The company continues to bleed customers and revenue.

- Especially in a tough macro environment where consumers are curtailing spending, the company's pricing at $8-$10 per serving is unappetizing for a home-cooked meal.

- Liquidity continues to pose a challenge for the company.

So far, the 2023 rebound rally has managed to lift up almost all small and mid-cap tech stocks, even those that seemed to be dangling on a lifeline. Even Blue Apron ( APRN ), the original meal-kit company that has been struggling for years, managed to take advantage of the resurgence in risk-taking to shoot up ~60% since the start of the year and stave off a delisting from the NYSE (which requires the company to maintain a market cap of at least $50 million and a share price above $1).

It's unclear, however, how much of a lifeline this company has left. In my view, investors are best off ignoring this year's phantom rally and remaining on the sidelines.

The customer bleed continues

Blue Apron is focusing all of its efforts on cost-cutting and liquidity, in a struggle for mere survival (more on that next). But I think the core of the company's issue is this: is the meal-kit format even still viable anymore? Are customers still going for this type of service?

{kind=link}

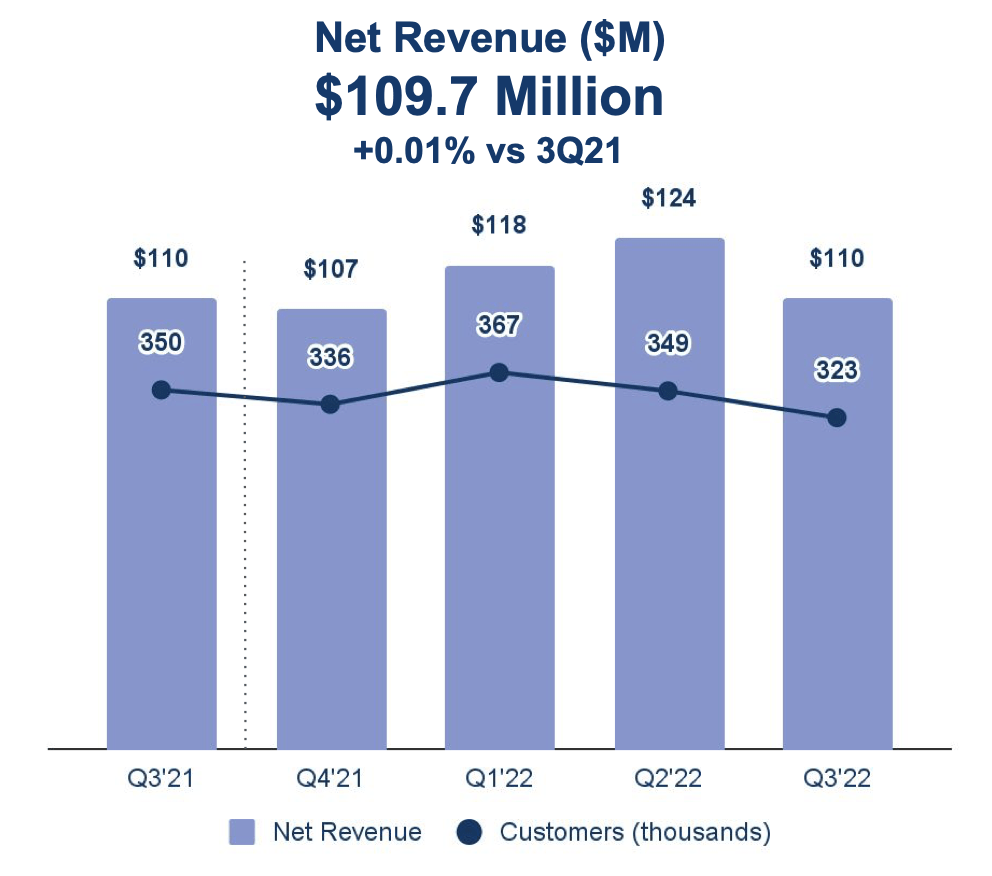

In Blue Apron's most recent quarter, the company achieved flat revenue growth of $109.7 million. Active customers, meanwhile, shed 26k quarter-over-quarter, and 27k (-8%) year over year.

The company is stuck in a tough place in this macro environment. Amid inflation and recessionary fears, consumers are cutting back on their discretionary spending - and convenient at-home meal kits like Blue Apron are something of a luxury.

The company's biggest plan - 4 servings with 4 meal recipes per week - costs $128, which comes out to $8/serving - not including a $10 shipping fee. Smaller plans, like 2 servings for 3 meals a week, cost $10/serving. That's a hefty charge for an at-home meal in this economy.

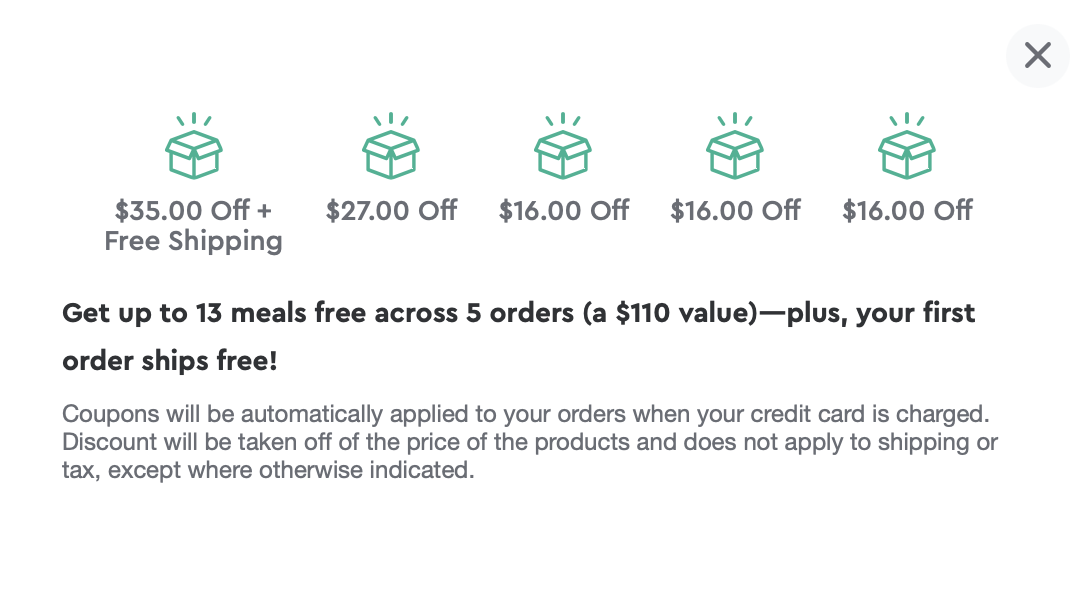

Blue Apron, of course, still continues to rely on introductory promotional offers that significantly reduce these prices. A customer can still sign up with $35 off and free shipping reduced from their first box. But I think it's this kind of promotional activity that encourages high churn, as customers defect when these promotional rates expire and the much higher standard prices kick in.

{kind=link}

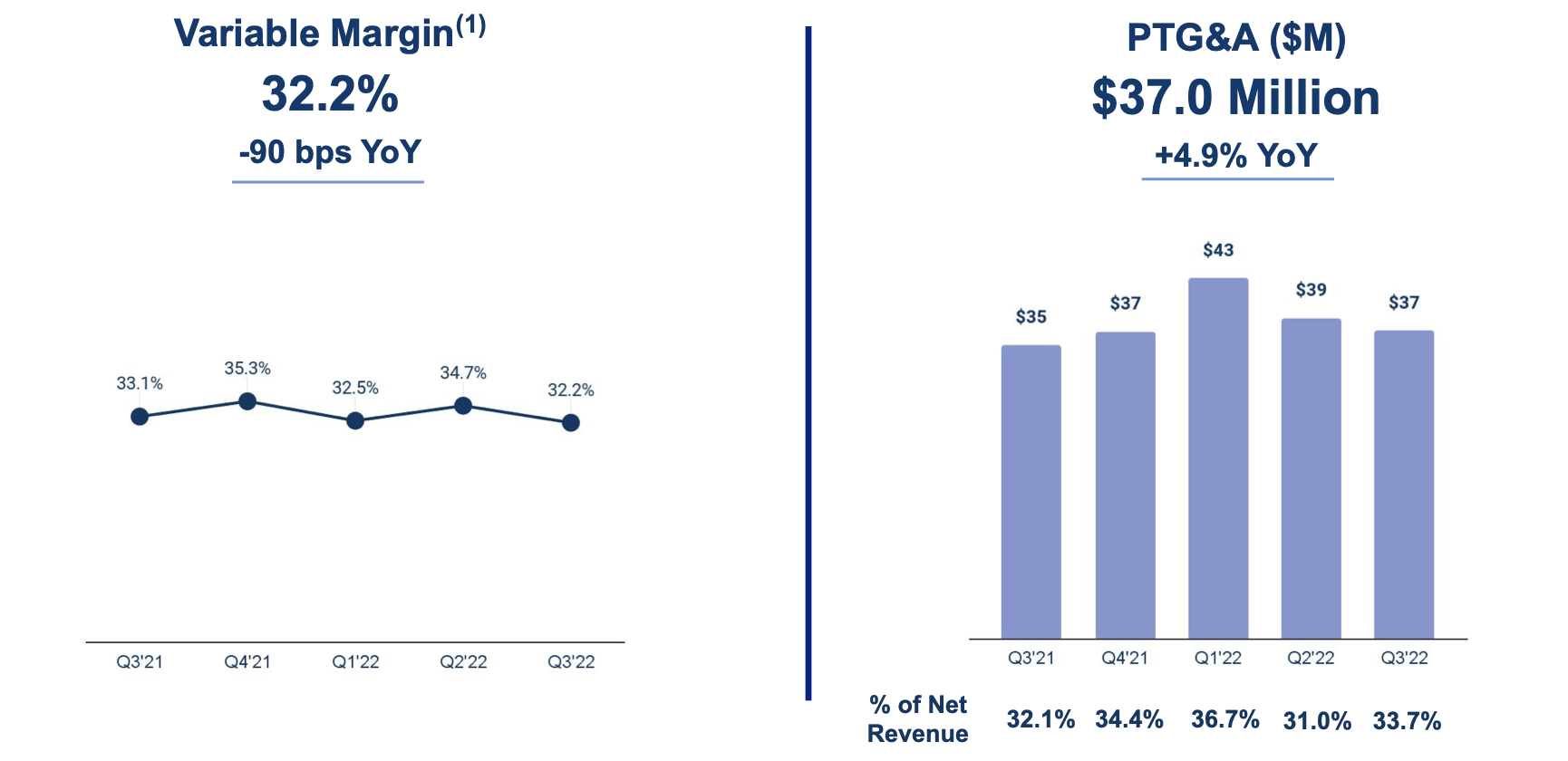

And perhaps it's a greater mix of promo (versus full price) customers that are helping to drive down the company's variable margin, down 90bps y/y to 32.2%. Blue Apron is stuck in a hard place here: as its number of customers and orders shrinks, the company faces deleverage issues in its procurement and warehouse operations, but without margins and profitability the company can't spend to chase growth, either. In Q3, the company reported a 21% y/y reduction in marketing spend, which is partially the reason behind the consistent bleed in customers.

{kind=link}

Cost-cutting may not provide the answer

On top of Blue Apron's decision to cut marketing spend, the company also made the decision to lay off 10% of its workforce (which may not even be enough to solve the company's issues). All in all, the company notes it has identified a run rate of $50 million in annual savings.

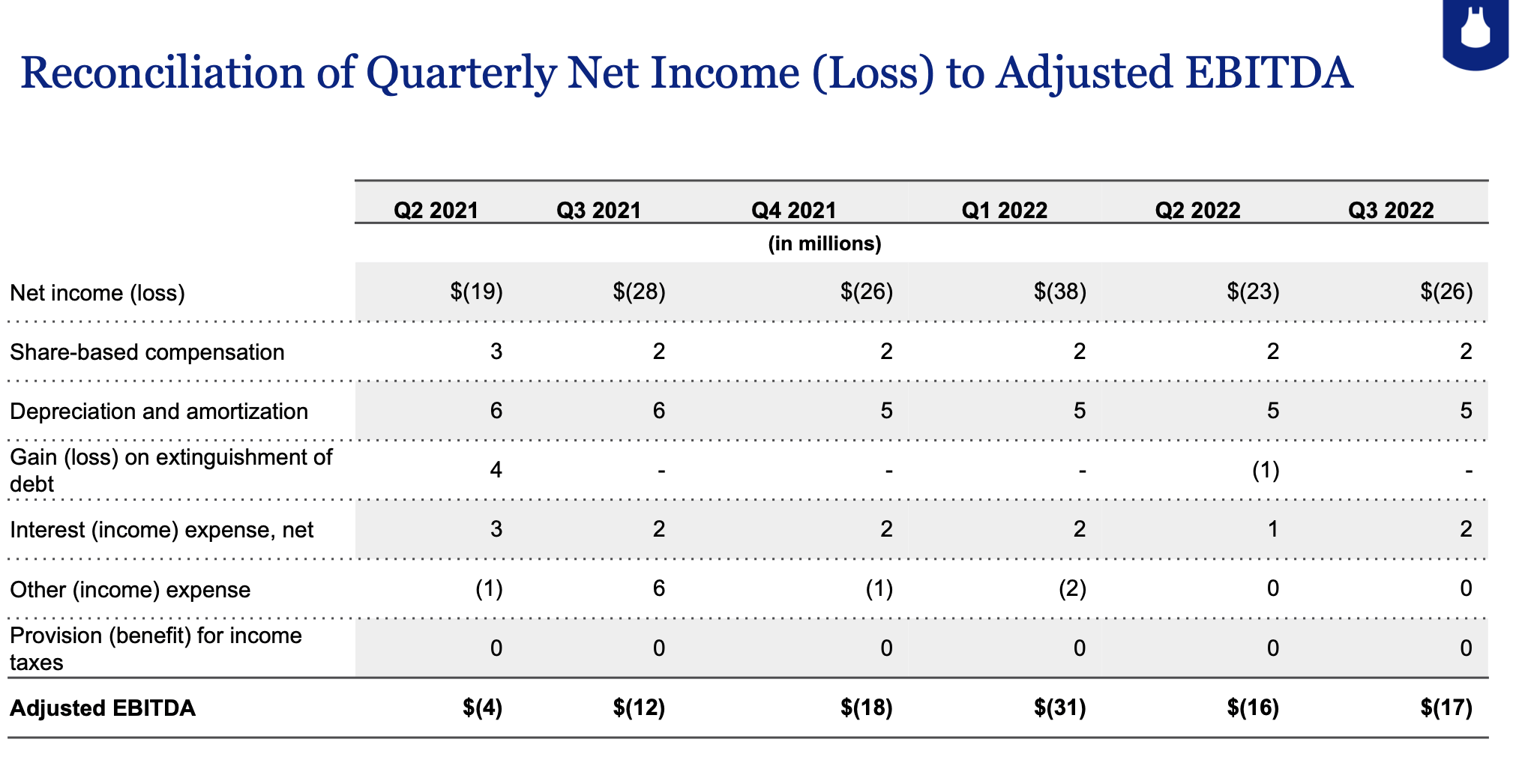

But is this enough? In Q3, the company generated negative adjusted EBITDA of -$17 million. In the trailing twelve months, adjusted EBITDA losses were -$82 million.

{kind=link}

The company has a goal to get to adjusted EBITDA breakeven: but even if it fully realizes $50 million in opex savings that translate directly to adjusted EBITDA, it won't hit positive. And that's assuming revenue can continue to perform at flat levels and gross margins don't get impacted further: in reality, I think harsh economic tidings plus the reduction in marketing spend (thus putting Blue Apron's brand even further into a fading background) will cause continued revenue deceleration and volume deleverage.

Liquidity continues to be a challenge for Blue Apron. At the end of the third quarter, the company had only $31.0 million of cash remaining, on top of $35.8 million of long-term debt. It managed to raise $14 million in a follow-on offering in October after the close of the quarter, but considering Q3 free cash flow burn alone was -$22.7 million, this is only a temporary salve.

The company is still due $56.5 million from a previously agreed-upon private placement, with the buyer displaying cold feet. Per temporary CFO Mitch Cohen's remarks on the Q3 earnings call :

As Linda discussed earlier, we remain active in discussions with Mr. regarding his funding. On November 6, we entered into a pledge agreement under which an affiliate of his granted us a security interest in certain assets of private companies with the value estimated to be significantly in excess of the $56.5 million owed to us under the RJB private placement agreement.

Additionally, we're working on a number of cost savings initiatives and in discussions with financial advisers to evaluate financing and other alternatives. We also are in discussions with our lenders as assuming we receive no funding from Mr. Sanberg or other sources, we expect to be in breach of our minimum liquidity requirement of the covenant as early as later this month.

We believe the pledge for Me. Sanberg affiliates gives us an alternative path to secure the funding and demonstrates to our lenders, we are taking necessary steps necessary actions to secure liquidity."

The lack of follow-through on this funding agreement drove Blue Apron to withdraw its previously-stated guidance of 7-13% y/y revenue growth in FY22 - which is now looking entirely unrealistic considering YTD revenue through the first three quarters of FY22 came in at a -3% y/y decline.

Key takeaways

With a shrinking customer base and no choice but to slash marketing spend, and a workforce-reduction move that is unlikely to trim Blue Apron's cash burn in a meaningful way, I continue to see no path forward for Blue Apron. Maintain caution here and stay on the sidelines.

For further details see:

Blue Apron: How Much Longer Can It Keep Bleeding Red Ink?