BCC - Boise Cascade Company Is A Hold For Long-Term Value Seekers

2023-11-03 17:20:53 ET

Summary

- Boise Cascade has favorable long-term value drivers, including demographic advantages and low housing inventory.

- BCC faces challenges in Q4 due to uncertainty in the US economic growth outlook and rigid interest rate environment.

- The company's inventory management strategy, dividend payment, and share repurchase program demonstrate confidence in its finances.

BCC's Stability Is The Key

Boise Cascade Company (BCC), which deals in wood products and building material distribution in the US and Canada, likely has a few hiccups before it attains a more stable growth path. The uncertainty over the US economic growth outlook and a rigid interest rate environment will likely keep its topline and margin depressed in Q4. However, the long-term drivers, including favorable demographics and housing inventory drawdown, have sufficient juice to push the company toward a recovery in my view.

BCC's inventory management strategy should also help keep the cash flow under control, to a certain extent. I believe the company's dividend payment and share repurchase program also reaffirm its confidence in its finances. The stock is reasonably valued compared to its peers, with a tilt toward stock price appreciation over the medium term. I consider the stock a "hold" for the medium-to-long term.

Business In Brief

Boise Cascade's Wood Products operation has five EWP (Engineered Wood Products) facilities, eleven plywood/veneer plants, and two sawmills. Used primarily for single-family construction, it seeks to extend EWP products to multi-family and light commercial construction. BCC's EWP products have longer lengths than traditional lumber materials and have lower labor and installation costs. It also offers engineering support like 3D structural modeling and detailed project planning.

The company's Building Materials Distribution (or BMD) operation has 38 warehouse centers and one truss plant. BMD's advantages include bundling floor-to-roof products with nationwide distribution capabilities.

Assessing The Industry Drivers

BCC's Investor Presentation October 2023

{kind=link}

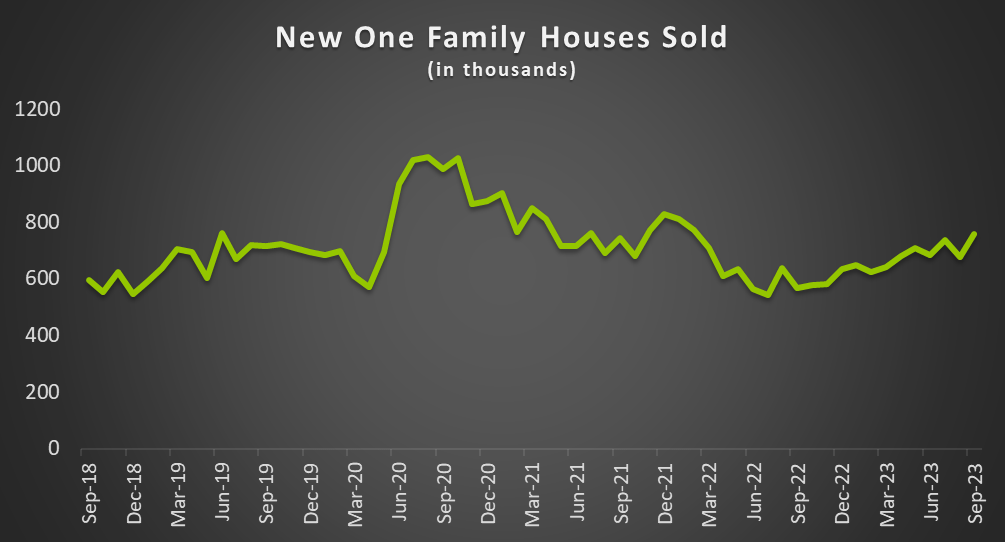

In Q3, US housing sales dropped by 6% compared to a year ago. As interest rates increased, housing affordability adversely affected consumers in 2023. Higher interest rates led to higher mortgage rates, while home prices were resilient. Not everything was uphill, though. The sales of new one-family houses increased by 19% year-to-date until September. The US economy remained steady despite the recessionary fears. Also, the existing home inventory went down as the pace of new residential construction continued.

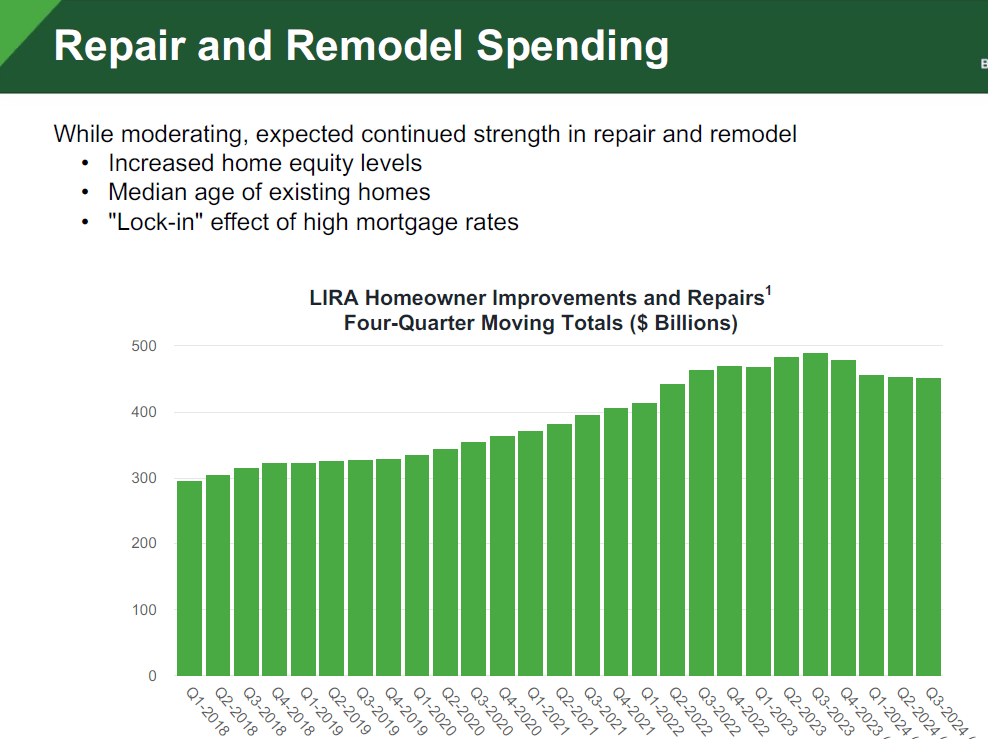

According to estimates provided by the company, the single and multi-family housing construction will remain stable in 2024. However, the growth in renovation spending could decelerate while homeowners' investment in their residences might fall. Over the long term, residential construction, repair, and remodeling activities are on an uptrend due to a favorable demographic structure and lower housing inventory.

Near Term vis-à-vis Long-Term Outlook

{kind=link}

Given the environment discussed above, BCC's sales volume in Q4 began on a less-than-encouraging note. In October, its sales volume was 6% lower than the Q3 average following the seasonal slowdown in construction activity. In Q4, its sales volume could potentially get sequentially lower, but it could also still outdo the sales volume recorded a year earlier. In engineered wood products, its pricing could trail the Q3 level by "single-digits" sequentially, as estimated by the company.

However, BCC's recent acquisition of BROSCO (in October) can add volume and mitigate organic loss. Through the acquisition, it added two full-scale distribution centers that would provide scale in the Northeast region. It will strengthen the company's offerings in interior and exterior doors, moldings, railings, windows, stair parts, etc. Investors may note that BROSCO's TTM revenue and EBITDA were $191 million and $19 million, respectively.

Margin And Inventory Strategy

{kind=link}

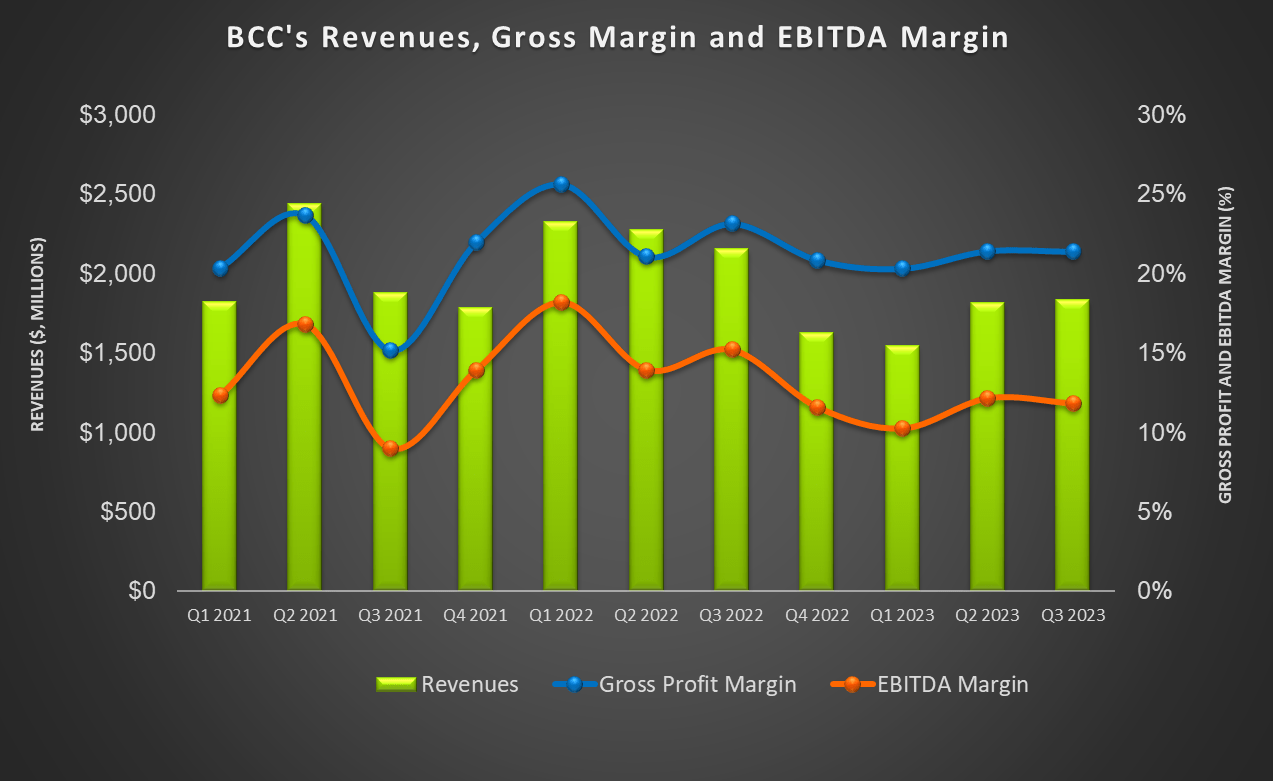

A slow start to the fourth quarter could put more pressure on the operating margin, which was already lower by 20 basis points in Q3 compared to Q2, and 190 basis points compared to a year earlier. So, the company will look to manage its inventory to offset the adverse effects. With a restored supply chain, it will position appropriately across the product lines. It will align with market activity, which would be a departure from the destocking exercise in 2022.

So, it will rely on two-step distribution to manage inventory volume and price risk. Nonetheless, deleveraging of fixed costs, gross margin weakening from product price erosion, and acquisition-related costs can lower the company's EBITDA margin in Q4.

Q3 Drivers Explained

{kind=link}

In Q3, BCC's revenues from the Wood Products segment decreased by 13%, while EBITDA margin fell by 590 basis points. Lower engineered wood products and plywood sales prices and laminated veneer lumber (or LVL) sales volumes primarily accounted for the deterioration in the segment results. Year-over-year, LVL volumes were down by 5%, but I-joist's sales volume was resilient. However, quarter-over-quarter volumes and lead times were substantial sequentially, which indicates the company's improved response to stronger-than-expected demand in 2023.

Its revenues from the Building Materials Distribution segment decreased by 15% in Q3, while its EBITDA margin fell by 200 basis points. Lower pricing in nearly all product lines in this segment negatively impacted the results. The decline in segment EBITDA was also reflected in a gross margin decrease and a rise in selling and distribution expenses.

Cash Flows And Debt Level

In 9M 2023, BCC's cash flow from operations decreased steeply (by 36%) compared to a year ago, led by lower revenues. Free cash flow (or FCF) declined by 44% in 9M 2023. I expect the inventory level to improve in the coming quarters as the pricing environment for lumber and panels stabilizes. It will, however, like to keep inventory on hand to account for any potential price volatility. Capex, on the other hand, can increase by $200 million in 2024 compared to 2023 as the company previously announced projects are completed. This can lower its FCF in 2024.

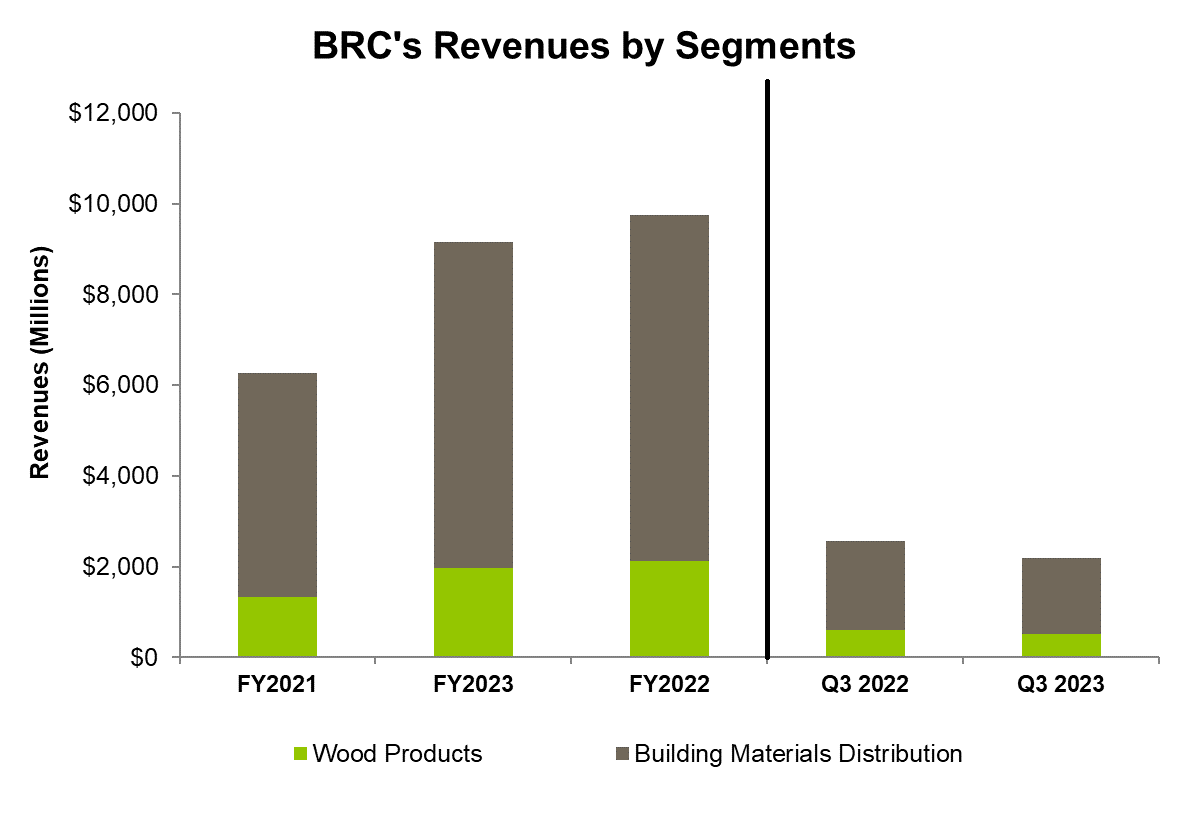

BCC has a much higher debt-to-equity ratio (0.45x) than some competitors (BXC, LPX, BRC). Its liquidity (cash & equivalents plus available borrowings from a revolving credit facility) totaled $1.66 billion as of September 30, 2023. The company pays a dividend of $0.20 per share. It also has ~2 million shares available under its share repurchase program. With sufficient liquidity, I believe it should meet its shareholder returns objective despite any fall in cash flows.

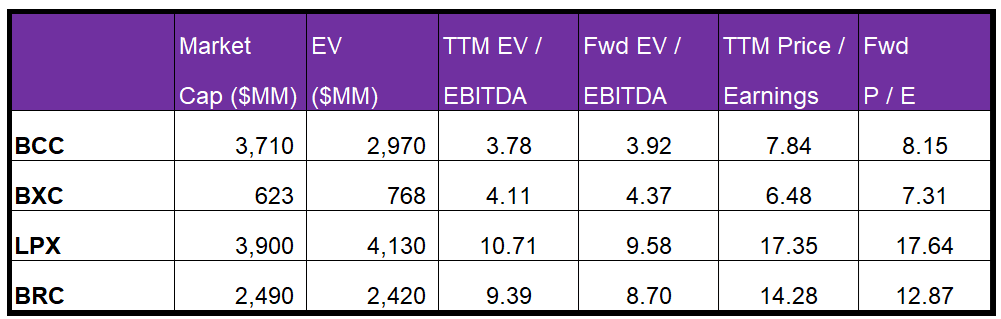

Relative Valuation And Returns Forecast

Author Created and Seeking Alpha

{kind=link}

BCC's forward EV/EBITDA multiple is expected to expand versus the current EV/EBITDA. This is in contrast to its peers because its EBITDA is expected to decrease versus an increase in EBITDA for its peers in the next year. This typically reflects in a lower EV/EBITDA multiple than peers.

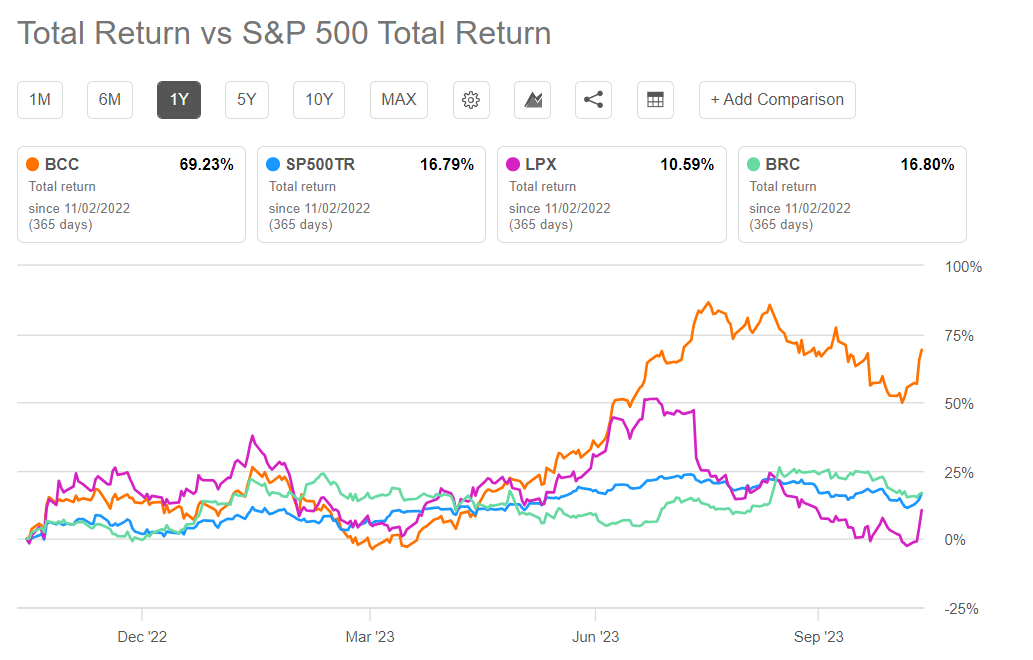

The stock's EV/EBITDA multiple (3.8x) is much lower than its peers' (BXC, LPX, and BRC) average of 8.1x. So, the stock is reasonably valued versus its peers. It is also trading at a slight discount to its past five-year average. Given the recessionary fear in the US, I do not see the stock improving sharply in the short term. However, if it trades at the past average in the medium term, it can climb 13% from the current level.

Given the near-term drivers, I think the stock may slide slightly (5%-10% downside potential), but with strengthened strategic positioning, it should back up to yield positive returns in the medium term.

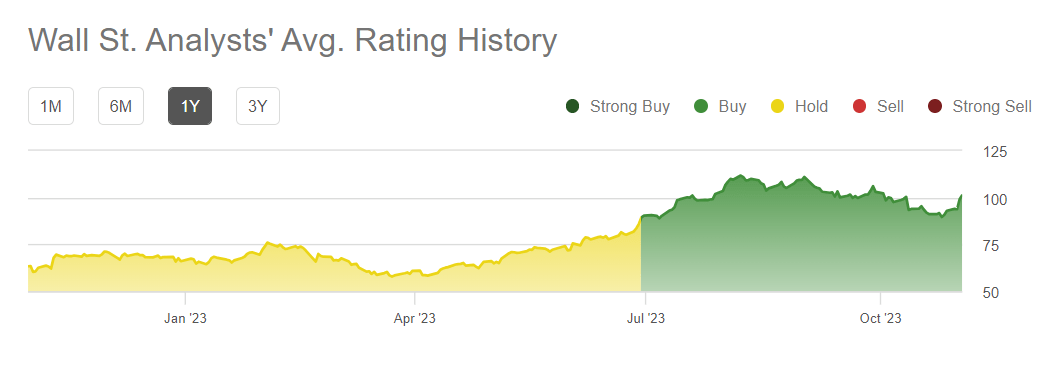

Wall Street Rating & Target Price

{kind=link}

In the past 90 days, two sell-side analysts rated BCC a "buy" (including "Strong buy"). Three analysts rated it a "hold," while one rated it a "sell". The consensus target price is $116.6, suggesting a 15% upside at the current price.

Risk Factors

{kind=link}

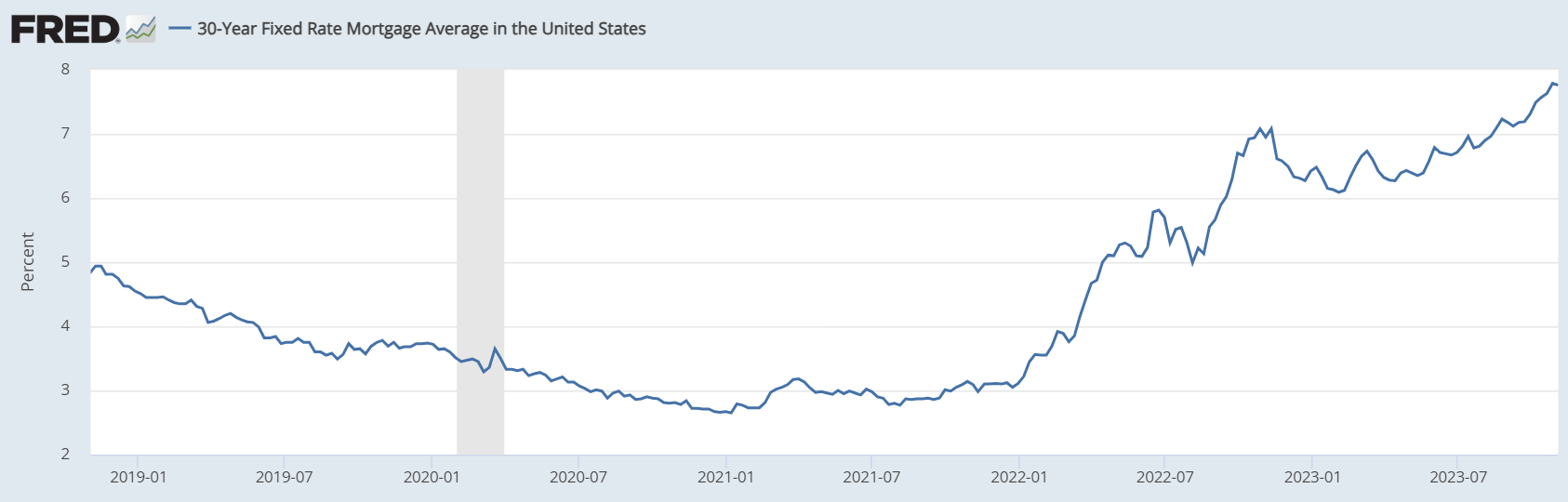

BCC's financial results, as I see it, critically depend on the US housing and residential construction market. The 30-year average fixed mortgage rate increased by 20% since the start of 2023. Economic uncertainties will continue to wrap around consumer sentiment, while relatively higher interest rates will affect the increased mortgage rate. These factors can adversely affect home sizes and amenities as the price incentives fall.

The other key risk for the company relates to fluctuations in OSB, plywood, and lumber pricing. If prices fall below the cash production or purchase costs, it can result in short-term losses. Also, the BMD segment operates in a highly fragmented and competitive industry where the barriers to entry are relatively low. This affects the company's pricing strategy as market share can be sensitive to pricing changes.

What's The Take On BCC?

{kind=link}

The US housing market is currently in flux, weighing on BCC's near-term outlook. The current interest rate regime in the US can lead to higher mortgage rates. On top of that, the renovation spending growth and homeowners' investment can decelerate. The company has started Q4 on a low note as the sales volume in October declined from the Q3 average. In engineered wood products, pricing can be concerning as stiff competition would make a recovery tenuous.

Despite the recessionary fears in the economy, the pace of new residential construction did not slow down. To offset the topline fragility, it recently acquired BROSCO, adding two distribution centers to expand its scale in the Northeast region. It will also fine-tune its inventory to mitigate the pressure on working capital. However, a planned increase in capex means its FCF can stay under pressure in 2024. Given the relative valuation, I think returns from the stock can go south before it gains encouraging ground in the medium-to-long term.

For further details see:

Boise Cascade Company Is A Hold For Long-Term Value Seekers