BXC - BlueLinx Q4 Earnings: At 4x EPS This Is Attractive

Summary

- BlueLinx has been on a tear in the past 3 months, together with many of its peers.

- BlueLinx's guidance for Q1 is less than optimal. That being said, I don't believe its Q1 guidance is as bad as analysts expect.

- According to my calculation, BlueLinx is priced at 4x EPS.

Investment Thesis

BlueLinx ( BXC ) has seen investors clambering into the stock in the past 3 months, with its share price substantially outperforming the S&P 500. Accordingly, the stock had to prove itself with this report.

Furthermore, BXC put out Q1 guidance that left a lot to be desired. However, I argue that its guidance, despite being bad, isn't quite as bad as analysts expect.

According to my calculations, the stock is priced at 4x EPS.

What's Happening in the Market?

In the past 3 months, homebuilding stocks have been strong and substantially outperformed the S&P 500. That's despite all the fears of rising rates and the impact that would have on housing. The market is attempting to sniff out the end of the pain trade in housing.

Put more simply, expectations for BlueLinx were high as the company headed into this earnings report. But as you'll read through, the outlook could actually support that bullish view.

But before that, let's discuss some negative considerations.

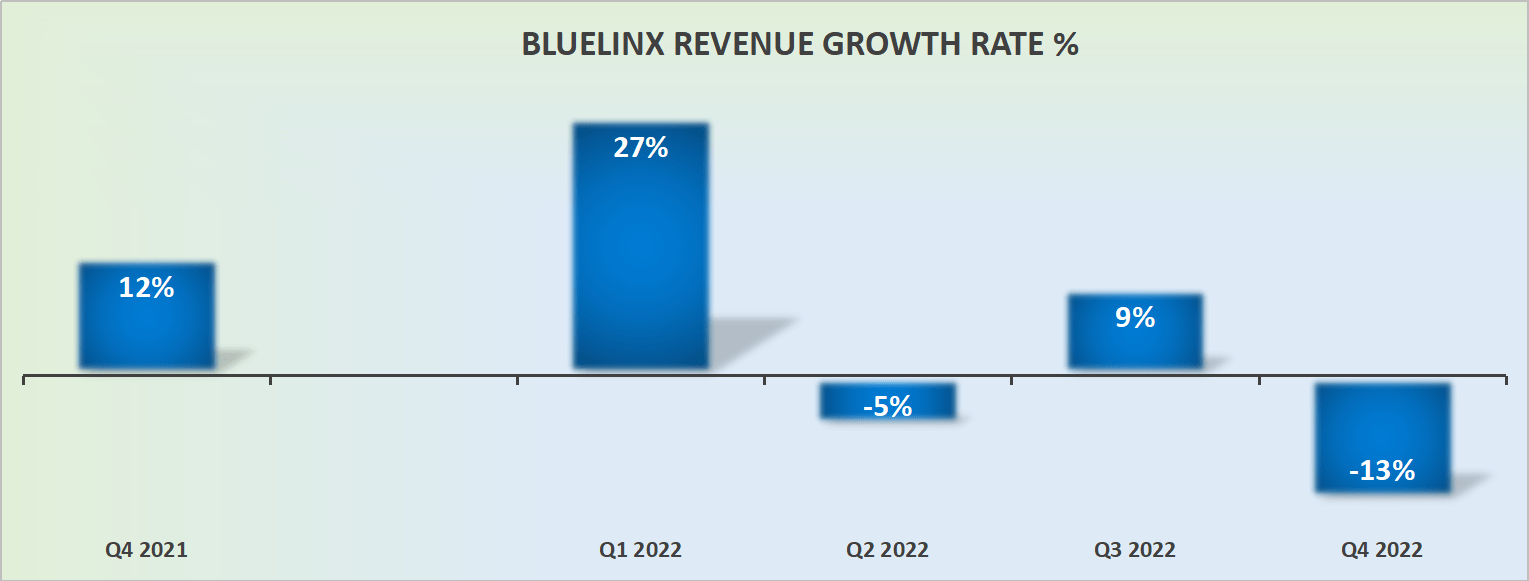

Revenue Growth Rates Turn Negative

{kind=link}

Few investors had any hopes that BlueLinx's Q4 revenue growth rates would be anything but negative. But what investors perhaps didn't expect is for BXC to report negative 13% y/y growth rates. That's quite a dramatic shift from the overall trajectory for 2022.

Looking ahead to Q1, management guides for its Specialty product volumes to be down 15%, while its Structural products volumes are flat with the prior year.

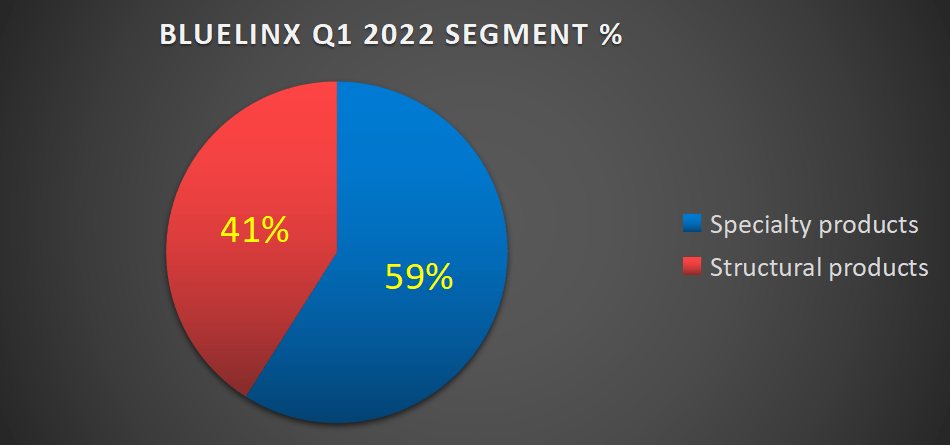

In the graphic that follows I've taken the segment breakdown from last year's Q1 to help us figure out how the guidance is likely to play out.

{kind=link}

What you see here is that approximately 60% of the business last year was made up of its Specialty products. So, we can surmise that the performance of BXC's specialty products has a larger impact on BXC's bottom line performance than its Structural products.

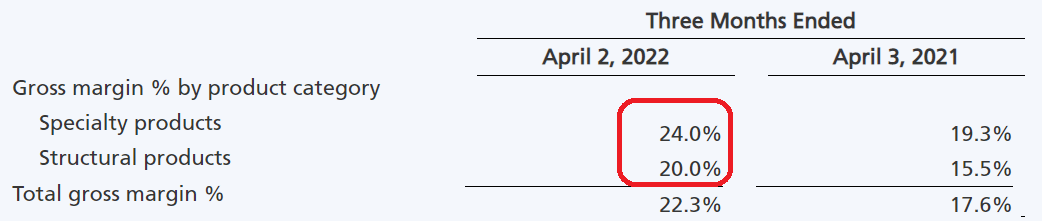

And then, take into consideration the margin profile of its segment from last year's Q1 2022.

{kind=link}

For Q1 2023, BXC's Specialty products are expected to be approximately 19% at the high end. While its Structural products' gross margins are expected to be around 11% at the high end.

So, it's not only that the margins will probably average around 14%, but that the overall volume of revenues will also be down at least 10%.

Operating Leverage Cuts Both Ways

In last year's Q4, the company posted 12% y/y revenue growth rates, and this allowed its EBITDA margins to expand to close to 12% EBITDA margins (as a percentage of sales).

While this time around, its revenue growth rates compressed, leading its EBITDA margins to compress by approximately 390 basis points and to land just higher than 7%.

So, let's have no doubts that BXC is indeed on the back foot. Lumber prices are down and volumes are also down, which combined will see BXC's margins come down from about 22% to somewhere close to 14%.

But does this mean that compared with a year ago, BXC's EPS will be down 70% y/y? I'm not sure. Perhaps EPS gets cut by 55% y/y or even 60%. But I'm not sure that analysts' expectations of a cut of 74% y/y is justified.

SA Premium

If I assume a 60% cut to BXC's EPS for Q1, that would imply that BXC's EPS would end up around $5.28, that's significantly higher than analysts' expectations of $3.46.

Furthermore, I'm inclined to believe that even if I'm too bullish on my Q1 expectations, I've certainly got a margin of safety built into my calculations.

BXC Stock Valuation -- 4x EPS

To be frank, BXC has entered a downturn in economic activity. BXC's statements lead me to believe that since the start of Q4, its prospects have dimmed.

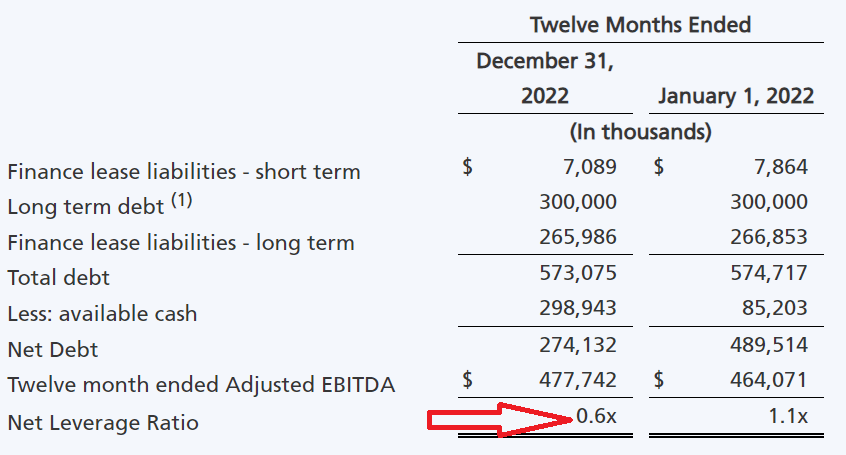

That being said, there's no doubt that its balance sheet enters this part of the cycle in a substantially better positioned than it was this time last year.

{kind=link}

So, not only is its balance sheet much stronger, but I don't believe that the business is going to be unprofitable in the very near term.

While it's quite impossible to predict how things will unfold in 2023, I'm inclined to believe that from the outlook in Q1 through to the end of 2023, things will remain stable, and not worse.

Consequently, according to my estimates, I believe that BXC will probably report around $19 of EPS in 2023. That's a 60% cut to BXC's EPS figures reported in 2022.

This leaves the stock priced at 4x EPS.

The Bottom Line

There are many reasons not to get involved with BXC. For one, its near-term prospects are getting weaker, not stronger. Indeed, its guidance for Q1 tells us this much.

But from my understanding, nobody is arguing that the business is going to be unprofitable. Yes, there's a setback in its intrinsic value, but at the same time recall that BXC's balance sheet is meaningfully stronger than in prior downturns.

Altogether, I'm bullish on this stock.

For further details see:

BlueLinx Q4 Earnings: At 4x EPS, This Is Attractive