ROIC - Blue-Chip Real Estate Is A Bargain - Top Picks Across 5 Sectors

2023-04-21 08:30:00 ET

Summary

- Media pundits frequently and sloppily equate office buildings with "commercial real estate," but the two are not equal. There's a lot more to CRE than half-empty downtown office towers.

- I am staying far, far away from office REITs, even if they seem like deep values right now.

- But non-office REITs appear to have been sold off particularly hard amid investors' desire to shed all exposure to "commercial real estate."

- That has resulted in a rare opportunity to accumulate shares of blue-chip (non-office) REITs at huge discounts and high dividend yields.

- I highlight my top picks in five different real estate sectors.

Commercial Real Estate ? Office Real Estate

People in the media often equate "commercial real estate" with "office real estate." That's frustrating as someone who frequently writes about REITs and CRE generally but rarely ever writes about office properties or office REITs. They are not the same.

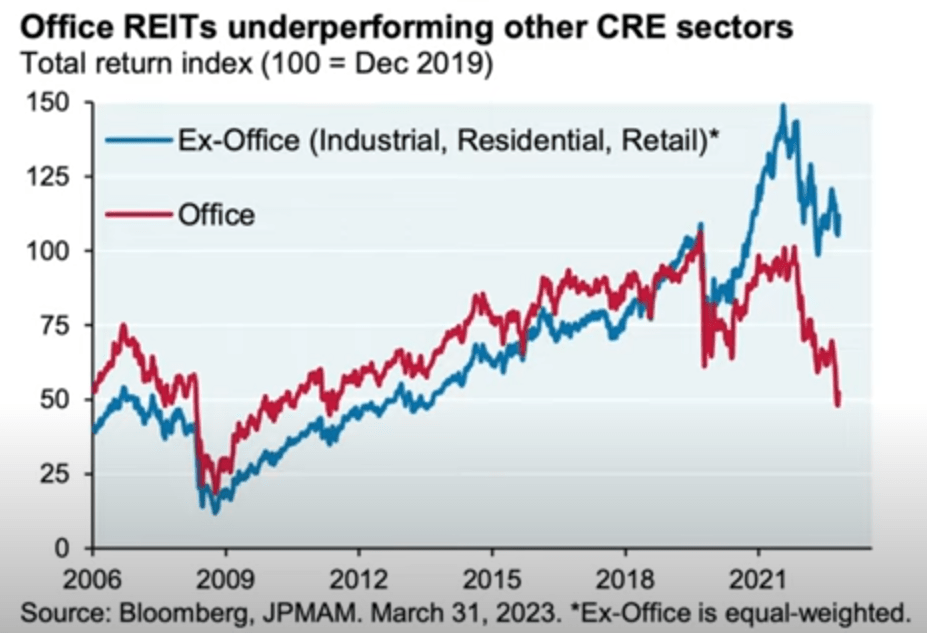

The following chart shows that non-office REITs remained above their pre-pandemic level at the end of March while office REITs specifically have plunged below pandemic lows.

{kind=link}

The Compound And Friends

Office real estate does not equal commercial real estate.

And yet, you hear all the time in media the huge problems with "commercial real estate," by which they are referring specifically to office real estate. This is sloppy and intellectually lazy, but everyone seems to do it, so everyone else does it too.

I think this close association of commercial real estate with office properties is causing all REITs to sell off. Right now, the Vanguard Real Estate ETF ( VNQ ) is 11% below the level at which it began 2020.

This masks a world of various performance between the different sectors of real estate as well as between different REITs.

I'm bullish CRE, even though I'm not touching office REITs with a 10-foot pole. If you'd like to read my reasoning on this, see my recent research reports posted exclusively for High Yield Landlord subscribers:

- MARKET UPDATE - Banking Crisis: First Domino To Fall In The Office Apocalypse?

- MARKET UPDATE - Beware A Potential Boom In Office Building Conversions

The office CRE fallout will be a multi-year process. I'd caution against jumping into any "dirt cheap" office REITs. They could be value traps. Even if they survive, that doesn't mean they'll be out of the woods in 2024 or 2025. Interest rates may not go back to ultra-low levels, and lenders may never again be as enthusiastic about making office building-secured loans as they once were.

Meanwhile, employers don't seem to be winning the "return to office" standoff with remote workers. At least not yet. So, as the economy weakens, the pressure to cut costs by downsizing leased office space will mount, which in turn will only solidify the new hybrid/remote work norm.

Think about this: Debt-to-assets (at cost), a crude approximation of loan-to-value, ended 2022 at about 59% for Boston Properties ( BXP ) and 45% for SL Green ( SLG ).

Cohen & Steers estimates that office real estate has shed 25% of its market value since its 2022 peak. Some experts project peak-to-trough declines in office prices of 40%. Such a decline in market value would produce LTVs of 98% for BXP and 74% for SLG. And that assumes BXP and SLG will not need to sell any assets or increase debt, which they almost certainly will.

You think office LTVs don't look too bad, but that's at the market values of yesteryear.

Now consider:

- The office CRE debt rolling over in 2023-2024 that was originally priced during the much lower interest rate environment of 2013-2014 or 2018-2019 (example: 30% of SLG's total debt matures through 2025)...

- And the fact that office CRE rental revenue is falling as tenants lay off workers and downside space...

- And the likelihood that office landlords will have to invest heavily in capital expenditures to compete for a shrinking pool of office demand...

- And the probability that office REITs' total assets will drop as they sell properties (at big discounts) to pay off debt...

- And the fact that white collar workers overwhelmingly prefer hybrid or fully remote work arrangements...

You do the math.

Office real estate is riddled with risks. But commercial real estate more broadly is a different story. REITs that own other types of real estate appear to be "guilty by association" and are being dumped because of the media's repeated sloppy implications that the problems of office real estate are the problems of all CRE.

That's fine with me, actually. I am happy about this broad misconception, because it allows me to buy discounted blue-chip REITs with high-quality real estate, strong balance sheets, little vulnerability to rising interest rates, and zero exposure to office properties.

Let's take a look at five examples in different sectors.

Life Science: Alexandria Real Estate Equities ( ARE )

ARE, led by founder and executive chairman Joel Marcus, owns many of the highest quality life science (medical research & development) properties in the world, located in many of the most productive and supply-constrained life science clusters in the world.

Amid aging populations around the world, these state-of-the-art biotech properties are extremely valuable to pharmaceutical companies. From 2001 through 2020, global biotech R&D spending rose 13.7% annually, more than three times pharmaceutical industry spending more broadly. This R&D spending should continue to grow at a strong rate to take advantage of the tidal wave of healthcare consumption in the decades to come.

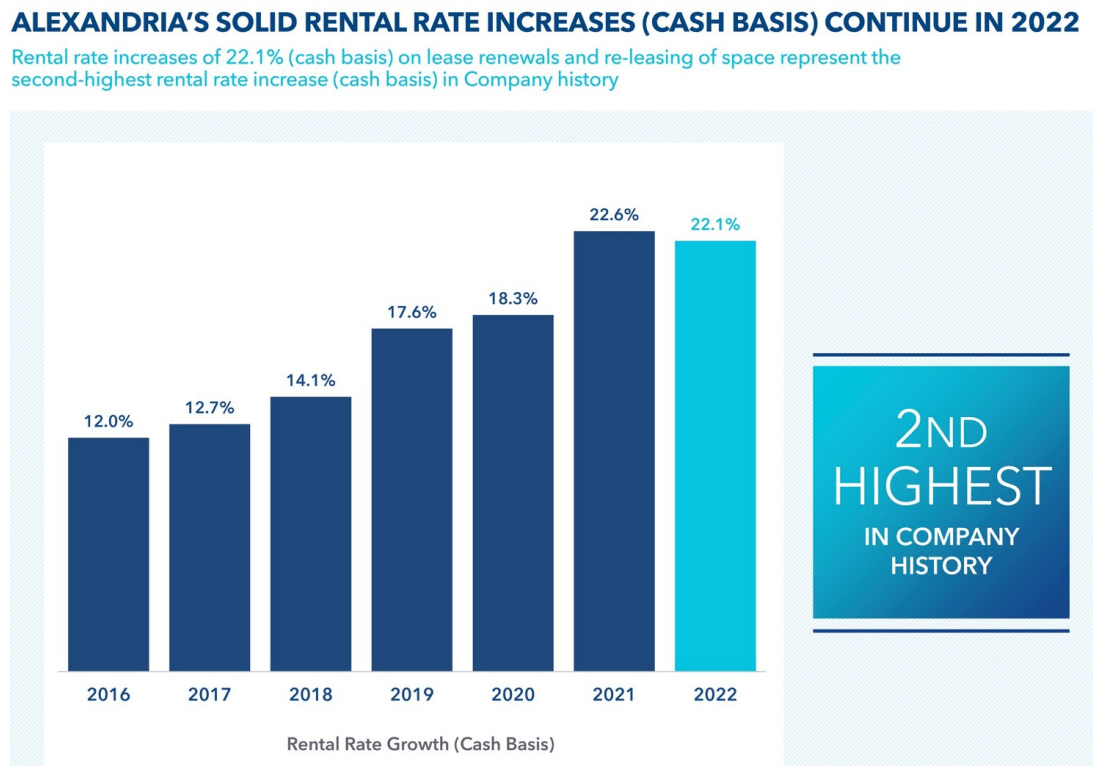

Hence we find the cash leasing spreads (rent growth on new and renewal leases) surging higher in recent years as biotech companies scramble to secure the best buildings to conduct R&D.

{kind=link}

ARE Q4 2022 Supplemental

What about ARE's balance sheet?

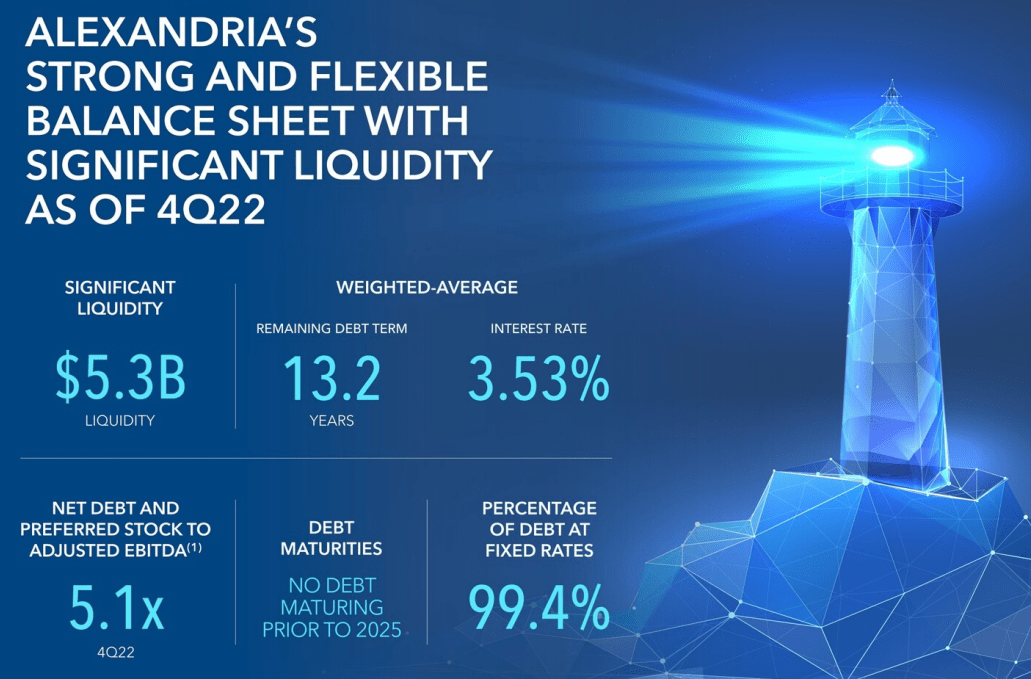

Here the unbeatable quality of ARE's properties is matched by an ultra-strong balance sheet - one of the strongest in the entire REIT space.

{kind=link}

ARE Q4 2022 Supplemental

ARE's weighted average remaining debt term of about 13 years is nearly double the weighted average remaining lease term of 7 years.

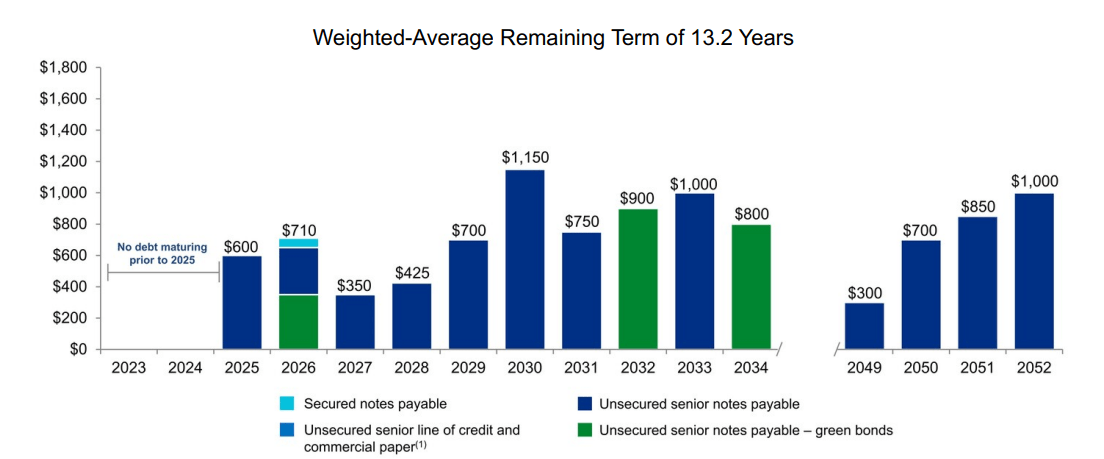

What's more, ARE's BBB+ credit rating is well-deserved, as over 99% of debt is fixed-rate with a modest net leverage ratio of 5.1x, no maturities until 2025, and a well-laddered maturity ladder thereafter.

{kind=link}

ARE Q4 2022 Supplemental

The market's two primary concerns about ARE seem to be:

- It's association with office REITs.

- The effect Silicon Valley Bank's collapse could have on its VC-funded tenants.

ARE almost always gets classified as an office REIT, so amid the office REIT apocalypse ARE has been the baby getting thrown out with the bathwater. But Class A life science properties are unique. Much of the R&D conducted in them cannot be accomplished remotely.

As for ARE's exposure to VC-funded biotech companies (in both its tenant base and its own small venture capital arm), this is not a major concern. About 90% of ARE's top 20 tenants and 48% of total tenants are either investment grade-rated or large publicly traded corporations, or both. And there are still plenty of VCs out there willing to fund promising biotech ventures. VC funding may be drying up for crypto miners and other highly speculative investments, but not as much for biotechs.

ARE's dividend yield of 3.9% is well-protected by a ~55% payout ratio, and the dividend growth record averaging ~6% annually looks likely to continue for a long time to come.

Net Lease: Agree Realty Corporation ( ADC )

I recently made an extensive case for " Why This Recession-Resistant REIT Is A Strong Buy Today ," so I'll refer you to that article and keep my comments here brief.

ADC owns a rapidly growing portfolio of 1,839 net leased retail properties. "Net lease" refers not to a property type but a set of lease terms that requires the tenant to pay for all or most of property-level expenses such as maintenance, real estate taxes, and insurance, in exchange for full control of the property premises.

Through this strategy, ADC is a highly defensive growth machine, using a combination of equity, debt, and retained cash flow to accretively acquire recession-resistant properties leased to the nation's leading retailers.

ADC April Presentation

ADC also enjoys peer-leading balance sheet strength, with only 5.4% of total debt maturing until 2028. Better yet, ADC entered 2023 with about $1.5 billion in total liquidity, including about $550 million in forward equity.

ADC is cheaper than it has been anytime in the last 5+ years based on price-to-AFFO as well as dividend yield. The REIT yields 4.3%, has a ~75% payout ratio, and has grown its dividend at an average annual pace of 6% over the last 10 years.

Industrial: Rexford Industrial Realty ( REXR )

REXR is an industrial REIT concentrated entirely in the extremely supply-constrained Southern California market, and it exudes quality in every conceivable way.

- It provides essential (and quite scarce) industrial space in Southern California.

- It enjoys multiple competitive advantages such as relationships that allow it to buy off-market properties at 5-6% yields when the market value of its assets is under 4%. (Not to mention an extensive portfolio in the most supply-constrained industrial real estate market in the nation.)

- Even in the current environment, REXR's cost of capital is still conducive to external acquisitions, exemplified by the 5% debt recently issued .

- It has incredible pricing power (~60% cash leasing spreads in 2022) as well as unit growth ($400 million+ acquisitions in the first few months of 2023).

- The BBB+ credit rating exemplifies REXR's top notch balance sheet, characterized by low debt as measured by net debt to EBITDA of 3.7x.

- The management team led by co-CEO and company co-founder Howard Schwimmer is among the best in the industry.

- The dividend growth record is impeccable, sporting a 17% CAGR over the last 5 years and a 21% hike most recently.

REXR just released its Q1 2023 results , and they are just as stunning as their performance over the last few years.

REXR Q1 2023 Earnings Release

Although core FFO per share growth should slow a bit this year to 8.7% from last year's 19.5% growth, demand for REXR's space remains ultra-high as illustrated by 2023 guidance for same-property NOI growth roughly equal to 2022's red hot 10.5% cash SPNOI growth and 7.4% GAAP SPNOI growth.

Most investors will look askance at REXR because of its 26.4x core FFO multiple and 2.7% dividend yield. But REXR's quality and fast rate of growth earn it the high valuation. And assuming the REIT's annual dividend growth averages 12% for the next decade, buying at today's 2.7% starting yield would render a 10-year yield-on-cost of 8.4%.

Telecommunications Infrastructure: Crown Castle ( CCI )

US-based telecommunications infrastructure REIT CCI also recently reported Q1 2023 earnings results , which revealed no surprises whatsoever. AFFO per share grew 2% in Q1 and 2023 guidance calls for AFFO per share growth of 3%.

Shareholders are frustrated with CCI right now for two main reasons:

- The merger of T-Mobile ( TMUS ) and Sprint is resulting in some consolidation in cell tower leases, leading Sprint to cancel some of its long-term leases with CCI. The headwinds from these lease cancellations will last through 2025.

- CCI typically keeps some variable rate debt on its balance sheet. Currently, 15% of CCI's debt is variable rate, and 12% is unhedged (truly floating). In Q1 2023, interest expenses surged 23% year-over-year and 5.2% quarter-over-quarter.

But the Sprint lease cancellations are a one-time, temporary headwind that almost certainly won't be repeated with other tower tenants. Already, 75% of CCI's revenue comes from three tenants: T-Mobile/Sprint at 38% of rent, Verizon ( VZ ) at 19%, and AT&T ( T ) at 18%. CCI's infrastructure is mission-critical for its tenants, which makes its revenue streams extraordinarily stable and predictable.

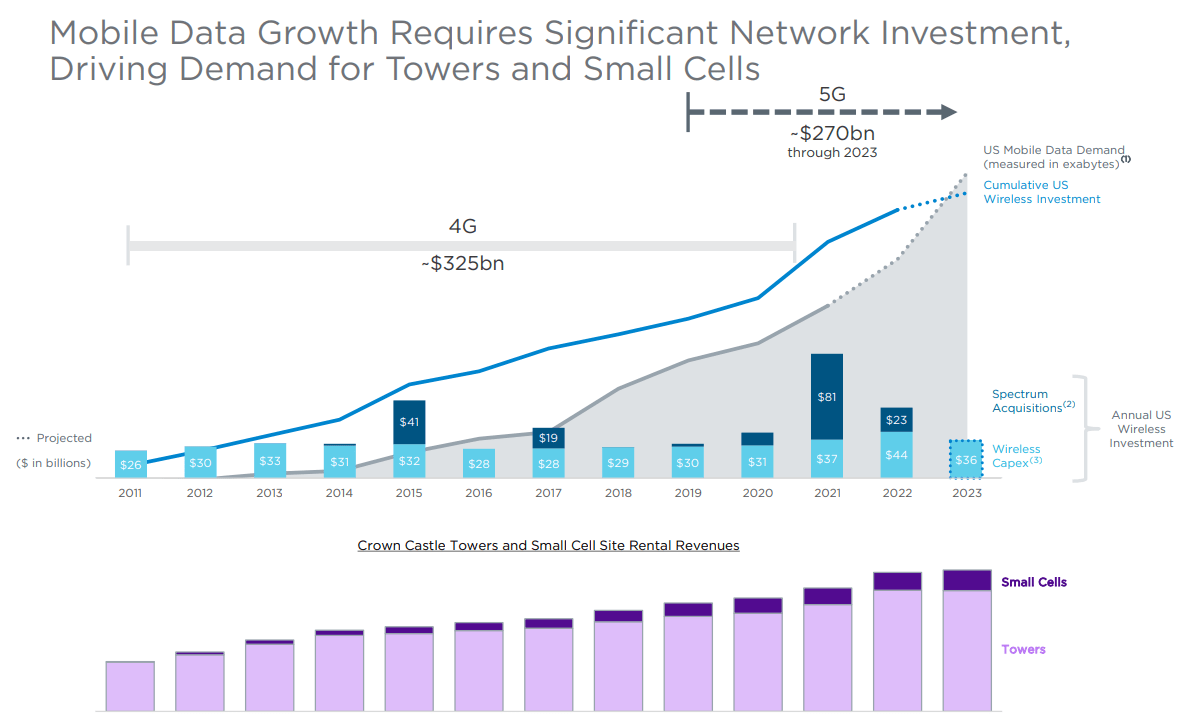

Moreover, CCI owns the most extensive portfolio of cell towers, small cell nodes, and fiber lines in the nation, which gives the REIT a dominant market position in this industry.

CCI Q1 2023 Presentation

Small cells, basically mini-cell towers installed in dense urban areas meant to boost the signal in high-traffic zones, is a unique growth channel in the 5G era.

One of the most attractive aspects of CCI's business model is the ability to add multiple tenants to the same towers/small cells with little to no additional capex. As of Q1 2023, CCI had an average of 2.4 tenants per tower with a cash yield on invested capital of 12.2%. For towers built or acquired in 2006 or before, the cash yield on invested capital is 20%, while it's 9% for those built or acquired after 2006. Across the whole portfolio, including small cells, CCI's yield on invested capital in Q1 stood at 9.6%.

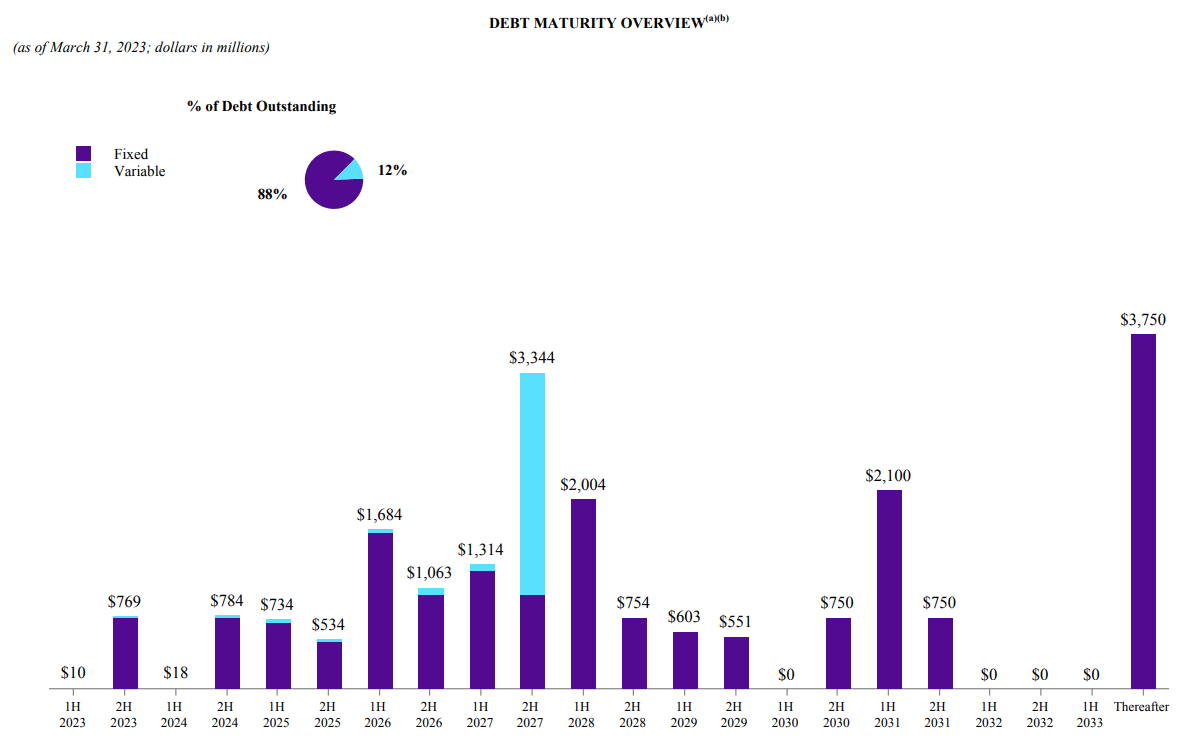

And while the floating rate debt is a weakness right now, the good news about CCI's BBB/BBB+ balance sheet is that debt is relatively low and maturities are well-laddered. Total debt to enterprise value sits at 28%. Net debt to EBITDA is very comfortable at 5.0x, and only 6.5% of total debt matures this year.

{kind=link}

CCI Q1 2023 Supplemental

The Sprint cancellations and floating rate debt are temporary headwinds, certainly, but in the long run, the future still looks bright for this quality compounder and dividend grower. Mobile data usage should continue to grow rapidly, which will require growth in infrastructure spending.

{kind=link}

CCI Q1 2023 Presentation

In the past decade, CCI's dividend has grown at an average annual rate of about 9%, although management has stated the dividend growth should come in lower than its 7-8% annual target over the next few years due to the Sprint cancellations.

Assuming 2% dividend growth through 2025 and then 7% dividend growth thereafter, buying CCI at today's 4.9% dividend yield should still produce a 10-year yield-on-cost of 8.4%.

Retail: InvenTrust Properties ( IVT )

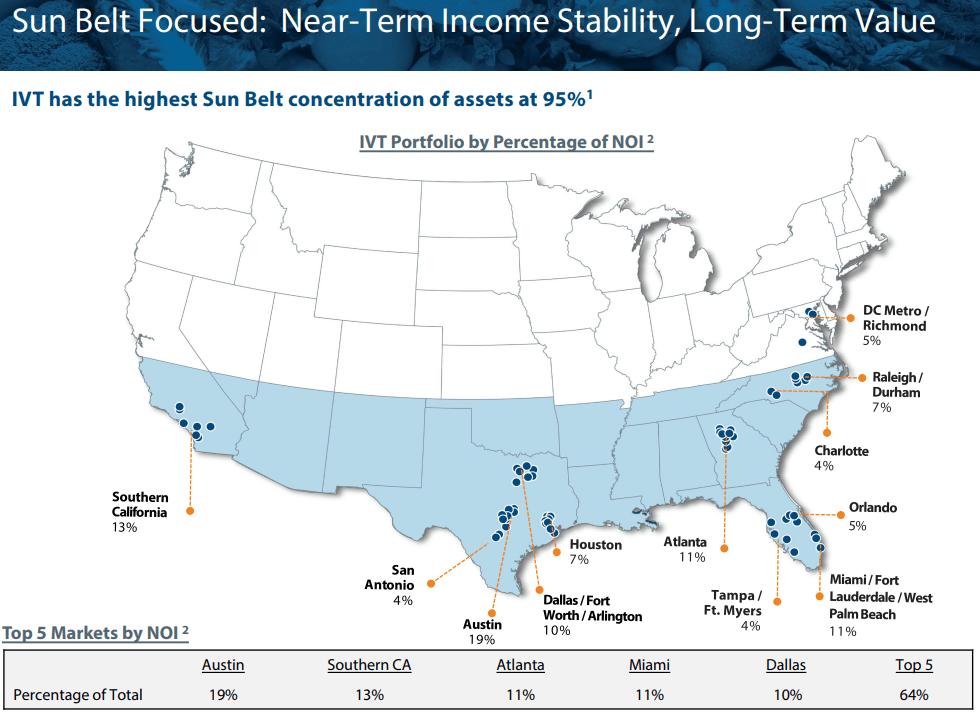

IVT is a primarily grocery-anchored shopping center REIT focused overwhelmingly (95% of properties) in Sunbelt states like Texas, Florida, Georgia, and North Carolina. In fact, IVT has the highest concentration of properties located in the Sunbelt among its anchored shopping center REIT peers.

{kind=link}

IVT Q4 2022 Presentation

As more and more people and businesses move into the Sunbelt (many of them working more often from home), IVT's centers should continue to benefit. The grocery store anchors draw significant foot traffic to the centers, and smaller tenants benefit from their presence there.

Last year was a strong one for leasing at IVT's properties. Occupancy jumped from 93.9% at the end of 2021 to 96.1% at the end of 2022, and same-property cash NOI growth came in at 4.6%, toward the higher end of its peer group:

| RETAIL REIT |

| 2022 Same-Property NOI Growth |

| 2023 Guidance SPNOI Growth |

| InvenTrust |

| 4.6% |

| 3.5-5% |

| Regency Cntrs ( REG ) |

| 2.9% |

| 0-1% |

| Kimco Realty ( KIM ) |

| 4.4% |

| 1-2% |

| Brixmor ( BRX ) |

| 6.6% |

| 1.5-3.5% |

| RPT Realty ( RPT ) |

| 4.3% |

| 1.5-3.25% |

| Phillips Edison ( PECO ) |

| 4.5% |

| 3-4% |

| Retail Opp. Inv. ( ROIC ) |

| 4.6% |

| 2-5% |

| Kite Realty ( KRG ) |

| 5.1% |

| 2-3% |

| SITE Centers ( SITC ) |

| 0.8% |

| (1%) to 2.5% |

Notice, however, that IVT expects the strongest SPNOI growth of its peer group this year. The midpoint of IVT's 2023 SPNOI growth guidance of 4.25% is 75 basis points higher than its grocery-anchored peers in Phillips Edison & Co. and Retail Opportunity Investments.

IVT recently acquired multiple shopping centers with near-term debt maturities that will need to be refinanced with higher interest rates. Hence the difference between 2023 guidance for same-property cash NOI growth of 3.5% to 5% and core FFO per share growth of 1.5% to 4.5%.

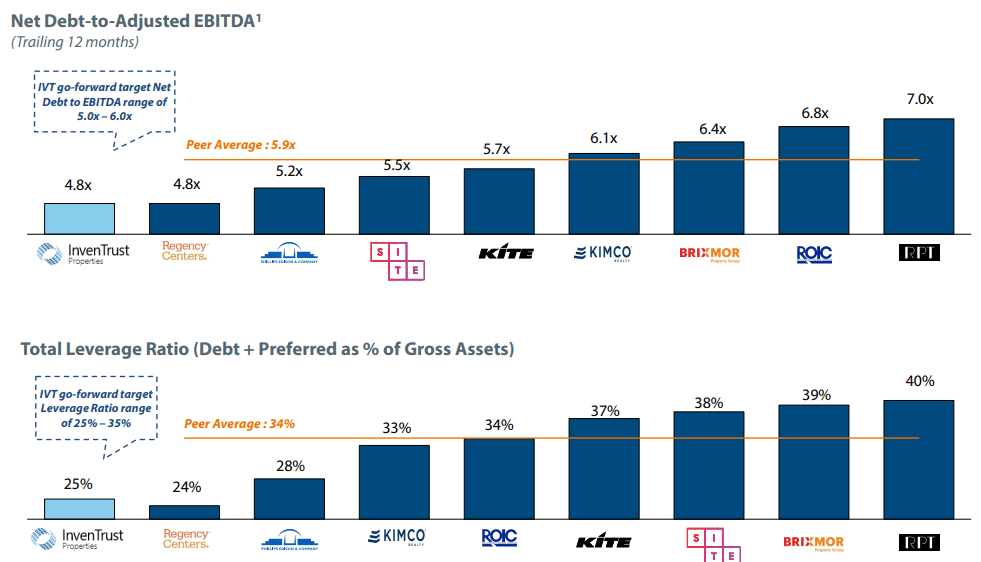

IVT also enjoys among the lowest leverage of its shopping center REIT peer group at a 25% loan-to-value and 4.8x net leverage ratio.

{kind=link}

IVT Q4 2022 Presentation

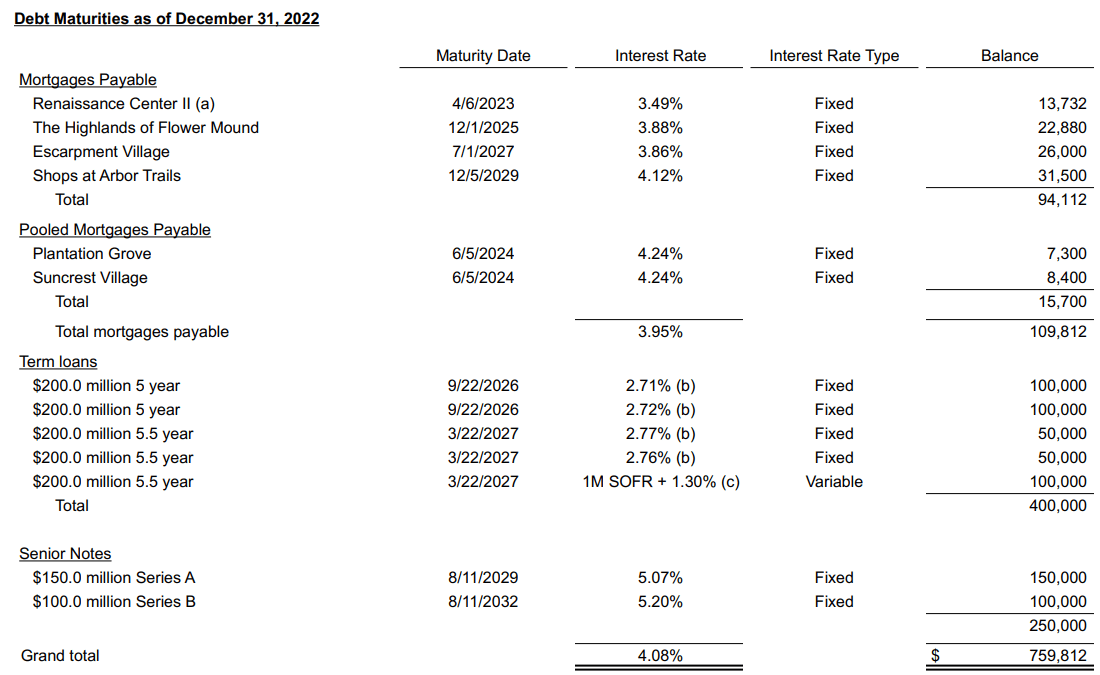

As of the end of 2022, IVT had only one loan, a mortgage, coming due in 2023, and now the maturity date has already past, so we should find out about the refinancing terms on the upcoming Q1 conference call.

{kind=link}

IVT Q4 2022 Supplemental

As you can see, though, little other debt is coming due soon. The next maturities are over a year away, in June 2024. Only 5.1% of total debt matures in 2024 and 2025, and the weighted average debt maturity currently sits at 5.0 years.

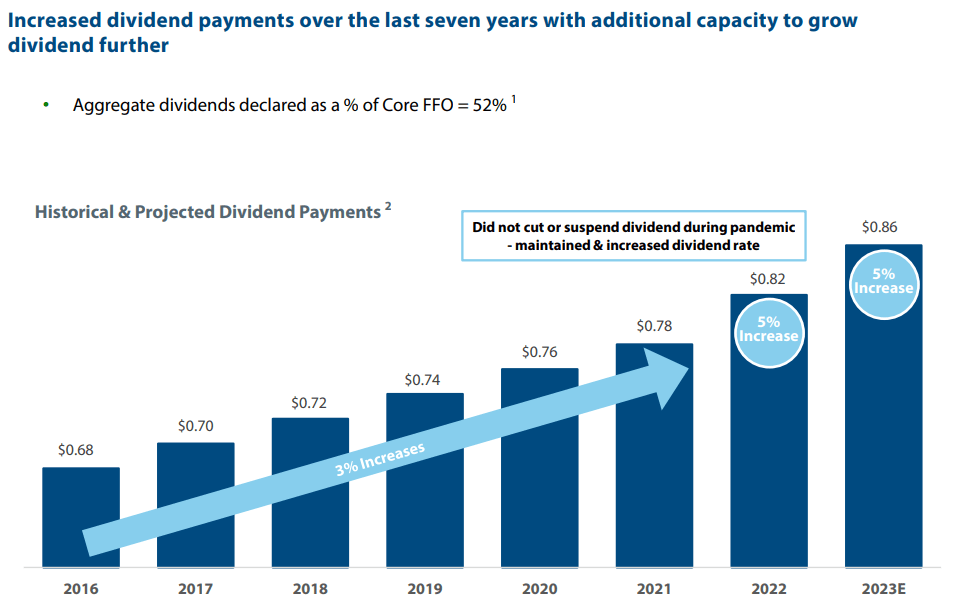

Another area of strength for IVT is the dividend growth record. Unlike most of its retail REIT peers, IVT did not cut its dividend during COVID-19 and instead gave shareholders a raise . In 2022 and 2023, IVT has upped the dividend by 5%.

{kind=link}

IVT Q4 2022 Presentation

The 2022 core FFO payout ratio came in at 52%, down from 56% in 2021. And for 2023, the payout ratio is expected to remain between 52-54% even after the hike. This very low payout ratio leaves ample retained cash flow to self-fund acquisitions and revenue-generating investments into its current properties.

Bottom Line

The current bloodshed in REITdom is a fantastic opportunity to accumulate shares of blue-chip REITs that own high-quality real estate and maintain strong balance sheets. Association with office real estate is causing all REITs to sell off, despite most of them having little to no exposure to this space.

REIT investors should rejoice at this opportunity to buy the best of the best at a rare discount. That's certainly what I'm doing.

For further details see:

Blue-Chip Real Estate Is A Bargain - Top Picks Across 5 Sectors