BME - BME Offers A Good Mix Of High Yield And Market-Beating Total Returns

2023-07-03 12:02:40 ET

Summary

- BlackRock Health Sciences Trust is a CEF focusing on healthcare, offering a 6.5% yield and a strong performance record, even beating S&P 500 in total returns since its inception.

- The fund trades stocks and writes covered calls, and is currently trading at a rare -4.3% discount against its NAV; its dividends have remained fairly flat despite its holdings being known as dividend growers.

- BME is considered a good fund with an above-average performance and supports a dividend yield close to 7%, but investors should not expect dividends to rise significantly in.

BlackRock Health Sciences Trust ( BME ) is a CEF focusing on healthcare industry that's been around for nearly two decades. When all considered, this is a good fund for income-oriented investors who are looking for a place to get a decent 6.5% yield with low volatility and track record of strong performance.

BME has accomplished something that not many funds have accomplished which is beating S&P 500 in total returns since inception which puts it in the top 5% of all funds and gives it a highly deserved 5-star rating by Morningstar . Typically, it's very rare for an actively-managed fund to beat S&P 500 in total returns in the long run, especially if it's not highly focused on tech stocks, not to mention the well-known statistic that 99% of fund managers fail to beat S&P 500 in the long run.

The fund combines multiple strategies to accomplish its goals, including trading stocks as well as writing covered calls. For much of its history, the fund traded at a slight premium of 4-6% against its NAV, but currently it is trading at a -4.3% discount, which is very rare for the fund. The last time the fund was trading at such a large discount was during the COVID crash, and that discount didn't last long. Before that we also saw the fund briefly on discount during the market correction that occurred in Q4 of 2018 which brought S&P 500 down by -19.9%. In other words, the only times this fund traded at a discount in the past was during market crashes or deep corrections. This is actually the first time the fund is trading at a discount while the overall market is not in a correction mode, which is telling me that the discount might not last for long.

The fund has an interesting dividend history. It originally started as paying quarterly dividends but switched to monthly payments later on. If you don't count special dividends like the big $4.50 payment in 2015, the fund's dividend has been fairly flat around 20–21 cents per share per month. Over the years the fund hasn't cut its dividends but haven't raised them much either.

This is interesting considering the fact that many of the fund's largest holdings are known as dividend growers. For example, the fund's largest holding is UnitedHealth ( UNH ) which grew its dividends by 571% in the last decade. This stock corresponds to close to 9% of BME's total weight.

The fund's next three biggest holdings, accounting for another 15% of its total weight, are also solid dividend growers. Eli Lilly ( LLY ) raised its dividends by 130%, Johnson & Johnson ( JNJ ) raised its dividends by 80% a nd Merck ( MRK ) raised its dividends by 70% in the last decade. You'd think that some of this dividend growth would make its way to BME's dividends, but so far it hasn't. I must admit that this is one disappointing aspect of this fund, but it still didn't stop the fund from outperforming in total performance, so it could get a pass.

The fund writes covered calls to boost its dividends so that it doesn't have to sell as much stock to generate income. It sells calls against individual stocks that it holds, which is different from many other covered call funds that sell calls against index funds. Currently, the fund's coverage ratio is 35%, so it only writes calls against one third of its holdings while the remaining two thirds are allowed to grow and prosper if those stocks were to rally higher. Also keep in mind that large cap healthcare stocks inherently tend to have low volatility, so selling covered calls on these stocks won't generate the yields you'd get from selling covered calls on tech stocks like BlackRock's some other funds such as BST ( BST ) are doing. At best, selling covered calls against companies like JNJ and MRK will generate about 1-2% additional yield annually, which isn't much.

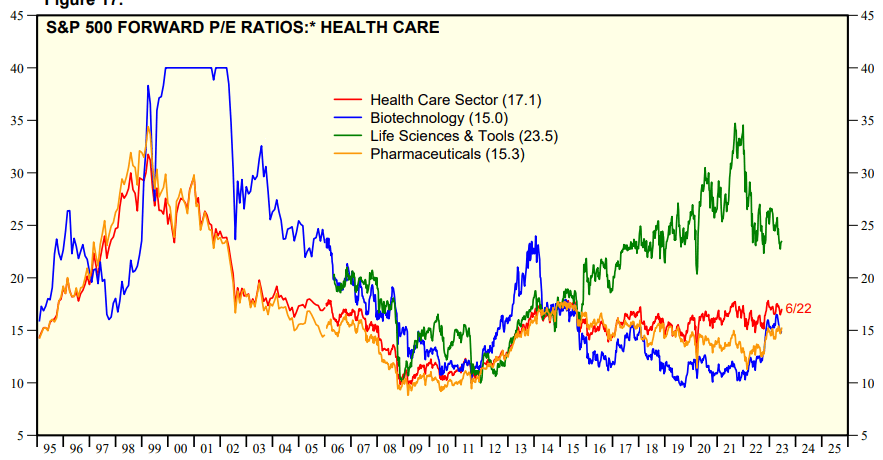

Moving forward, I expect healthcare stocks to perform decently. Apart from financials and REITs this is one of the cheapest sectors in P/E basis. In overall, healthcare sector has a P/E of 17, biotechnology subsector has a P/E of 15.0 and pharmaceuticals have a P/E of 15.3 while Life Sciences and Tools have a higher P/E of 23.5. Moreover, health insurance and healthcare management companies trade in single digit P/Es.

{kind=link}

Apart from valuations, we also know that there is going to be a lot of demand for healthcare moving forward. Some people call healthcare field to be "recession proof" which I'd partially agree with. It is recession-proof in that people have to spend money on healthcare no matter what because this is not a discretional spending. In many countries, healthcare spend is protected and covered by the government regardless of whether the economy is booming or in recession. On the other hand, being "recession proof" doesn't mean that healthcare stocks will outperform. This year we've already seen them underperform. YTD overall market is up 17% while a variety of healthcare related indices are flat at best.

One thing I always say in healthcare related articles remains true. Population is getting older, people keep living longer, and people keep getting sicker at younger ages due to bad dietary habits and lack of exercise. Now people will need active healthcare for longer periods of time. We now have data showing that half of Americans have at least one type of chronic disease, and the rate is increasing. About 30 years ago, young people having chronic diseases like diabetes, heart disease and hypertension were unheard of, but now it's becoming mainstream and are seen even in people in their 20s. The demand for healthcare won't disappear anytime soon.

Overall, BME is a good fund with a track record of beating overall market returns. This is not saying that BME will continue beating market returns in the future, but at least we can say that it will have an above average performance. The fund supports a dividend yield close to 7%, but I wouldn't expect dividends to rise much more from here since the fund prefers issuing special dividends once in a while than hiking dividends, even though most of its largest holdings have a history of hiking dividends significantly. Investors who choose to put their money into BME should be comfortable with this type of approach.

For further details see:

BME Offers A Good Mix Of High Yield And Market-Beating Total Returns