ASML - Boeing: A New China Crisis

Summary

- Fresh tensions mounting between US and China shatters Boeing's hope on aircraft sales.

- The company has $7 billion worth of Boeing 737 MAX aircraft awaiting delivery to China.

- Boeing loses $14 billion in revenues annually due to missed China sales with a $575 billion sales potential.

- Boeing's addressable market is currently 20% smaller due to political tensions.

- While Boeing might be missing on revenues over the longer term, in the near term, it's not missing anything because it hasn't had significant sales to China for years.

Relations between China and the US has deteriorated further in recent days, and while the tension between the countries is nothing new, each step down in the relations between the super powers brings the world in an even more uncertain situation. In this report, I want to discuss how foreign relations between the US and China are affecting Boeing ( BA ) and the implications this has.

In order to get a complete picture, I will be discussing the importance of the Sino-American relationship including the relative strengths and weaknesses of the countries and how that translates to the aerospace industry and what Boeing is missing now and what they could very well be missing for the foreseeable future. I also will discuss why China in some way still heavily relies on Boeing products which at this time is one of two elements that could help restoring Boeing sales to China. This will be a data driven analysis, so where possible and relevant I will be sharing the data and graphs with you.

Two Super Powers: One Problem

{kind=link}

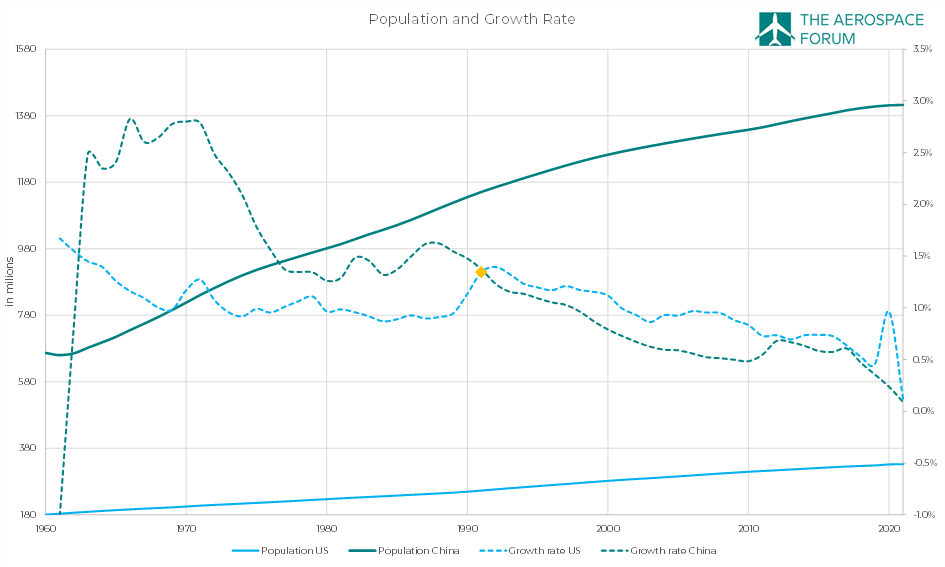

Population US and China (The Aerospace Forum)

When talking about the tension between China, we can go days, months, years or even decades back. As a starting point, I decided to use a graph of the US and China population and their respective growth rates since 1960. Ideally, I also show you how the demographics have developed but that would provide another variable that is hard to visualize over time. You might wonder why I would even bother showing you a graph of the population. The reason is quite simple: Economies are built upon various pillars and one of those pillars is the population which basically forms your domestic addressable market and to some extent determines your domestic production capacity. Combine that with natural resources a country holds, and you can see how energy requirements and energy policy is formed as well as trade requirements with a policy built around that.

Both countries have seen their population grow. The Chinese population grew by 117% since 1960 while the US population grew by 83%. If you would zoom in on the recent years, then we would see that the Chinese population is plateauing. This is visible in the growth rate represented by the dotted line in the figures. What we basically see is that since 1991 the growth rate for the US tops that of China but both countries saw their growth rates decline and since 1991 that growth rate is lower for China than it is for the US. In fact, in 2022 the Chinese population even declined driven by the pandemic and with population being one of the pillars of an economy that obviously creates concerns and develops friction especially between the No. 1 and No. 2 economies in the world which happen to be the US and China.

I wouldn’t say that China is having an imminent problem, but declining population growth is a concern. It's also the reason why China got rid of the one-child policy in 2016.

Switching To Economy

Just a very rough observation would be that with population growth declining, China has to look elsewhere for growth. So, trade and a strong geopolitical position is extremely important to them, which further amplifies the competitive stance of both economies. However, while the US has the better growth rate, China excels in one very important metric and that's the relative size of its middle class. The US middle class constitutes 50% of the population or around 166 million people, down from 61% in 1971. Looking at the absolute numbers, the middle class did still grow by 31%. The Chinese middle class grew from 3% or around 28 million people in 2000 to over 50% or more than 700 million people now. So, the growth of the Chinese middle class is simply more impressive.

{kind=link}

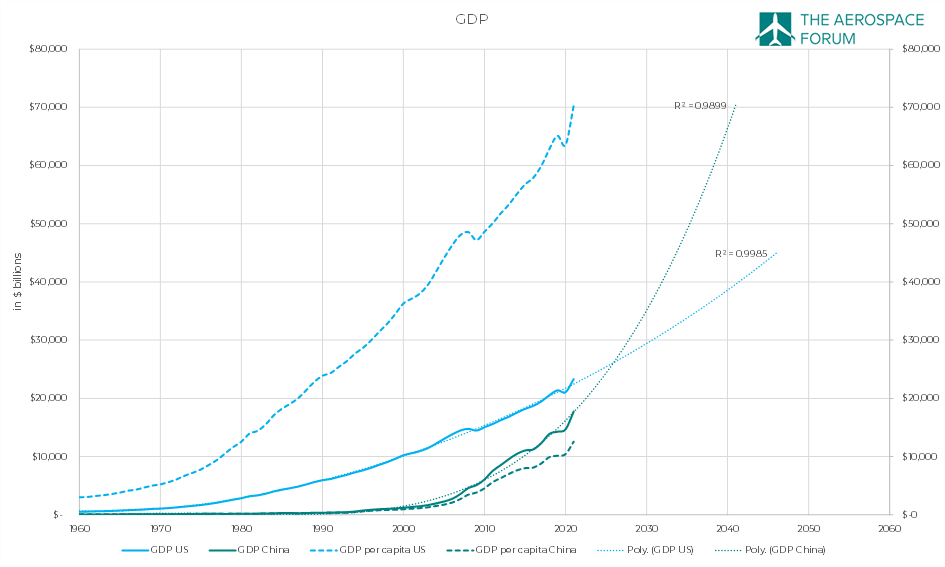

GDP US and China (The Aerospace Forum)

While China’s middle class is growing, its GDP per capita shown as the green dotted line and the right axis is much smaller than that of the US. The bigger problem for the US is that just following the trendline, it will lose its position as the world’s biggest economy, and over the long term any geopolitical advantages that come with that position. Just the trend as it's now would suggest that by 2025 that would already happen. Obviously, the reduced growth rate in population as well as growth rate reduction in GDP will delay that somewhat and the expectation is that China will overtake US as the world’s biggest economy by 2035. That explains very well why the previous White House administration as well as the current one are tough on China.

Whether China will overtake the US will be the case remains to be seen, because Japanese projections doubt whether the economic position swap will happen in the coming decades at all citing the zero-COVID policy and the trade tension with the US. While I do believe that the trade war between the US and China ultimately will have no winners, it does seem that there are institutions that believe that when it comes to preserving the spot as the No. 1 economy in the world the trade war might have had a positive impact. So, I discussed the population as well as the GDP now and we can already see why there is a lot of tension.

The Chinese American Dream

The next step is addressing why these countries grew so dependent on each other even though neither country likes to admit it. The national ethos of the US is The American Dream, based on a pillars of ideals including democracy, freedom, liberty and equality those who work hard would be able to climb the social ladder and be prosperous. A stark contrast with China. Technically, the American Dream should translate to a growing middle class and as I highlighted the middle class in the US has been declining.

To keep that dream alive, what happened is that the cost of that dream was pushed down. So, the costs of having a house, car, TV and a bunch of material things had to be brought down. That's where China comes into play. Many manufacturing jobs were transferred to China to bring costs of production down, which in some way should translate to the American Dream being available to more people not by promoting prosperity necessarily but by making the items associated to that dream more affordable. So, that's in a way the US did and does depend on China and it provided China with various things:

- Export to the US

- Knowledge in manufacturing

- A growing middle class

{kind=link}

US-China trade deficit (The Aerospace Forum)

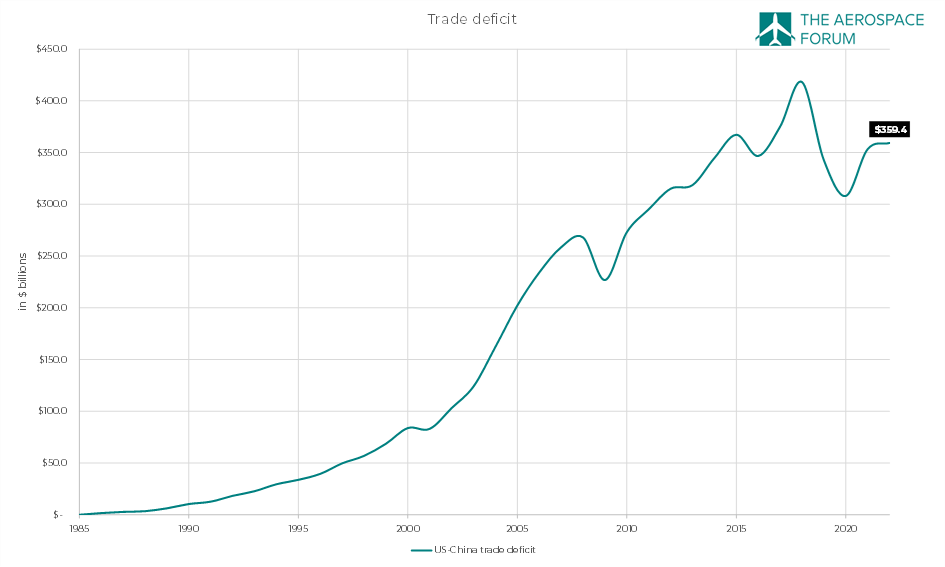

As China’s middle class also grows, so does their power on the world stage and they're actively leveraging that by allowing and denying access to their domestic market. With a growing middle class in China, the country also has a bigger group of people with money to keep happy and that becomes harder when economic growth is slowing, so in some way it's expected from the Chinese government they leverage their growing middle class to generate value in China for China.

In many cases, China is only willing to do business if over the longer term it helps them become self-sufficient. At the same time, the US is seeing the growth in China and the addressable market and with the US domestic market saturated China offers great potential that US corporations want to make use of. So, this is supposed to be a two-way street but the trade deficit shows that this is not really the case. Largely due to the pandemic the deficit eased somewhat, but we do see that while China has a huge addressable market for the US the deficit runs in the hundreds of billions of dollars.

This was reason enough for President Trump to engage in a trade war with China hoping for a deal that would keep US as the biggest economy in the world for a while longer. What was not quite taken into account was the reason why manufacturing was placed in China in the first place and that this in some way allowed the US to focus on more advanced manufacturing. Think about tech, but also aerospace.

Trade Deficit And Aerospace

{kind=link}

Boeing sales to China (The Aerospace Forum)

Up until this point, we have not yet addressed aerospace. So, where does aerospace feather into this? With prosperity in China growing, so does the demand for luxury items but also air travel. So, China offers a huge market opportunity for Boeing and Airbus as well. At the peak, data from The Aerospace Forum shows that direct deliveries to Chinese airlines (excluding deliveries to lessee deliveries to Chinese airlines) was $10 billion but the growth in value delivered in that one area where the US runs a trade surplus which also include aero engines was significant. In other words, aerospace is a key component of reducing the deficit or keeping it stable as a minimum.

{kind=link}

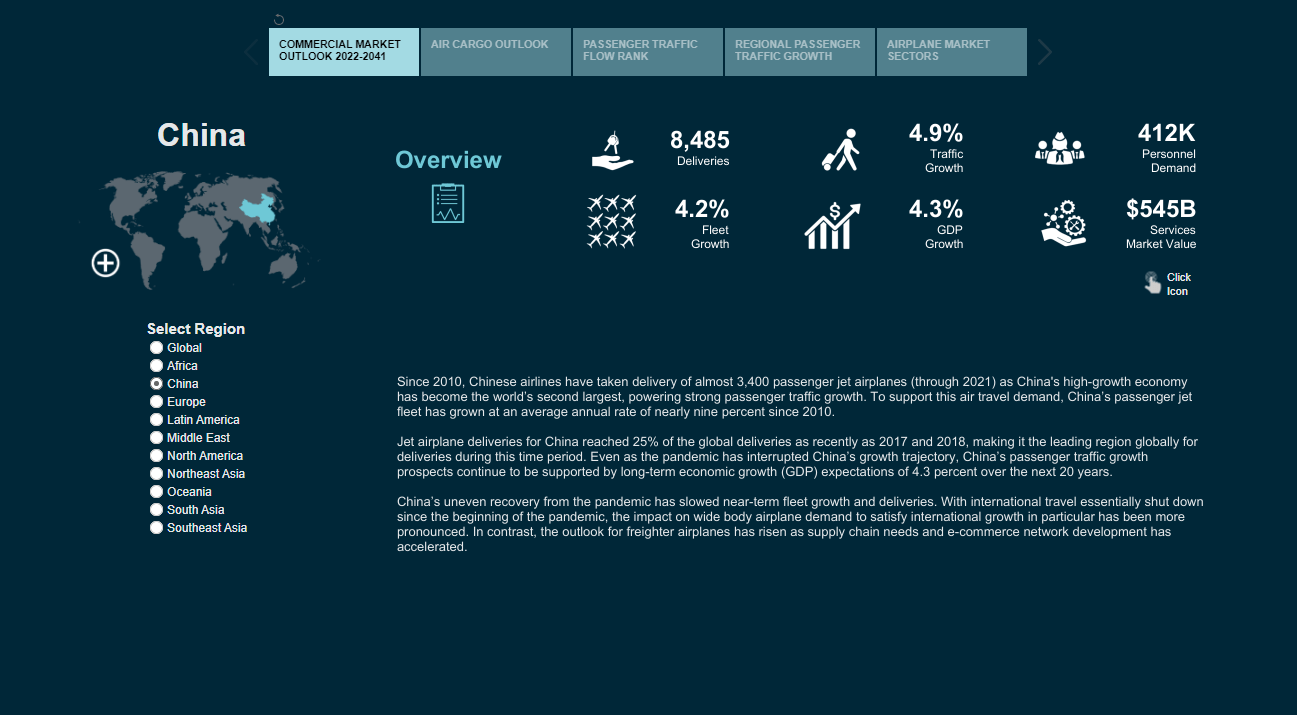

Boeing market outlook China (The Boeing Company)

Boeing has stopped providing dollar value estimates on the value of aircraft deliveries likely driven by the MAX crisis where Boeing appeared too focused on financials instead of delivering a solid engineering product. With nearly 8,500 aircraft expected to be delivered in the coming 20 years China makes up for one out every five deliveries. The Aerospace Forum estimates the value excluding regional jets to be around $575 billion over those 20 years or $28.75 billion annually. If we give Boeing a 40% market share, that would equate to $11.5 billion. So, while aerospace plays a key role in reducing the trade deficit looking at the 2018 delivery value of Boeing jets to Chinese airlines there does not seem to be a lot of upside.

That's where a trade deal could actually help Boeing significantly. With a trade surplus for commercial aircraft products, this is one of the areas where a deal would explore increased sales likely at the expense of Airbus ( EADSF ). With the relation between China and the US having been tough for years, also under the Presidency of Barack Obama who sought increased influence around the South Chinese Sea, Airbus seemingly benefited more from filling the demand for aircraft among Chinese airlines. However, my data shows that in 2018 Boeing still accounted for 60% of the delivered value. With the US-China relation becoming sour, more orders started flowing Airbus’ way and having an assembly line in Tianjin obviously helps. It's also the reason why Boeing opened a completion center in China in 2016. Both companies know that in order to get orders they will have to give something in return that can help their industry.

Either way, driven by the Boeing 737 MAX and Boeing 787 crisis at first and the pandemic later on, demand for aircraft imploded.

China Is Tough On The Boeing 737 MAX

Putting it all together, China and the US are colliding in various areas as both countries battle to become or remain the No. 1 economy in the world. The interests are big. Former President Trump recognized this and initiated a trade war. One can question how effective that trade war really was, but President Biden did not provide a reset also recognizing the threat China poses to its position as the No. 1 economy in the world as well as the geopolitical power and influence that comes with it. China was supposed to expand US purchases by $200 billion over 2 years as part of the Phase One trade deal signed in January 2020.

However, the pandemic did not help China sticking to the trade agreement as consumer behavior changed globally. Once the pandemic hit, there never really was a chance for the trade agreement to come to fruition. During the pandemic, China continued accepting $14 billion worth of Airbus aircraft over three years even though demand for aircraft was pretty much non-existent due to China’s zero-COVID policy. Boeing’s deliveries to China were valued at less than $900 million over the same three years in which Airbus generated $14 billion in revenues from China. The tension between the US and China was part of the problem. The other problem was the grounding of the Boeing 737 MAX and the delivery stop of the Boeing 787, which are the key products for the Chinese market.

{kind=link}

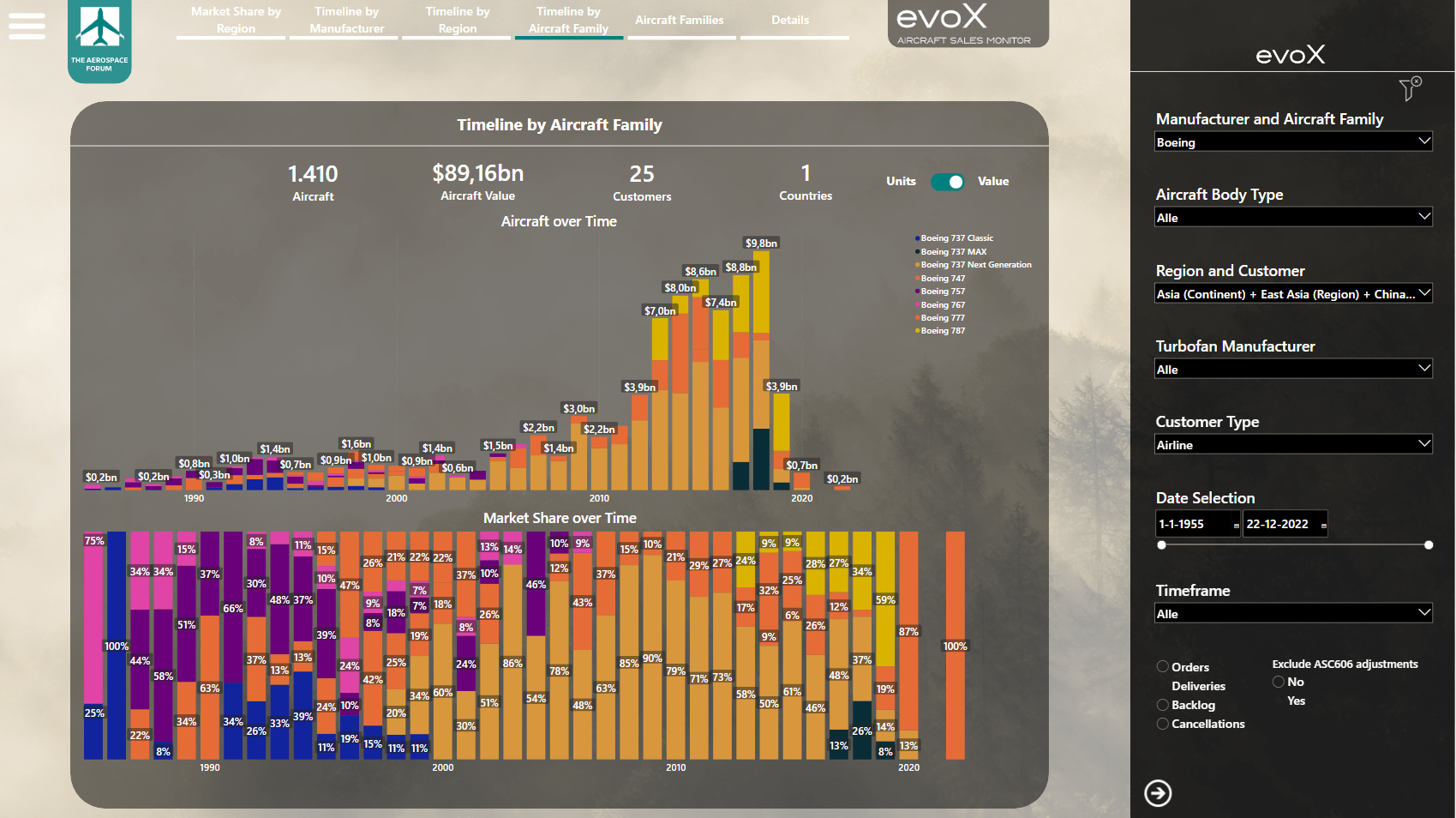

Boeing sales to China by aircraft family (The Aerospace Forum)

An overview of the deliveries from Boeing directly to Chinese airlines shows that depending on the year up to 97% of the delivery value was generated by the Boeing 737 and Boeing 787. So, naturally with those programs suffering problems even if China was willing to take deliveries Boeing had no product it could deliver for some time. China, however, was particularly tough on the Boeing 737 MAX, which was made part of the tension and the country’s own aspirations to become a big aircraft manufacturer.

On China’s dealings with the Boeing 737 MAX, I can probably write an entire book highlighting how a combination of circumstances led to China’s tough stance on the Boeing 737 MAX. Following trade tension between the US and China, the country was quick to ground the Boeing 737 MAX after the second crash with the MAX in March 2019. That decision was not wrong, but what became clear is that with demand for air travel eroded in China for a prolonged period of time due to COVID-19 a recertification of the MAX in China would not come close any time soon. With no demand for the jet, China set itself the target of delaying recertification of the Boeing 737 MAX until its own C919 was certified.

By 2021, the Boeing 737 MAX was allowed back in the skies of many countries, but not in China. From the perspective of air travel demand, China did not need the Boeing 737 MAX and the airplane had value in the geopolitical tension between the US and China. While a Phase One agreement was reached in January 2020, the relation between the US and China had further soured. President Trump had called COVID a "Chinese virus" in March 2020, and heavily criticized China, which obviously did not help the relation between the two super powers . In the same year Trump pulled through on revoking US special treatment of Hong Kong, and while many may have had hopes that things would change under President Biden, the opposite is true. Things got worse. Biden did not revert the preferential treatment of Hong Kong due to the Chinese influence on Hong Kong, and the March 2018 US-China talks in Alaska also called the Anchorage meetings a miserable failure. The talks were intended to improve the relations between the two countries but the opposite happened and the talks eventually were rather hostile than constructive.

By September 2021, the US expressed frustrations over the Chinese government allegedly blocking a sale of Boeing aircraft to China. Such a sale could narrow the trade deficit somewhat. By December 2021, the Chinese regulator had paved the way for the Boeing 737 MAX to return to service in China. However, there was no indication when that would happen, and given the tough relations with the US and the pandemic China was not in a hurry to put the Boeing 737 MAX back in service.

{kind=link}

The Boeing Company

What certainly did not help the MAX getting back any time soon in China was Pelosi’s visit to Taiwan in August 2022. The visit followed a month after China announced an airplane order for nearly 300 Airbus jets, clearly putting on display what the US and Boeing is missing out on due to the elevated tensions. Recognizing that the visit to Taiwan had not done anything good to Boeing’s chances to deliver the 138 Boeing 737 MAX aircraft that Boeing had already built for Chinese customers, Boeing made a bold move to pressure China as it started remarketing those jets. With demand for aircraft increasing and supply capability falling short of demand, there was a strong case for reselling the jets. Simultaneously, it sent a strong signal to the Chinese government that stalling recertification would eventually leave them without Boeing 737 MAX aircraft available on short notice even if they would need them. It was one of the elements that contributed to a Chinese rethink on their stance on the MAX, even more so with demand revival in mind and the C919 certified.

In November 2022, following protests from the Chinese population against the zero-COVID policy that had strangled the country for years, a quick reopening started spurring a surge of demand for air travel. The first Boeing 737 MAX quietly re-entered service in China some months later, indicating that the type had been certified to return to service. With demand recovering, China simply could no longer allow itself to keep the Boeing 737 MAX hostage of the geopolitical tension between two global superpowers.

Hopes Fade For Boeing As Quickly As They Came

During the fourth quarter earnings call in January, Boeing shared that it had paused the remarketing of Chinese jets which was the clearest sign of hope that Boeing could soon recommence deliveries to China. Obviously, the first step would be to get all Boeing 737 MAX jets already delivered to China back in the air, but the pause on the remarketing effort also showed significant hope on a resumption of deliveries which would be accretive to Boeing’s ability to recovery the balance sheet. Demand for single aisle jets is significant. Boeing projects demand for almost 31,000 single aisle jets in the coming 20 years of which 6,370 aircraft are destined for China. That hopes on a delivery resumption were high is not odd. Recovery of air travel in China would increase demand for jets as we saw happening in other parts of the world once COVID-19 restrictions were eased in, and in the five years before the Boeing 737 MAX crisis, China accounted for 23% of all Boeing 737 deliveries according to data from the evoX Aircraft Sales Monitor .

The airframer recently announced the opening of a new assembly line which will be operational in the second half of 2024 and could push Boeing’s single aisle production capacity beyond 80 aircraft per month. Hopes to one day facilitate sales to China likely played a role in the decision as well.

Prior to the ceremony for the delivery of the final Boeing 747, Boeing CEO David Calhoun gave an interview to Bloomberg TV discussing the hope that a sales pipeline in China could be developed. That was before the US and Canada shared that they were tracking a balloon that was believed to be from China. In response to the sighting, Secretary of State Blinken canceled his diplomatic visit to Beijing and just like that the hope of normalization floated away from Boeing as the visit was seen as a pivotal moment for Boeing to recover the delivery stream and for an opening of aircraft sales to China as commercial aircraft products are one of the key areas that can be leveraged to balance trade between the two countries.

So, what we're seeing is that each time Boeing seems to be getting closer to a delivery resumption, the geopolitical tension plays up as one of the parties throws a spanner in the works. While some progress has been booked with the Boeing 737 MAX in China, there are only very small steps that seemingly aim for the US to drop the harsh stance toward China. That stance has shifted more from trade to technology as the US has actively been seeking for the Dutch government to limit exports of advanced chip manufacturing tools from ASML ( ASML ) to China.

What's Next For Boeing?

{kind=link}

Luchtvaartnieuws

The game of cat and mouse that has been going on for years between China and the US and intensified more in recent days could not come at a worse moment for Boeing. Obviously, the big question is what is next for Boeing. I'm convinced that the decision to open a fourth line in Everett will not be impacted by the current situation between China and the US. Obviously, absent of sales opportunities on the longer term Boeing is losing a significant part as an addressable market, but I don’t see why that would impact recent decisions to open a fourth production line for the Boeing 737 MAX because the need for it has been clear for years. A fourth line also will create an opportunity for Boeing to stabilize production and hike production rates without the pressure hiking on three lines would normally bring.

Actually we don’t even know whether there's going to be any adverse impact for Boeing, but if the past years of tension are a gauge for the path forward then things are not looking good for a return to delivery for Boeing in China. In fact, I believe that hopes are fully reset at this point from Boeing’s side with the only hope on some movement being demand for the aircraft and not so much any easing in tensions between the US and China. I expect Boeing to provide some comment on it in its next earnings call, but a first step could once again become remarketing the $7 billion worth of aircraft destined for China.

Beyond the Boeing 737 MAX, we also have to look at the Dreamliner. In the past Boeing dialed production back due to lackluster sales to China. Around 10% of the Dreamliners are delivered to China and Boeing is aiming to return to a rate of ten aircraft per month by 2025-2026. The big question now of course is whether Chinese sales will be filling some of those slots.

For Boeing, billions of dollars are at stake and while there was some optimism in recent weeks it is not looking good for a recapture of the market in the near term, and the way things stand now, I would not be surprised if Boeing reverted to a delivery vision that does not include China for the foreseeable future at the rates that the company grew accustomed to.

In the near term, besides the change in mindset regarding sales opportunities to China I don’t see dramatic changes for Boeing or any of its suppliers, most prominently Spirit AeroSystems. The reason is that demand for aircraft from customers excluding the Chinese ones is robust and Boeing deliveries to China have not been of significance in recent years. In fact, Boeing current performance showcases pressures from supply chain keeping the company down and sales to China already are low. In 2022, deliveries to China airlines accounted for just 0.25% of the revenues. So, Boeing is not losing much in the near term relative to its current revenue generation from China on aircraft deliveries. At this point I view deliveries to China as a remote opportunity rather than a near-term certainty.

Long term the potential loss of sales is significant. Using the 2018 revenue generation I estimated $9.8 billion in sales to Chinese airlines. If you add Chinese lessor sales and services, sales were around $13.8 billion accounting for around 13.5% of the revenues. Those revenues at current standing are not coming back and new business generated from any demand increases as well as sales to balance trade are also not materializing. So, Boeing already does not have those sales now but long term it will could them up to $14 billion annually.

China Is Putting Its Own Aspirations At Stake

{kind=link}

COMAC

At the start of this report, I addressed the population of China and the US and from there drilled down to the economies of both countries and highlighted the growing middle class in China both in absolute and relative terms. So, the opportunity is big and I valued it at $575 billion over the long term and the way it stands now Boeing will not be able to capture that market at least not when looking at the geopolitical tension.

However, eventually China might be hurting itself in the long term as well. As I mentioned earlier, China allows foreign companies to its market if it has some long term benefit as well for them. As the economy grows and the commercial aircraft potential is huge in China, the interest to start supply that market with an own product has also grown. That's why China has developed the COMAC C919 which competes with the Boeing 737 MAX and the Airbus A320neo family. Supply chains for aerospace are more globally oriented than ever and only with a long history in aerospace, good international relations and a big aerospace footprint, countries have a chance of making a viable commercial aerospace product. In some sense, having the spot as the No. 1 economy in the world helps you establish better relations that could translate into aircraft sales. China does not have that position yet, but it might some here in the coming one or two decades.

However, while the country is the industrial zone of the world it does not have a commercial aircraft manufacturing that can really measure itself with Europe or the US. The reason is quite simple, it does not have history and decades of experience manufacturing jets. Boeing for example does and while wars are not fun, it are wars that make technological advancement, insights and innovation thrive and that has happened for Boeing.

As a small example, due to World War II the aerospace industry became familiar with survival bias. To reduce bomber losses aircraft were inspected upon return to improve the design. Bullets hole were visible in the aircraft and, naturally, one would say that in order to improve the bomber losses one should reinforce the areas where bullets had penetrated the aircraft skin. It was Abraham Wald, a mathematician, who did not follow that line of thought and said “well these aircraft with bullet holes did return, so while there is damage it are not critical damages preventing the bomber from returning safely. So, instead the parts that do not have damage should be reinforced, because aircraft that do have damage in those areas have suffered critical damage and were not able to return home to be inspected." It's are lessons like those that the industry learns in decades and has compounded that China does not have. China does not have to learn the lesson again but it can learn on the shoulders of giants namely Boeing and Airbus and it did. Airbus opened a production line in Tianjin in 2008 and, to capture sales, Boeing opened a completion center in Zhoushan in 2016. Lessons learned and chains created around those two facilities without doubt help the aircraft manufacturing industry in China that it will leverage and is leveraging for its own aspirations to produce commercial aircraft. Pushing Boeing down in China due to trade tension also means that it's delaying the development of the industry in China.

The C919 is seen as a Chinese aircraft and it's indeed manufacturer by China, but its share of foreign components is huge and that also means that in an escalation with the US, the US can halt the export of US components and urge other countries to do the same and it will without doubt bring the entire commercial aircraft manufacturing industry to an almost complete standstill in China. Beyond that risk and that of the mutual dependence on trade, there are over 1,250 Boeing aircraft in the fleets of the three biggest airline groups in China namely Air China ( AIRYY ), China Eastern Airlines ( CHEAF ) and China Southern Airlines ( CHKIF ). So, in the end, China needs the US as much as the US needs China. China nor Airbus can replace those 1,250 jets in the coming years and then there is the complexity of having to retrain pilots if you do replace Boeing aircraft with aircraft from other manufacturers as well. Also, for services and spare parts, there's dependence on Boeing to keep those aircraft serviceable over the longer term.

Conclusion: Boeing Stock A Buy With Or Without China

Aerospace is involved in a lot of things and it can be seen as an extension of geopolitical positions and enhancing that position. Over the past few days, hopes for a delivery resumption to China have quickly faded for Boeing. A visit from Secretary of State Blinken was seen as a positive pivot for sales to China to resume and a sales pipeline to develop which could help both countries balancing trade. That visit has been canceled and instead of seeing developments that are positive for Boeing, we're seeing developments that are harming Boeing’s business. Returning to normalization would ultimately bring around $14 billion in revenues to Boeing from China and those sales are currently extremely unlikely to materialize unless there either is demand from that for China or relations between the superpowers improve for which we have no indication at all. Neither party is acting constructively and in the end that is hurting the US aircraft manufacturing industry.

For Boeing, in the long term and absent of normalization this would mean that the addressable market is some 20% smaller equating to hundreds of billions of dollars in sales. Nevertheless, I do believe Boeing shares remain a buy as the company has gone without sales to China for some time now, and even absent of those sales the company is positioned to significantly reduce it net debt. Besides that, what remains is that Airbus and COMAC cannot service the aircraft demand for China, so if the country wants to keep a thriving airline and travel industry at some point they have to consider getting back to Boeing for the jets.

For further details see:

Boeing: A New China Crisis