BA - Boeing: This Is A Buy-The-Drop Situation (Rating Upgrade)

2023-09-22 12:12:28 ET

Summary

- The Boeing Company's Commercial Market Outlook projects strong demand for new aircraft until FY 2042, indicating incremental revenue and FCF growth potential for the company.

- The global aircraft fleet is expected to about double in size over the next two decades, driven by fleet expansions and upgrades by airlines.

- Air cargo is another source of growth for Boeing, with increasing demand from logistics providers for aircraft capacity.

- Boeing has a valuation advantage compared to Airbus, based off of free cash flow.

Shares of The Boeing Company ( BA ) are in the midst of a month-long consolidation that puts investors looking for an attractive long-term investment into a unique position. According to Boeing’s latest Commercial Market Outlook, the airline industry is set to see strong demand for new aircraft over the next two decades, which should translate to robust revenue and earnings tailwinds for the aircraft manufacturer. Boeing is a free cash flow-profitable manufacturing company, and it faces favorable demand projections. Considering that shares are currently in a consolidation pattern, I believe investors are faced with a unique buy-the-drop situation!

Previous rating

I previously rated Boeing a hold -- Wait For A Drop Before Buying -- due to the fact that the airline industry as a whole was set to profit from a return of airline passengers after the pandemic. A post-COVID normalization in air travel as well as successful restructuring measures translated into a favorable risk profile for Boeing. However, the valuation was not as attractive. Most recently, Boeing projected enormous, multi-decade growth in the airline industry, both for passenger and cargo planes. Given the improved outlook, I believe shares of Boeing are worthy of a second look.

Boeing’s Commercial Market Outlook

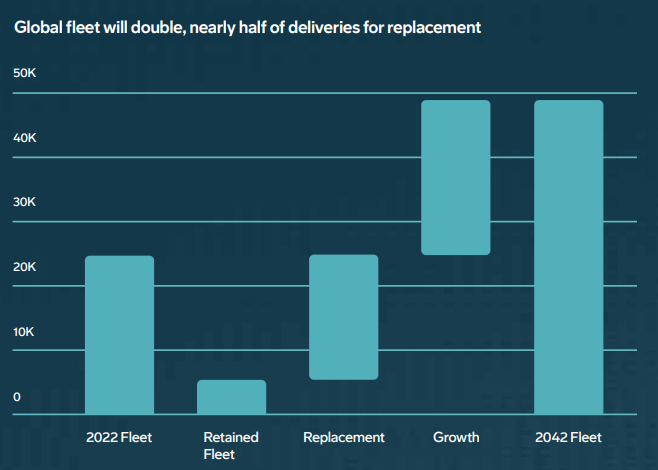

Boeing publishes its Commercial Market Outlook annually, which provides analysts and investors with insights into the company’s projections for long term aircraft demand. Boeing’s Commercial Market Outlook, covering the period 2023-2042, projects that the global aircraft fleet will about double in size over the next two decades (with FY 2022 being the base year). The biggest driver of this growth will be the expansion of aircraft fleets.

Airlines are set to upgrade their aging fleets and invest billions of dollars into buying newer, larger and more fuel-efficient models to transport passengers as well as cargo from point A to point B. Boeing also increased its forecast for aircraft demand coming from China which is expected to total 8,560 new commercial airplanes by 2042. China alone is expected to account for approximately 20% of global aircraft demand until FY 2042.

Source: Boeing Commercial Market Outlook

{kind=link}

Growth driver: air cargo

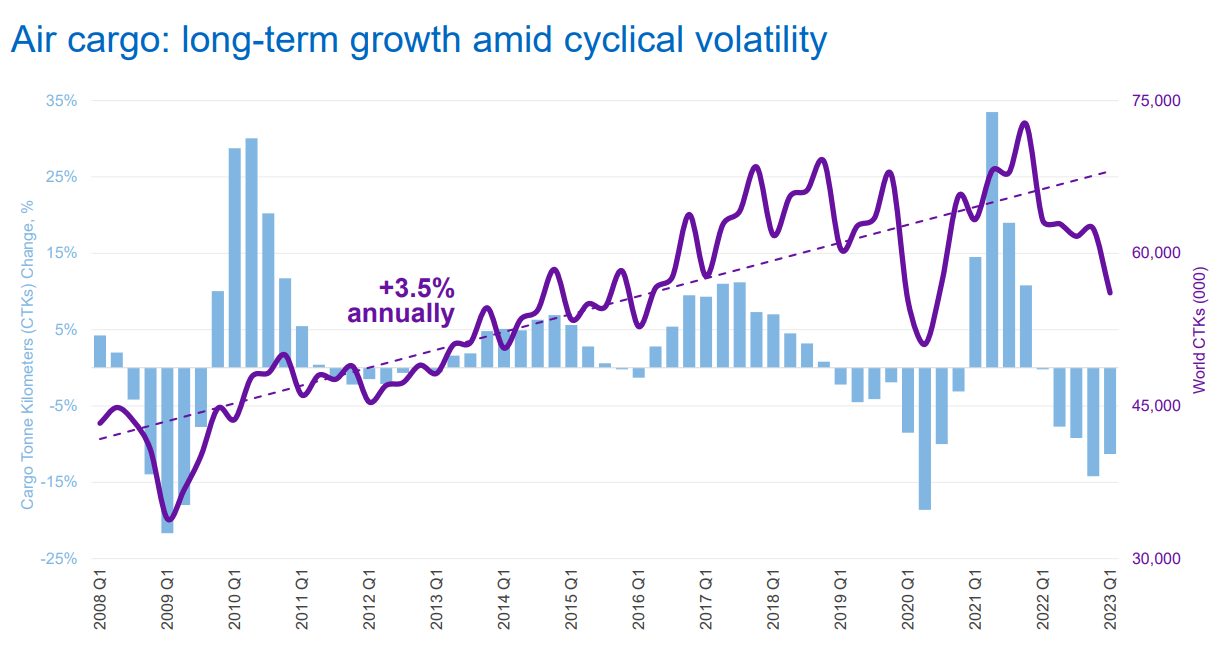

A return of passenger travel after the pandemic is not the only source of growth for aircraft manufacturers like Boeing. Cargo freight is another industry that demands growing capacity. In the long term, air cargo has proven to be highly cyclical (as has passenger air travel), but the trend line is upward sloping and indicates growing demand from logistics providers that deliver parcels internationally. Boeing has said that the demand for cargo freighters is chiefly driven by sectors such as e-Commerce as well as growing supply chain networks.

{kind=link}

Boeing now achieves positive free cash flow and impressive margins

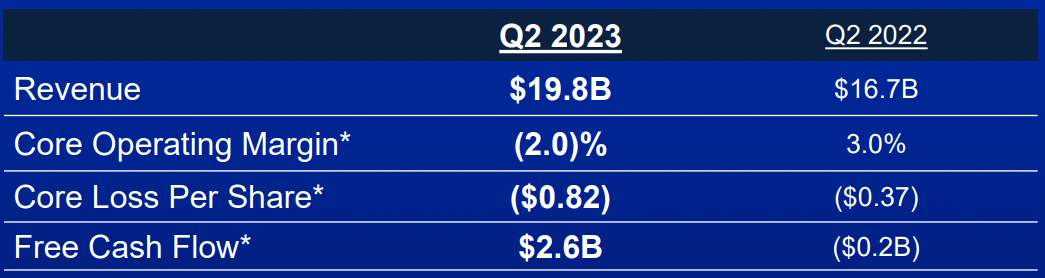

Boeing burned through a lot of cash during the pandemic and only recently achieved the milestone of reporting positive free cash flow. In the second-quarter, Boeing reported $2.6B in free cash flow on $19.6B in revenues… which calculates to an impressive free cash flow margin of 13%.

Given that Boeing issued a very strong demand outlook for the aircraft industry, I see potential for the company to improve its free cash flow margins going forward as well. For context, Boeing lost $20B in free cash flow in FY 2020, but the firm has since seen a gradual recovery as flight restrictions related to the COVID-19 pandemic were lifted. In FY 2021, Boeing lost $4B in free cash flow which was followed by a $2.3B free cash flow gain in FY 2022.

{kind=link}

Confirmed free cash flow guidance for FY 2024

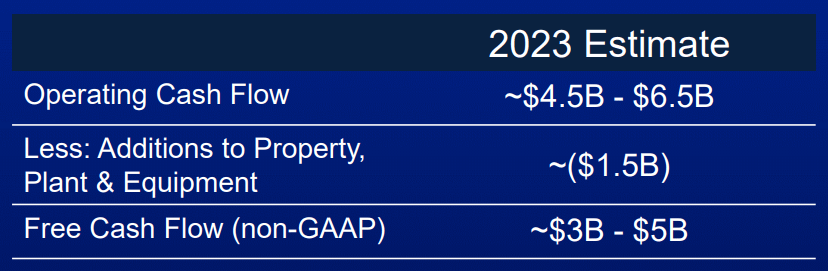

That the market situation for Boeing is improving could be seen in the firm's free cash flow outlook Boeing submitted earlier this year. In the second-quarter, Boeing confirmed that it expects to see $3-5B in free cash flow in FY 2023 which would, in the high-case, represent a 117% year-over-year increase. In the low-case of $3B in free cash flow, the year-over-year growth would still be a respectable 30%. The strong free cash flow recovery is driven chiefly by accelerating order and delivery growth for Boeing's 737s and 787s.

{kind=link}

Boeing's valuation compared against its biggest rival

Boeing is currently trading at a P/FCF ratio of 15.3X. For context, Airbus ( EADSF ), Boeing’s most formidable direct rival in the aircraft making business, is trading at a free cash flow multiplier factor of 26.0X. Boeing might therefore not be a complete bargain, but it clearly has a valuation advantage compared to its biggest competitor in the industry.

Given the strong demand outlook that Boeing recently presented, I believe Boeing could trade at 20X FCF. A 20X free cash flow multiplier factor implies that Boeing could have a fair value closer to $260, implying 30% revaluation potential.

Risks with Boeing

What I don’t like about Boeing is that the company is subjected to cyclical aircraft order patterns from the airline industry. Typically, airline companies place orders with Boeing or Airbus if they believe that future demand is going to lead to high aircraft utilization. With a recession potentially on the horizon, a drop-off in new aircraft orders would be a negative short term development for Boeing. Events such as COVID-19 and other pandemics also have the potential to fundamentally disrupt Boeing’s manufacturing operations as well as free cash flow outlook.

Final thoughts

The Boeing Company is in a buy-the-drop situation, in my opinion. Shares of the aircraft manufacturer have dropped 18% from their 1-year high and Boeing’s fundamentals (demand outlook, return of passenger travel and long term growth in the air cargo industry) have further improved lately and increasingly support a bullish long term investment presentation for Boeing. The aircraft maker is also free cash flow positive and generated more FCF in the second-quarter than it did in the entire 2022 fiscal year. Additionally, I believe Boeing, from a valuation point of view, is making a stronger value proposition than it did two months ago!

For further details see:

Boeing: This Is A Buy-The-Drop Situation (Rating Upgrade)