BVHBB - Bluegreen Vacations: Double-Digit Quarterly Net Sales Growth And Undervalued

2023-10-25 04:11:31 ET

Summary

- Bluegreen Vacations reported double-digit quarterly net sales growth.

- The company has acquired resorts in 2023 and has significant construction in progress, indicating potential capacity increases.

- Bluegreen Vacations is trading cheaper than competitors and has the potential for future free cash flow growth.

Bluegreen Vacations Holding Corporation ( BVH ) delivered double-digit quarterly net sales growth and recently announced more acquisitions of resorts in 2023 and significant increases in construction in progress. With these figures, I believe that we may see significant increases in BVH capacity in the coming years, which may enhance FCF expectations. Bluegreen Vacations also appears to be trading cheap as compared to other peers in terms of EV/3 Years Median EBITDA, and DCF model implied undervaluation. Even taking into account risks from the total amount of debt or shareholder concentration, Bluegreen looks like a must-follow stock.

Bluegreen Vacations Holding: Double-Digit Quarterly Net Sales Growth y/y

With 46 hotels and resorts under its ownership and management and with another 23 clubs associated through joint programs, Bluegreen Vacations is a company in the tourism industry that offers vacation packages within urban environments as well as in the Caribbean islands.

There is a peculiarity in the business model of this company since in addition to offering direct contacts for the booking and stay of tourists, it offers a series of vouchers in point formats called vacation ownership interest through which the owners of these vouchers can exchange their points for services within the company's properties or their joint agreements.

By paying for these programs that offer points to use some of the company's facilities or other hotels, the owners and participants of the joint membership programs have access to more than 7,000 hotels throughout the world, some of them are well-known chains and some are day-passing hotels. The payment and purchase of these vouchers not only allow the use of hotel facilities but also offer a very small percentage interest sum on these properties, which means that the company is mainly dedicated to the management of hotel capacities.

The company's operations are divided into two operating segments: one that covers the sale of property interests and another that deals with the management and administration of the hotel facilities. In this sense, it is good to note that the revenue that comes from the segment from the sale of property interests is considerably greater than that of the hotel management segment.

With that about the operating segments, it is worth noting that the recent quarterly report included growth from the sale of interests and revenue from resort and club management. We are talking about total quarterly revenue growth of close to 10% y/y.

Source: 10-Q

Balance Sheet

As of June 30, 2023, Bluegreen Vacations reported cash worth $178 million, with restricted cash of about $52 million, which I believe is a considerable amount of money to finance further design of vacation packages.

The company also reported notes receivable of close to $618 million, vacation ownership interest inventory worth $447 million, and property and equipment of about $87 million. Total assets stand at about $1.525 billion, more than 1x the total amount of liabilities. With these figures, I believe that the balance sheet appears quite solid.

Source: 10-Q

I do not think the total amount of debt is significant because Bluegreen Vacations delivers positive FCFs. However, I believe that most investors out there would appreciate the information about the interest rates being paid and how it does affect the cost of capital. In the last annual report, I saw interest rates close to 4% and 6%-7%. With this in mind, I believe that the WACC may be larger than 6%-7%.

The note payable to BBX Capital accrues interest at a rate of 6% per annum and requires payments of interest on a quarterly basis; provided, however, that interest payments may be deferred at the option of the Company, with interest on the entire outstanding balance thereafter to accrue at a cumulative, compounded rate of 8% per annum until such time as the Company is current on all accrued payments under the note, including deferred interest. Source: 10-k

Woodbridge’s junior subordinated debentures accrue interest at a rate of 3-month LIBOR plus a spread ranging from 3.80% to 3.85%, mature between 2035 and 2036, and require payments of interest on a quarterly basis. Source: 10-k

The list of liabilities includes accounts payable worth $25 million, deferred income close to $16 million, receivable-backed notes payable of close to $19 million, and receivable-backed notes payable non-recourse worth $505 million. Besides, with note payable to BBX Capital, inc. of close to $35 million, total liabilities stood at about $1.243 billion.

Source: 10-Q

Given The Know-How Accumulated And Marketing Efforts, I Assumed That Further FCF Growth Will Occur Thanks To Organic Growth.

As we said, the core of Bluegreen's operations involves the financial services segment and the sale of interest in hotel facilities. The business strategy involves expanding marketing channels and approaching customers through promotions and offers of tourism programs to generate sales directly in this sense. Given the expertise of management and the number of hotels being run, I believe that Bluegreen Vacations will most likely know how to reach new customers and grow organically. As a result, under my DCF model, I assumed that FCF will most likely grow.

A More Diversified Offering, Economies Of Scale, And Further Acquisition Of Resorts Will Most Likely Lead To FCF Margin Expansion

The current objectives are to expand the operating margins along with an acquisition strategy that allows the company to develop an even broader and more diversified hotel offering. In my view, as soon as the net leverage decreases a bit, and debtholders approve the acquisition of new hotels, we can expect further net income growth.

Bluegreen continues to pursue opportunities for new resort or land acquisitions. Source: 10-Q

With that about the intentions of management, it is also worth considering that Bluegreen Vacations will most likely experience net sales growth and FCF growth thanks to recent acquisitions made in 2023. In this regard, there is the acquisition of a resort in Branson, Missouri, and a resort located in Nashville, Tennessee.

In April 2023, Bluegreen/Big Cedar Vacations purchased a resort in Branson, Missouri for $7.1 million including transaction costs. The transaction was accounted for as an asset acquisition with the purchase price allocated to VOI inventory in the Company’s unaudited consolidated balance sheet as of June 30, 2023. Source: 10-Q

In May 2023, the Company purchased the property and other assets of a resort located in Nashville, Tennessee for approximately $53.6 million including transaction costs. The transaction was accounted for as an asset acquisition. Of the purchase price, $51.6 million was allocated to VOI inventory and $2.0 million was allocated to certain property and equipment in the Company’s unaudited consolidated balance sheet as of June 30, 2023. Source: 10-Q

Construction In Progress Increased Significantly In 2023, So I Would Be Expecting Increases In Capacity Soon

Bluegreen Vacations reported an increase in construction in progress in 2023. It increased from close to $8 million to about $100 million. With these figures in mind, I believe that many investors out there may be expecting increases in capacity and further increases in net sales expectations.

{kind=link}

Free Cash Flow Model

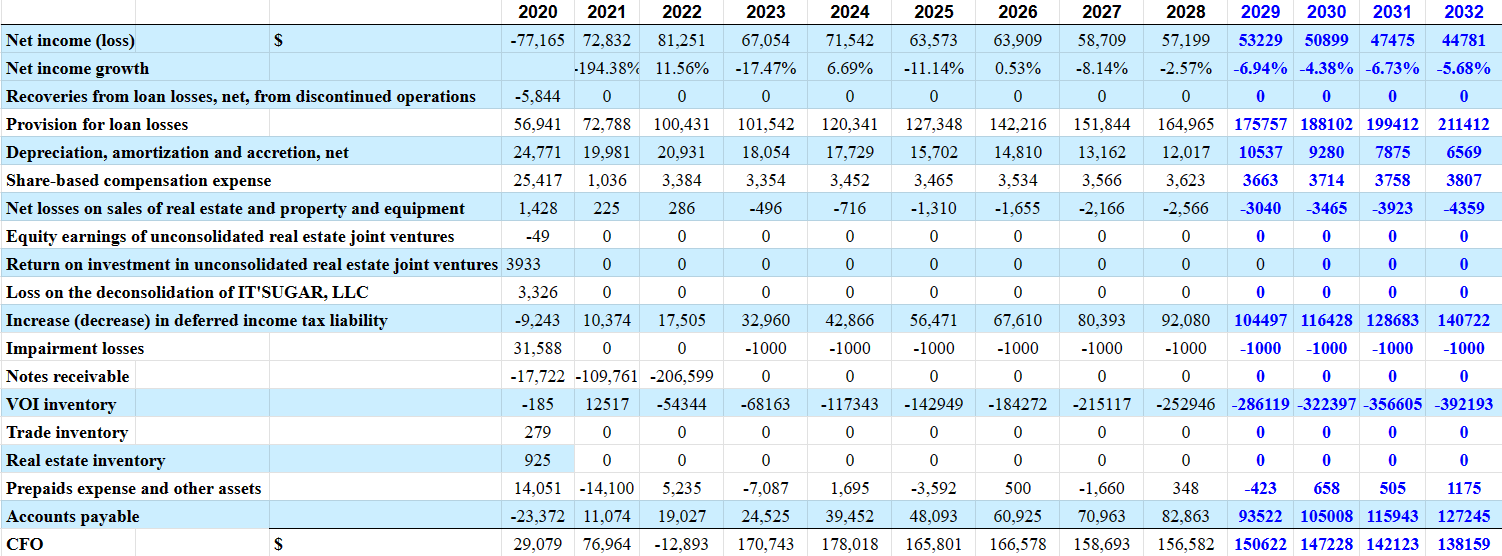

For the assessment of future cash flow statements, I assumed previous assumptions and previous financial figures like net income, changes in accounts payables, changes in receivables, and previous FCFs.

Source: YCharts

I assumed a future 2032 net income of close to $44 million, 2032 provision for loan losses of about $211 million, 2032 depreciation, amortization, and accretion of close to $6 million, and share-based compensation expenses of close to $3 million.

Additionally, with net losses on sales of real estate and property and equipment close to -$5 million, increases in deferred income tax liability close to $140 million, and changes in VOI inventory of about -$393 million, I included changes in accounts payable close to $127 million.

{kind=link}

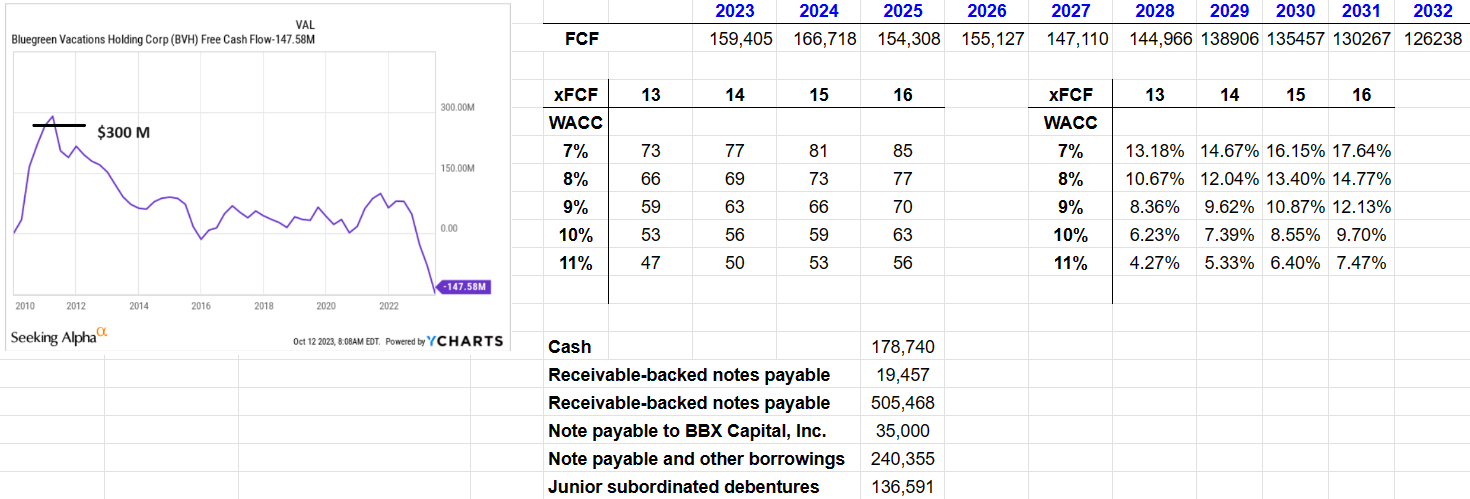

Finally, I obtained 2032 CFO of close to $138 million, capex worth -$12 million, and 2032 FCF of close to $126 million. The median FCF from 2020 to 2032 would be close to $138 million.

{kind=link}

Taking into account the 10 years, 7 years, and 3 years median, the EV/FCF multiple would be close to 13x-19x FCF. With these figures in mind, my terminal EV/FCF would be between 13x and 16x.

Source: YCharts

If we also include a cost of capital between 7% and 11% and EV/FCF of 13x-16x, the implied price target would be between $47 and $85 with a median close to $56-$66 per share. Besides, the internal rate of return would stand at about 4% and 17% with a median close to 9%-10%.

{kind=link}

Competitors

Marriott Vacations Worldwide Corporation ( VAC ) and Hilton Grand Vacations ( HGV ) are the companies with the greatest operational capacity and the greatest recognition. They operate within the hotel market and sell interest portions directly or indirectly on their own hotel capacities. In terms of EV/3 Years Median EBITDA, Bluegreen Vacations is trading cheaper than VAC and HGV with a larger EBITDA margin.

Source: YCharts Source: YCharts

There are other entertainment companies outside the intrinsic hotel market that offer similar services. In any case, at present, these companies do not generate direct competition for Bluegreen Vacations. With regard specifically to the competition over the management and administration of hotels and resorts as well as tourism facilities, there are a large number of participants in this industry that are not limited only to traditional markets, but also add new booking platforms as well as electronic and other hosting systems with growing trends.

Risks

It is important to note that a large amount of the shares of this company are in the hands of a few owners. Certain minority shareholders may not appreciate that a significant part of the voting power is controlled by a few directors. Their interests may be different from that of minority investors. As a result, we may see lower demand for the stock.

Several directors of the Company, currently collectively beneficially own 6% of the Company’s Class A Common Stock and 75% of the Company’s Class B Common Stock which in the aggregate represent approximately 81% of the total voting power of the Company’s Class A Common Stock and Class B Common Stock. This control position may have an adverse effect on the market price of the Company’s Class A Common Stock and Class B Common Stock. In addition, their interests may conflict with the interests of the Company’s other shareholders. Source: 10-k

In addition, the company reports large agreements with partners like Bass Pro, which represent a significant part of the total amount of interest sales. It is a risk because trouble with this large partner may lead to a significant decline in sales.

During the three months ended March 31, 2021 and 2020, VOI sales to prospects and leads generated by the agreement with Bass Pro accounted for approximately 13% and 10%, respectively, of our VOI sales volume. Subject to the terms and conditions of the settlement agreement, we will generally be required to pay the fixed annual fee with respect to at least 59 Bass Pro retail stores and a minimum number of Cabela’s retail stores that increases over time to a total of at least 60 Cabela’s retail stores by the end of 2021 Source: 10-Q

With this, we must point out the risks of the hotel industry as well as the construction industry in the development of facilities. Lastly, we can add that the company's own business system involves a series of financial risks in the purchase and repurchase of ownership interests in the market.

Conclusion

Bluegreen recently reported double-digit quarterly net sales growth. With recent acquisition of resorts in 2023 and construction in progress increases, Bluegreen Vacations will most likely deliver capacity increases, which may enhance net sales growth expectations in the coming years. Also, trading a bit cheaper than other large competitors, such as Marriott Vacations Worldwide Corporation or Hilton Grand Vacations, Bluegreen Vacations looks cheaper if we look at future FCFs. I do obviously see risks from the total amount of debt, shareholder concentration, or the relationship with Bass Pro, however, the company remains cheap.

For further details see:

Bluegreen Vacations: Double-Digit Quarterly Net Sales Growth, And Undervalued