MCN - BOE: Improving Finances Make This Covered Call CEF Worth Considering

2023-12-05 18:43:47 ET

Summary

- BlackRock Enhanced Global Dividend Trust is a closed-end fund that aims to provide income-seeking investors with upside exposure while writing covered calls against a portion of its equity holdings.

- The BOE closed-end fund offers diversification through exposure to foreign assets, which can help solve the problem of low international exposure for the average American investor.

- The fund's share price has declined slightly, but its total return has only underperformed the S&P 500 Index by thirty basis points since early July.

- The fund managed to correct the problem of insufficient distribution coverage that it had in 2022.

- The fund's shares are trading at a very large discount on net asset value.

BlackRock Enhanced Global Dividend Trust ( BOE ) is a closed-end fund, or CEF, that income-seeking investors can employ to meet their goals without being forced to completely give up the upside exposure inherent in a common equity investment. As is the case with most “enhanced” equity closed-end funds, this one seeks to achieve its goal by writing covered calls against a portion of its equity holdings. This fund is not as aggressive about the use of covered call options as some other funds with a similar strategy, however. It still manages to achieve a 7.64% yield, which is much better than either the American or most foreign equity indices, but admittedly it is not particularly competitive compared to what other closed-end funds manage to achieve. This is true even among those funds that employ a similar strategy. We can see that here:

| Fund |

| Current Distribution Yield |

| BlackRock Enhanced Global Dividend Trust |

| 7.64% |

| BlackRock Enhanced Equity Dividend Trust ( BDJ ) |

| 8.70% |

| BlackRock Enhanced Capital & Income Fund ( CII ) |

| 6.42% |

| Eaton Vance Enhanced Equity Income Fund ( EOI ) |

| 8.26% |

| Eaton Vance Enhanced Equity Income Fund II ( EOS ) |

| 7.56% |

| Madison Covered Call & Equity Strategy Fund ( MCN ) |

| 10.06% |

The fact that the BlackRock Enhanced Global Dividend Trust has a lower yield than many of its peers is something that might reduce its appeal in the eyes of those investors who are seeking to earn a very high level of income from the assets in their portfolios. However, it does have one advantage that the other funds on this list do not have. This is in its ability to provide diversification due to its exposure to foreign assets. As I have written about many times in the past, one of the biggest problems that the average American investor has is that their international exposure is not nearly as high as may be desired from a risk-management perspective. This fund can help to solve that problem.

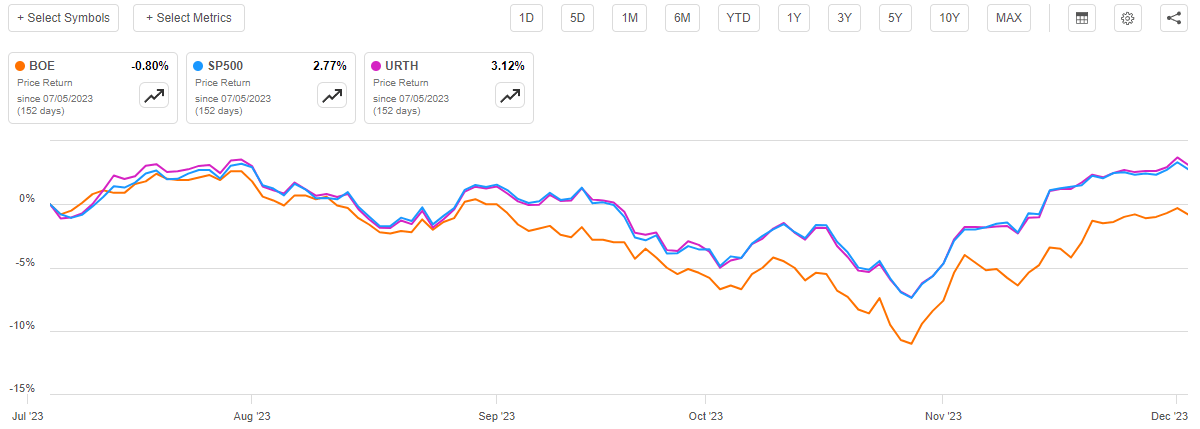

As regular readers may recall, we last discussed the BlackRock Enhanced Global Dividend Trust around the beginning of July. At that time, we concluded that the fund did bring a certain amount of diversity to a portfolio, but it seemed to be struggling to maintain its distribution. The market has seemingly not been particularly friendly to this fund since the time that the previous article was published. As we can see here, the fund’s share price has declined by 0.80% despite the fact that both the S&P 500 Index ( SP500 ) and the MSCI World Index ( URTH ) are up over the same period:

{kind=link}

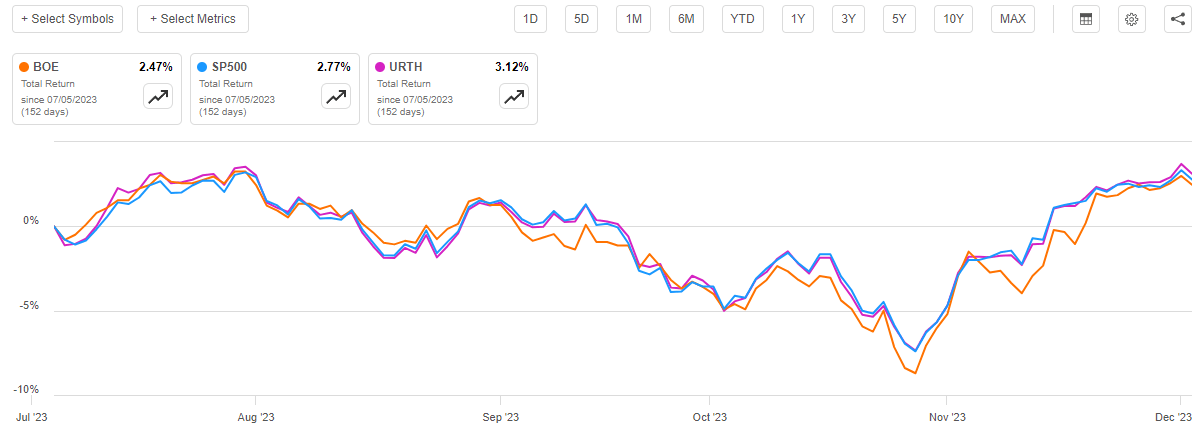

As I have noted in past articles though, share price performance is not necessarily the most important thing to consider with assets like this fund. This is because closed-end funds aim to maintain a relatively stable net asset value while paying out all of their investment gains to the shareholders in the form of distributions. As such, we should look at the total return that the fund’s shareholders actually received during the period. This is illustrated in this chart:

{kind=link}

This certainly presents a very stark difference between the fund’s share price and the return that investors actually received. As we can clearly see, investors in the BlackRock Enhanced Global Dividend Trust only underperformed the S&P 500 Index by thirty basis points since early July. This fund still underperformed the MSCI World Index too, but that is generally what we expect. After all, as was mentioned in my previous article on this fund, the fund’s strategy generally causes it to underperform during bull runs.

At this point, investors and readers might be wondering if it makes sense to add this fund to a portfolio today. After all, the market today is a very different one from what existed just a few months ago. Let us investigate in order to answer this question.

About The Fund

According to the fund’s website , the BlackRock Enhanced Global Dividend Trust has the primary objective of providing its investors with a very high level of current income and current gains. As mentioned in the introduction, the fund aims to achieve this strategy by investing in dividend-paying stocks from companies all around the world and writing call options against its assets in order to generate a synthetic dividend via the option premiums. The website describes the fund’s strategy thusly:

BlackRock Enhanced Global Dividend Trust’s primary investment objective is to provide current income and current gains, with a secondary investment objective of long-term capital appreciation. Under normal circumstances, the Fund invests at least 80% of its net assets in dividend-paying equity securities and at least 40% of its assets outside of the U.S. (unless market conditions are not deemed favorable by Fund management, in which case Fund would invest at least 30% of its assets outside of the U.S.). The Fund may invest in securities of any market capitalization, but intends to invest primarily in securities of large capitalization companies. The Fund generally intends to write covered put and call options with respect to approximately 30% to 45% of its total assets, although this percentage may vary from time to time with market conditions.

This fund is in many ways similar to the BlackRock Enhanced Equity Dividend Trust, which we discussed a few weeks ago. This can be found in the fact that both funds invest primarily in dividend-paying securities and write covered call options against the securities in the portfolio to generate premium income. BlackRock has a third fund that also employs a covered call-writing strategy, the BlackRock Enhanced Capital & Income Fund, but that fund tends to hold a lot more exposure to the mega-capitalization technology companies and similar firms that do not pay much in the way of dividends. If the comments on a few of my recent articles are any indication, many investors are trying to reduce their own exposure to these companies due to the fact that they now account for an outsized proportion of the major stock indices.

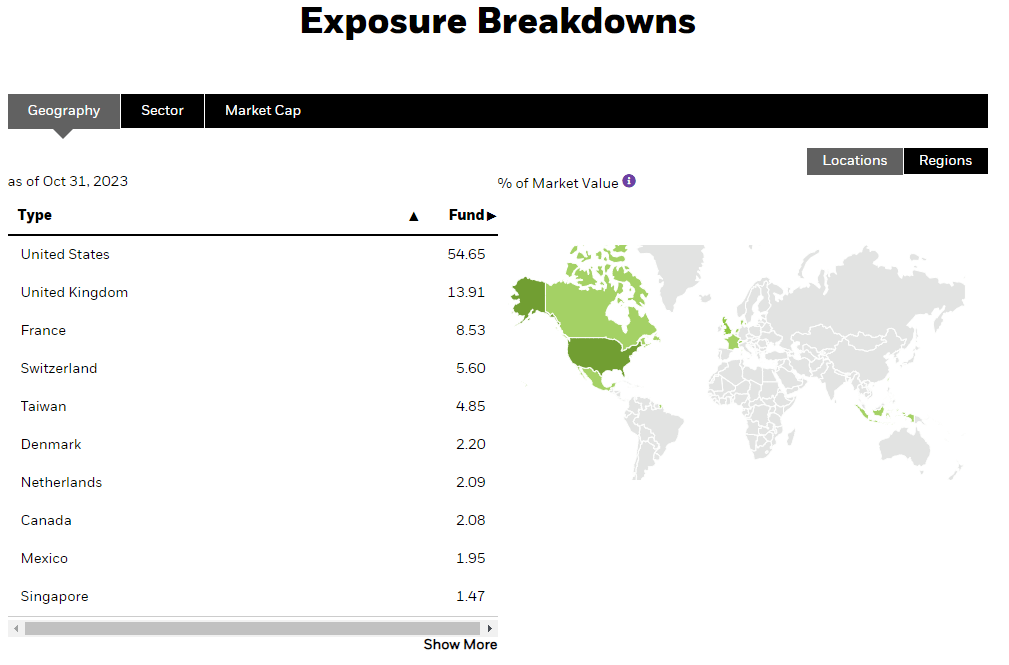

The fund’s description on its website states that the BlackRock Enhanced Global Dividend Trust invests at least 40% of its assets outside of the United States. The fund currently is sitting at a bit more than that. As of right now, only 54.65% of its assets are invested in the securities of American issuers:

{kind=link}

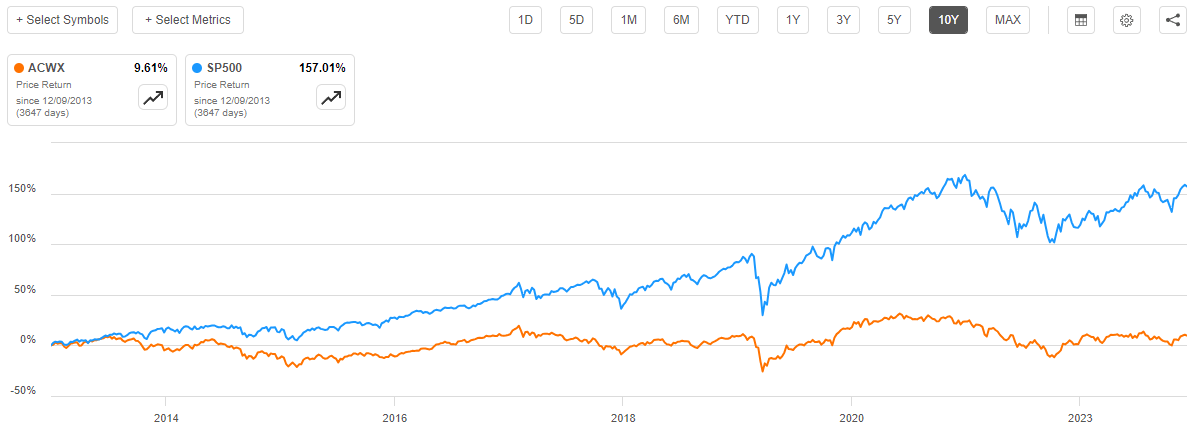

This clearly means that 45.35% of its assets are invested outside of the United States. This is a fairly high percentage of foreign assets for any global fund right now. After all, as of right now, the United States accounts for 69.85% of the MSCI World Index. It is something that is very nice to see though, due to the inherent fact that most American investors have an outsized proportion of their assets invested in the United States. This makes sense, as American stocks have significantly outperformed foreign ones over the past decade. For example, let us compare the trailing ten-year performance of the S&P 500 Index to the MSCI All-Country World ex-U.S. Index ( ACWX ):

{kind=link}

As we can see, when the United States is excluded from the data, the global stock market only appreciated by 9.61% over the past decade. That is substantially worse than the S&P 500 Index over the same period. As such, we can conclude that the United States has been responsible for the bulk of the global market gains over the past ten years. As such, unless an investor was actively diversifying away from the United States, they almost certainly have an outsized proportion of their total assets invested domestically. It is not difficult to see how this is a problem, especially for Americans. After all, most Americans live and work in the United States so any sort of domestic economic shock could affect both their income and their savings. If the investors were instead diversified all over the world, they might be able to avoid some of the adverse impacts of such an event.

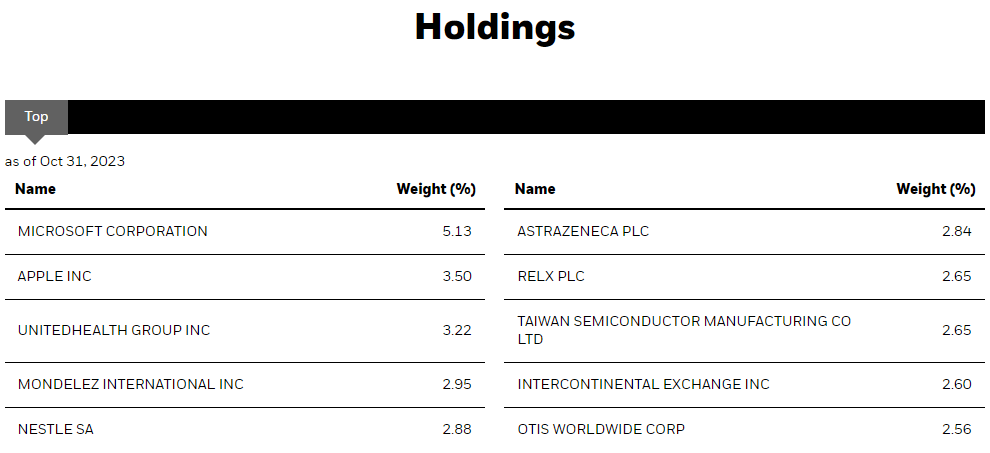

A look at the fund’s largest holdings supports the same conclusion about being invested internationally as the geographic exposure chart from the fund’s webpage. Here are the largest positions as of the time of writing:

{kind=link}

We do still see a number of American companies on this list, but some are foreign:

| Company |

| Home Country |

| Microsoft Corporation ( MSFT ) |

| United States |

| Apple Inc. ( AAPL ) |

| United States |

| UnitedHealth Group ( UNH ) |

| United States |

| Mondelez International ( MDLZ ) |

| United States |

| Nestle SA ( NSRGY ) |

| Switzerland |

| AstraZeneca ( AZN ) |

| United Kingdom |

| Relx ( RELX ) |

| United Kingdom |

| Taiwan Semiconductor Manufacturing ( TSM ) |

| Taiwan |

| Intercontinental Exchange ( ICE ) |

| United States |

| Otis Worldwide ( OTIS ) |

| United States |

There are still six American companies on the list, two of which are among the “Magnificent 7” stocks that many investors are trying to manage their exposure to. According to Goldman Sachs , Apple and Microsoft are both among the top five stocks that mutual funds are underweight relative to the index.

This fund is not really an exception to this, as Microsoft is 7.13% of the S&P 500 Index and Apple is 7.24% of the index. In the MSCI World Index, Apple is 5.13% of the total and Microsoft is 4.51% of the total index weighting. As such, this fund is underweight Apple relative to both indices, and it is underweight Microsoft relative to the S&P 500 Index but not to the MSCI World Index. This is something that investors may want to keep in mind prior to purchasing this fund, as it is possible that they may already have significant exposure to both of these stocks depending on what else is in their portfolio. There is a risk to having too much of a portfolio tied up directly or indirectly in only a few stocks so that risk needs to be considered before purchasing shares of this fund.

There have been a significant number of changes since the last time that we discussed this fund. For example, Reckitt Benckiser Group ( RBGPF ), Accenture ( ACN ), Sanofi ( SNY ), Paychex ( PAYX ), Philip Morris International ( PM ), and Diageo ( DEO ) have all been removed from their positions among the largest holdings in the fund. In their place, we have UnitedHealth Group, Mondelez International, Nestle, Relx, Intercontinental Exchange, and Otis Worldwide. We also see that the weightings of a few major holdings have changed, but this could be caused by one asset outperforming another on the market and is not necessarily the result of the fund actively trading stocks and changing its positions. Either way, we can clearly see that sufficient changes have been made to make the assumption that this fund has a relatively high annual turnover. However, this assumption is not really correct, as the fund’s 44.00% annual turnover is higher than many other equity closed-end funds. As I pointed out in the previous article on this fund:

“The reason that this matters is that it costs money to trade stocks or other assets, which is billed directly to the fund’s shareholders. This creates a drag on the fund’s performance and makes management’s job more difficult. After all, the fund’s managers need to generate sufficient returns to cover the added expenses and still have enough left over to appropriately reward the shareholders. This is a task that few management teams are able to accomplish on a regular basis, which is one reason that actively managed funds often fail to outperform their benchmark indices.”

As we saw in the introduction, the BlackRock Enhanced Global Dividend Trust has underperformed both the S&P 500 Index and the MSCI World Index over the past five months. This is exactly what we would expect from a covered call fund though, since the covered call strategy trades upside capital gains potential for an upfront premium. As such, during a strong bull market, the strategy will tend to underperform. However, it will outperform during flat or bear markets. We have seen both types of market over the past five months, although in aggregate the market was up slightly.

The fund was not quite able to match the gain, but it did better than might be expected. This is because this fund is only 42.73% overwritten, so it still has more than half the portfolio able to produce capital gains. As such, it is not capping its upside potential as much as some other funds that have higher options coverage. Investors who are overall bullish but want to reduce the volatility of the assets in their portfolios might appreciate this.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the BlackRock Enhanced Global Dividend Trust is to provide its investors with a very high level of current income and current gains. In order to accomplish this objective, the fund primarily invests in dividend-paying common stocks from around the world and then writes call options against them in order to generate income in the form of premiums.

These option premiums act as a sort of synthetic dividend and as I discussed in a recent article , the effective yield of these synthetic dividends can be incredibly high. The fund pools the premiums, the dividends that it receives, and any realized capital gains together into a pool of money that it then pays out to the shareholders, net of any capital gains. We can naturally expect that this should result in the fund’s shares having a fairly high yield.

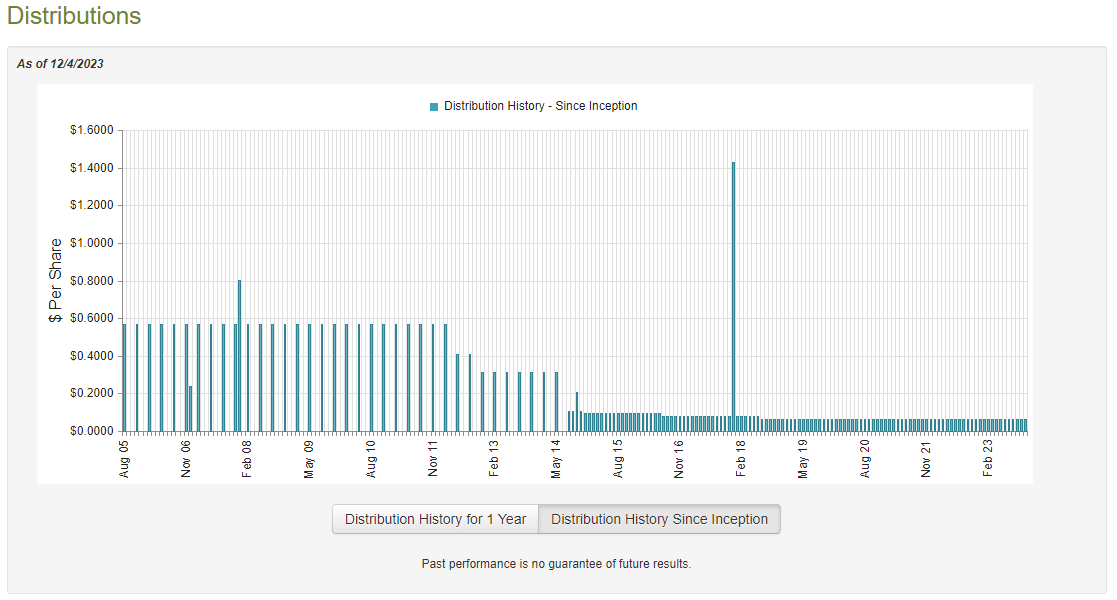

This is certainly the case, as the BlackRock Enhanced Global Dividend Trust currently pays a monthly distribution of $0.0630 per share ($0.7560 per share annually), which gives the fund a 7.64% yield at the current share price. As mentioned in the introduction, this is a bit lower than some other covered call funds possess, but it is not so low as to be unattractive. This is especially true considering that this is one of the few covered call funds that invests internationally. Unfortunately, the fund’s distribution has not been particularly consistent over the years. In fact, as we can see here, this fund has been very slowly reducing its distribution for nearly two decades:

{kind=link}

This is something that may prove to be a bit of a turn-off for those investors who are seeking to receive a safe and secure income from the assets in their portfolio. This is especially true today, since inflation still remains well above the 2% level that the Federal Reserve considers to be healthy, and this high inflation is rapidly increasing the price of all of the things that we need to buy on a daily basis. As such, we would prefer to have our incomes grow over time, not stay static or decline. With that said, as long as the fund can keep its distribution stable, it is possible to get a growing income by reinvesting a portion of the distribution that the fund pays out while using the rest as spending money. As such, the most important thing for us right now is to determine how well the fund can sustain its current distribution.

Fortunately, we have a relatively recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the six-month period that ended on June 30, 2023. This is a more recent document than the one that we had available to us the last time that we discussed this fund, which is quite nice to see. After all, that previous document is nearly a year old at this point and a lot has happened in the past year. The time period that is covered by this report gave us a fairly euphoric market that was aggressively bidding up asset prices in the expectation that the Federal Reserve would soon cut interest rates. While the majority of the capital gains were focused on the “Magnificent 7” technology stocks (see here ), the fund may have still had some potential to earn capital gains or options profits by taking advantage of the strong market. This report should give us a good idea of how well it managed to do.

During the six-month period, the BlackRock Enhanced Global Dividend Trust received $13,252,662 in dividends from the securities in its portfolio. We have to subtract out the money that the fund paid in foreign withholding taxes and add in a small amount of income from other sources. When we do that, we see that this fund had a total investment income of $12,305,917 during the period. It paid its expenses out of this amount, which left it with $9,102,764 available for shareholders.

As might be expected, this was nowhere near enough to cover the distributions that the fund paid out. During the six-month period, this fund paid a total of $23,663,713 to its shareholders. At first glance, this might be concerning as the fund is clearly failing to fully cover its distributions with its net investment income.

However, there are other methods through which the fund can obtain the money that it needs to cover the distributions. For example, the fund receives premiums from the call options that it writes against the stocks in the portfolio. This money is not considered to be investment income for tax purposes, but it clearly represents money coming into the fund that can be distributed. In addition, the fund might be able to realize capital gains when stock prices go up. This is also not considered to be investment income. The fund had quite a bit of success at these tasks during the period, as it reported net realized gains of $8,951,510 and had another $43,448,993 in net unrealized gains. Overall, the fund’s net assets increased by $32,797,677 after accounting for all inflows and outflows during the period. This is very nice to see as it clearly indicates that the fund did manage to cover its distributions during the period.

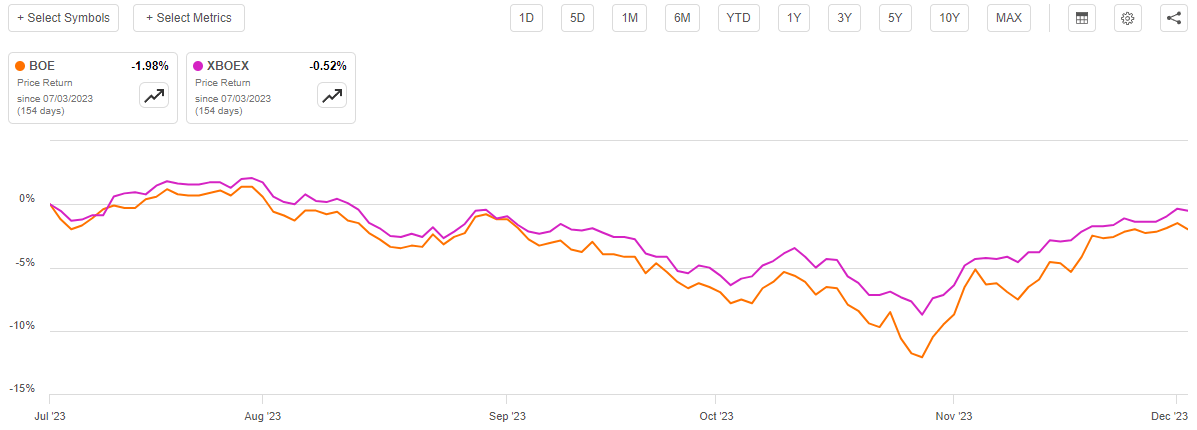

With that said, we can see that the fund’s net investment income and net realized gains together were not sufficient to cover the distributions that were paid out during the period. The fund was essentially forced to rely on net unrealized gains to fully cover the payout. As everyone reading this is well aware, unrealized gains can be erased by a market correction and we did have a market correction shortly after the period covered by this report. As such, it is not certain that the fund will be able to sustain its distribution going forward. As we can see here, the fund’s net asset value per share is down 0.52% since July 1, 2023:

{kind=link}

This suggests that the fund has not generated sufficient returns in the second half of 2023 to cover the distributions that it paid out since the end date of the most recent financial report. However, the fund’s net asset value per share is up 4.45% year-to-date so it appears that the excess returns that it generated in the first half of the year have been sufficient to carry it through thus far. Overall, this fund’s distribution should be fine as long as the current market strength remains intact. There is no guarantee that this will be the case, however.

Valuation

As of December 4, 2023 (the most recent date for which data is currently available), the BlackRock Enhanced Global Dividend Trust has a net asset value of $11.51 per share but the shares currently trade for $9.90 each. This gives the fund a 13.99% discount on net asset value at the current price. This is an enormous discount, but it is not as good as the 14.99% discount that the fund’s shares have had on average over the past month. However, as I have pointed out before, a double-digit discount is generally a very reasonable entry price for any fund, so the current price appears to be acceptable.

Conclusion

In conclusion, the BlackRock Enhanced Global Dividend Trust is one of the few closed-end funds that does a pretty good job of helping investors diversify their portfolios internationally. This is something that is especially important for American investors considering that many of them are substantially overweighted to the United States right now. This fund employs a covered call-writing strategy to reduce its volatility, which is important for those risk-averse investors who are dependent on their portfolios to provide the money that they need to pay their bills or finance their lifestyles. It appears that it also managed to fix the distribution coverage problem that we discussed earlier this year. Overall, this fund might be worth considering today.

For further details see:

BOE: Improving Finances Make This Covered Call CEF Worth Considering