BMEZ - BMEZ: Deep Discount On Beaten Down Sector

2023-12-12 19:52:24 ET

Summary

- BlackRock Health Sciences Term Trust is trading at a deep discount and has struggled due to the poor performance of the biotech healthcare sector.

- The fund's new distribution policy aims to retain assets when times are lean and reward shareholders when things are going well.

- BMEZ has a focus on private investments, which adds to its risk profile but also presents potential growth opportunities.

Written by Nick Ackerman, co-produced by Stanford Chemist.

In October, a few of the technology-oriented BlackRock ( BLK ) closed-end funds shifted their distribution policies. Stanford Chemist highlighted this earlier at the time of the announcement in more detail and why it wasn't a big deal. The overall adjustment was to retain assets better so the funds don't erode too fast when times are tough, such as they have been for some sectors.

One of those sectors that has been struggling the most has been healthcare, and more specifically, the biotech healthcare subsector. That directly impacts BlackRock Health Sciences Term Trust ( BMEZ ), and the fund has been struggling for a while now. After initially launching in early 2020, this fund exploded higher through the raging innovative tech space of 2020 and 2021. Since then, the fund has deflated to trade below the fund's original inception price.

Today, I wanted to give BMEZ an updated look as it trades at a deep and attractive discount. I believe the fund continues to be a 'Buy,' but it is definitely for the riskier investor. I also believe the new distribution policy is better for the fund in the long term.

Alongside these positives for the fund, Saba Management is also in play here. They own a sizeable and growing position in this fund, along with several other BlackRock funds they are campaigning against that we've been discussing. Additionally, besides Saba buying up shares, the fund has been buying up its own shares. When a fund repurchases shares when trading at a discount, that is accretive to the NAV , benefiting all current shareholders.

The Basics

- 1-Year Z-score: -0.73

- Discount: -15.90%

- Distribution Yield: 8.03%

- Expense Ratio: 1.32%

- Leverage: N/A

- Managed Assets: $1.755 billion

- Structure: Term (anticipated liquidation January 29, 2032)

BMEZ has an investment objective to "provide total return and income through a combination of current income, current gains, and long-term capital appreciation. It intends to do this through "at least 80% of its total assets in equity securities of companies principally engaged in the health sciences group of industries and equity derivatives with exposure to the health sciences group of industries."

Along with the investment policy, the fund also utilizes an options strategy. They have no leverage in the form of borrowings, which I view as a positive given the already volatile biotech space of which BMEZ carries a significant weight. This comes with its own pros and cons, such as potentially capping upside during a strong bull market. However, in a flat market, the fund can generate returns and is a slightly defensive strategy. The options premium brought in can help reduce some of the losses sustained during a down market.

BMEZ last listed being overwritten by under 24%, so most of their portfolio is running uncapped. I would view that as a positive currently, while the healthcare space is looking depressed.

'Poor' Performance But In Line With The Broader Sectors

As noted, healthcare and specifically biotech have performed quite terribly. That means it wasn't only BMEZ that struggled; it was the sector as a whole, with biotech performing quite terribly. We see BMEZ come right in the middle in terms of a total NAV return performance between the investible sector benchmarks of SPDR S&P Biotech ETF ( XBI ) and Health Care Select Sector SPDR ETF ( XLV ).

Ycharts

BMEZ coming right in the middle is about what we would expect as the more traditional healthcare companies have helped hold the fund up while biotech struggled mightily. This is a performance chart from BMEZ's inception, which does show that despite the drop in price since inception, it's still generated positive total returns due to the distributions the fund paid out. An important distinction for looking at the overall results of an investment is also to incorporate those distributions and dividends, but this is especially true for closed-end funds that will generate all or nearly all of their returns via payouts.

With all that being said, we can see that on a total share price basis, the fund has not performed, leading to a bit of a loss over the course of coming up on the end of its fourth trading year. Inception was in January 2020, so we are getting there. What this resulted in is the fund trading at a deep and attractive discount currently. In fact, it's near the widest discount this fund has traded at, excluding the sharp drop we saw during Covid.

Ycharts

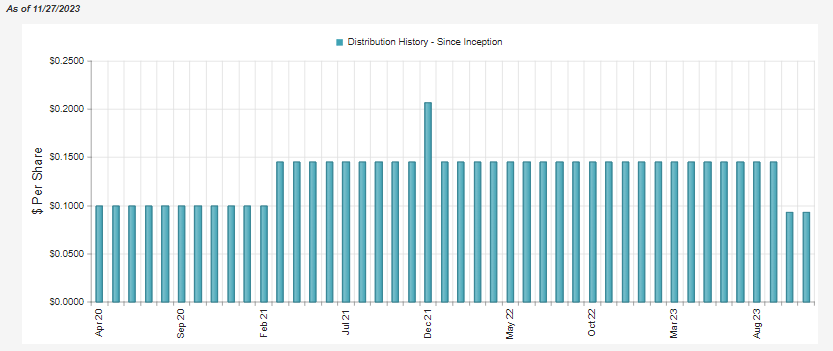

Distributions - 6% Managed Plan

The new distribution policy kicked in recently, and it is based on 6% of the average NAV over the prior rolling 12-month period. That means when things are going well, the payout will increase. When things are going poorly, the fund will start to see its payout pared back. That means the fund will be retaining those assets to rebound when it happens - which I believe is what the positive is.

{kind=link}

That does mean the payout will vary every month going forward, and it also resulted in an immediate and sizeable drop when switching to this plan. Of course, no one likes that, and it was likely a contributing factor to seeing the fund's discount widen in the more recent months.

Like most equity funds, they will rely on capital gains to fund their distribution. Additionally, BMEZ, being a more growth-oriented fund that is focused on innovative companies, makes the reliance even higher. In fact, BMEZ produces no net investment income and instead relies solely on gains being able to be generated to fund its payout. This is not that unusual for this type of fund, either.

{kind=link}

Helping to offset the realized losses seen in the semi-annual report was the fund taking in nearly $11 million from writing options. However, they realized losses of $15 million from their underlying portfolio. At the same time, during the first half of the year, the fund was still performing fairly well, with a fair bit of unrealized gains coming in and rebounding from last year's substantial losses.

In the second half of the year, things started to turn sour again, leading to NAV per share declining. Generally, the best way to quickly see if a fund is earning its payout or not is simply watching the NAV through a given period of time. To highlight this, here is the YTD NAV performance.

Ycharts

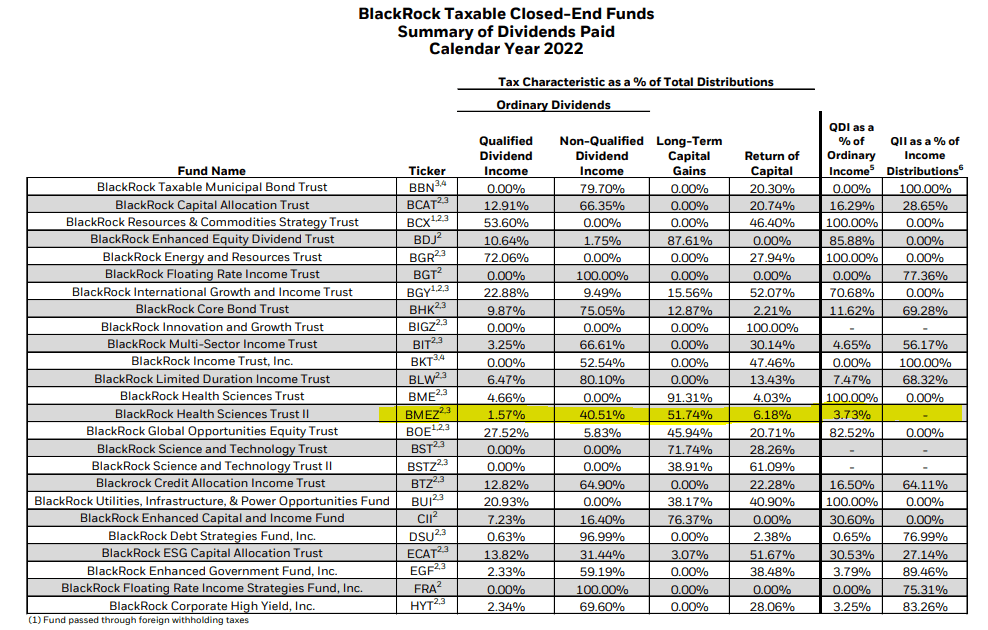

For tax purposes, we discussed that in our prior update. Here's a recap:

Given the sizeable losses in the prior year, it might come as a bit of a shock that most of the distribution isn't classified as return of capital. Only a small portion is, with the larger allocation being long-term capital gains and non-qualified dividend income. That would be vastly different from the coverage metrics we see above.

BMEZ Distribution Tax Classification (BlackRock (highlights from author))

This is a good reminder that tax classifications aren't representations of actual distribution coverage as so many investors seem to believe. While they can tend to correlate, they are two separate data points to consider and interpret. In the case of BMEZ, it would appear that realized long-term gains from the prior year being so large were pushed into this year.

{kind=link}

BMEZ's Portfolio

What makes this fund a bit riskier, aside from the overall more volatile holdings from the biotech space, is that BMEZ also has a focus on private investments. On paper, these investments can seem less volatile, but that's because they don't generally get marked as regularly - only if they go through another round of funding and then the valuation can shift dramatically. With markets being depressed mostly outside of the mega-cap tech names, most venture companies haven't been looking to raise new funding.

With that being said, BMEZ doesn't run as aggressively in terms of its exposure to these private companies compared to its cousin funds. For some context, BlackRock Science and Technology Term Trust ( BSTZ ) is running with around 35% of the fund in private investments.

As of the last semi-annual report , BMEZ listed less than 7% being allocated to level 3 securities.

{kind=link}

Their last quarterly commentary noted that private company exposure was at 9% allocated over 21 private companies. That was up from the 17 listed in their Q2 commentary , which was one down from the private allocation that stood at 18 holdings in total in our prior update. That was because Adicon Holdings went public on the Hong Kong Stock Exchange.

More recently, the four new private companies all came in the last quarter, and they have had a practice of not listing the actual company names. On their website, they sometimes show up as "project" names or, in the case of their commentary release, simply Company A-D.

{kind=link}

In total, the goal has been to target around 25% of the portfolio being invested in private companies. So, this is anticipated to grow over time when the market opens up in this space.

This is still important to consider because it all means that the current discount might not be as deep as it first appears. Instead, there is some leeway that should be considered. The lower the level 3 security exposure, the less leeway we should apply.

For example, let's say they are wrong by over half, and the valuation is only around $70 million rather than ~$146 million listed. That would have meant NAV would have been roughly $18.35 as of their last report instead of $19.06. A meaningful amount of difference at around 3.73% would still indicate a significant discount relative to the $16.42 market price shares were trading on the day of the report.

So, it's definitely important to consider that even with the assumption of being massively incorrect in the valuation, the difference isn't enough to make it not appealing. It just simply wouldn't be as appealing.

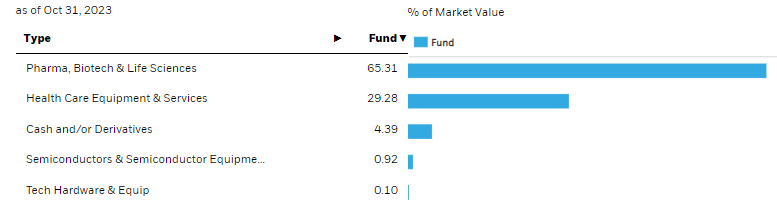

BMEZ lists the sector exposure breakdowns in fairly large buckets, so that can make it more difficult to get a quick reference of just how biotech-heavy the fund is. They also include pharmaceutical investments in this basket. This was roughly in line with how the fund was positioned in terms of sectors earlier this year.

{kind=link}

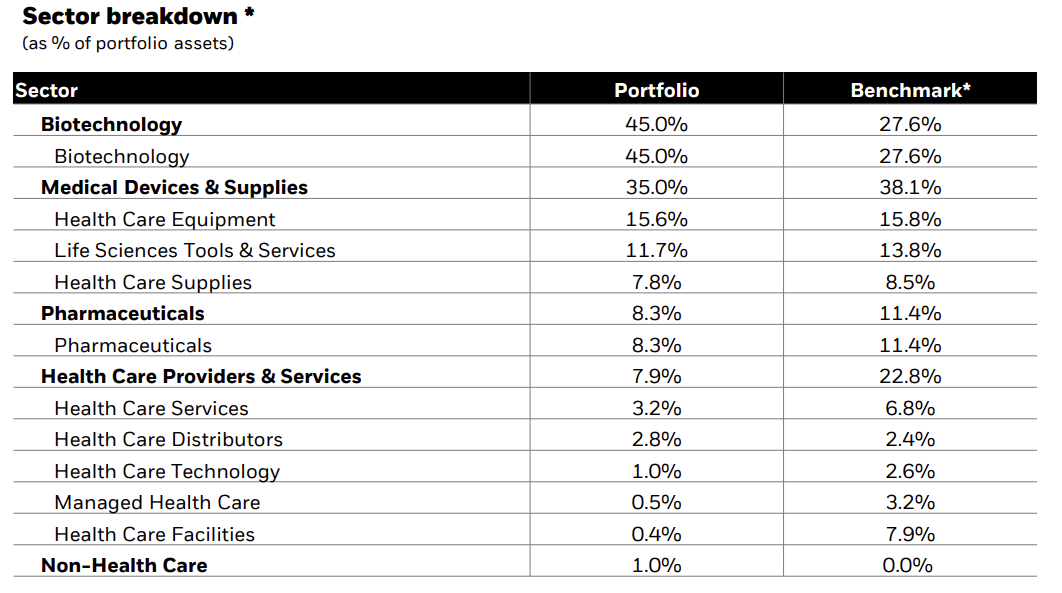

In their latest quarterly commentary, which is dated a month before the above breakdown, biotech is listed at around 45% of the fund's portfolio. That is up from the end of 2022 when the allocation stood at 40.2%. Three of the four new private companies in the portfolio are likely at least partially responsible for seeing this increase.

{kind=link}

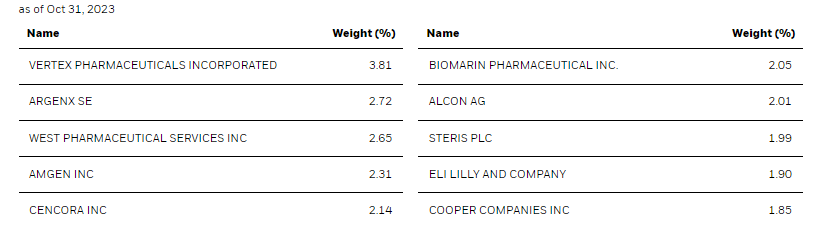

In looking at the top ten, we see a lot of familiar names that we saw earlier this year, which is in line with the fairly small gyrations we saw in the overall sector weightings.

{kind=link}

That said, one notable addition to the top list is Eli Lilly and Company ( LLY ). LLY has been on a tear as a weight loss play. This has driven shares to trade at some stratospherically high levels, with it pushing around a 90x forward P/E ratio now. This was actually an addition to the portfolio fairly recently because it wasn't listed in their last N-PORT or semi-annual report, both of which are as of June 30, 2023.

Conclusion

BMEZ is trading at a sizeable discount and the biotech space has continued to perform poorly, that's led to poor results for BMEZ. However, more private investments in the company could mean we are starting to see an unthawing of the venture capital space, which is what makes BMEZ more unique in the first place. Saba is also in the mix with this fund, and that could lead to some further potential upside catalysts in the future. All this lines up to make BMEZ a 'Buy' candidate, but only for those that have a higher risk tolerance.

For further details see:

BMEZ: Deep Discount On Beaten Down Sector