TDG - BLW: A Nice Compromise Holding For Your Debt Allocation But Current Price Is Too High

2024-01-08 04:24:36 ET

Summary

- The BlackRock Limited Duration Income Trust specializes in providing investors with a high level of current income from low-duration securities.

- The fund has outperformed the Bloomberg Aggregate Bond Index over the past three years, delivering a gain of 13.41% compared to a loss of 10.48% for the index.

- The fund's distribution of $0.1079 per share results in a current yield of 9.23%, which is higher than some of BlackRock's other fixed-income closed-end funds.

- The fund could be a very reasonable compromise for people who doubt the rate cut narrative but still want some upside exposure if rates do decline.

- The fund is a buy if it can be obtained at a discount, however the current price is far too high to represent a good entry point.

The BlackRock Limited Duration Income Trust ( BLW ) is a closed-end fund that specializes in providing investors with a very high level of current income from the assets in their portfolios. The fund's 9.23% current yield is a testament to its success in this area, and indeed this yield is somewhat higher than some of BlackRock's other fixed-income closed-end funds. For example, consider the following:

| Fund |

| Current Yield |

| BlackRock Limited Duration Income Trust |

| 9.23% |

| BlackRock Core Bond Trust ( BHK ) |

| 8.22% |

| BlackRock Income Trust ( BKT ) |

| 8.70% |

| BlackRock Corporate High Yield Fund ( HYT ) |

| 9.77% |

| BlackRock Enhanced Government Fund ( EGF ) |

| 5.03% |

One of the reasons for this is the fund that this fund invests primarily in securities with relatively low duration. A low duration suggests that investors will end up receiving payments from the bond totaling the face value very quickly, which implies that these bonds either have very high yields or maturity dates that are fairly close to the present. For reasons that we will discuss in this article, these are better securities to hold in the current environment than long-term bonds, but they are not as good as floating-rate securities today. The fund does have a lower yield than the best floating-rate bond funds anyway, so investors who want to earn as much income as they possibly can might want to gravitate to one of those funds instead. However, as a few commenters on my other articles have pointed out, it is best to hold a combination of floating-rate and fixed-rate debt securities and this fund appears on the surface to be a good way to achieve the latter goal.

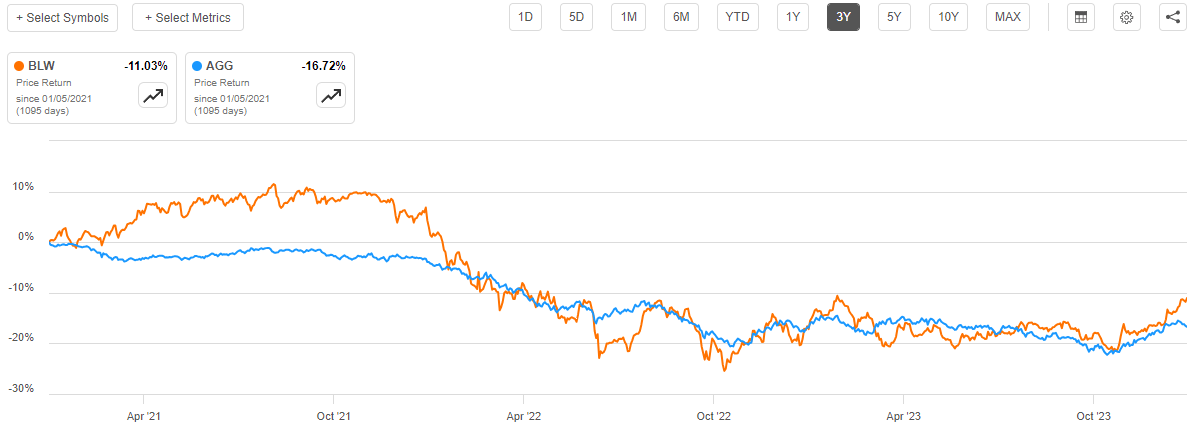

Over the past three years, the BlackRock Limited Duration Income Trust has delivered a fairly strong performance to its investors. The fund's share price is down by 11.03% over the period, which is much better than the 16.72% decline of the Bloomberg Aggregate Bond Index ( AGG ):

{kind=link}

This is actually what we would expect to see from a fund that invests in limited-duration debt. The big advantage of these securities is that they do not decline nearly as much as long-term bonds when interest rates rise. As interest rates have generally increased over the trailing three-year period, we would expect that this fund should be able to outperform more traditional long-term debt. Curiously though, we do see that there were a few periods during which the fund's shares appeared to be just as affected by interest rate movements as the index. This might be due to the fund's use of leverage, as low-duration securities should be more stable than the bond market overall in the face of changes in interest rates.

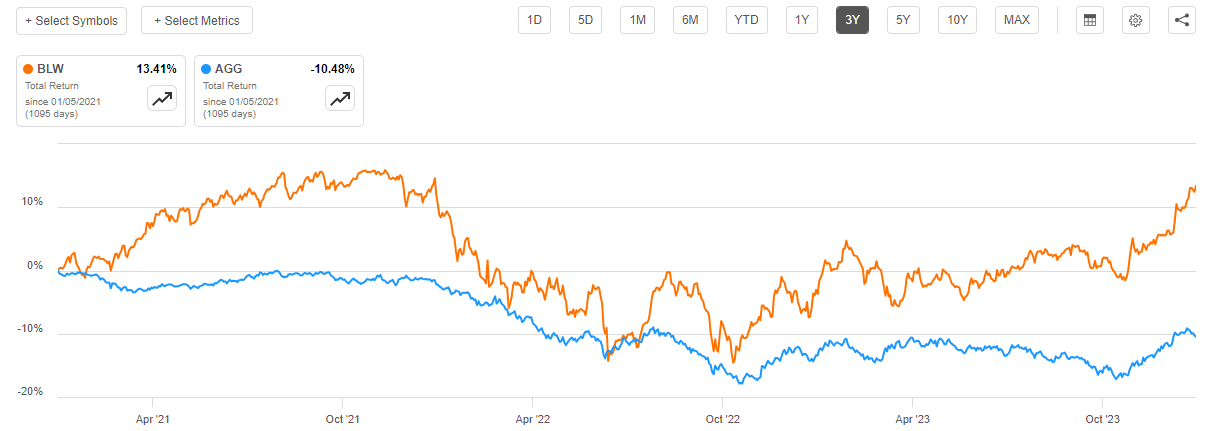

As I have pointed out in numerous previous articles though, a cursory look at the fund's share price performance does not really provide an accurate picture of what investors in the fund actually received. This is because bonds deliver a significant portion of their investment return in the form of direct payments to their holders. The BlackRock Limited Duration Income Trust, as with all closed-end funds, pays out all its investment profits to the shareholders and aims to keep its portfolio value relatively stable over the long term. As such, we need to incorporate the distribution into our analysis to determine the return that investors actually received. When we do this, we see that investors in the BlackRock Limited Duration Income Trust received a 13.41% gain over the past three years, which was a substantial improvement over the 10.48% loss suffered by investors in the Bloomberg Aggregate Bond Index over the same period:

{kind=link}

This seems almost certain to appeal to income-focused investors. After all, with this fund, investors not only receive a very high yield but also beat the broader bond market over time.

However, past performance is no guarantee of future results so we still want to investigate the fund further in order to determine if it could be a good investment today. Let us do that.

About The Fund

According to the fund's website , the BlackRock Limited Duration Income Trust has the primary objective of providing its investors with a high level of current income and capital appreciation. The current income part of this objective makes sense considering the fund's overall strategy, but the capital appreciation aspect is not so sensible. Here is how the website describes the fund's strategy:

BlackRock Limited Duration Income Trust's investment objective is to provide current income and capital appreciation. The Fund seeks to achieve its investment objective by investing primarily in three distinct asset classes:

- intermediate duration, investment-grade corporate bonds, mortgage-related securities, asset-backed securities, and US Government and agency securities;

- senior secured floating-rate loans made to corporate and other entities;

- US dollar-denominated securities of US and non-US issuers rated below investment grade, and, to a limited extent, non-US dollar denominated securities of non-US issuers rated below investment grade.

The fund's portfolio normally has an average duration of less than five years (including the effect of anticipated leverage), although it may be longer from time to time depending on market conditions. The Fund may invest directly in such derivatives or synthetically through the use of derivatives.

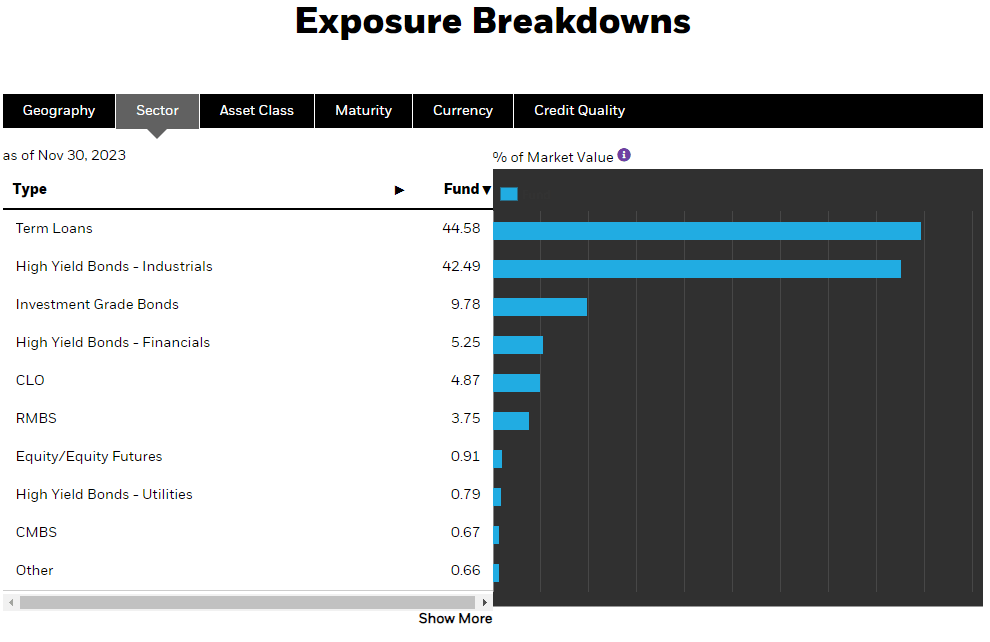

Thus, this is a debt fund that invests in a fairly wide variety of debt, or so it claims. In fact, right now the fund's portfolio is fairly balanced between floating-rate securities and high-yielding corporate bonds (colloquially called "junk bonds"):

{kind=link}

As we can clearly see here, 44.58% of the fund is invested in floating-rate term loans and 42.49% of the portfolio is invested in junk bonds that are issued by non-financial corporate entities. The remaining things in this portfolio have much smaller weights, but we can still see a combination of both floating-rate securities and fixed-rate junk bonds. That is one reason why the fund is able to achieve its goal of limiting its duration risk. Junk bonds tend to have fairly low duration because their high yields result in the investor receiving payments totaling the face value of the bond much more rapidly than investment-grade bonds. Floating-rate securities have essentially no duration risk because of their reset feature. Essentially, the duration of these securities is set to zero on the date that the coupon payment gets readjusted to the market interest rate plus a spread. This is one reason why floating-rate securities are typically completely unaffected by interest rate changes. We have discussed the inherent protection that floating-rate securities offer investors against interest rate risk in numerous previous articles. The fact then that roughly half of the fund (the term loans plus the collateralized loan obligations) is invested in floating-rate securities should thus make the fund's portfolio much less volatile in the face of changing interest rates than a pure fixed-rate bond fund would be.

The fact that the BlackRock Limited Duration Income Trust only invests in debt securities is what makes the fund's objective of capital appreciation very difficult to achieve on any sort of long-term basis. This is because debt securities do not deliver net capital gains over their lifetimes. An investor purchases a bond at face value and receives the face value back at maturity. Thus, there are no net capital gains because there is no connection to the growth and prosperity of the issuing company. While bonds do change price when interest rates change and it is possible to profit from those changes by trading bonds, these are not really the same thing as common stocks deliver. After all, interest rates cannot go below zero so there is a limit to how high bond prices can actually go. Thus, all the fund can really deliver to the investors is income from the bond's coupons and possibly some trading profits. However, those trading profits may be hard to come by from the floating-rate securities in the portfolio, which account for roughly half of the portfolio. That somewhat limits the potential trading profits here compared to a fund that only invests in fixed-rate securities, so most of what the investors will be receiving will be current income generated by the securities. The difference here is admittedly somewhat academic because money is fungible, but it is important not to be misled by the fund's investment objective.

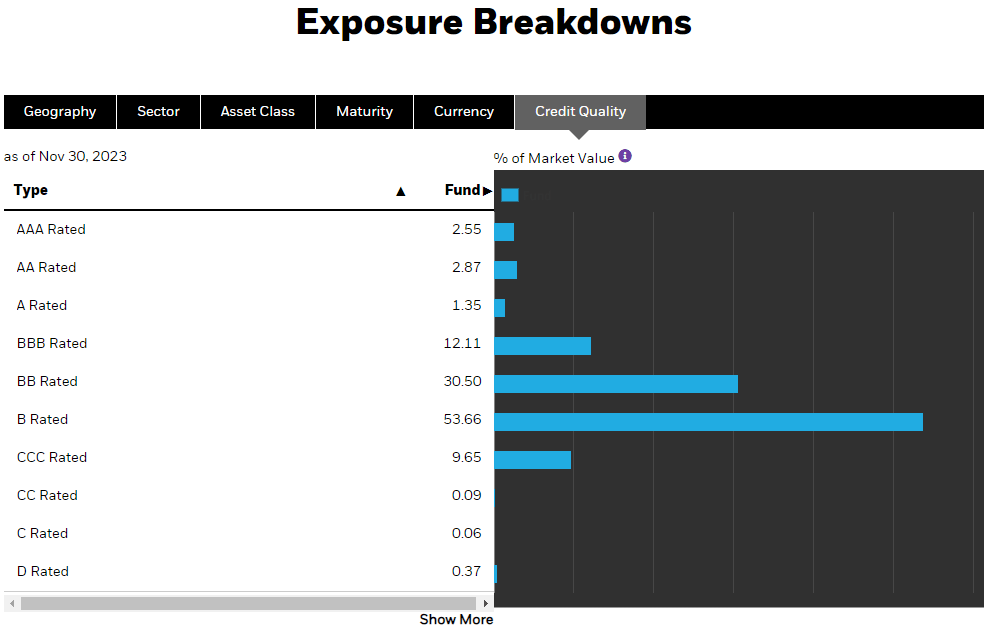

One thing that eagle-eyed readers might note in the description of this fund's strategy is that it specifically states that this fund will be investing in below-investment-grade securities. We saw this earlier with the fund's positions in both high-yield industrial issues and high-yield financial issues. This is something that might concern risk-averse investors, which includes a number of investors who are primarily interested in the generation of income from their portfolios. Fortunately, we might be able to derive a little comfort by looking at the credit ratings that have been assigned to the securities in the fund. Here is a brief summary:

{kind=link}

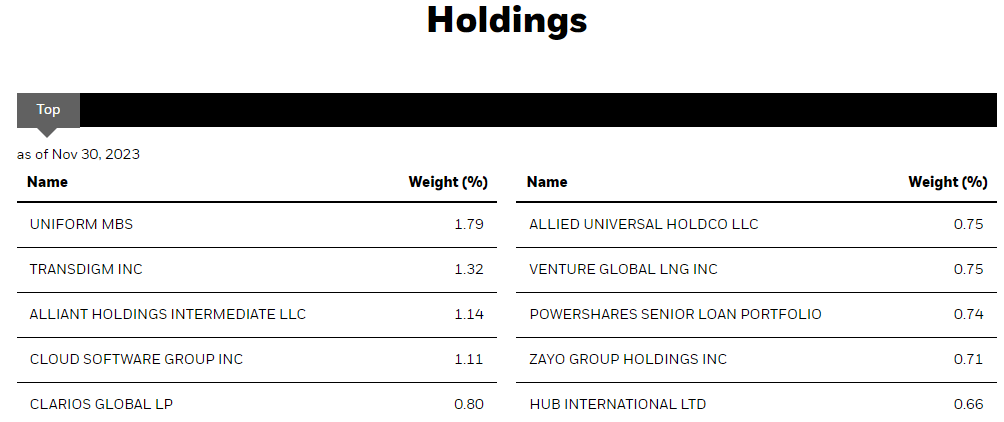

An investment-grade security is anything that is rated BBB or higher by the major rating agencies. As we can see above, these securities account for 18.88% of the fund's assets. That is obviously a minority of the portfolio, so the overwhelming majority of the fund's assets are invested in junk debt. We can see though that 84.16% of the fund's assets are invested in either BB-rated or B-rated debt. These are the two highest possible ratings for junk debt, and the official bond ratings scale states that these ratings are only issued to entities that do have the capacity to carry their current debt load even if the economy suffers from a short-term shock. While BB-rated and B-rated entities do not have balance sheets that are as strong as investment-grade issuers, they are also not companies that we need to lose sleep worrying about if they are included in our portfolios. This is especially true when we consider that this fund is not heavily exposed to the debt of any single issuer. As we can see here, the largest single issuer in the fund only represents 1.32% of its assets:

{kind=link}

The Uniform MBS which accounts for 1.79% of the fund does not count as the largest issuer that is represented in the fund. This thing is a mortgage-backed security that is backed by mortgages issued to dozens, if not hundreds, of entities. Thus, there is not a single debtor who is ultimately responsible for making the payments to the bondholders. The largest single debtor whose securities are in the portfolio is TransDigm ( TDG ) and that company only accounts for 1.32% of the fund's total assets. TransDigm is an aerospace manufacturer that we frequently see represented in BlackRock's closed-end funds. The company's common stock rates reasonably well both among Seeking Alpha's contributors and Wall Street analysts:

Seeking Alpha

It seems unlikely that we need to worry about the company's bonds if its stock is a reasonable investment. I might be worried about the company if everybody was screaming that the shares should be sold, but this is not what we see here. As such, we probably do not need to worry about the company's presence in the portfolio. At 1.32% of the fund's total holdings, it does not represent a large enough presence to have any real impact on the fund's overall performance anyway. The same goes for everything else in the fund. In short, we should not need to worry about issuer-specific risks here.

The fund specifically states that it invests in securities that have a lower duration than the bond market as a whole. The fund has an effective duration of 3.22 years compared to 6.15 years of the Bloomberg U.S. Aggregate Bond Index, so this is certainly true. Duration is a measure of how sensitive a bond's price is to changes in interest rates, with lower duration figures indicating lower sensitivity. Thus, the securities in this fund should be less affected by interest rate movements than the broader market index. That is something that could be very important right now.

In a recent article , I made the case that investors should take advantage of the recent strength in bonds and take profits because the Federal Reserve is unlikely to reduce interest rates to anywhere near the degree that the market expects. The market is currently pricing five to six 25-basis point cuts to the federal funds rate in 2024 and the economy is far too strong to justify that, at least if you believe the official numbers. That level of interest rate cuts would require a severe recession to hit the economy within the next thirty days. It seems highly unlikely that such an economic shock will occur, and as long as the economy remains resilient, the central bank will need to keep rates high in order to avoid a reignition of inflation. Thus, bonds are overpriced right now and are due for a correction when the Federal Reserve fails to deliver on a rate cut in March, as the market currently expects.

The BlackRock Limited Duration Income Trust should hold its value more than most fixed-income funds in such a correction due to two reasons. The first of these is that roughly half of the fund is invested in floating-rate securities that will be relatively immune to such a correction. The second reason is that the fund's lower-than-average duration should cause the fixed-rate securities to hold their value much better than bonds with a higher duration. With that said, I do still expect that this fund will see its share price and net asset value decline if the Federal Reserve disappoints the market but not nearly as much as many other bond funds or the index.

The fund does still have some upside exposure to falling interest rates that a floating-rate fund lacks. This is due to the fixed-rate bonds in the portfolio. These probably will not appreciate as much as the Bloomberg U.S. Aggregate Bond Index in the event of declining long-term interest rates, but the fund should outperform a floating-rate fund in the event that the Federal Reserve does slash interest rates significantly for some reason. As such, this fund could work as something of a nice compromise for risk-averse investors.

Leverage

As is the case with most closed-end funds, the BlackRock Limited Duration Income Trust employs leverage as a method of boosting the effective yield of its portfolio beyond that of any of the underlying assets. I explained how this works in a number of previous articles. To paraphrase:

In short, the fund borrows money and then uses that borrowed money to purchase floating-rate loans, high-yield bonds, and other income-producing debt securities. As long as the yield that the fund receives from the purchased assets is higher than the interest rate that it needs to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. This fund is capable of borrowing money at institutional rates, which are considerably higher than retail rates, so this will usually be the case. It is important to note that the use of leverage is less effective today with borrowing rates at 6% than it was a few years ago when interest rates were essentially negative.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and leverage. This is one reason why the fund's share price and net asset value seems to be somewhat more volatile than we would expect given the nature of its assets. As such, we want to ensure that the fund is not using too much leverage because that would expose us to an excessive amount of risk. I generally prefer a fund's leverage to be under a third as a percentage of its assets for this reason.

As of the time of writing, the BlackRock Limited Duration Income Trust has leveraged assets comprising 32.37% of its portfolio. This is a bit lower than the leverage that is employed by some other debt-focused closed-end funds, which is rather nice to see as it should mean that this fund will be somewhat less volatile than some other debt funds. That should prove to be reasonably appealing to risk-averse investors.

The fund's current leverage is also well below our one-third preference, which is also nice to see. Overall, this fund's use of debt should represent a reasonable balance between the risk and the reward. There is probably not too much for us to worry about here with respect to the fund's leverage.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the BlackRock Limited Duration Income Trust is to provide its investors with a very high level of current income and capital appreciation. However, since the fund invests primarily in bonds and other debt securities, the majority of its total returns will be in the form of coupon payments coming into the fund. The fund receives these payments, and since the majority of the holdings are below-investment-grade bonds, the coupon payments can be quite large as a percentage of the bond's face value. This fund takes things a step further and borrows money to allow it to control more bonds than it could solely with its equity capital, which has the effect of boosting the fund's effective yield. The fund pools all of the payments that it receives from the bonds in the portfolio and combines the payments with any profits that it manages to earn by selling bonds that experience price appreciation due to interest rate movements. The fund then pays out all of this money to its shareholders, net of its expenses. We might expect that this would result in the fund's shares having a very high yield.

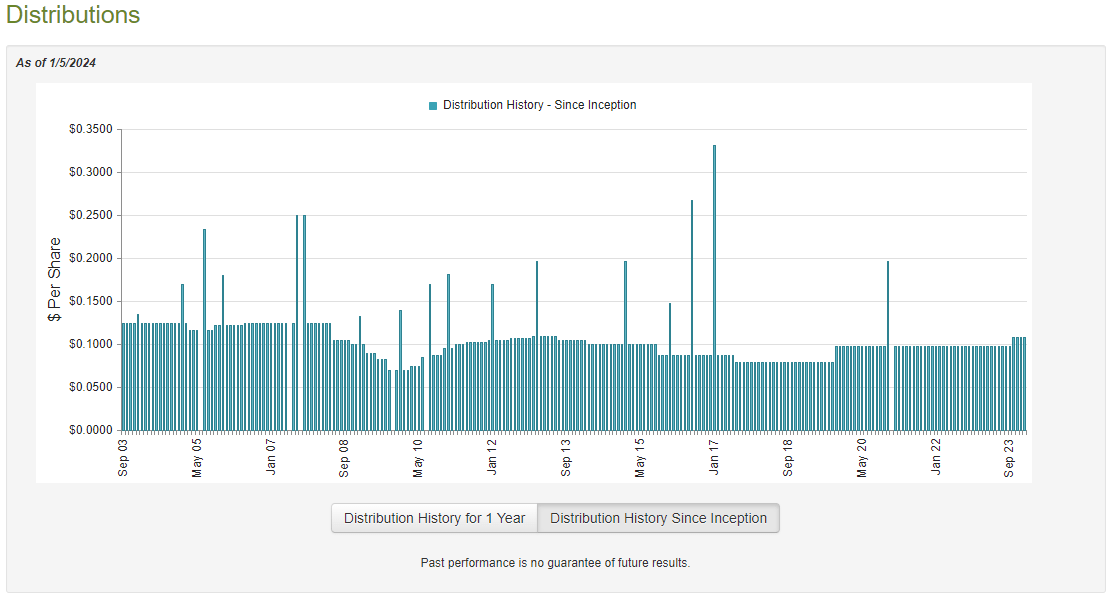

This is indeed the case, as the BlackRock Limited Duration Income Trust pays a monthly distribution of $0.1079 per share ($1.2948 per share annually), which gives it a 9.23% yield at the current price. As mentioned in the introduction, this compares favorably to BlackRock's other bond funds, and it is also reasonable considering the yield that we can obtain from similar funds offered by other fund houses. Unfortunately, the fund's distribution has not been especially consistent over the years. As we can see here, the fund has both raised and cut its distribution numerous times over its history:

{kind=link}

This history might prove to be something of a turn-off for investors who are looking for a secure and consistent source of income that they can use to pay their bills or finance their lifestyles. However, it is quite understandable that the fund would be forced to change its distribution frequently. After all, this fund is dependent on the income that it can receive from the debt securities that are in its portfolio and that depends on bond yields and interest rates. Thus, the bond's distribution will somewhat depend on interest rates, which we saw last year when the fund raised its distribution in October. Nearly every fund that invests in floating-rate securities raised its distribution at least once in the past year or so and this one is clearly no exception. That might improve the fund's appeal, especially considering how many fixed-income funds reduced their payout in response to the shift in the monetary environment back in 2022.

As is always the case, we want to ensure that the fund is able to sustain its distribution without destroying its net asset value. After all, no fund can sustain a destructive distribution over an extended period. This is because the required return needed to break even will keep increasing until it becomes impossible to realistically achieve. Let us have a look at the fund's finances to see how well it is covering the payout.

Unfortunately, we do not have an especially recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the six-month period that ended on June 30, 2023. As such, it will not include any information about the fund's performance over the past six months. This is rather disappointing because there were a few events that occurred over the period that could have had an impact on the fund's portfolio. In particular, long-term interest rates rose precipitously over the summer of 2023, which could have had a negative impact on the value of the fixed-rate securities in the fund's portfolio. This trend reversed around the middle of October and from that time until the end of the year bond prices were rising. This report will not provide any information about how the fund handled either of these events, which is disappointing. We will have to wait for the annual report to get that information, but that report will probably not be released for a month or two. As such, we have to go with what we have to try and determine how strong the coverage of the distribution is.

During the six-month period, the BlackRock Limited Duration Income Trust received $458,690 in dividends and $26,593,166 in interest from the assets in its portfolio. When we combine this with a small amount of income that the fund received from other sources, we get a total investment income of $27,287,766 during the period. The fund paid its expenses out of this amount, which left it with $18,959,550 available for the shareholders. That was, unfortunately, not nearly enough to cover the $21,019,644 that the fund paid out in distributions during the period. At first glance, this is likely to be concerning since we typically would prefer to see a debt fund pay its distributions entirely out of the net investment income. This fund clearly failed to accomplish that task over the period.

However, the fund does have other methods through which it can obtain the money that it needs to finance the distribution. For example, it might have been able to exploit changes in bond prices to earn some capital gains that could be distributed to the shareholders. Realized capital gains are not considered to be investment income, but obviously they do result in the fund making some money. The fund had mixed results at accomplishing this task during the period. It reported net realized losses of $14,895,803 but this was offset by $21,545,555 net unrealized gains during the period. Overall, the fund's net asset value increased by $4,589,658 after accounting for all inflows and outflows during the first half of 2023. Thus, the fund did technically manage to cover its distributions, but it had to rely on unrealized gains to do so.

As everyone reading this is no doubt well aware, unrealized gains can be erased during a market correction. As such, we should not really rely on them as a method of covering distributions. Fortunately, the fund seems to be okay right now. As we can see here, its net asset value per share increased by 2.56% since July 1, 2023:

{kind=link}

This suggests that the fund managed to fully cover all of the distributions that it has paid out since the most recent report was released. It also had a bit of money left over, so we can conclude that the distribution appears to be sustainable for the time being.

Valuation

As of January 4, 2023, the BlackRock Limited Duration Income Trust has a net asset value of $14.00 per share. However, the shares currently trade for $14.03 each. That gives the fund a 0.21% premium on net asset value at the current price. This is a much worse price than the 0.92% discount that the fund has had on average over the past month. As such, the current price looks to be too high, especially considering the risk that the Federal Reserve will disappoint the market and cause the fund's shares to fall.

Conclusion

In conclusion, the BlackRock Limited Duration Income Trust is a good compromise holding for investors who doubt the narrative about five or six interest rate cuts this year but still want some upside exposure from fixed-rate securities. In fact, if the fund had a reasonable discount, I would have given it a weak buy rating for that reason. However, the current price is far too expensive given the risks here. For the most part, this fund does look very good except for that premium. It is worth watching though and buying if it starts trading at a discount following a correction. For now, though, it is too risky to buy at the current price.

For further details see:

BLW: A Nice Compromise Holding For Your Debt Allocation, But Current Price Is Too High