BOKF - BOK Financial: Loan Growth Unlikely To Fully Compensate For A Plunge In Other Operating Income

Summary

- The top line will benefit from healthy commercial loan pipelines and rising interest rates.

- The non-interest income will likely decrease this year due to lower mortgage refinancing income as well as losses on derivatives.

- The December 2022 target price suggests a small downside from the current market price. Further, BOKF is offering a low dividend yield.

Earnings of BOK Financial Corporation ( BOKF ) will likely plunge this year due to lower mortgage banking income and losses on derivatives booked during the first half of the year. Further, the provisioning will likely increase, which will drag earnings. On the other hand, strong commercial loan growth and moderate margin expansion will lift the bottom line. Overall, I'm expecting BOK Financial to report earnings of $6.83 per share for 2022, down 24% year-over-year. Compared to my last report on the company, I've increased my earnings estimate as I have slashed my provision expense estimate. For 2023, I'm expecting the company to report earnings of $7.88 per share, up 15% year-over-year. The year-end target price suggests a small downside from the current market price. Therefore, I'm maintaining a hold rating on BOK Financial.

The Topline to Continue Full Steam Ahead

The loan portfolio grew by a remarkable 3.0% in the second quarter of 2022, or 12% annualized, which beat my expectations. The management mentioned in the earnings presentation that it expects loan growth to approach a double-digit rate for the full year of 2022. In my opinion, this target can be achieved thanks to healthy pipelines and growth momentum. Commercial real estate (“CRE”) commitments grew by 7.5% during the second quarter, as mentioned in the conference call . The management expects these commitments to translate into balance sheet growth over the next several quarters.

Further, economic factors will sustain loan growth. BOK Financial operates in several states across the Midwest and Southwest. Further, the company focuses on commercial and CRE loans. Therefore, the purchasing managers' index is a good gauge of credit demand. Both the manufacturing and services PMI indices are still in expansionary territory, which bodes well for loan growth.

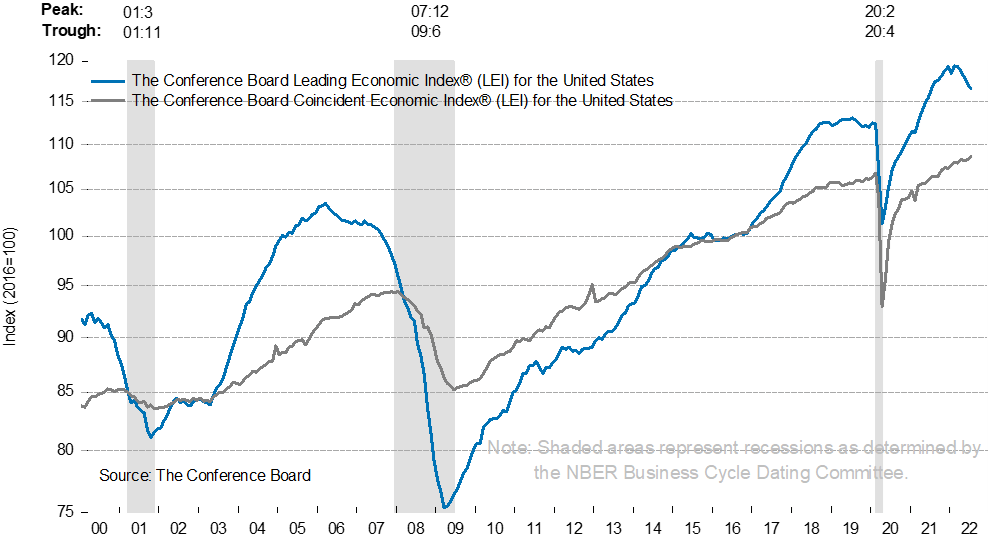

On the other hand, the U.S. leading economic index is persistently on the downtrend, which is bad news for loan growth.

{kind=link}

Overall, I'm expecting the loan portfolio to increase by 2% in the last two quarters of 2022, or 8% annualized. Beyond 2022, I'm expecting loan growth to slow down to 6%, which is closer to the historical norm.

In my last report on BOK Financial, I estimated loan growth of 7.1% for 2022. I've increased my loan growth estimate due to the second quarter’s performance and the management's updated guidance. At the same time, I've reduced my estimates for other earning assets as such high loan growth should crowd out the growth of securities. The following table shows my balance sheet estimates.

| FY18 |

| FY19 |

| FY20 |

| FY21 |

| FY22E |

| FY23E |

| Income Statement |

| Net interest income |

| 985 |

| 1,113 |

| 1,108 |

| 1,118 |

| 1,123 |

| 1,194 |

| Provision for loan losses |

| 8 |

| 44 |

| 223 |

| (100) |

| 8 |

| 16 |

| Non-interest income |

| 617 |

| 694 |

| 844 |

| 756 |

| 594 |

| 684 |

| Non-interest expense |

| 1,028 |

| 1,132 |

| 1,166 |

| 1,178 |

| 1,116 |

| 1,176 |

| Net income - Common Sh. |

| 446 |

| 501 |

| 432 |

| 614 |

| 461 |

| 532 |

| EPS - Diluted ($) |

| 6.63 |

| 7.03 |

| 6.19 |

| 8.95 |

| 6.83 |

| 7.88 |

| Source: SEC Filings, Author's Estimates (In USD million unless otherwise specified) |

In my last report on BOK Financial, I estimated earnings of $6.54 per share for 2022. I've increased my earnings estimate as I've slashed my provision expense estimate.

Actual earnings may differ materially from estimates because of the risks and uncertainties related to inflation, and consequently the timing and magnitude of interest rate hikes. Further, a stronger or longer-than-anticipated recession can increase the provisioning for expected loan losses beyond my estimates.

Maintaining a Hold Rating

BOK Financial has a long-standing tradition of increasing its dividend every year. Given the earnings outlook and the payout trend, I’m expecting the company to increase its dividend by $0.01 per share to $0.54 per share in the fourth quarter of 2022. The earnings and dividend estimates suggest a payout ratio of 27% for 2023, which is close to the five-year average of 30%. Based on my dividend estimate, BOK Financial is offering a forward dividend yield of 2.4%.

I’m using the historical price-to-tangible book (“P/TB”) and price-to-earnings (“P/E”) multiples to value BOK Financial. The stock has traded at an average P/TB ratio of 1.50 in the past, as shown below.

| FY18 |

| FY19 |

| FY20 |

| FY21 |

| Average |

| TBVPS - Dec 2022 ($) |

| 56.4 |

| 56.4 |

| 56.4 |

| 56.4 |

| 56.4 |

| Target Price ($) |

| 73.5 |

| 79.1 |

| 84.8 |

| 90.4 |

| 96.0 |

| Market Price ($) |

| 91.6 |

| 91.6 |

| 91.6 |

| 91.6 |

| 91.6 |

| Upside/(Downside) |

| (19.8)% |

| (13.7)% |

| (7.5)% |

| (1.4)% |

| 4.8% |

| Source: Author's Estimates |

The stock has traded at an average P/E ratio of around 11.5x in the past, as shown below.

| FY18 |

| FY19 |

| FY20 |

| FY21 |

| Average |

| EPS 2022 ($) |

| 6.83 |

| 6.83 |

| 6.83 |

| 6.83 |

| 6.83 |

| Target Price ($) |

| 64.6 |

| 71.4 |

| 78.3 |

| 85.1 |

| 91.9 |

| Market Price ($) |

| 91.6 |

| 91.6 |

| 91.6 |

| 91.6 |

| 91.6 |

| Upside/(Downside) |

| (29.5)% |

| (22.1)% |

| (14.6)% |

| (7.2)% |

| 0.3% |

| Source: Author's Estimates |

Equally weighting the target prices from the two valuation methods gives a combined target price of $81.5 , which implies an 11.1% downside from the current market price. Adding the forward dividend yield gives a total expected return of negative 8.7%. Hence, I’m maintaining a hold rating on BOK Financial.

For further details see:

BOK Financial: Loan Growth Unlikely To Fully Compensate For A Plunge In Other Operating Income