BND - BND: A Poor Way To Invest Your Fixed Income Now

2023-08-18 17:59:19 ET

Summary

- The Vanguard Total Bond Market Index Fund has long been widely recommended as a safe investment option for conservative investors.

- But it has only traded since 1986 when inflation had been tamed though bond yields were still at very high levels.

- It is now heavily invested in treasuries and issues of the most indebted companies, many of their bonds barely of investment grade quality.

- Given its noncompetitive distribution yield, we suggest much safer alternatives available to the retail investor.

For decades bond funds have always been what all investment professionals recommended that conservative investors invest in for "safety." No investment advisor would ever have been fired for putting an elderly widow's money into a bond fund.

The Total Stock Market and Total Bond Fund Index Fund/ETF Portfolio Is A Common No-Brainer D-I-Y Solution

Do-it-yourself investors were likely to find many voices online suggesting they adopt the approach championed by John C. Bogle and invest in mutual funds with the lowest expense ratios.

Many Bogle Disciples went farther, led by Taylor Larimore of the Bogleheads forum . They advised that do-it-yourself investors should keep their finances simple by investing in a "three fund portfolio" made up of a U.S. broad market index fund like the Vanguard Total Stock Market Index Fund ( VTSAX ), an international index fund like ( VTIAX ), and the Vanguard Total Bond Market ( VBMFX ).

The more risk adverse the investor was, the more they were told they should allocate to the bond fund. Some investors, including John Bogle himself , eschewed international investment for U.S. investors and advised a two fund approach that required investing only in the Total Stock Market and Total Bond Market funds. Over time the three or two fund approach has become mainstream and you will find it recommended by many investment sites and publications.

More recently, investors have moved to investing in the ETF equivalents of these investments which allow portability to other platforms other than Vanguard, the recommendations you will see are for the Vanguard Total Stock Market Fund ETF Shares ( VTI ), the Vanguard Total International Stock Index Funds ETF class ( VXUS ) and Vanguard Total Bond Market Index Fund ETF Shares ( BND ).

As you can see, until the coming of COVID-19 the bond component of these simple portfolios performed brilliantly from the inception of the Total Bond Market Index Fund in December of 1986.

Vanguard Total Bond Market Index Fund Performance

Inception - July 2020

This chart makes it understandable why investors were lulled into believing that the Vanguard Total Bond Fund and its ETF offspring, BND, were indeed "safe as houses." But that safety was an illusion.

Let's extend our chart out to the present:

Vanguard Total Bond Market Index Fund Performance

Inception - August 2022

The explanation for what happened is simple. As the chart below shows, the Vanguard Total Bond Market Index fund began trading at a time when the Fed funds rate was near an all-time high. Though the inflation it had been raised to counter was tamed, rates persisted in being far higher than inflation for a long, long time.

In 1986 the average Fed Funds rate was 6.80%. The Vanguard Total Bond Fund's yield at inception was north of 8%, though inflation in 1986 was only 1.86%.. Its yield (the yield of the bonds it held) only slowly declined over the following years because it took quite a while for investors to trust that inflation had been truly controlled.

So though inflation never again rose over 5.4% (in 1990) and remained under 3% for most of the following years, the yield of the Vanguard Total Bond Index Fund slowly declined though remained above 6% over inflation until the mid-2000s.

VBMFX Performance vs. Its Yield

Complacent Investors Ignored Bond Math

Not surprisingly, during the decades up until 2022, bonds were safe and BND a fine way to buy them. But investors who had never experienced the frightening inflation of the 1970s forgot how bond math works.

Unlike stocks, bonds behave in a very predictable way.

- If you buy a bond and the yield of a newly issued bond is lower , the value of your bond, should you wish to sell it, will rise until the price the buyer pays gives his investment a yield similar to that of the newer bonds on the market. This meant that as bond rates declined BND's NAV grew.

- If you buy a bond and the yield of a newly issued bond is higher , the value of your bond, should you wish to sell it, will decline until the price the buyer pays is competitive with the newer bonds on the market. This means that if rates go up BND's NAV will decline. If they go up fast when BND's yield is low as it was in 2020, that decline will be much bigger than its yield.

- The amount by which the principal value of your bond will rise or fall can be estimated by looking at how much time your bond has to wait until it is redeemed. The longer until the bond matures, the higher -- or lower -- its trading value. The amount by which a bond's value will decline is indicated by its duration, which is a technical term denominated in years. In theory a bond with a duration of 5 years will gain or lose 5% for every 1% change in prevailing interest rates. BND's duration hovers around 6 Years, so a 1% rise in rates could be expected to knock 6% off its NAV.

Duration is a concept that works very well when pricing individual bonds, but its usefulness declines when applied to a bond fund that holds thousands of bonds of a wide range of maturities, as is the case with Vanguard's bond fund. Which holds an ever-changing selection of bonds of maturities ranging from short to very long, since its goal is to reflect the entire bond market (minus high yield bonds, TIPS, and some mortgage bonds.) In actuality the duration of BND has changed over time, so it isn't possible to predict exactly how it will respond to a 1% rise in rates.

You will read all kinds of estimates of how long it will take for the NAV of a bond fund to recover based on its duration. I have seen several that suggest it takes (Duration * 2) +1 year for that recovery to take place. That would be 13 years for those who bought BND in 2021. These estimates ignore the fact that bonds are always being bought and sold as BND tracks its index. It also ignores the fact that some bonds may default and some companies that issued its bonds go bankrupt.

The bottom line is that when bonds have nowhere to go but up, you can expect to lose money in any bond fund and quite a lot of money in one with a 6-year duration.

Moreover, the other takeaway is that when inflation persists and investors get worried about it again, bond issuers will have to tempt them with higher yields to convince them to buy their bonds. We can expect bonds to go back to yielding several percent more than inflation unless by some miracle inflation vanishes and stays vanished for several more years.

The Financial Media Have Done a Poor Job of Reporting on The Federal Reserves' Clearly Delivered Message

We all read article after article throughout 2022 telling us after each meeting of the FOMC that the Federal Reserve was nearing a "pivot." This year, as rates continue to climb steadily higher, the talk has turned to promising that we are now in a final "pause" which will be followed by the coming of lower rates.

But I have been listening to the actual press conferences that Chairman Jerome Powell has given after each FOMC meeting, and I have been shocked by the gap between what he actually has said and how reporters have reported his speech in the financial press.

Powell has stated again and again that the Federal Reserve is dedicated to lowering inflation to its 2% target and that it does not want to make the mistake that was made in the 1970s, when the Fed declared victory over inflation too quickly and lowered rates only to see inflation surge to levels that eventually required that the Fed Fund rate reach 20.61% on July 20, 1981.

Powell has also repeatedly stated that the unemployment rate stands at a historic low. Since the Fed has only two legally defined mandates, that it prevent damaging unemployment and fight inflation, all its efforts have to be concentrated now on controlling inflation.

He also repeats in response to questions about all the other factors that reporters question him about, that it is not the Federal Reserve's job to think about the budget, the deficit, or any of the other factors that are constantly brought up by writers in the Financial Press as reasons why the Federal Reserve will "have to" lower rates. That, he has stated repeatedly in his addresses, is "fiscal policy" which is the job of Congress. Not the Fed.

If you don't believe me, go listen to his latest (or any) press conference which you can find on YouTube .

How The Total Bond Market Index Fund has Changed

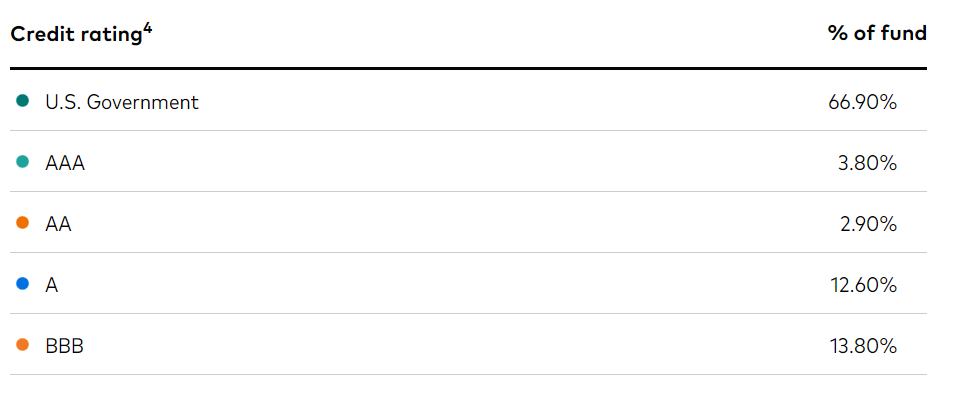

For many years I was investing in bond funds, before the advent of QE, the total bond market was made up of a mix of government bonds (treasuries and agency bonds) and Corporate bonds. Treasuries usually had the lowest yields for the same maturity because of their perceived safety, backed as they were by the excellent credit of the United States. Highly rated corporate bonds paid another percent or so, while the corporate bonds issued by companies whose bonds received ratings that though still investment grade were lower, BBB, and BBB-, had higher yield.

But over the past decade, as the government has taken on more and more debt, the amount of the total U.S. bond market made up of government bonds has soared. By now 66.90% of the bonds in BND are Government bonds. This figure which includes 46% made up of Treasuries and Agencies (I assume the GSE agencies) and another 20.1% of which is made up of Government Backed Mortgage Bonds.

BND Portfolio Credit Rating as of 7/31/2023

{kind=link}

As you can see, a significant amount of the non-government debt is made up of the bonds issued by companies with the lowest investment grade rating. I note that Vanguard does not break down its BBB credit category into BBB+, BBB, and BBB- categories. However, when I have used FAST Graphs to examine the credit ratings of the supposedly higher quality stocks S&P 500 I have found a surprising amount of them bearing the BBB- rating which is only one step above junk.

BND's Market Cap Weighting May Be Tilting its Corporate Bond Weighting Towards Needier Companies' Bonds

Furthermore, there is an important point to consider. I was made aware of it in a trenchant article written by Rich Roche that explored several issues with the Bloomberg U.S. Aggregate Bond Index. That is the parent index of the Spliced Bloomberg U.S. Aggregate Bond Float Adjusted Index that is tracked by BND.

That issue is this: this bond index, like the indexes Vanguard uses for most of its index funds, is market cap weighted. But where market cap weighting applied to a stock index means you end up owning the most successful companies, the reverse is true when buying corporate bonds. The companies that issue the most debt are not likely to be the ones whose debt you want to own. But that is what you get in a cap weighted index. As Roche states,

Issuers who go deepest into debt - the biggest bums - have the largest weights in a cap-weighted benchmark. Cap-weighted indexes must buy bonds in proportion to their capitalization weight to minimize tracking error to the benchmark, even if the security is only marginally of high enough quality to make it into the benchmark. These securities are the most likely to be downgraded or to default.

During the 40 years rates continued to slowly decrease over time, companies found it cheaper to refinance their debt, so the question of how dangerous it might be to invest heavily in the bonds of companies that were facing problems refinancing debt were not significant. But as we all know, there is a lot of corporate debt, taken on at very low rates, which will have to be refinanced within the next few years. The consequences of investing in the bonds of the "biggest bums" may be painful for those who hold their bonds.

In addition, bond funds have a problem. When you own a bond, you get back your principal if you hold it to maturity, so your only loss is caused by the decreasing buying power of money you put into the bond if the interest it paid was less than inflation. But bond indexes typically sell their bonds a year before they mature locking in face value losses caused by rising bond rates.

BND's Yield is Not Competitive with The Bonds It Holds

Two-thirds of the bonds I would be buying via BND are treasuries, many of them long-dated ones. You can see the actual holdings listing on the Vanguard website's Portfolio page for BND. But the payment you will get from BND every month is far lower than what you'd get if you bought that treasury.

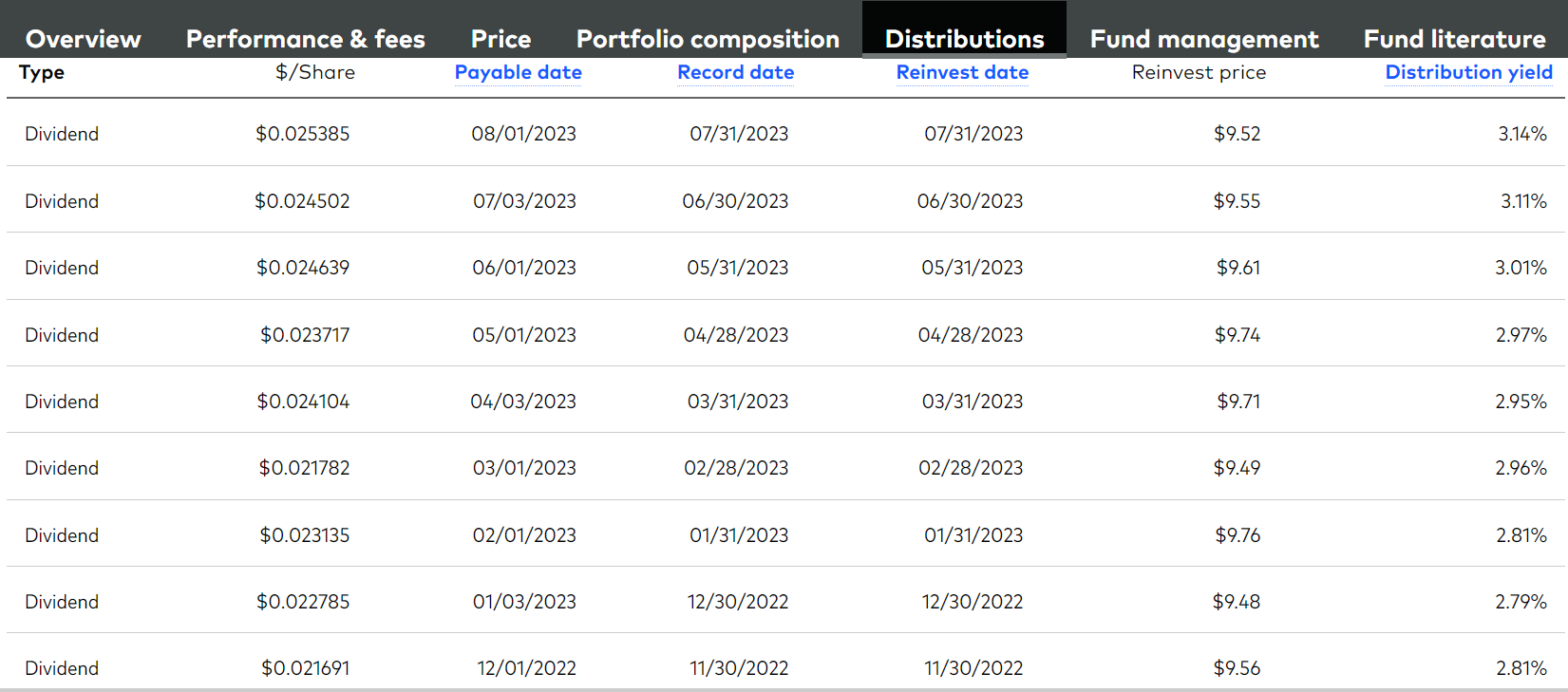

Though BND had a SEC Yield of 4.56% at the end of July 2033, experience has taught me that bond funds may never pay out interest that matches that SEC yield. What you want to look at is the distribution yield, which is what the fund actually puts in your pocket.

You won't see a distribution yield percentage given for BND, because it is an ETF whose price fluctuates all day. But you can see the distribution yield for the Admiral Shares mutual fund share class of the fund BND is a share class of, VBTLX. It's most recent payment represented a yield of 3.14% on its closing price.

VBTLX Distribution History 12/01/2022 - 7/31/2023

{kind=link}

That isn't much. And though BND enthusiasts argue that its distribution rate will rise as rates rise, as you can see, that distribution rate increases very slowly. Its payout has increased by only 0.42% over the last nine months, to get to that anemic 3.14%.

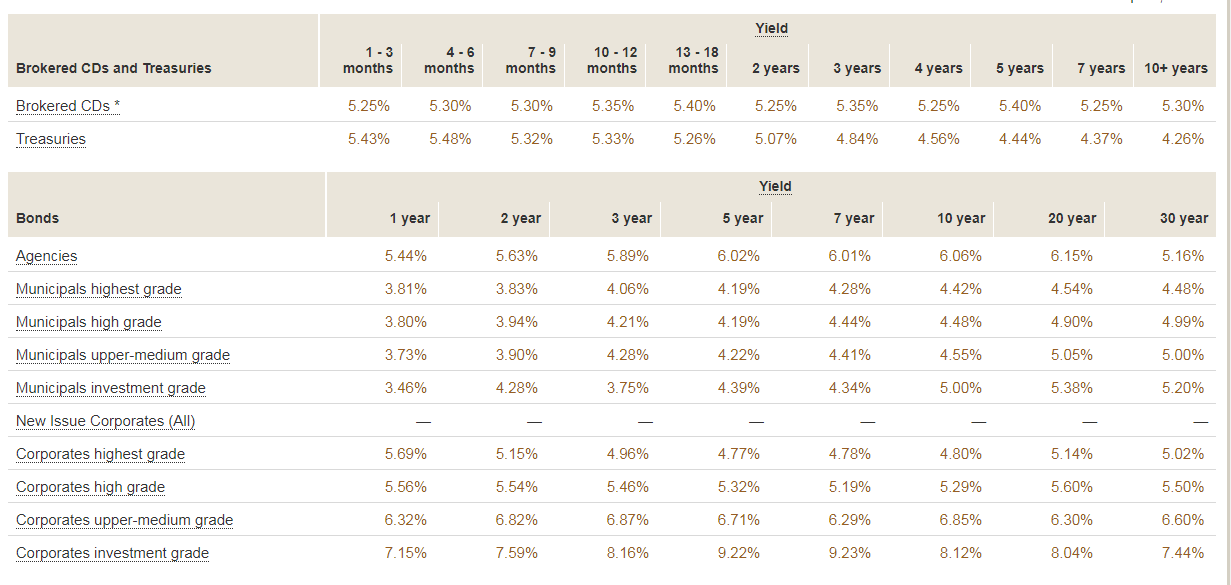

You could get a whole lot higher yield were you to buy 5-year Treasury notes on your own. Vanguard is offering one at a yield of 4.56%. And when you buy the treasury notes, you are guaranteed to get your principal back in five years no matter what happens with inflation. That won't happen with BND.

You can get a much higher yield, 5.47% as I write this, more than 2% higher than BND if you buy very short-term treasuries. (You can also get better rates on the secondary market, in my experience if you invest at Schwab, but that's another article.)

Vanguard Current Bond Rates - 8/18/2023

{kind=link}

Why This Is Your Grandaddy's Bond Market

Back in Grandpa's day, intermediate bonds were not a safe investment. The yields investors received from their bonds were far lower than inflation, eroding their buying power. That is one reason you don't see the creation of a total bond market fund until 1986, when bonds were beginning to recover.

The safest way to invest during the period of surging inflation that prevailed through the 1970s and early 1980s was in the shortest possible fixed income securities.

The first widely popular low expense fixed income fund offerings were therefore money market funds like the T. Rowe Price Prime Reserve Money Market Fund ( PRRXX ), which started trading on 01/26/1976 that held securities with a maturity of days or weeks. Vanguard's first money market fund started trading in 1981.

That's why if you have relied on BND, now that inflation has become an issue again and may possibly persist for significantly longer than the financial press' wishful thinking suggests, you need to rethink your strategy.

Don't Backtest BND - Inflation Has Changed Everything

Even now, when investors are still sitting on significant capital losses in the bond funds they bought back before 2021, I see people justifying investing in BND because historically it has yielded X%. Or pointing out that during some year in the past when rates rose investors quickly made up any temporary losses. These arguments ignore the hard fact that until 2020, BND operated only during a period when inflation rates were declining steadily, while interest rates remained considerably above the inflation rate. The advent of inflation like none we have seen in the economy since 1981 makes any backtest that runs only back to the middle 1980s irrelevant.

Worse are those backtests that look back at the 1970s, without taking into account the huge changes in the investment environment since then. Bonds in the 1960s were bought by institutions and those few investors wealthy enough to be able to buy large quantities and pay a hefty broker's commission. The few bond funds available had very high expense ratios along with the high broker commission and front load required to buy them. There were not hordes of retail buyers buying and selling daily with the click of a mouse. You can't expect bond funds today to behave anything like the bond market before the advent of online discount brokers.

So there is no backtest that can tell you how BND will behave in a new era where inflation meets extremely fast retail-driven bond markets, where nervous investors may take one look at their declining bond fund balance, panic and sell.

BND holds many bonds that were issued during the decade of near-zero QE Fed rates. Many of those bonds have years to go before they mature so rising rates have damaged their current asset value. They can only be sold at a loss. Companies who loaded up on cheap debt will have to refinance at higher rates at the same time that inflation has heavily damaged their profit margins. There will be more defaults especially in the poorer quality bonds in BND.

The Safest "Safe Fixed Income"

Money Market Funds

Money market funds are still the safest investment in an uncertain rate environment when inflation is still not tamed. Those of us who were adult investors in the early 1980s remember that. Money markets currently are offering yields over 5%. That yield goes up days after the Fed raises its rate. And unlike the case with BND, when you buy into a money market fund no matter what happens with rates, you don't have to worry about losing principal.

If you are in a higher tax bracket and investing in a taxable account a municipal money market fund may give you more after-tax income. But I have found that their rates are not competitive unless you have a huge taxable income and live in a state like California with exorbitant state taxes. This Fidelity Tax Equivalent Yield calculator can tell you if the rate on a muni money market fund makes sense for you. A prime money market fund would be taxed like a CD. So would some "government" money market funds that invest in derivatives and non-GSE bonds and hence are not exempt from state taxes.

A Rolling Ladder of One Month Treasuries

For those with several thousand dollars or more to invest and a willingness to invest a couple of minutes every month, there is an even better alternative: very short-term treasury bills. You can buy them at auction or on the secondary market at major brokerages like Schwab, Vanguard, and Fidelity.

Right now one month treasuries are yielding more than money market funds, If you have an unexpected need for your money they can easily be sold on the secondary market without fees, as long as you invest at one of the major brokerages.

This is not the case with brokered CDs which are extremely hard to sell on the secondary market and will result in a loss of principal if you need to sell them in a rising rate environment. Right now brokered CDs have a worse yield than treasuries, too. This is a sure sign that rates are still likely to be rising.

In a taxable account, short-term Treasuries have the advantage that you don't have to pay state or local income tax on their interest. Compared to a money market fund, this gives you an additional 0.30% or more in-your-pocket if you pay 5% in state or local tax. The actual advantage depends on how high your state and local taxes are.

Buying anything but the shortest treasuries can make your taxes a bit more complex, if you are investing in a taxable account. But if you stick to treasury bills, which only extend a year or less, rather than the longer-term Treasury notes you don't have to worry about accounting for accrued interest when you buy on the secondary market. The brokerage's 1099B will give you all the information you need to use common tax software to file.

Back before the advent of QE we old timers "knew" that treasury bonds were safest but paid the lowest yield for a given maturity. We expected them to pay a percent or two above the current rate of inflation. Because Corporate bonds were riskier, we expected them to offer another percent more yield than treasuries of the same maturity. Finally, because they were not liquid, we expected to get 2% or more over treasuries from higher yielding bank CDs.

QE changed that, but it's pretty clear that the Fed is licking its wounds over the damage its far-too-long adherence to QE has done to the economy. I expect rates to remain higher than they have been for the last decade for far longer than another year. It is quite possible, too, that stagflation will set in and inflation will continue to be a factor and force the Fed to continue to raise rates no matter how the economy is otherwise behaving.

If you have held BND for years enjoy your profits. But if you aren't willing to leave your money in it for 20 years or more, untouched, it is a very poor investment today.

For further details see:

BND: A Poor Way To Invest Your Fixed Income Now