BNDD - BNDD: Long-Term Treasuries Plus Yield Flatteners

2023-06-12 05:08:28 ET

Summary

- The Quadratic Deflation ETF is a fixed-income ETF that seeks to benefit from lower growth, deflation, and lower or negative long-term interest rates.

- The BNDD ETF's name may be misleading, as it outperformed in inflationary 2022 due to its yield curve flattening options.

- Investors should consider the likelihood of a recession and the potential for interest rate cuts, which may steepen the yield curve and be detrimental to the BNDD ETF.

In this article, I will review the Quadratic Deflation ETF ( BNDD ), a fund that is marketed as benefiting from deflationary environments. While we are currently in an inflationary environment, it is important to be prepared for what can happen in the future.

I find the BNDD ETF to be quite misleading. It is simply a long-term treasury ETF with a portfolio of yield curve flatteners. While curve flattening tend to be associated with deflation , that does not have to be the case. For example, in 2022, the yield curve flattened dramatically as the Fed raised short-term interest rates rapidly in response to inflation .

Looking ahead, I believe a pending recession will lead to yield curve steepening, so the BNDD may not be the best choice.

Fund Overview

The Quadratic Deflation ETF is a fixed income ETF that seeks to "benefit from lower growth, deflation, lower or negative long-term interest rates, and/or a reduction in the spread between shorter and longer term interest rates by investing in U.S. Treasuries and options."

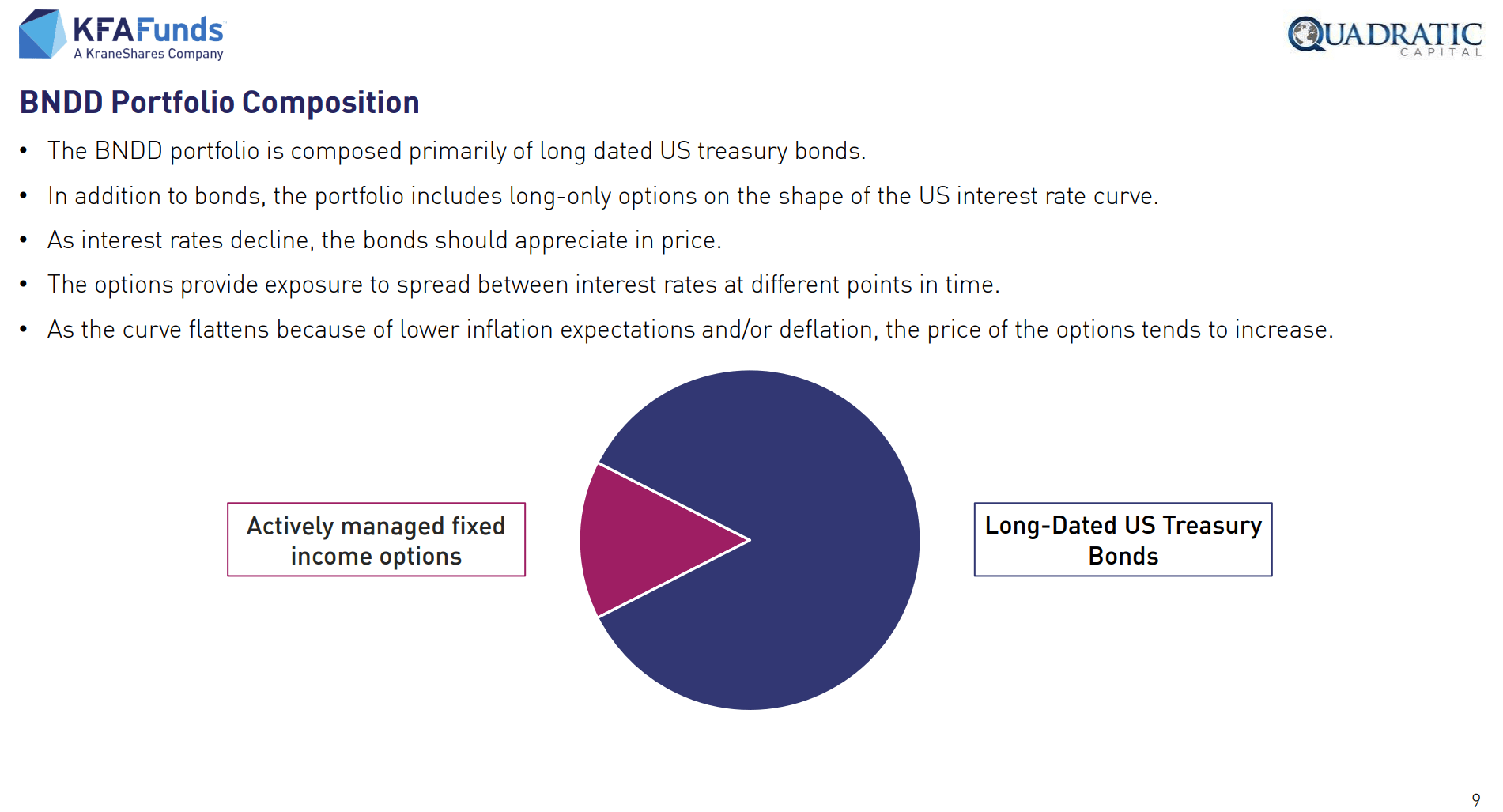

The fund aims to achieve its goals by owning long-dated US treasury bonds plus an actively managed portfolio of options that bet on the flattening of the US yield curve (Figure 1).

{kind=link}

The BNDD ETF may buy calls, spreads (long and short options at different strikes), and butterflies (long one call, short two calls at higher strike, and long a fourth call at an even higher strike) that are expected to appreciate in value as the yield curve flattens or inverts.

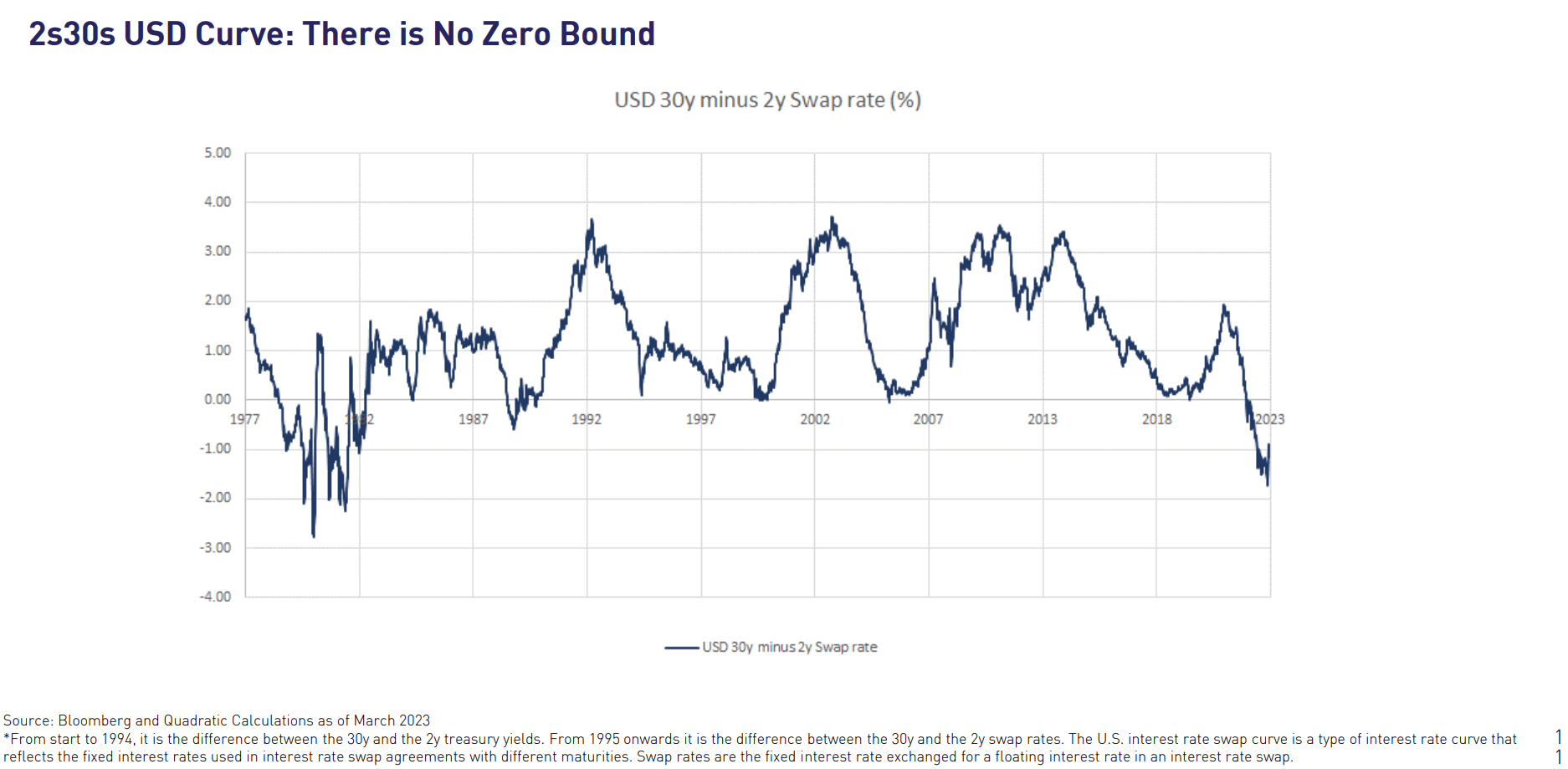

While yields themselves have a lower bound of zero, spreads do not have a lower bound and can go into negative territory in extreme circumstances (Figure 2).

Figure 2 - Yield spreads do not have lower bounds (BNDD investor presentation)

{kind=link}

The BNDD ETF was launched in September 2021, and has $55 million in assets. The BNDD ETF charges a 1.01% net expense ratio, although it is reduced to 0.96% until August 2023.

Portfolio Holdings

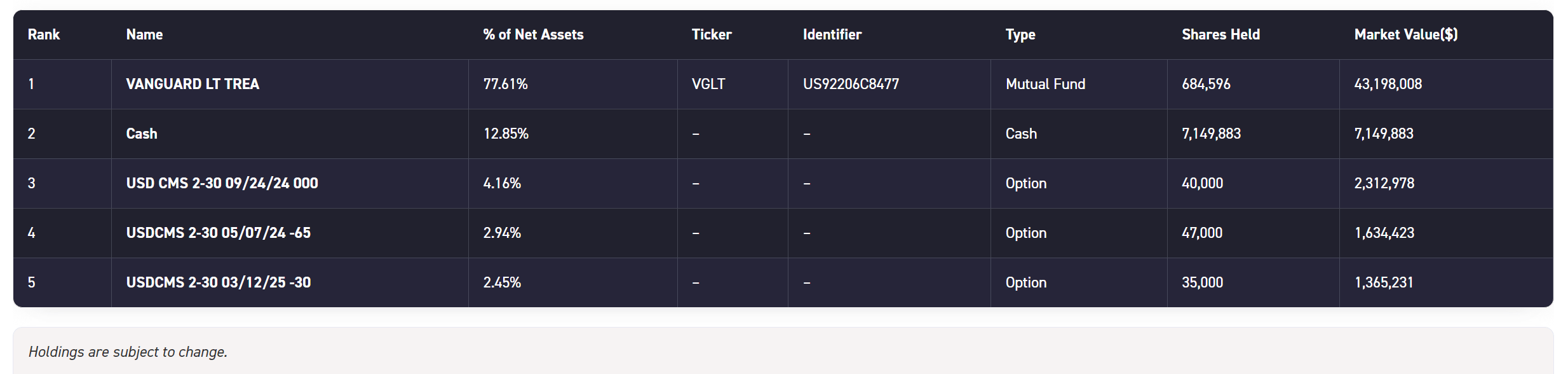

The BNDD ETF's portfolio is shown in Figure 3. The fund currently holds 77% of its assets in the Vanguard Long Term Treasury ETF ( VGLT ), 13% in cash, and the rest in OTC options that bet on the 2-30 yield spread.

{kind=link}

Distribution & Yield

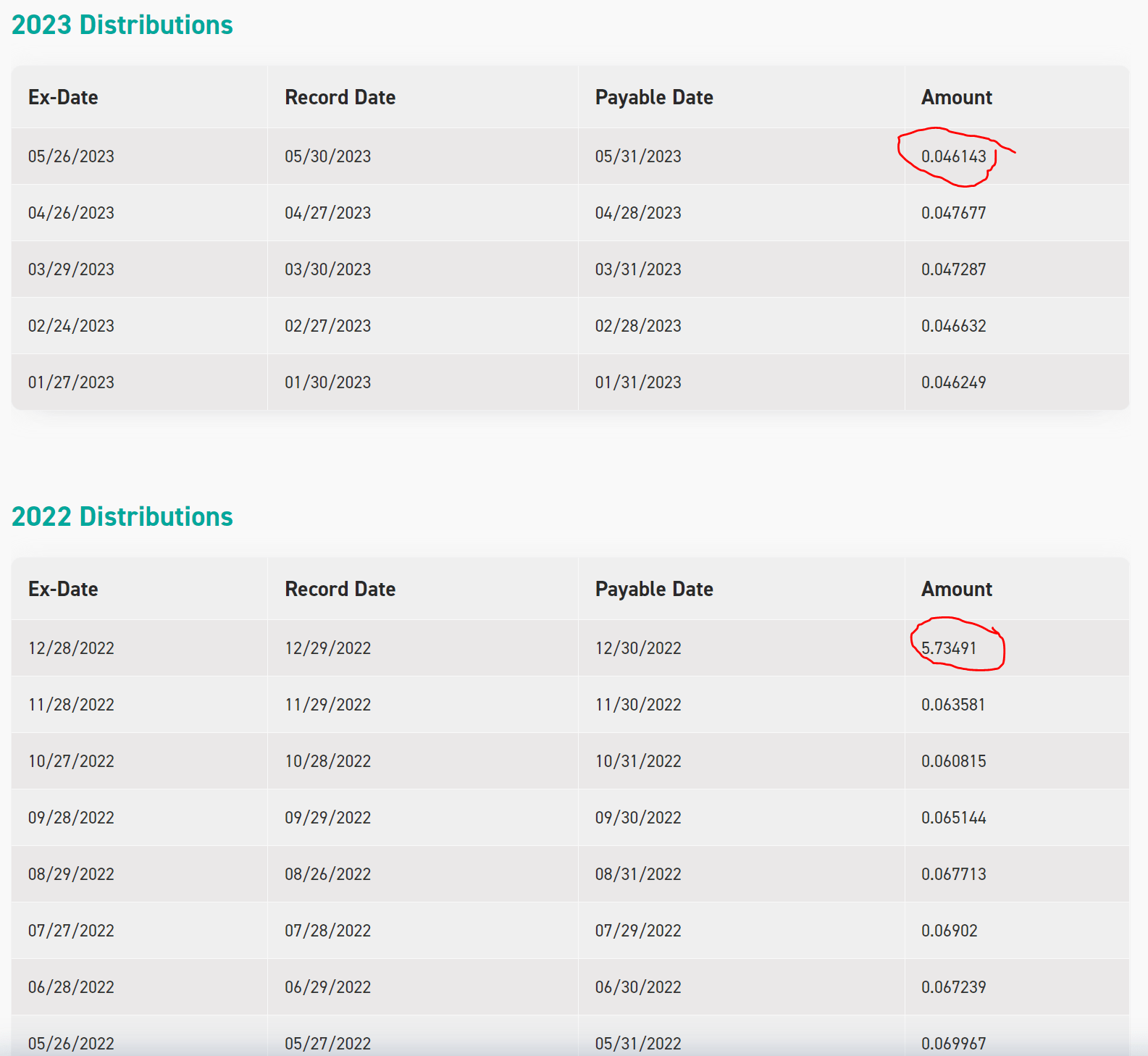

The BNDD ETF has a 30-Day SEC yield of 1.53% and its most recently monthly distribution of $0.046143 / share annualizes to 3.6% yield (Figure 4).

{kind=link}

Investors should note that the BNDD ETF paid a large distribution in December 2022 of $5.73491/share due to the realized gains of the fund's OTC options portfolio.

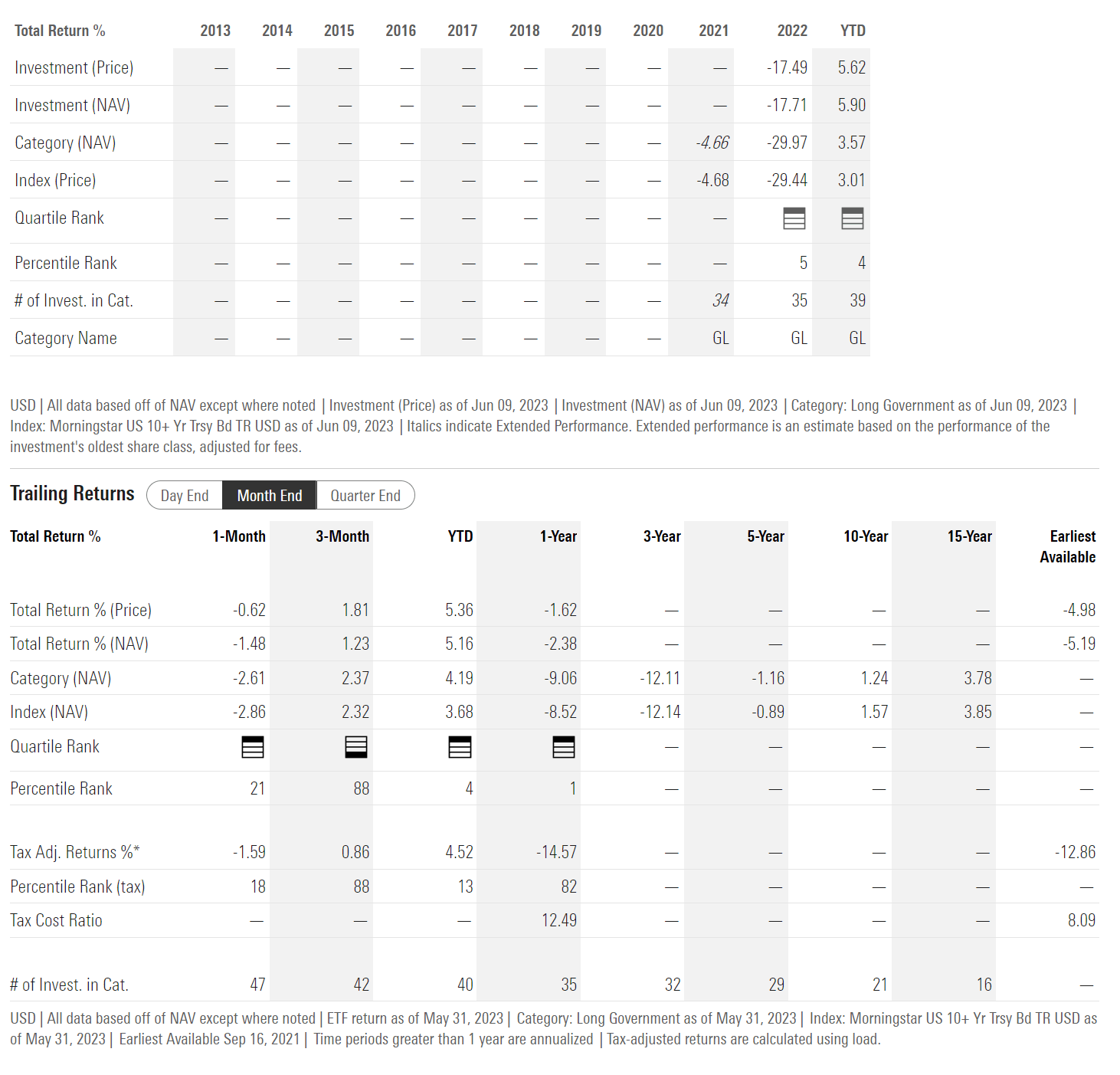

Returns

Figure 5 shows the BNDD ETF's historical returns since inception. The BNDD ETF only has a year and a half of operating history, so it may be hard to pass definitive judgment on the fund.

{kind=link}

The BNDD ETF returned -17.7% in 2022, and has an average annualized return of -5.2% since inception to May 31, 2023.

While the BNDD ETF's returns have been poor in absolute terms, that is mostly due to the long-term treasury position of the ETF, as the flattener positions have added 'alpha' since inception. For example, relative to the Bloomberg Long U.S. Treasury Index, the BNDD ETF have outperformed the benchmark by a cumulative 18.1% to March 31, 2023 (Figure 6).

Figure 6 - BNDD has outperformed due to options portfolio (BNDD annual report)

BNDD Managed By Star Manager

The BNDD ETF is managed by Nancy Davis , a former Goldman Sachs head trader who have won numerous awards and industry accolades. However, unlike its sibling fund, the Quadratic Interest Rate Volatility and Inflation Hedge ETF ( IVOL ), the BNDD ETF has not been as successful in raising assets.

Another Poorly Named Fund Aimed At Retail Investors

Consistent with my initial assessment of the IVOL ETF, I find the BNDD ETF's name and description to be misleading. The IVOL ETF is best described as 'TIPS ETF Plus Options On Interest Rate Steepeners' and the BNDD ETF is best described as 'Treasury ETF Plus Options On Interest Rate Flatteners' .

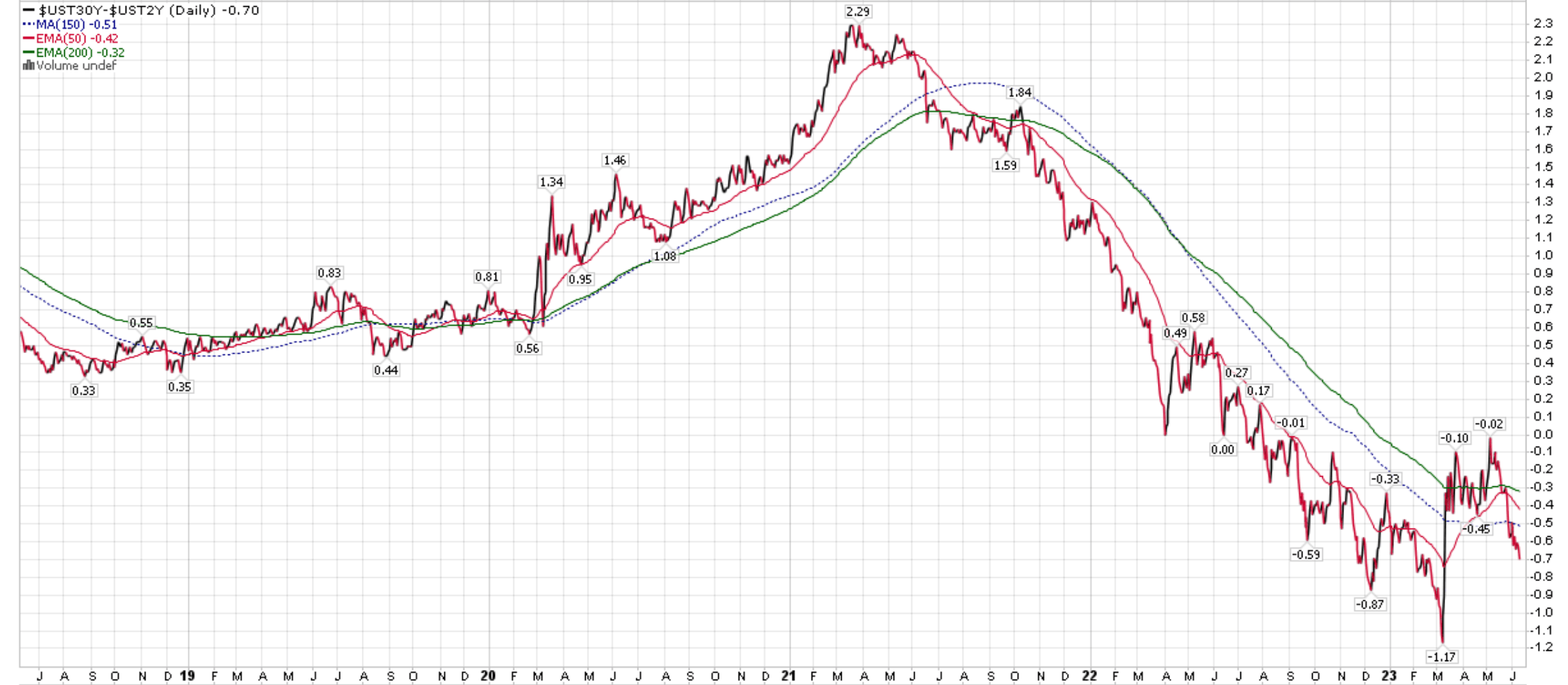

Just as the IVOL ETF did not 'protect' investors during the most recent inflationary episode as IVOL's portfolio of TIPs bonds can fall in value from rising interest rates, the BNDD ETF can 'outperform' in an 'inflationary' period as long as the yield curve flattened, as we saw in 2022 (Figure 7).

Figure 7 - 2/30 yield curve flattened dramatically in 2022 (Author created with price chart from stockcharts.com)

{kind=link}

Taking a step back and looking at the IVOL and BNDD ETFs in tandem, I fear Quadratic may be wrapping sophisticated OTC interest rate options into retail products that the average retail investor may not understand.

Tails I Win, Heads You Lose...

In fact, cynics may argue Quadratic has set up a 'tails I win, heads you lose' product line up by allowing investors to bet on either interest rate steepening ("IVOL") or flattening ("BNDD"). What is common is that both funds have relatively static ~80% allocation to low cost ETFs while charging a ~1% management fee. So the actual fee works out to ~5% for the 'active' option portfolio.

Which One To Choose?

Furthermore, combining yield curve bets with long-duration assets muddies the water. The ideal situation for the IVOL ETF is falling interest rates (positive for duration) with short-term interest rates falling faster than long term interest rates (steepening).

For the BNDD ETF, it is falling interest rates (positive for duration) with long-term interest rates falling faster than short-term interest rates (flattening).

Looking forward, these are the two key questions investors need to consider. Is interest rates going to rise or fall? Is the curve going to steepen or flatten?

My best guess is that interest rates may stay 'higher for longer' as the Fed tries to combat stubborn inflation. However, if the economy falls into recession in the coming quarters, investors will expect the Fed to cut interest rates to stimulate the economy. This expectation should steepen the yield curve. Therefore, I lean towards the IVOL ETF over the BNDD ETF at this juncture.

Conclusion

The Quadratic Deflation ETF owns a low cost long-term treasury ETF plus OTC options that bet on a flattening 2/30 yield curve.

Similar to its sibling fund, the Quadratic Interest Rate Volatility and Inflation Hedge ETF, I find the description of the BNDD ETF to be highly misleading. The BNDD ETF outperformed long-term treasuries in 2022 due to its interest rate flattener options, despite 2022 being 'inflationary' instead of 'deflationary'. Interest rate curve steepening or flattening does not have to necessarily correspond to inflation or deflation.

Looking forward, my view is that the economy will likely fall into recession and investors will start to price in interest rate cuts. This should steepen the yield curve, which will be detrimental to the BNDD ETF.

For further details see:

BNDD: Long-Term Treasuries Plus Yield Flatteners