TMUS - BM Technologies Q3: Turning Point

2023-11-22 08:41:46 ET

Summary

- Management showed their ability to execute by finalizing the FCB deal and reducing OPEX (-15% YoY) through their profit enhancement plan.

- Management's focus on the higher education business is exactly what they should be doing as it has the most immediate opportunity, cheapest CAC, better economics, and a true competitive advantage.

- I believe the strong higher education deposit base, interchange fee uplift, and the variable rate DPSA will lead the company to significant profitability in 2024 and breakeven EBITDA in Q4.

Summary

Following the Q3 earnings report BM Technologies (BMTX) released Monday, I wanted to publish an update and my review of the print.

I recently covered BMTX in late September highlighting the business overview, my bullish thesis, financial highlights, and views on management. I've linked the article here . Below I will cover the status of my thesis & risks and provide my updated model/forecasts & intrinsic value calculations.

To summarize the quarter overall:

- Management showed their ability to execute by finalizing the FCB deal and reducing OPEX (-15% YoY) through their profit enhancement plan [PEP]

- Management's clear focus on the higher education business is exactly what they should be doing as it has the most immediate opportunity, cheapest CAC, better economics, and a true competitive advantage

- I believe the strong higher education deposit base, interchange fee uplift, and the new variable rate DPSA will lead the company to significant profitability in 2024 and expectations for breakeven EBITDA next quarter

Thesis Review

- FCB Post-Transfer Economics: Now that the FCB transfer will officially be complete on or around December 1st, these new economics will come to fruition. I have adjusted my model to match management's guide on FCB's Durbin Exemption interchange uplift from 45 bps to 65 bps. This new fee structure will result in significant EBITDA accretion (I'm estimating ~+$4.65mm in 2024). This isn't just a massive economic win for the company but also shows management's ability to execute, rebuilding the market's confidence in the team.

- Deposit Base Stabilizing: Results here were 2-part; there was a strong recovery in higher ed deposits (+5.5% YoY) as a result of the increased disbursement processing activity but T-Mobile (TMUS) deposits continued to flee (-18.5% QoQ). Given the rate sensitivity of T-Mobile deposits, I don't see this base recovering until we see meaningful rate cuts. Management is also doubling down on higher ed which is the right move in my opinion. With currently <15% of BMTX-handled disbursements going to BMTX Vibe accounts, there is so much immediate opportunity to scale this deposit base without the need to acquire new university partnerships. Management outlined a clear plan to increase that 15% figure and reduce post-graduation churn by offering a cash-back rewards program starting in Q1 '24, fraud tools, and an ID verification tool.

- Cheap CAC at Universities: Currently BMTX is by far the market leader in the university-branded banking business touching 1 in every 3 college students eligible for refunds. The moat BMTX created in this segment offers them a huge opportunity to acquire new customers very cheaply relative to other fintech offerings or banks. By funneling a larger percentage of total disbursements into BMTX vibe accounts (via the new initiatives mentioned above), this deposit base could grow very quickly. Alongside potential deposit base growth, the new variable rate DPSA (Customers Bank/T-Mobile also variable rate now) and uplift in interchange fees creates a compelling bull case for the higher ed business.

- Massive Operating Leverage: The management team really proved this thesis point in Q3. They cut OPEX by 15% YoY (people spend -22% QoQ), will realize 60% of the $15mm cost savings by the end of 2023, and will achieve the full target in the 1st half of 2024. As top-line in the higher ed business grows through deposit base expansion and better take rate economics for servicing and interchange, earnings power should expand significantly.

- New BaaS Partnerships: As management mentioned on the call, they will pursue new BaaS partnerships opportunistically but will not let it hinder the focus on the higher ed business. New BaaS partnerships were never a part of my forecast but instead an additional upside kicker if they were to come to life. The focus on higher ed is much more meaningful and a better use of time and resources.

Risks

- Macro: Higher rates continue to impact T-Mobile deposits which is the main earnings risk I see with the business. Fortunately, management has taken steps to improve service fee yield by switching both higher ed and BaaS take rates to be variable rate-based.

- Trading Mechanics: The stock is still very illiquid which causes significant price volatility. As management continues to show focus and execution ability, I truly believe there is good reason for volume to increase as more sophisticated investors start building up the shareholder base.

- Bank Transfer: No future risk as the transfer is official and will be fully complete within 2 weeks.

- Regulatory: No updated view.

Financial Highlights

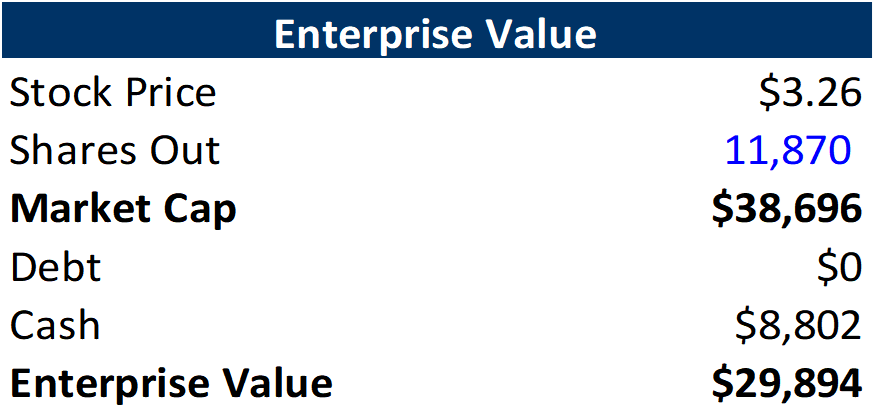

Current Enterprise Value

{kind=link}

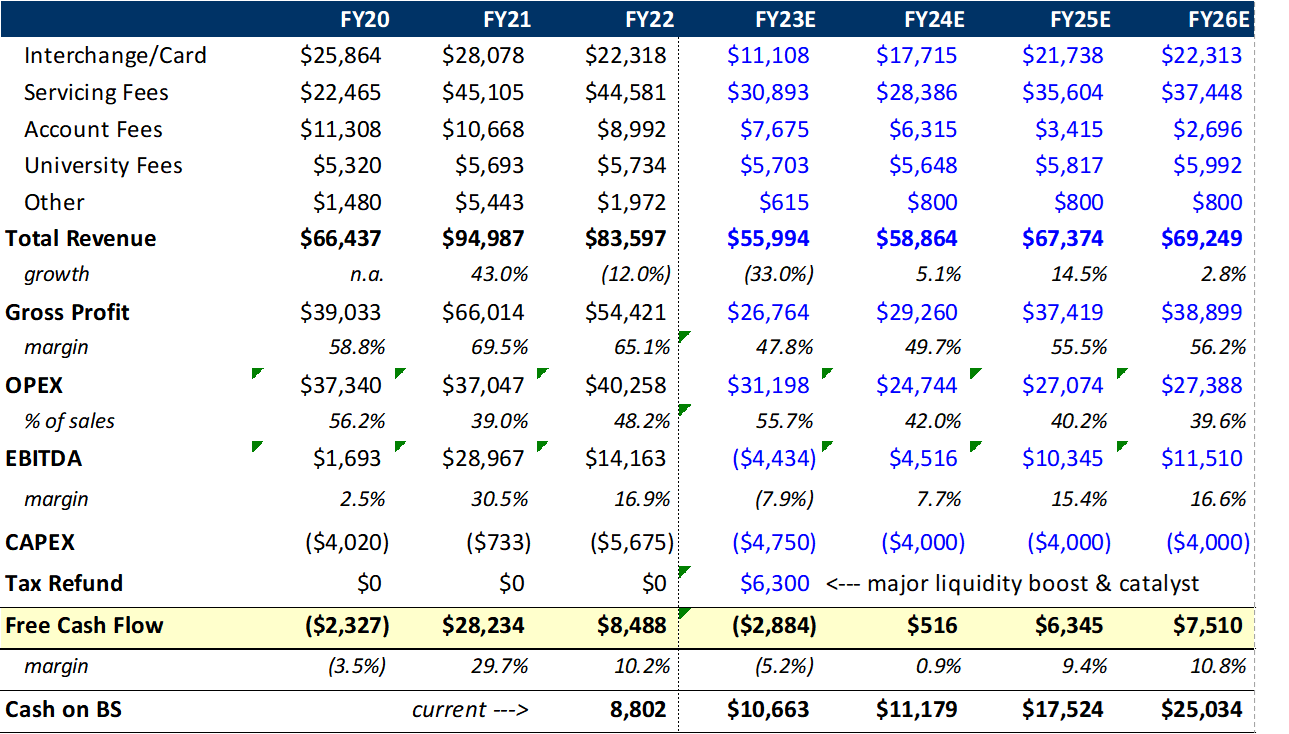

Updated Model Highlights

{kind=link}

Updated Model Assumptions: FCB transfer completed 12/1/2023, broke out core processing payments from tech amortization given new 3-year core processor agreement - affecting gross margin, stronger higher ed deposit recovery, higher ed interchange take rate to 65 bps, $4.3mm tax refund received in Q3 -> $2mm expected to be received in Q4.

Intrinsic Value Calculations

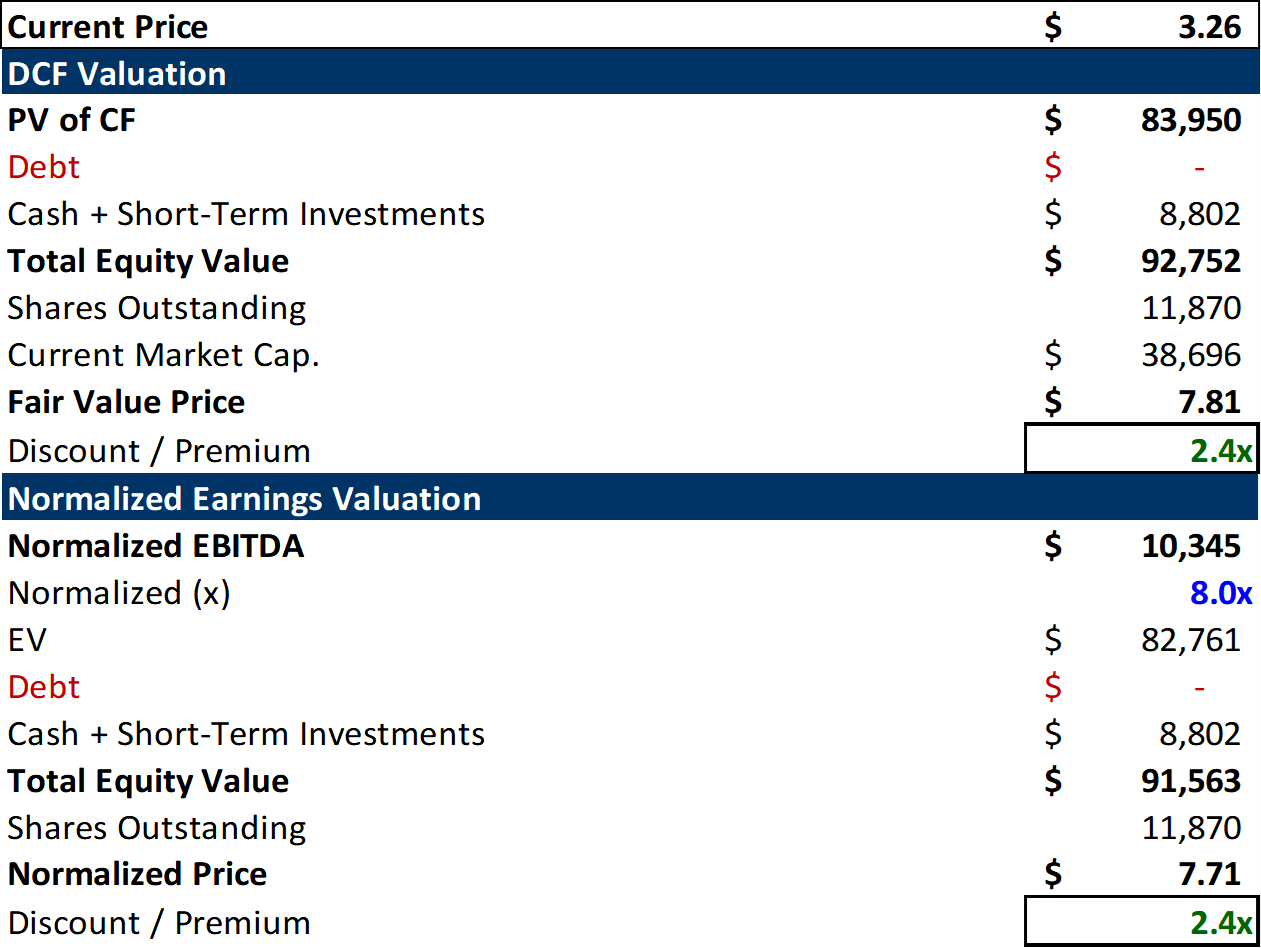

{kind=link}

Calculated intrinsic value using DCF and normalized earnings methodologies. Used 13.13% discount rate for DCF and had T-Mobile deposits dropping to 270mm in 2024 and sticking flat through the forecasted period. Used 8x multiple at a discount to the comparable average of 14.5x given the difference in business size and quality (my opinion).

Summary

I believe BMTX currently trades at a discount to the intrinsic value of the company. In my opinion, the margin of safety is still wide (see my last article : cash, assets, and "too-big-to-fail") and growth opportunities in higher ed are massive. Management's execution ability was shown this quarter and their clear focus was refreshing and my biggest takeaway from the call.

For further details see:

BM Technologies Q3: Turning Point