BOE - BOE: Discounted Global Covered Call Fund

2023-03-23 22:05:05 ET

Summary

- BOE shares some similarities with BDJ but has a sizeable portion of its portfolio outside the U.S.

- The fund's performance in 2022 was helped out by call writing, but having some heavier weightings in tech seemed to hurt results.

- BOE is currently paying out an attractive distribution that seems sustainable at the current level.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on March 8th, 2023.

After looking at an update of BlackRock Enhanced Equity Dividend Trust ( BDJ ) recently, it seems only fitting that we look at its global sister, BlackRock Enhanced Global Dividend Trust ( BOE ). They report on a consolidated annual report, so we have a fresh report for BOE available.

Similar to its sister BDJ, the fund had held up relatively better than the broader market, thanks in part to its covered call strategy. A strategy that is slightly defensive and works best in a flat market. During strong bull markets, these sorts of funds can lag.

However, despite BOE being similar and having a relatively higher emphasis on value-oriented sectors now, the fund did underperform BDJ quite significantly for 2022. Through 2022, BOE had a greater emphasis on tech stocks, which could have driven the results we are seeing. Also, it's much more attractive at a deep double-digit discount, whereas BDJ has been commanding a premium lately.

Since our last update , the fund's discount hasn't changed hardly at all. On the other hand, we've also seen some recovery since our last update, so the fund's performance reflects that. The S&P 500 Index isn't a direct benchmark, but it can give us some color on how the broader "market" performed.

BOE Performance Since Prior Update (Seeking Alpha)

With an attractive discount, this fund is worth considering for investors looking to increase global exposure.

The Basics

- 1-Year Z-score: 0.18

- Discount: -11.47%

- Distribution Yield: 7.59%

- Expense Ratio: 1.06%

- Leverage: N/A

- Managed Assets: $705.93 million

- Structure: Perpetual

BOE has an investment objective to "provide current income and current gains, with a secondary objective of long-term capital appreciation."

The fund intends to achieve this through the following:

investing in at least 80% of its net assets in dividend-paying equity securities and at least 40% of its assets outside of the U.S. The Fund may invest in securities of companies of any market capitalization but intends to invest primarily in securities of large-capitalization companies. The Fund generally intends to write covered put and call options with respect to approximately 30% to 45% of its total assets. However, the percentage may vary from time to time with market conditions.

They focus on writing options on individual stocks in their portfolio. The fund last reported that the portfolio was 43.66% overwritten at the end of February 2023. That is on the higher end of its 30 to 45% target. That could suggest they are more defensive at this time. Having more of a portfolio overwritten could suggest that they don't foresee these positions being called away.

The fund's expense ratio is higher than BDJ's but not excessively. BOE is less than half the size of BDJ, so that could be some of what is causing this.

Performance - Attractive Discount

2022 was an important year for looking at the performance of funds as it was a bear market year. With covered call funds, they can often avoid some of the downside due to collecting option premiums. We saw that work out exceptionally well for BDJ as the value-heavy portfolio leaning also played a role.

BOE's performance wasn't particularly strong, but some of the downside moves were avoided relative to SPY .

YCharts

However, we know that BOE is more than large-cap U.S. stocks. The fund invests the vast majority of its portfolio in large-caps at a 95.81% representation of its portfolio, but it's also ~50% global positions. With that being the case, they provide in their annual report more appropriate benchmarks that reflect its positioning better.

Unfortunately, the MSCI ACWI Call Overwrite Index doesn't have a long history at this point, so we can't see the 5 and 10-year performance metrics for comparison. What we can see is that in the last year, BOE has outperformed its benchmark as expected.

The underperformance over the last 5 and 10 years also isn't particularly shocking. As we said, during bull markets, covered call funds can lag results as the upside can potentially be given up. Of course, higher expense ratios and portfolio positioning also play a role.

{kind=link}

At the same time, BOE could be considered more attractive because the fund's discount is quite attractive. While it has experienced trading at a deep discount fairly consistently, the current level is below the last 10-year average.

YCharts

It's easy to think that international investments always underperform the U.S. Historically, that wouldn't be accurate to say , though. Their performances have moved in cycles, with the U.S. lately haven't a particularly extended period of outperformance. That's why some investors today probably think that internationals always underperform. For some of us, it always has in our investing careers.

{kind=link}

Meaning that at some point, an investor will be happy to hold international investments as they outperform their U.S. counterparts. When that happens is really anyone's guess. Therefore, being diversified can be an appropriate approach. Given the attractive valuations internationally relative to the U.S., that could potentially be something that helps boost the chances of international outperformance going forward.

Global Valuations (JPMorgan)

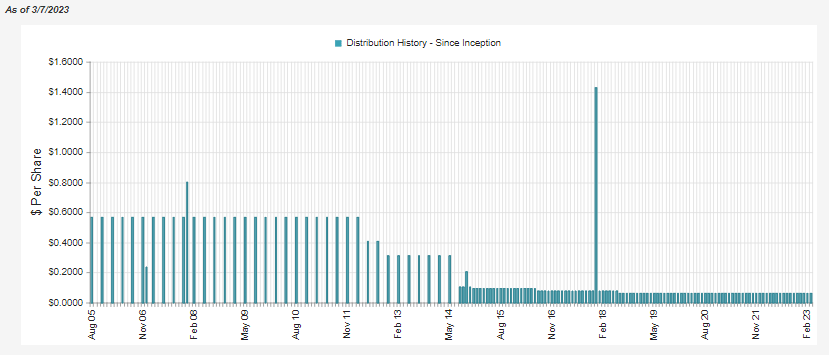

Distribution - Options Writing Contribute To Coverage

I've touched on the distribution cuts in the past in more detail. However, since the fund has underperformed with its global exposure, it's not surprising to see that it has several distribution cuts. These cuts happened even outside of the GFC, a time when many other funds were cut. Still, these cuts are familiar and something we've seen with other globally focused funds.

Since equity funds such as BOE require capital gains to fund their distributions when lacking performance, the chances of the distribution reaching unsustainable levels increase.

{kind=link}

The current NAV distribution rate of 6.72% makes the current distribution sustainable, in my opinion. Of course, if equities continue to remain pressured and make new lows, then sustainability will come into question.

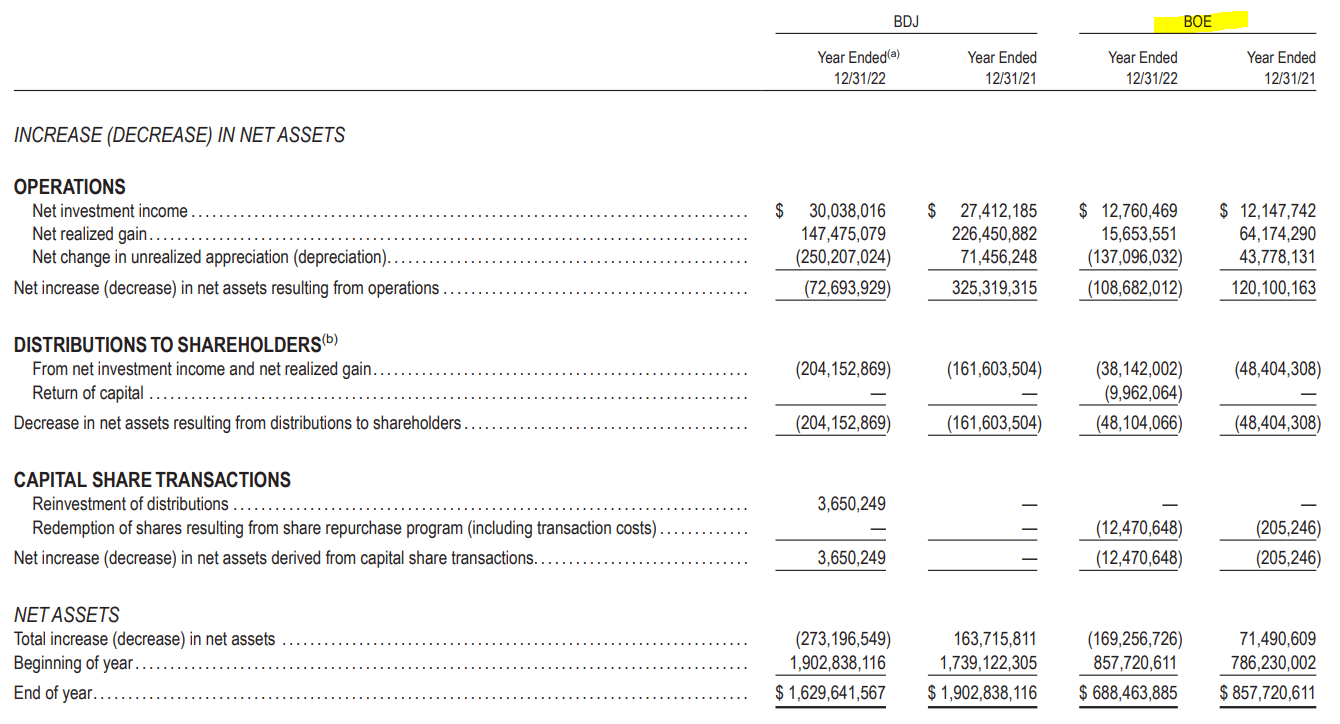

BOE experienced some net investment income year-over-year. However, it was fairly negligible. NII coverage here comes in at around 26.53%, meaning a sizeable gap of capital gains will need to be found to sustain the distribution.

{kind=link}

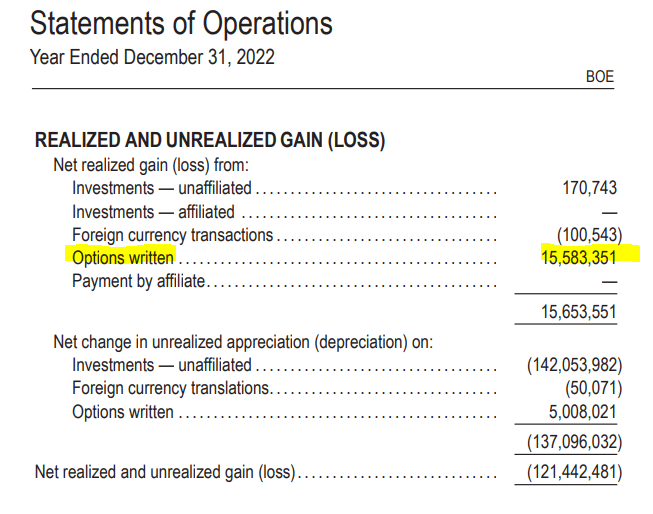

In the last year, they were able to recognize $16.654 million in realized capital gains to help support that shortfall. Some investors might be interested to know that these capital gains came almost entirely from their options writing strategy. The realized gains from their underlying portfolio were actually quite minimal.

{kind=link}

That being said, we can clearly see that the fund suffered substantial unrealized losses. After factoring in the NII and options written capital gains, we are still coming to a shortfall of the $48.104 million it paid out in the year 2022. Thus, why the coming years will be important to see how the fund performs to start covering its distribution.

One might have noticed that the fund's total distributions paid out year-over-year fell, and that's due to the fund repurchasing shares. Since the fund is trading at a discount, this is accretive to the fund on a per-share basis. They took 1,285,502 shares out of circulation in the last year, or over $12.47 million in assets from the fund. This is also a factor of why NII may not have climbed year-over-year higher than it otherwise would have on an absolute basis.

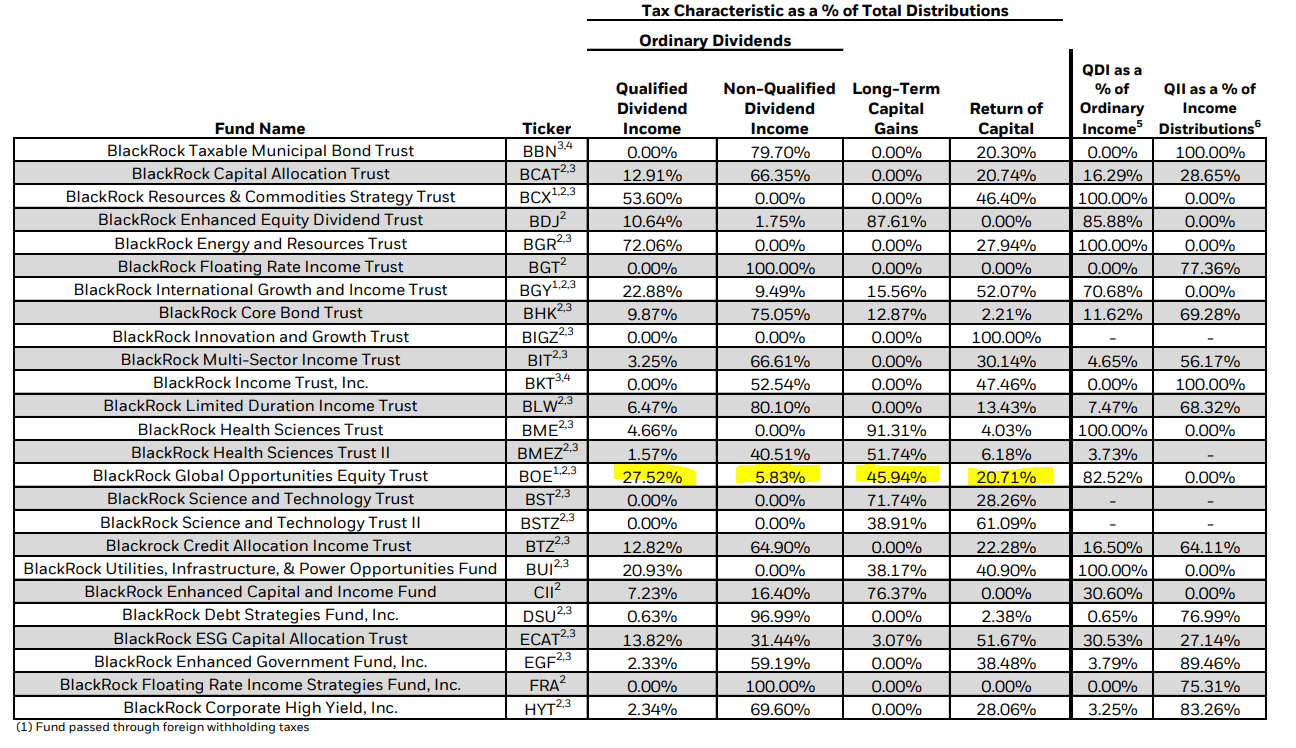

For tax purposes in 2022 , the fund's primary classification was long-term capital gains. This was followed by qualified dividends and then return of capital. Given the shortfall in coverage, ROC would have been expected.

{kind=link}

While it would have technically been destructive ROC, it isn't always a bad thing.

- For tax purposes, it means the taxes are deferred for investors as it reduces an investor cost basis, and then taxes are only potentially due when sold.

- It could also have meant that they didn't want to sell off assets that they would have otherwise appreciated but that they wanted to hold onto. Instead of realizing enough gains in the fund, trimming losers and keeping winners could have been better.

- The other benefit here is that utilizing ROC distributions also means a level distribution rather than adjusting in what could potentially be a down year or two. Instead, investors receive a steadier payout that can become more predictable.

BOE's Portfolio

Another way to illustrate how large the companies that BOE is holding onto besides labeling them as "large-cap" is by providing the average market cap of their holdings. That comes to $161.462 billion. That's even larger than BDJ, with an average market cap weighting of $102.6 billion. Considering that a company with any market cap over $10 billion is considered a large-cap stock, we can see that these funds, specifically BOE, really lean into some mega-cap stocks .

BOE's managers were less active in the last year as they reported 44% portfolio turnover, lower than the preceding two years, which were 65% and 61%. However, the years 2019 and 2018 were even quieter at turnover rates of 26% and 28%, respectively.

Geographically speaking, the fund hasn't changed its orientation to a large degree. U.S. exposure comes to around 47.6% of the fund's assets; our last update shows that it was 46.58% at the end of October 2022.

BOE Geographic Allocation (BlackRock)

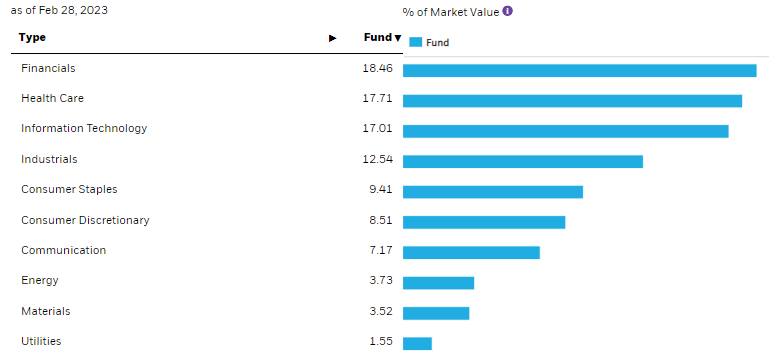

There has been a shift with BOE's tech exposure having been reduced. Similar to BDJ, we now see financials and healthcare command the top sector allocations. This is a shift when nearly 21% of the portfolio was allocated to tech in October. Not only October, but in our update before that as well, tech was also the largest weighting for the period ending June 2022.

{kind=link}

The late shift to more value-oriented sectors could have been what was costing the fund performance in 2022. Also, normal valuation fluctuations would have driven down tech exposure as they underperformed. As reflected with BDJ, if an investor only invested in BDJ, they might not have even known there was a bear market last year as they had only experienced a total performance drop of around 10% in October. That was when many other positions were dropping further into bear territory and reaching new lows.

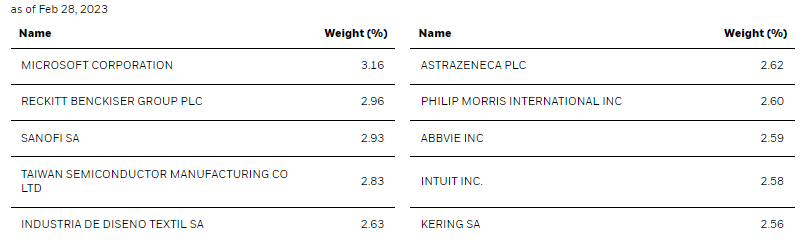

In the grand scheme of things, it wasn't a dramatic shift for the fund into financials and healthcare. All these sector weightings are almost equal at this point now. This is reflected in the fund's top ten, with several tech names but also a good mixture of healthcare names.

{kind=link}

We have Microsoft ( MSFT ), which has been one of the top holdings going for a while now. Sanofi ( SNY ), AstraZeneca ( AZN ) and AbbVie ( ABBV ) are also regular names that help represent the healthcare names.

We have Philip Morris International ( PM ) to balance the healthcare names. That's one of the newer positions in the top ten, not a new name to the portfolio, but a name they've increased exposure to in the last year. To start 2022 , they held 150,940 shares of PM. This was expanded to 189,817 by the end of 2022.

Relatively strong performance for PM in the last year also meant that the weighting would have been pushed higher relative to several of their other top holdings. While they are in opposite industries, tobacco is seen as a defensive play similar to healthcare due to regular and predictable cash flows. Similar to recessions having a relatively limited impact on healthcare operations, people won't give up their smokes so easily, either.

YCharts

Conclusion

The fund is currently trading at an attractive discount. While the fund regularly trades at an attractive discount, the latest is slightly below its longer-term average. Additionally, with an orientation of the portfolio tilted towards international investments, that could further add to what is seen as a relative discount to U.S. companies. Deeper discounts are always possible, but we see the discount closer to the bottom of the fund's range rather than the top. That could mean further discount widening in a significant way is potentially limited.

At this time, the fund's distribution still seems more than reasonable despite a challenging environment for equities, as it isn't at an elevated level on a NAV basis. That can provide predictable cash flows for an investor on a monthly basis. Risks could emerge to the payout should equities continue to struggle and reach new lows.

For further details see:

BOE: Discounted Global Covered Call Fund