BLSFF - BlueScope Steel: Strong Balance Sheet Attractive Earnings Multiple

2023-07-12 10:30:00 ET

Summary

- BlueScope Steel Limited is an Australian steel producer with substantial activities in the USA.

- A higher-than-expected steel price during the past semester has resulted in a guidance increase.

- Steel prices have softened again, so I'm not expecting FY 2024 to be better than FY 2023 at this point.

- As of the end of December, BlueScope had in excess of 10% of its market cap in net cash, while the positive working capital position exceeded A$3B.

Introduction

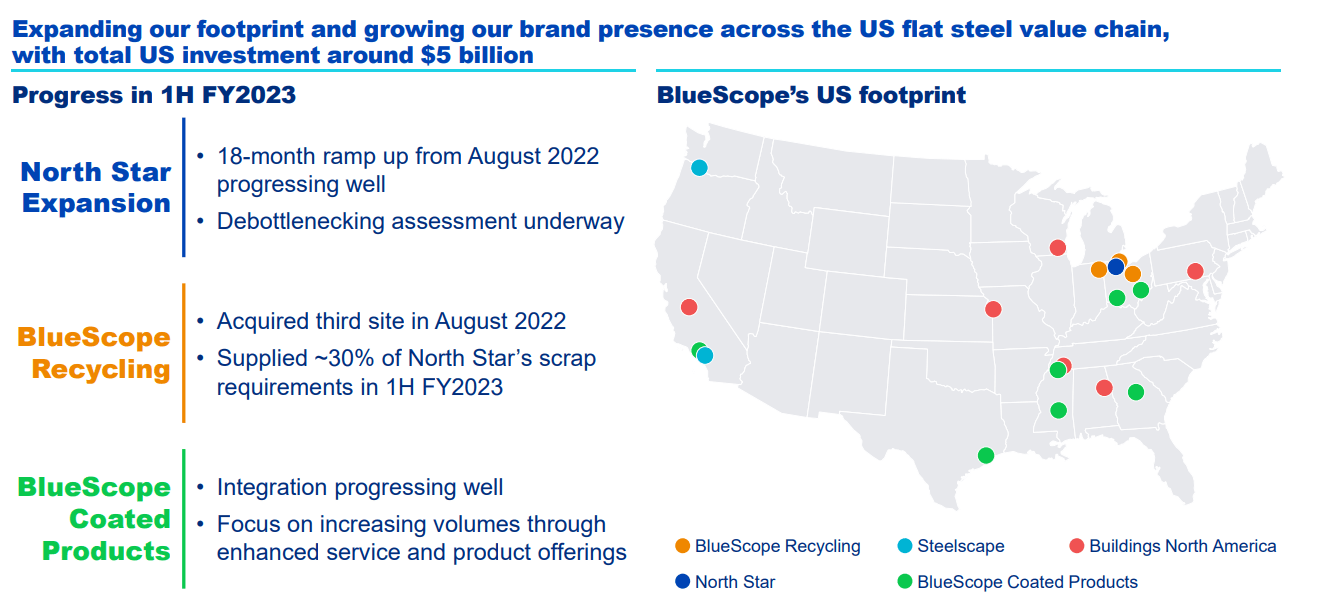

BlueScope Steel Limited ( BLSFF , BLSFY ) is a large steel producer with its main activities in Australia and the USA (where it has close to 30 production sites ). It has recently expanded its exposure to metallic coated and painted products with a recent acquisition. During FY 2022, the company also established BlueScope Recycling and Materials , which will help the company to source the scrap it uses for its steelmaking activities.

Although FY 2023 (the financial year of the company ends in June) should be worse than the previous two years due to a slowdown in the steel production sector, it looks like BlueScope may be in for a "soft" landing, as its second semester will likely come in substantially better than it had initially expected. Plenty of reasons to have another look at BlueScope Steel, which has come a very long way since my first article was published in 2015.

Seeking Alpha

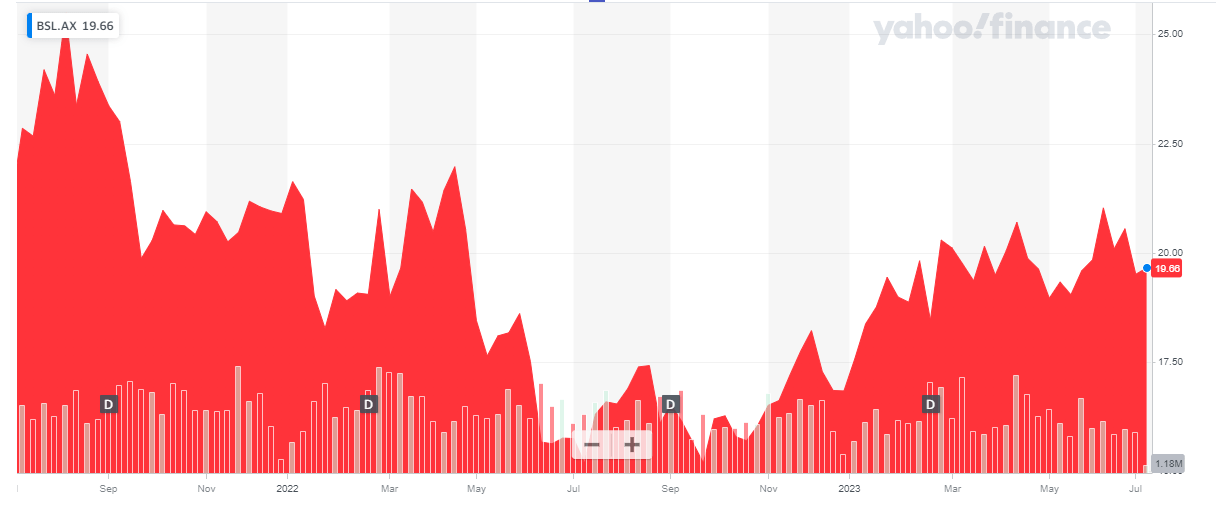

The total return since that first article in 2015 is close to 400%, which is a pretty respectable result considering the stock is trading about 20% below its peak value from 2021. That being said, conceding just 20% from that peak value is actually a sign of the relative strength of the company, as most steel producers didn't perform as well as BlueScope did.

{kind=link}

BlueScope has its primary listing on the ASX, and I would like to recommend you to use the facilities of the ASX to trade in BlueScope's shares, as the liquidity is vastly superior to any of the secondary listings. The ticker symbol in Australia is BSL and the average daily volume is close to 1.8 million shares. The current share count is 467M which results in a market capitalization of A$8.95B. I will use the Australian Dollar as the base currency throughout this article.

A strong start of the calendar year resulted in a guidance increase

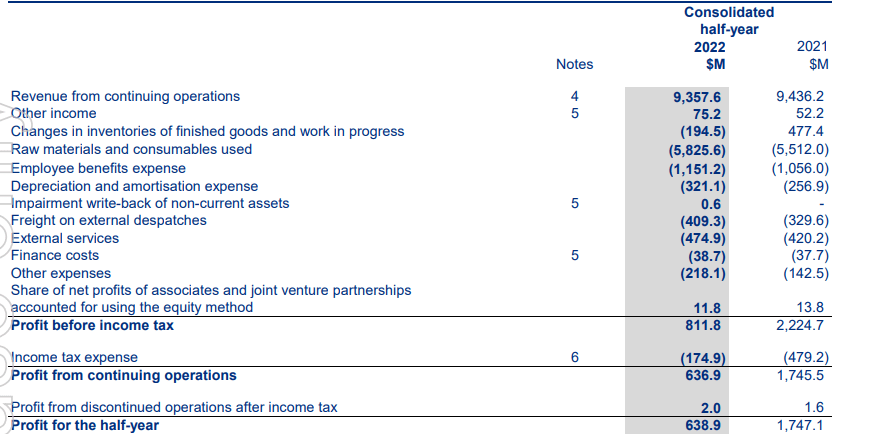

The total revenue in the first half of FY 2023 came in at A$9.36B which resulted in a decent pre-tax profit of A$812M. While that was about 60% lower than the pre-tax income generated in the first half of the preceding financial year, the difference can easily be explained by slightly lower margins in H1 2023 (due to higher input prices like labor, coal and other energy sources) while the H1 result of FY 2023 was hit by an A$195M negative inventory revaluation versus a positive revaluation of A$477M in H1 FY 2022. This alone accounted for almost half of the decrease in pre-tax income.

{kind=link}

Despite all this, the company obviously remained profitable with a net income of A$637M which worked out to A$1.28 per share.

Subsequent to releasing the H1 results, BlueScope Steel substantially increased the H2 guidance (and thus also the implied full-year guidance). In an update released at the end of April, BlueScope mentioned it is now expecting to generate a total EBIT of A$700-770M in the second half of the financial year, which is about 40% higher than the initial estimate of A$480-550M.

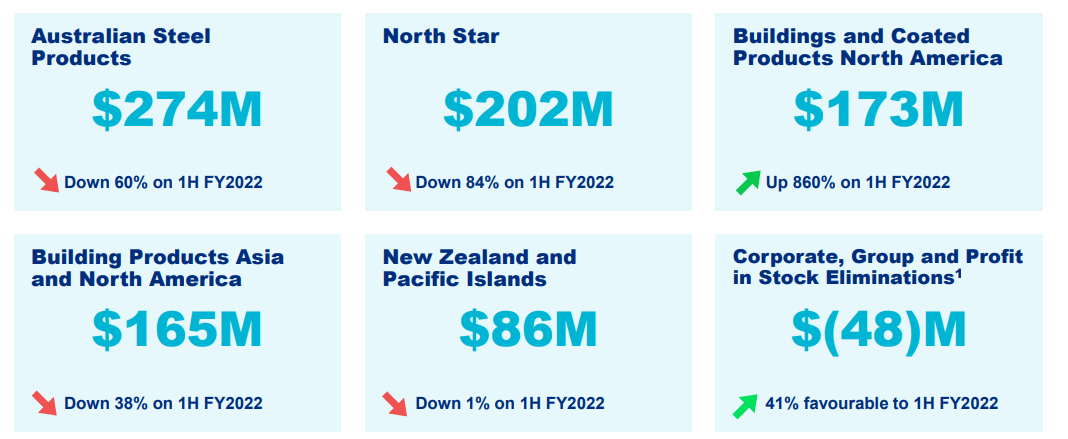

According to BlueScope, the U.S. operations (the North Star mini mill) is outperforming the initial expectations and management is now expecting a 50% better result than in the first half of the financial year (wherein it generated an A$202M EBIT) thanks to higher hot rolled coil prices and the positive impact from the expansion plans. While BlueScope Steel will only report its full-year results at the end of August, it is now clear that even if we use the lower end of the H2 guidance of A$700M, the full-year EBIT will come in at A$1.55B (with an upside potential of just over A$1.6B).

{kind=link}

One the North Star plant (where BlueScope acquired full ownership in 2015 ) will be running at full capacity, it will represent about 5% of the US flat steelmaking production capacity and as BlueScope expects a continuously increasing demand in this segment of the market, it expects the demand to continue to increase. The total ramp-up will take about 18 months and should be completed by the end of this year which will mark the completion of the 850,000 tpa expansion. Meanwhile, BlueScope is already investigating the possibility to expand the capacity yet again by 500,000 tonnes per year. About 50% of North Star's steel is sold to end-users in the automotive sector.

{kind=link}

Investment thesis

Using the updated full-year EBIT guidance of A$1.55B and knowing the finance expenses will continue to come in around A$50-80M per year, the pre-tax income will likely come in at around A$1.47B (using the higher end of the finance expenses). Applying an average effective tax rate of 22% (which is lower than the standard 30% tax rate in Australia as the company is also active in other countries with a lower average tax rate), this should result in a net income of A$1.15B or A$2.45 per share.

That makes BlueScope Steel rather cheap at its current valuation and while I understand paying 8 times earnings for a cyclical company may not sound cheap, I like the recent push to become a more vertically integrated company by acquiring other companies in the coating and recycling industry.

{kind=link}

The main question now obviously is whether or not the company can continue its strong performance in the next two years. Consensus estimates are calling for a 10-15% EBIT reduction on a YoY basis but perhaps BlueScope's next financial update in August will provide more details. Steel prices have fallen by about 20% since the April high so it is not unrealistic to expect an EBIT reduction towards A$1.3B in FY 2024, in which case the underlying EPS should come in at A$2/share. That would still make BlueScope an interesting vehicle to gain exposure to the steel price in the USA and in the Australasian markets. Meanwhile, the balance sheet seems safe with in excess of A$1.1B in net cash and a positive working capital position of A$3.43B (both are excluding lease liabilities).

I currently have no position in BlueScope Steel, but the volatility has boosted the option prices and I am considering writing a P18 for September for an option premium of A$0.50. Should the stock trade below A$18 at the expiry date, my average purchase price would be A$17.50, more than 10% lower than the current share price. And if the share price continues to trade above A$18, I can just pocket the A$0.50 option premium and write a new put option.

For further details see:

BlueScope Steel: Strong Balance Sheet, Attractive Earnings Multiple