SCHW - Blue Tower Asset Management Q1 2023 Commentary

2023-04-24 11:46:00 ET

Summary

- Blue Tower Asset Management is an investment advisory which provides separately managed accounts. Blue Tower's approach to value investing combines proprietary screening algorithms which identify potentially attractive investments with fundamental research that seeks to determine if the stock is truly a bargain and not a value trap.

- The primary cause of our outperformance this quarter was a rapid recovery in the prices of our Sberbank and Meta Platforms holdings.

- The sanctions on Russian investments, which prevent us from buying or selling Russian stocks, caused a dramatic increase in the internal dispersion of returns for our composites.

I am happy to report that the Blue Tower Global Value returned 14.10% net of fees (14.40% gross) in Q1 2023. The primary cause of our outperformance this quarter was a rapid recovery in the prices of our Sberbank and Meta Platforms holdings.

Please review your individual account statement to see the returns on your account as it will differ from the composite return. The sanctions on Russian investments, which prevent us from buying or selling Russian stocks, caused a dramatic increase in the internal dispersion of returns for our composites. Accounts that were opened after March 2022 will not own any Russian assets and will instead have a larger weight of all the remaining positions in the strategy[1].

This quarter, we exited our homebuilder stocks of Lennar ( LEN ) and D.R. Horton (DHI). While the companies have excelled since we invested, rising rates have caused contract cancellations to explode higher and their construction backlog to shrink significantly. Compared to the Q1 of the prior year, Lennar's 2023 Q1 saw a 33% decrease in construction backlog and a 18% decline in new orders (by dollar value). The cancellation rate increased to 21% from 10% last year[2]. While both homebuilders are still quite profitable and well-run, we wanted to exit before they are impacted by an impending recession. We used the capital to buy shares of the Charles Schwab ( SCHW ) which dropped in price due to the 2023 banking crisis.

We previously wrote about our investment thesis for Schwab in our Q1 2019 letter. We later sold our position in 2020 in order to free up capital for other opportunities that became available during the chaos of the Covid crash. Now the panic over the current banking crisis has created an opportunity to reenter this investment.

2023 Banking Crisis

I will only give a brief synopsis of the banking crisis as there has already been so much written about it. Banks have always been in the business of "lending long and borrowing short" which is to say that their funding depends on demand deposits from retail and corporate depositors who are able to withdraw their capital at any time, but their investments are in securities or private loans with much longer average maturities.

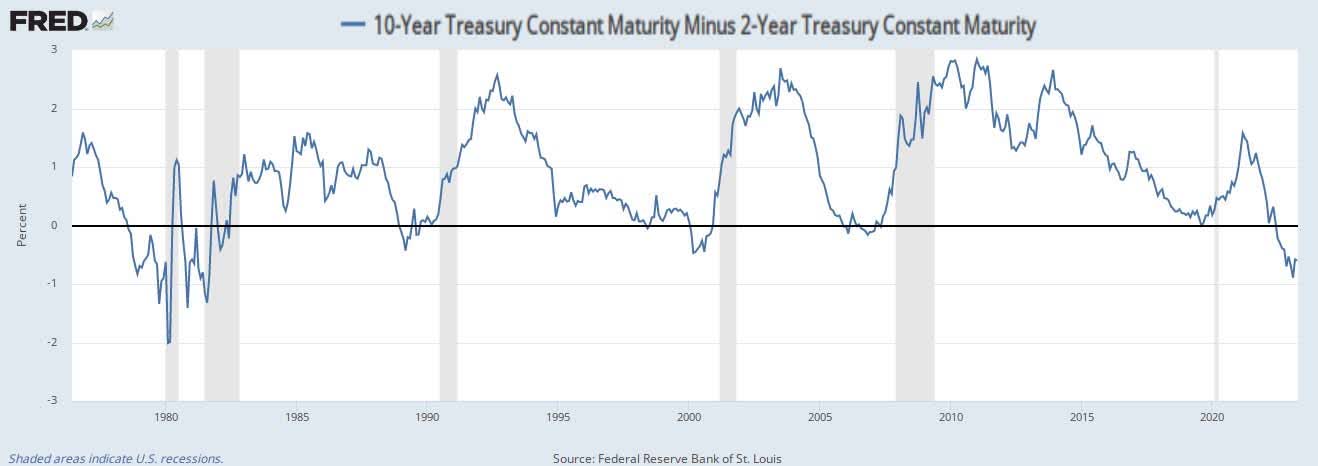

While people often focus on the ability of a yield curve inversion to predict recessions, the inverse yield curve does not so much predict a recession as it causes it. This is because by driving up the relative cost of capital for banks and other private lenders, a yield curve inversion reduces the ability of banks to make a profitable net interest margin by lending long to the borrowers in the economy. This lack of capital then reduces personal consumption and business investment.

Currently, the yield curve is more inverted than at any point since 1981 which historically would suggest that a recession is probable in 2024.

{kind=link}

Because the loans which banks have invested in are longer duration, the rise in interest rates has made them drop in value. If the loans are marked as held-to-maturity ((HTM)), then the banks do not have to recognize price changes on their accounting statements. This contrasts sharply with held-for-trading and available for sale securities which must be accounted for at the fair market value. Earned interest from HTM securities is recognized on the income statement. Under US GAAP accounting, debt securities can be classified " as HTM only if the reporting entity has the positive intent and ability to hold those securities to maturity [3] ." Therefore, once a bank attempts to begin liquidating HTM securities in order to meet liquidity needs of their depositors (such as in a bank run), it must reclassify these securities and recognize the market loss on their income statement.

With the rapid increase of interest rates over the last 18 months, many banks would have negative equity if they were forced to mark all of their HTM securities to market. This would cause a bank failure and force them into FDIC receivership. To help these banks with their liquidity needs and stave off their failures, the Federal Reserve created a new bank program, the Bank Term Funding Program (BTFP) on March 12th[4]. This allows banks to pledge as collateral certain types of debt securities in order to borrow money for up to a year without needing to sell their HTM securities. The interest rate charged to the banks under the BTFP is currently near 5%[5]. A major advantage of the BTFP is that use of the program will be confidential until one year after the program ends, so banks won't have to worry about creating a public perception that they are grappling with liquidity problems.

Charles Schwab Grapples with High Rates

Schwab began as one of the first low-cost electronic brokerages in 1971. Over the years, Schwab's banking division and financial advisor custody services have both grown to be an increasingly large portion of the business.

An equity brokerage business like Schwab is very attractive due to scale providing a barrier to entry. The costs of running a brokerage are largely fixed, so the industry naturally evolved to an oligopoly of a few major players that can all earn attractive returns on capital. Schwab's bank allows customers to have their banking and brokerage needs integrated under one roof. Charles Schwab Bank has grown to become one of the largest banks in the country, and at the end of 2022 had $126.6B of bank deposits in 1.7M accounts. Schwab acquired T.D. Ameritrade and the investment management business of USAA in 2019 and at the end of 2022 had $7.05T of client assets in 33.8M accounts. Schwab is now the second largest broker in the United States, with only Vanguard holding more assets.

When clients invest their money at Schwab's brokerage or keep money in Schwab Bank, they only collect a small interest from Schwab on their cash balances. These clients are fairly yield insensitive as they are storing their money at Schwab primarily for the convenience and the overall utility and service of the platform. In an April 6th statement, the two co-chairmen of the firm wrote " we know there is a level of cash clients prefer to keep in a highly liquid form, what we call transactional cash. That is money available to take advantage of investing opportunities that arise or for day-to-day personal cash flow needs. Typically, that transactional cash is in the range of 5-10% of a client's overall assets here at Schwab. [6] " Schwab can then invest this cash at market rates of interest which is much higher than what they pay for these cash balances. Over the years, net interest has become an increasingly large proportion of Schwab's income. In 2022, net interest revenue made up 51% of all net revenue.

Generally, higher interest rates translate into Schwab generating higher net interest revenue. Schwab's 2019 annual report had a rate sensitivity analysis which showed that a 100 basis point increase in rates led to a 4.8% increase in net interest revenue and the opposite led to a 7.4% decrease. Rate increases expand the spread that they collect. However, too much of a good thing can be toxic.

The rate increases have made many of the rate insensitive customers begin to rethink their capital allocation as they move cash from uninvested bank and brokerage balances into money market funds at the brokerage arm. As rates increase, more customers pull their cash from uninvested into money market funds. If Schwab is forced to access programs like the BTFP or write CDs in order to meet liquidity needs, then their cost of capital increases. Currently, Schwab pays interest rates of between 0.45%-0.48% APY for uninvested cash in checking accounts, brokerage accounts, and savings accounts. However, some of their CDs and money market funds pay as much as 4.94% and 4.84%, respectively 7 . Schwab believes that this rotation will eventually slow down as customers desire some cash to be uninvested and available for transactions.

The Federal Reserve's rate increases in 2022 and 2023 so far exceeded Schwab's forecasts. At the end of 2022, Schwab had unrealized losses of over $29 billion in their HTM securities. Their HTM balance sheet is generally made up of fixed income securities. As these HTM securities mature, their unrealized losses will decrease as their market price moves towards the par value. The danger is if they are forced to sell their HTM portfolio before they can mature in order to meet customer redemptions.

Fortunately, the Charles Schwab Corporation has a very deep liquidity pool. At the end of 2022, their Tier 1 capital leverage[7] was at 7.2% vs. the 4.0% required minimum. For the consolidated corporation, this translates to $40.3B in Tier 1 capital vs $22.5B required. The aforementioned programs and measures mean that they can access additional capital without needing to liquidate. The size and financial strength of Schwab is an advantage to attracting worried depositors during a banking crisis. The company reported that in the month of March, the firm pulled in $53 billion of net new client assets 5 .

In summary, we do not believe that Schwab is at risk of a liquidity crisis. They have deep pools of capital reserves and have many sources of liquidity that they can access. Higher interest rates help their main engine of profitability in the long-term. They should remain profitable enough to earn their way out of the unrealized losses they have accumulated before it becomes an issue. The concentration dynamics of the brokerage industry give them a sustainable business advantage.

Schwab in the Blue Tower Portfolio

Our investment in Schwab is not based upon a variant perception on interest rate forecasts or their earnings and revenue for the next few quarters. Rather, we believe that Schwab is a high quality business, will be able to survive the current crisis, and thrive for the long-term.

The current valuation is cheap after the drop and suggests a high forward rate of return. Current analyst consensus forecasts are for an 11.6% growth in net revenues for 2024 over 2023. At a $50.77 price and a consensus $4.47 EPS for 2024, it trades at a forward PE of 11.3. We don't have a specific price target in mind, but instead will compare our estimated forward rate of return for Schwab to our other opportunities.

Our current position size in Schwab is relatively small. Depending on the Federal Reserve's rate hike decisions, the banking crisis could become significantly worse. This could also cause the unrealized losses in Schwab's investment portfolio to become much worse, and the stock price to decline further. As long as we continue to believe the chance of their insolvency to be low, we will use price drops as an opportunity to build our position.

Update on our Russian Investments

Sberbank's (AKSJF) board of directors recommended paying a 25? per ordinary share dividend later this year. The fixing date for the dividends will be May 11th of this year. Sberbank had opted to avoid paying a dividend last year in order to build up their financial reserve for dealing with sanctions. The company has adapted well for the current circumstances and believes it will have a recovery in its earnings from the drop last year. Due to sanctions, our dividends from Sberbank will be stuck in either a "type-C" bank account in Russia or an OFAC escrow account in the United States.

Interactive Brokers began the process this past quarter of opening separate OFAC escrow accounts for sanctioned securities. Each account with sanctioned securities will have its own side pocket escrow account created. When this process is complete, all of our Sberbank shares will be held in these accounts. These escrow accounts are a new structure for Interactive Brokers, and their programming team is still troubleshooting some bugs that have popped up with it.

On February 25th 2023, Tinkoff Bank, the subsidiary bank of TCS Group, finally came under sanctions with the passing of the EU's tenth package of sanctions against Russia. These sanctions include asset freezes and led Tinkoff to suspend trading in Euros. Unlike our Sberbank ADRs which have been converted to local shares, we still have no changes in the status of our investment in TCS Group. As a Cyprus corporation, TCS is unaffected by the new Russian law banning foreign depository receipts. However, the London Stock Exchange continues to prevent trading of the global depository receipts (GDR) on their exchange. The USD-equivalent price of TCS Group on the Moscow Exchange and the pricing of our depository receipt at Interactive Brokers can be seen in the table below.

| London GDR price @ Interactive Brokers |

| MOEX Price (Rubles) |

| GDR price in USD based on MOEX[8] |

| TCS Group |

| $3.19 |

| 2651.50? |

| $32.51 |

Price as of April 14th, 2023

I look forward to receiving your questions and comments, and appreciate your continued support of our firm.

Best regards,

Andrew Oskoui, CFA Portfolio Manager

Disclaimer : This commentary does not represent a recommendation to trade any particular security, but is intended to illustrate Blue Tower's investment approach. These opinions are current as of the date of this commentary but are subject to change. The information contained herein has been obtained from sources believed to be reliable but the accuracy of the information cannot be guaranteed. Past performance is no guarantee of future results.

[1] Additionally, we will not be able to adjust the weighting of Russian stocks to account for deposits/withdrawals of existing investors. Sberbank shares appreciated this quarter leading to investors with Russia exposure outperforming the overall composite.

[2] Lennar 1st quarter 2023 earnings release, https://www.prnewswire.com/news-releases/lennar-reportsfirst-quarter-2023-results-301771966.html

[3] ASC 320-10-25-1(c) a

[5] The BTFP will lend at the one-year overnight index swap rate plus 10 basis points

[6] Our Latest Perspective on Industry Events 7 Cash Investments

[7] Tier 1 capital ratio is a measure of financial strength calculated by dividing a firm's equity capital and disclosed reserves by the total risk-weighted assets of the firm. It was adopted as part of the Basel III Accord on bank regulation

[8] Ruble/USD exchange rate based on IBKR market close rate of April 14th, 2023: 0.012262

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Blue Tower Asset Management Q1 2023 Commentary