BMTX - BM Technologies: Deep Value Turnaround

2023-09-20 08:25:44 ET

Summary

- BM Technologies is a fintech company that facilitates deposits and banking services between customers and partner banks.

- BMTX has immediate catalysts that will drive earnings power.

- Cash and other assets provide an excellent margin of safety.

- Stock trades at <1x normalized free cash flow.

Summary

Due to the lack of coverage and short trading history, I want to start off with a brief summary of BM Technologies (BMTX).

BMTX is a fintech company that facilitates deposits and banking services between customers and partner banks. There are 2 main segments of BMTX's business, higher education & BaaS (Banking as a Service). In the higher education segment, BMTX is the infrastructure powering college-branded bank accounts & student aid disbursement. ~70% of all college-branded bank accounts and debit cards are supported by BMTX; the partner bank holding custody of the deposits will be First Carolina Bank "FCB" following completion of the deposit transfer - expected within the next 3 months. In the BaaS segment, BMTX, with partner bank Customers Bank (CUBI), facilitates the banking platform for T-Mobile (TMUS) (T-Mobile Money).

BMTX makes money through deposit servicing fees (paid by partner banks), interchange fees on debit spend (typically paid by card networks), account fees, university subscription fees, and other ancillary fees. Between both segments, BMTX serviced ~$1B in average deposits as of Q2 and facilitated $2.8B in debit transactions in the last twelve months.

Thesis

There are 5 main points that are key drivers for BMTX's earnings power:

- FCB Post-Transfer Economics: Immediate upside to earnings power lies within the new FCB deposit service agreement. Effective upon transfer completion (expected to fully transfer before EOY 2023 - high confidence from management) deposit service fee take rate will increase from ~3% to ~4.5% on higher ed deposits due to variable rate servicing fee structure (CUBI also switched to variable rate structure resulting in servicing take rates increasing from ~3% to ~4.75%). Also, because of FCB's Durbin Exemption status (non-regulated), their net interchange take rate on debit transactions will increase from ~45 bps to ~85 bps. I expect these changes to add an incremental $9mm in EBITDA alone.

- Deposit Base Stabilizing: A very real risk to BMTX's business has been the depletion of deposits since the beginning of 2022. This decline is driven by stimulus checks from COVID creating an unrealistic deposit base & rate-sensitive deposits leaving as the Fed hiked rates. According to management, they believe BaaS accounts are finally stabilizing and reaching a point of normalization (higher ed accounts are mostly unaffected). As deposits find a floor, cash flow will also stabilize.

- Cheap CAC at Universities: A stabilizing deposit base coupled with strong higher ed growth (signing up >100,000 new accounts a quarter) is massively accretive to BMTX's earnings power. Tapping into student bodies at the colleges they currently serve is the cheapest way to grow deposits. With current student usage rates = 10 - 15% the opportunity is huge

- Massive Operating Leverage: After discussing with management, it is clear that their largest cost line item (Tech, Comm, Processing) is highly fixed in nature with the variability controlled by the company. With most of the expense going towards devs for new tech developments, as the business matures this line item will fall drastically as a % of revenue, producing massive operating leverage. In the near term, BMTX's profit enhancement plan "PEP" is expected to save $18mm in annualized costs (net of CAPEX) which management expects to be fully realized on a run rate basis in early 2024.

- New BaaS Partnerships: T-Mobile doesn't just provide contractual earnings for the next 2 years but also an anchor to bring on new BaaS partnerships. If BMTX can partner with another well-known brand for marketing flex to build a fresh deposit base, there will be immediate earnings and margin upside while removing uncertainty overhang. After talking with management, it is also very clear the T-Mobile partnership is very highly regarded removing a lot of post-contract termination risk.

Risks

While BMTX is not a depository institution, its performance is directly influenced by the banking sector which may be adversely affected by macro conditions and regulation changes. I have identified 4 key risks to an investment in BMTX:

- Macro

- (Core Business): Core business has been drastically affected by the rising interest rate environment as high-dollar deposits at T-Mobile have fled with haste. While a good portion of the deposit base is normalizing following excess stimulus, inflation has also eaten at debit spend (as credit card usage increases) hurting BMTX's interchange revenue.

- Macro (Stock Price): The stock price has been beaten down because it is grouped with broad SPAC and fintech drawdowns.

- Trading Mechanics: ADV = $30-40k/day meaning institutions cannot trade this stock without significant slippage. Because of this, it may take notable time for the market to realize this opportunity exists (why I deem it a risk). A mitigant is the CFO told me directly, alongside IR, that they want to get on the road and promote the story to potential shareholders.

- Bank Transfer: While management is extremely confident the transfer of higher ed deposits from CUBI to FCB will be completed by EOY, there's a chance this process is stalled or canceled, resulting in worse economics and further cash burn.

- Regulatory: Regulations in higher ed banking & Durbin Exemptions could pose risks to future earnings. While management has reiterated they are not concerned with regulatory changes, I have forecasted a substantial fall in account fees & other revenue to account for future risk potential. I highly doubt Durbin Exempt interchange fees for small banks will change due to the potential for negative sector-wide economic impact. Management is also keenly focused on compliance & regulations.

Financial Highlights

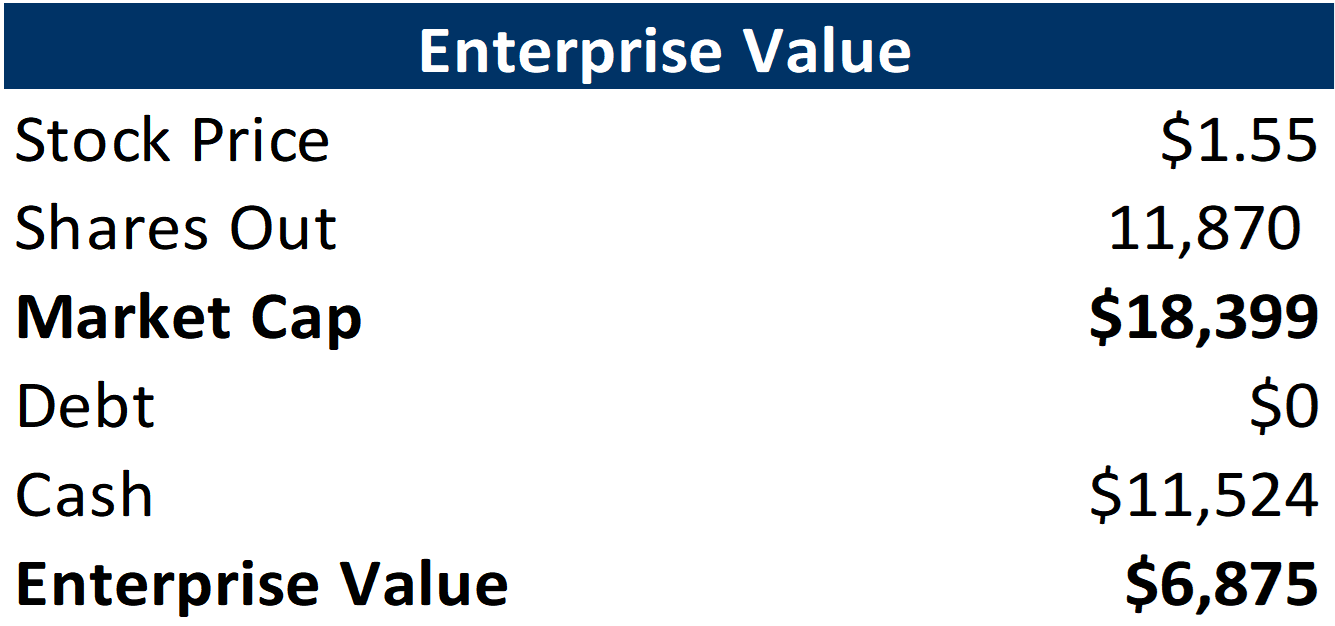

Enterprise Value

{kind=link}

Model Highlights

{kind=link}

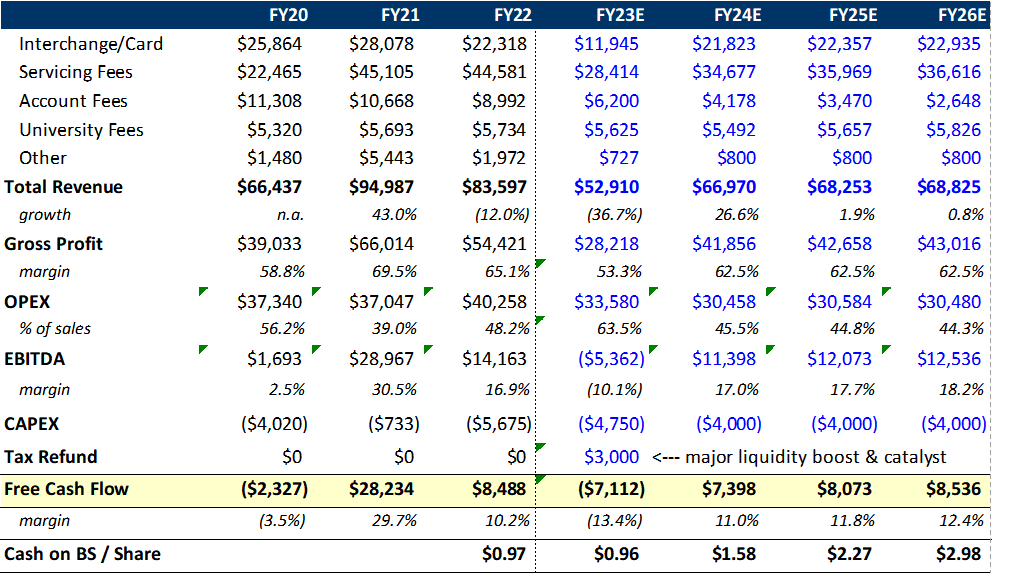

Model Assumptions: FCB transfer complete mid-Q4 '23, $18mm in PEP savings (excluding non-cash) by '24, <3% annual growth in deposits and debit spend, $4mm CAPEX (management forecasting $3mm), +$3mm cash in Q3 '23 for a tax receivable (management forecasting $4.5mm will convert to cash), management forecasting positive 2H '23 Core EBITDA.

Valuation

Absolute

Absolute Basis: On a normalized basis - assuming deposits have stabilized, the FCB transfer is successful, and PEP is complete by 2024: '24E Free Cash Flow = $7.4mm, current EV = $6.9mm, normalized EV/FCF = 0.93x (108% earnings yield)

Relative

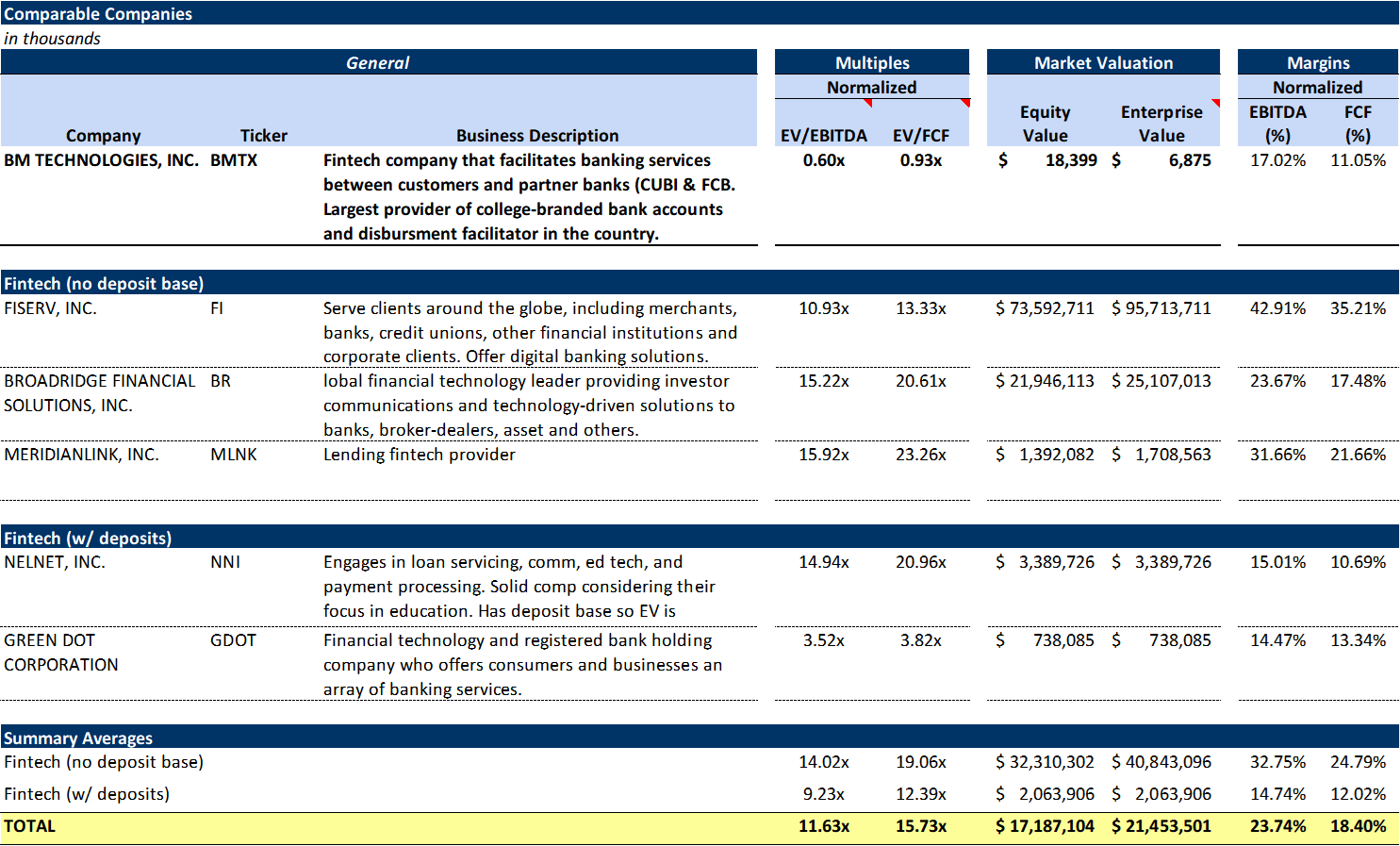

Due to the limited trading history, I focused on the closest comparable companies I could find to show relative valuation. Note there are no true, perfect public comps for this business.

{kind=link}

Disclaimer: EV = Market Capitalization for fintech companies with deposits. Earnings for fintech companies without deposits were normalized using historical growth to calculate 2024E earnings. For depository institutions, I used FY22 earnings.

Margin of Safety

I have identified 3 powerful sources of downside protection providing an attractive margin of safety for a potential investment in BMTX.

- Cash: While the valuation (above) provides security, the true margin of safety in this business is cash on the balance sheet. Currently, there is $0.97/share of cash in the business (total cash / shares outstanding). I believe the low will be $0.96 (due to operating burn associated with actively transferring funds to FCB & tech development CAPEX, positively aided by the expected $3mm tax refund expected to hit in Q3 '23) and will reach $1.58 by EOY 2024 from improved economics post-FCB transfer. With the current share price at ~$1.55, this cash provides significant downside protection. When stress-testing the business, 2024E EBITDA remains positive if the T-Mobile partnership ceases and if the FCB transition cancels. (if T-Mobile ceases the partnership and the FCB transition cancels simultaneously, EBITDA would be negative).

- Assets: Outside of cash, BMTX has 2 very real assets that would provide further downside protection in a worst-case scenario. First is the proprietary tech they have developed to serve banking customers and second is the amount of deposits they currently service (~$1B). That deposit base and tech may be massively valuable to a bank potentially looking to acquire.

- "Too-Big-To-Fail": Not in the traditional sense but instead because of how embedded BMTX is in the college-branded banking landscape. ~70% of all college-branded bank accounts are handled by BMTX who also solves a huge pain point for colleges by handling student aid disbursements and all the administrative and regulatory efforts involved with that process.

Shareholder Base/Insider Transactions

Following the de-SPAC in late 2020, PIPE investors are no longer in significant control of the float. There are currently 3 owners with 5-6% ownership including Luvleen [CEO], Vanguard, and Pacific Ridge Capital Partners (HNW investment advisor with a micro-cap strategy).

There are 22.7mm public & private warrants with a strike of $11.50 expiring in January 2026 I expect to be worthless (no dilution). No insiders have bought since de-SPAC due to the fact they consistently handle material non-public information. Post FCB transfer, I expect insider purchases as management continues to reiterate they know how undervalued the stock is.

Management

Luvleen Sidhu [CEO]: Luvleen founded BMTX through an incubation process at Customers Bank. Following the de-SPAC, there have been multiple management resignations (all personal reasoning related) and changes in the business model as they navigate a volatile banking environment. I believe Luvleen has rebuilt a resilient management team and is focused on the right things (growing deposits through nurturing current relationships, ensuring best regulatory practices, creating excellent technology, and refining banking partnerships). Because of this, I believe she is a great fit long term for the business.

Sidhu Family Involvement: Luvleen Sidhu founded BMTX with the guidance from, and as a subsidiary of, Customers Bank. The current Chairman & CEO of Customers Bank are Jay Sidhu (Luvleen's Dad) & Sam Sidhu (Luvleen's brother) who also headed up Megalith FAC, the SPAC vehicle used to take BMTX public - SPAC transactions with related parties like this were very common in 2021. While I don't intend to discredit Luvleen's accomplishments as CEO, it is an important dynamic to understand. As an investor, this relationship is very positive for BMTX given that CUBI is a highly regarded depository institution and has previously extended the banking partnership and aided in BMTX's success, which I believe will continue.

Jim Dullinger: Jim joined the company in March 2022 as Chief Accounting Officer and 11 months later took over CFO following the transition from their prior CFO to a corp dev role. Jim, like Luvleen, is very focused on the most accretive key drivers for the business and creating the most efficient processes for things the company can control. After speaking to Jim, it is clear he identifies problems, understands the business with extreme competence, is focused on long-term value creation, and sees deep value in the stock currently.

Jamie Donahue: Jamie joined BMTX as Chief Data Officer in October 2020 and has since assumed the role of President & CTO. Previously, Jamie spent 5 years at Finastra, a FinTech company owned by Vista. While at Finastra, he headed up the Cloud Architecture - Engineering & Delivery team. He also spent time at First Republic Bank as VP of Cloud Engineering.

Summary

At current levels, I believe BMTX is truly an incredible opportunity. They are vital to the college banking landscape, have a great partnership with T-Mobile, possess a deep margin of safety, and have strong catalysts that will drive immediate earnings power. Using normalized earnings estimates, this business shows potential for incredible shareholder returns.

For further details see:

BM Technologies: Deep Value Turnaround