INVH - Bluerock Homes Trust: Softening Real Estate And Financial Losses Overshadow Advantages

2023-10-05 17:48:36 ET

Summary

- Bluerock Homes Trust's stock price has dropped by half since its public listing in September 2022, which is unsurprising at a time when the single-family rental market is softening.

- Despite market challenges, the company comes with good credentials, has a promising market and has been profitable at the operating level in the past.

- However, its latest operating loss, lack of dividends and some unfavourable market multiples work against it.

Since its public listing in September 2022, the real estate investment trust [REIT] Bluerock Homes Trust ( BHM ) has seen its price drop to half its opening levels. To be fair, it hasn’t exactly been a good time for real estate, with rising interest rates and high inflation eating into buyers’ budgets. The S&P 500 Real Estate Index is down by almost 11% in the past year, in contrast with the 12% rise in the S&P 500 ( SP500 ) over the same time.

Single-family rental market softens

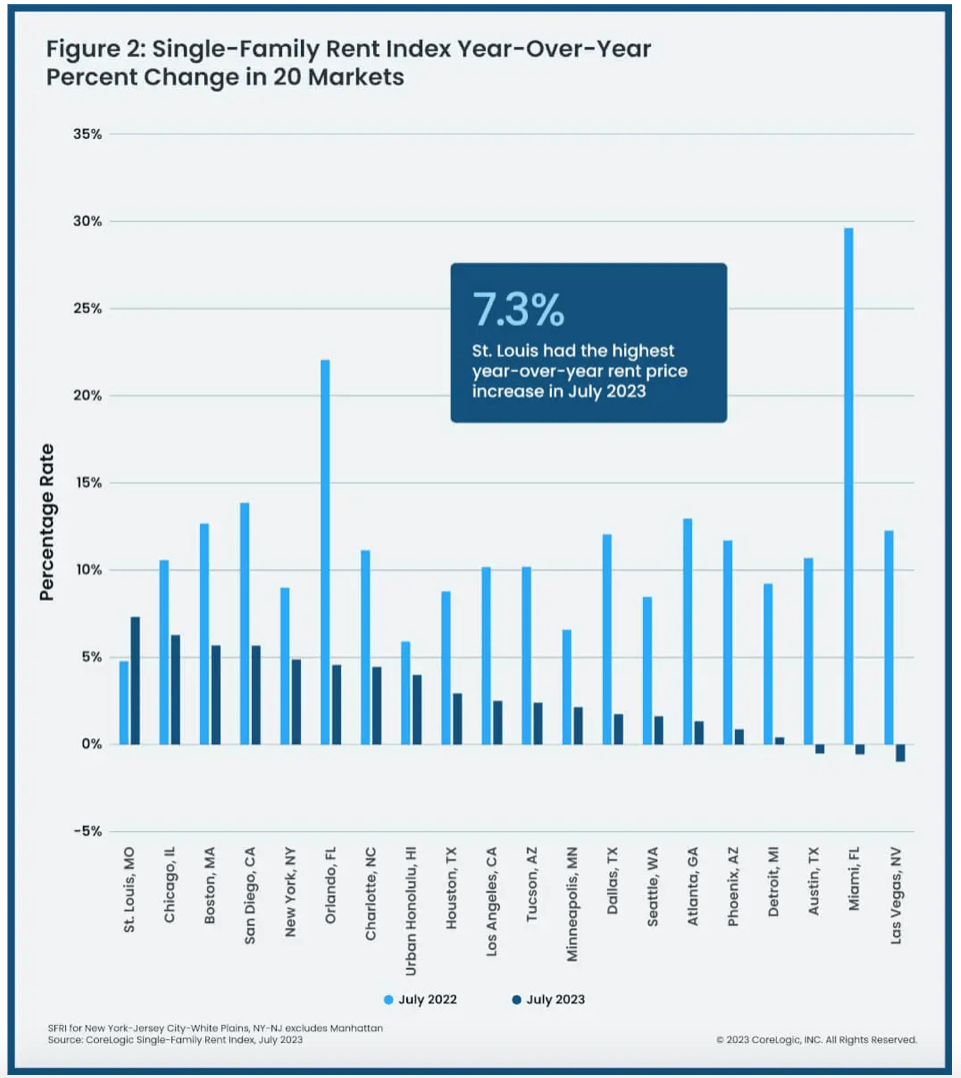

This also shows up in trends for single-family rentals, which is the focus of BHM. According to CoreLogic, a provider of real estate industry data and analytics, growth in single-family rents continued to slow down for the 15th straight month in July to grow by 3.1% year-on-year (YoY) in July. Even though BHM targets communities in growth areas, the slowdown is visible for it too, in cities like Tucson, Charlotte, Dallas and Seattle (see chart below).

{kind=link}

Advantage BHM

However, the fact is that the real estate market is cyclical and returns on stocks in the sector are best gauged over the course of a few cycles. It's from this lens that I’d look at BHM, which clearly has three other factors going for it.

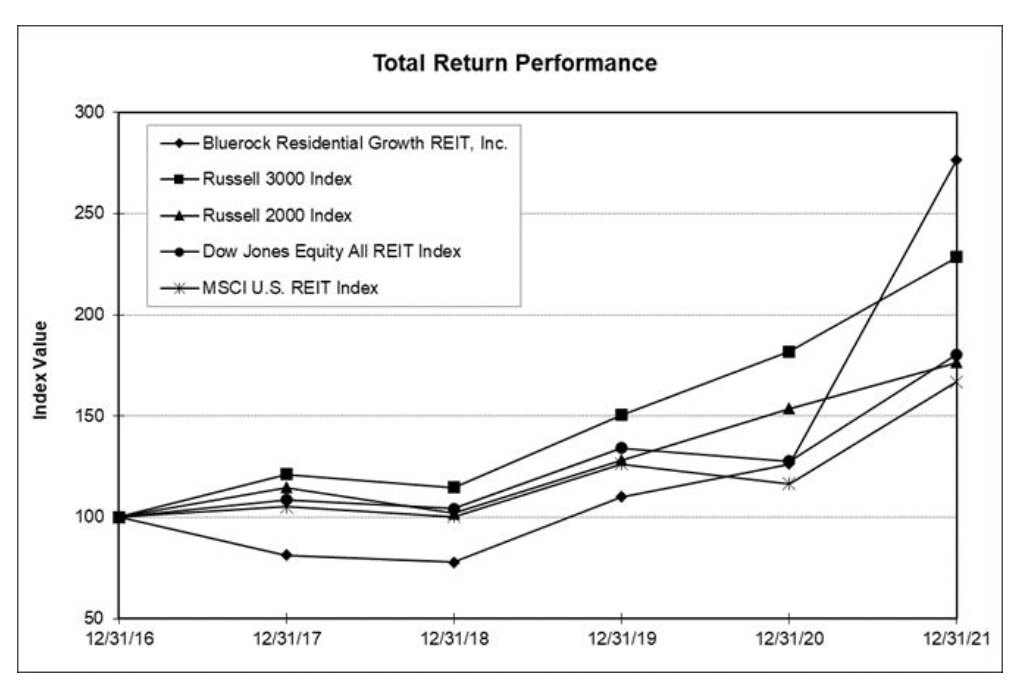

First, it comes with good credentials. The trust was a spin-off from the formerly publicly traded Bluerock Residential Growth REIT, which was acquired by Blackstone ( BX ) affiliates. The REIT did very well in the five years up to 2021, outperforming the Dow Jones Equity All REIT Index and the MSCI US REIT Index (see chart below). While it's possible that it wouldn't have sustained the rise, this chart does reflect the ability to outperform its segment.

{kind=link}

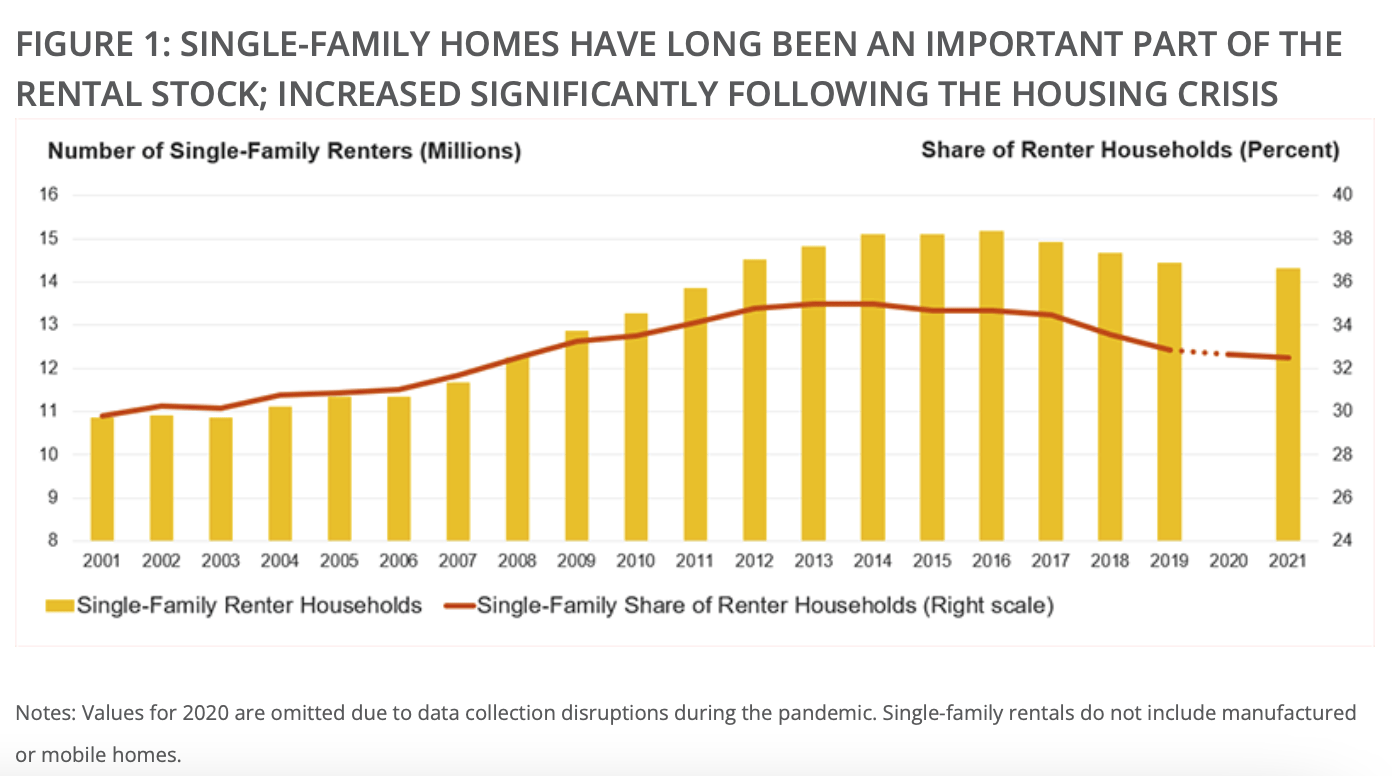

Next, according to a study by Harvard University’s Joint Center for Housing Studies, single-family rentals were a substantial proportion of 33% of total rentals as of 2021, up from a little under 30% in 2021. The absolute number of renters has risen by 3.5 million to 14.3 million renter households.

Demand for single-family units is expected to rise by another 7.5 million over the next four to five years. This in turn indicates that demand for rentals is likely to stay strong, even as supply remains restricted.

{kind=link}

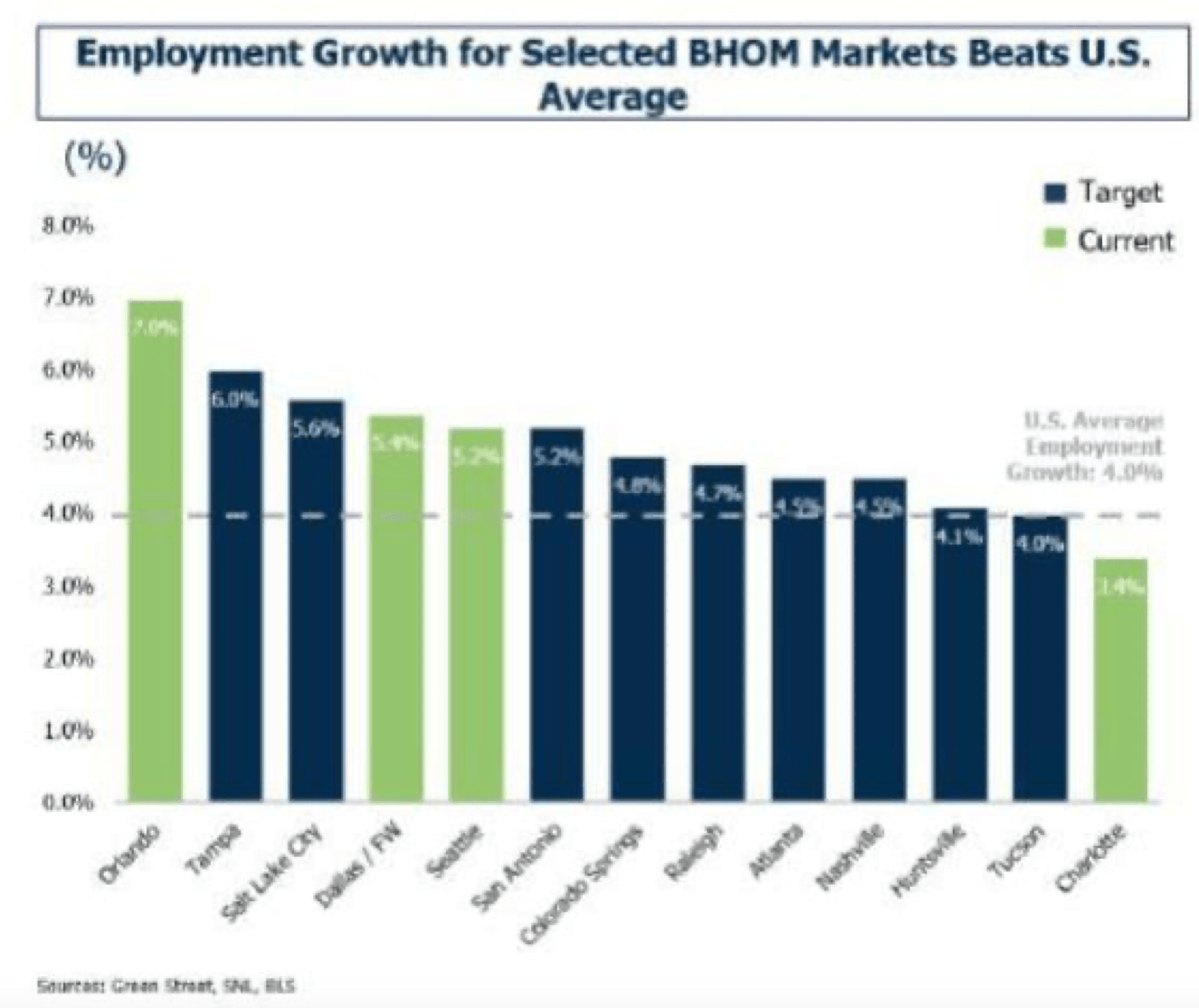

And finally, one of the company’s target areas, the Sun Belt region, is particularly well poised to benefit from this trend, with primary renters between the ages of 35-44 in the area expected to double over the next few years. There are good reasons for this of course.

Employment growth in cities like Dallas and Atlanta outstrips the average rise in employment in the US, as it does in BHM’s other target markets (see chart below). Essentially, the growing economies of these cities is expected to increase housing demand there.

{kind=link}

The financials

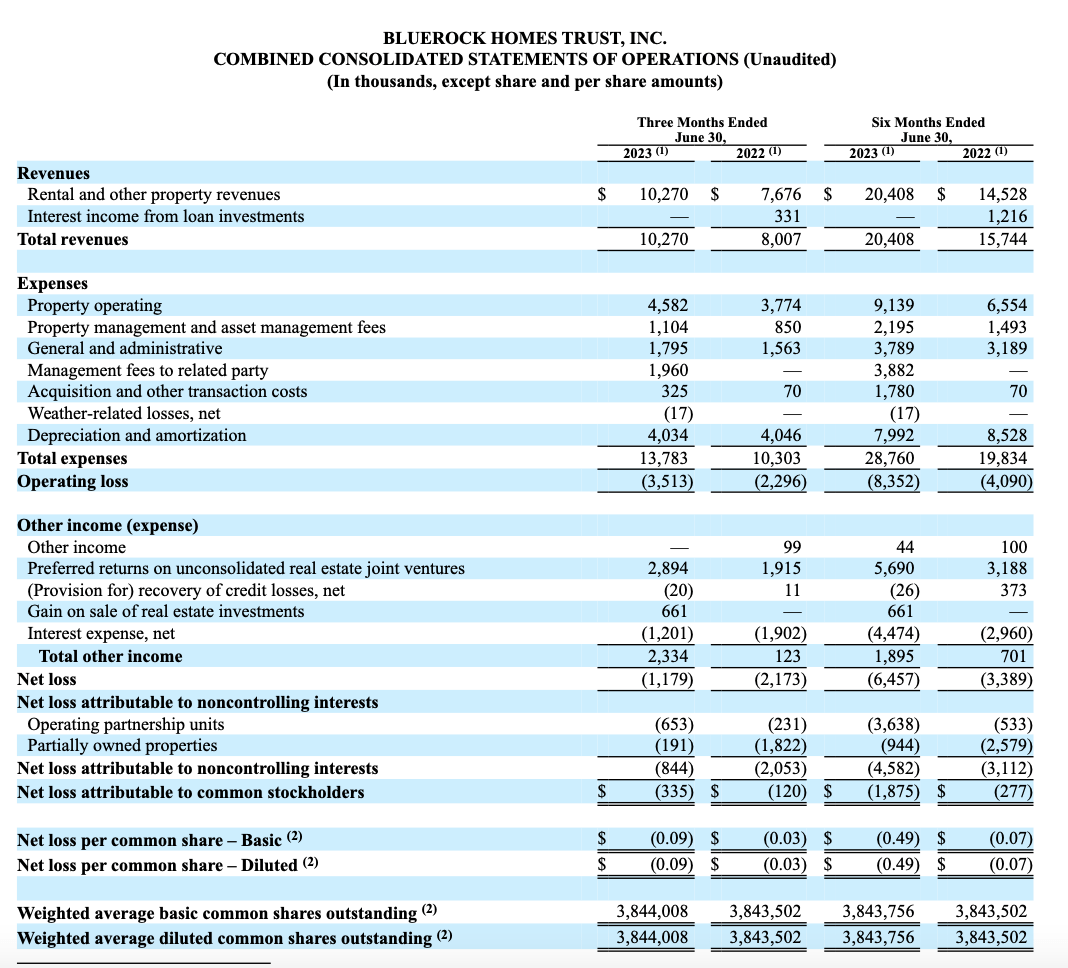

At the end of 2022, the company had a portfolio of 4,000 units across 13 states, additions to which resulted in a 21% YoY rise in total assets. The company’s revenues also grew by 133% while its operating income rose by almost 3x.

However, so far 2023 hasn’t been quite as good for the company. Even though the number of units it owns rose to 4,077 by the end of the first half of this year (H1 2023), its total assets actually corrected slightly to USD 658 million from 2022.

{kind=link}

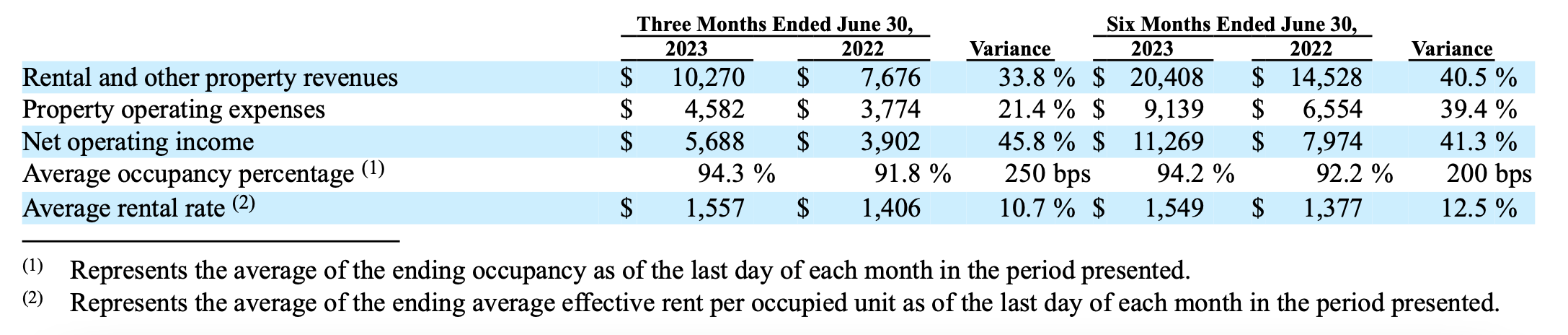

That said, the company’s revenues have still risen during this time by 30% YoY, as rental revenues rose by over 40% as both the occupancy rate and average rental rate rose (see table below). The difference between the two figures came from zero interest income on loan investments during H1 2023, compared to a 7% contribution during H1 2022.

{kind=link}

However, compared to the full year 2022, the company actually reported an operating loss in H1 2023, though it needs to be noted that it also showed a loss in H1 2022. It could be a seasonal pattern with the company, but without the benefit of longer-term data on it, we will know this only over time.

That said, the operating loss has doubled YoY, on higher property and asset management fees, but also on account of two other headwinds. The first is fees that now need to be paid as it’s externally managed. The second is transaction costs associated with property management services for over 1,000 homes. How these costs impact operating earnings in the future would be worth watching.

Market multiples

With a tangible book value per share of USD 40.50, the company’s current price levels of USD 12.60 look attractive. This also makes a favourable comparison against the biggest listed single-family rental REIT, Invitation Homes ( INVH ) and also the relatively smaller UMH Properties ( UMH ), which are both trading well above this value. Similarly, its price-to-rental revenue (P/RR) at 1.26x is also competitive with INVH at 8.3x and UMH at 4.9x.

However, the company’s price-to-funds from operations (P/FFO) ratio doesn’t look as encouraging. I calculated the trailing twelve months [TTM] number by assuming that the FFO for the full year 2022 is the same in each of the two halves of the year, which gives an FFO of USD 4.96 million for H2 2022. The company provides the number for H1 2023 at USD 0.93 million, with the difference between the two explained by the operating loss incurred during this time. This results in a TTM P/FFO of 25.3x. This figure is higher than that for INVH at 18.2x and UMH at 16.6x, which doesn’t look good.

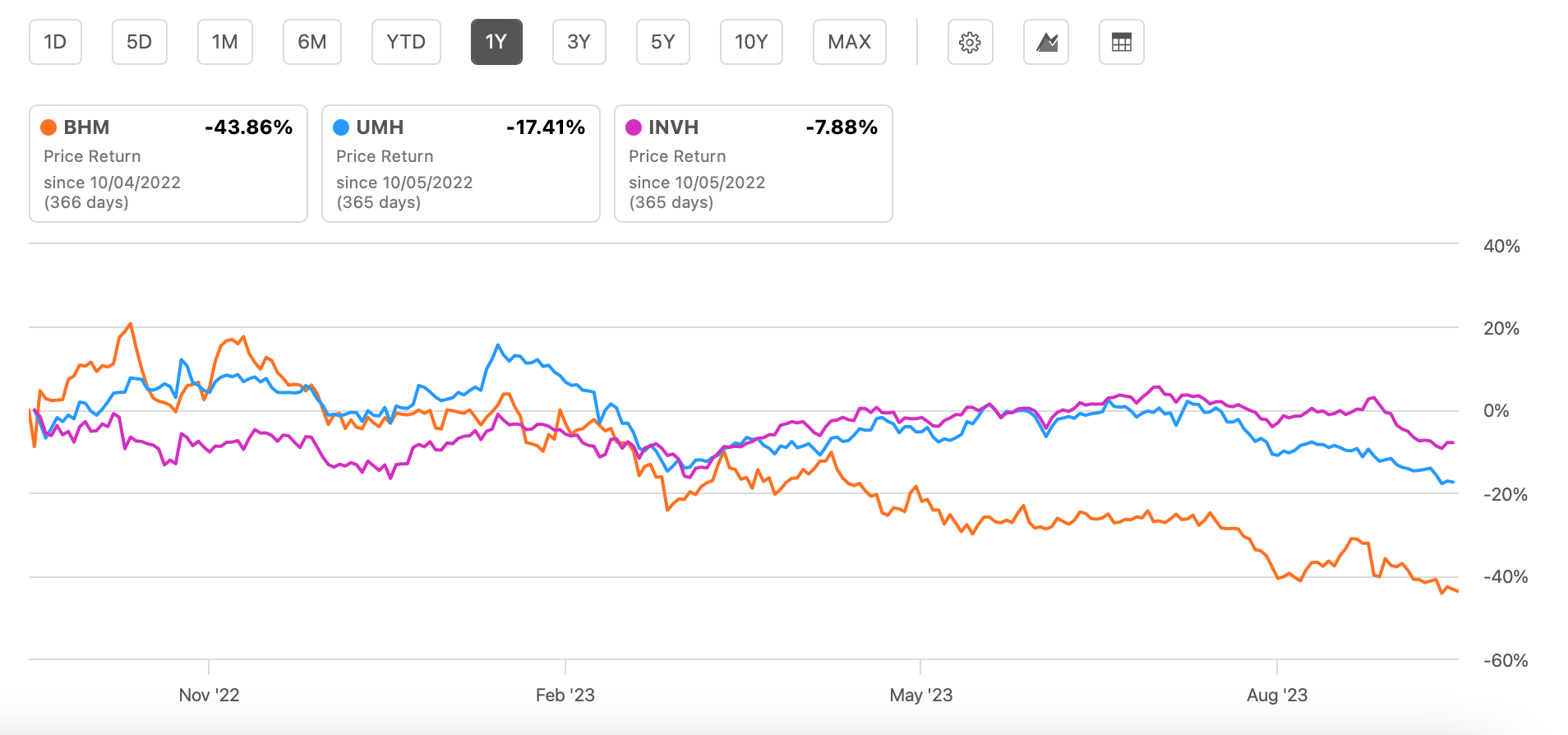

Also, as a loss-making entity, it doesn’t pay dividends while its peers do. Especially when stocks in the segment haven’t done well (see chart below), dividends can soften the blow, which puts BHM at a disadvantage.

{kind=link}

What next?

Based on the market valuations, the case for BHM is unconvincing at best, especially right now when the real estate market is sagging. This is reflected in the stock's performance and the company is no exception. Additionally, the fact that it doesn’t pay a dividend and its higher P/FFO ratio than peers also tempers the upside indicated by its tangible book value per share and low P/RR.

Its latest operating loss isn’t encouraging either after a robust 2022. How far the latest additions to costs impact the remainder of the year remains to be seen, though it is encouraging that its revenues have still seen a robust rise despite a cooling off in its target markets.

Going forward, these markets look promising, with growing employment rates that are likely to see an influx of millennial residents. The potential for the stock could become more visible over the next few years as market conditions improve on better macros. For now, though, I’m going with a Hold on BHM.

For further details see:

Bluerock Homes Trust: Softening Real Estate And Financial Losses Overshadow Advantages