BDNNY - Boliden: Great Company Difficult Price

2023-04-19 12:58:26 ET

Summary

- I recently re-reviewed companies in the Swedish mining/metals sector. Boliden is next in line, and here is my update on the company for 2023.

- Boliden is a superb company - and a company I know quite intimately due to my work with them, and where they operate.

- However, recent high valuations cause me to still be relatively careful with the company as an investment. There is a lot to like about Boliden - but not the valuation.

Dear readers/subscribers,

Despite attractive geographies and an attractive profile in terms of mining and its operations, Boliden (BDNNY) is an undercovered and underappreciated company with, as I see it, plenty going for it. However, it also needs to be trading at the right price for us to profitably invest in the business - to make sure the upside is actually good enough.

Last time I wrote about Boliden was in 2020. Since that time, the company has seen significant macro changes with impacts to operations. In this article, we'll review what we can expect from Boliden based on these trends and changes, and what this means when it comes to its valuation.

Updating on Boliden for 2023

I know Boliden quite a bit more than other mining companies - because, in my work, I often have direct contact with the company and its personnel. I've shared booths and groups in recruitment and marketing events, and I've been in frequent contact with their IR, and even parts of management. I've been analyzing the company for years - and for over a year now, I'm actually living close to one of the company's regional headquarters.

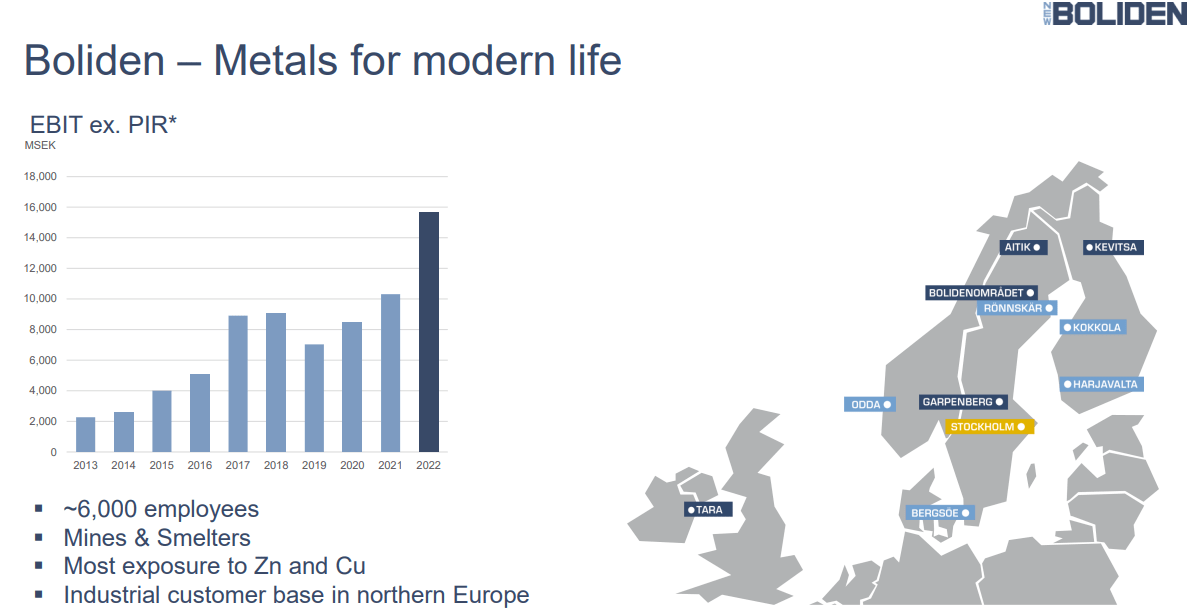

Boliden, if you recall my original article, is a mining company headquartered and run in Sweden (with operations mostly in Scandinavia, but including Europe) and involved in the first steps in the mining processing chain .

That means that Boliden does everything from exploring and prospecting, to mining and enriching, but also smelting, refining, and recycling. In fact, when it comes to the recycling of metals, Boliden is one of the foremost companies in the entire world, and this is one of its fastest-growing segments - and has remained so for going on nearly 5 years at this point.

Outside of recycling and its myriad-metal operations, what Boliden is most known for is its operations relating to Zinc and Copper. In fact, its copper operations put the company in the position of being a major player in the entire EV shift.

{kind=link}

Even with near-term uncertainties and volatilities, there's plenty to like here - and despite uncertainty, the demand for copper specifically is remaining solid here. If you need a refresher on where the company "plays", here is an overview of Boliden's current operations.

{kind=link}

The company is a northern-European mining operation, also with most of its customers in Northern Europe. The company is, if you look at it like that (and most of their employees do), a company of contradictions. It's small with only 6,000 people, but at the same time, it's listed on OMX large cap. It's local, with strong ties to communities where they operate, but at the same time, it sources a global network of smelters and resources. It's conservative, preserving what it can in terms of culture and operations, but at the same time, very few mining businesses in the world have managed to integrate technology to the degree that Boliden has. Things like Electric trolleys where most other operations still use standard transport trucks have been a thing for Boliden for a long time now.

Recent results confirm this relatively solid outlook. Like other miners and smelters, Boliden is volatile with ups and downs - and the latest few years have really seen it go "both ways", to up and down. I bought at the same time when I bought SSAB, which was over 3 years back - but I no longer own shares in the company.

{kind=link}

The latest few years with their excellent results have seen Boliden significantly improve its capital position, oftentimes going from net debt to overall net cash. The structure as of year-end 2022 includes an average interest rate for debt of 2.5%, with almost 60% equity and a 0% net debt/equity ratio.

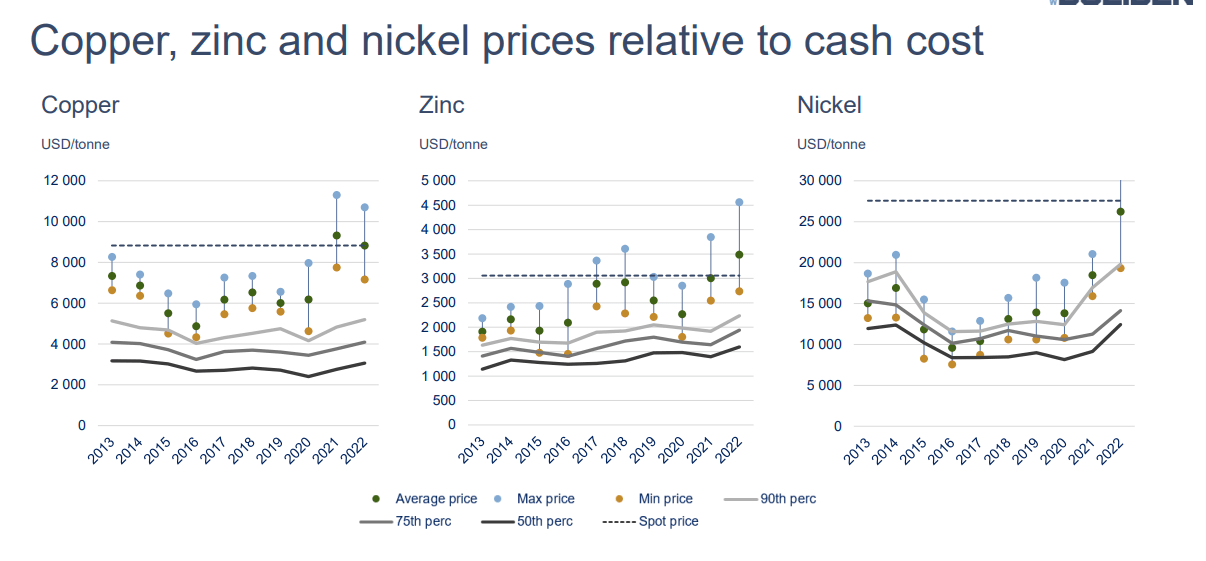

In the end, Boliden like any miner and smelter remains a company highly correlated to the market prices of specific metals. And as you can see, the market for most of these has been extremely favorable for the past few years.

{kind=link}

However, the same problematic trends we see in other parts of the segment, and which I've highlighted in other relevant articles for the company, can be highlighted and seen here. Costs are going up - especially energy, and market prices are slowly declining. For the time being, we have favorable FX and stabilization, but given the current macro environment, I believe that things will eventually turn down, not up.

Boliden isn't as overvalued as some indirect peers like SSAB ( SSAAF ) - for reasons I will show you later, I consider Boliden to be mostly fairly valued at this time with an actual potential upside in some cases. However, we're recently out of a bout of overvaluation, and the share price has been very unstable since COVID-19, going up and down significantly.

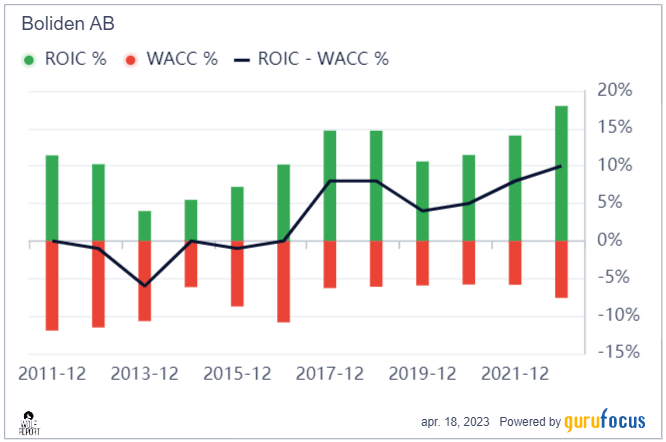

From a fundamental perspective, Boliden is one of the best miners in the world. Margins and return KPIs are in the top-90th+ percentiles for this business, including in ROE, ROA, ROIC, and ROCE - the company also has consistent profitability going back over a long period of time. What's more, the company's profitability in terms of its actual cost of capital has been climbing for years.

{kind=link}

Cash flow, income, and stockholder's equity has been rising in tandem with these positive trends. The only thing Boliden hasn't done is buy back shares - but this is not necessarily a negative for me.

Boliden is a very well-managed business with a solid potential upside. The company's reserves are still relevant for many, many years, and the company is moving into expansion into new mines as well, or expanding current mines, while also pushing productivity improvements through automated haulage, positioning systems, robot chargers, and other things.

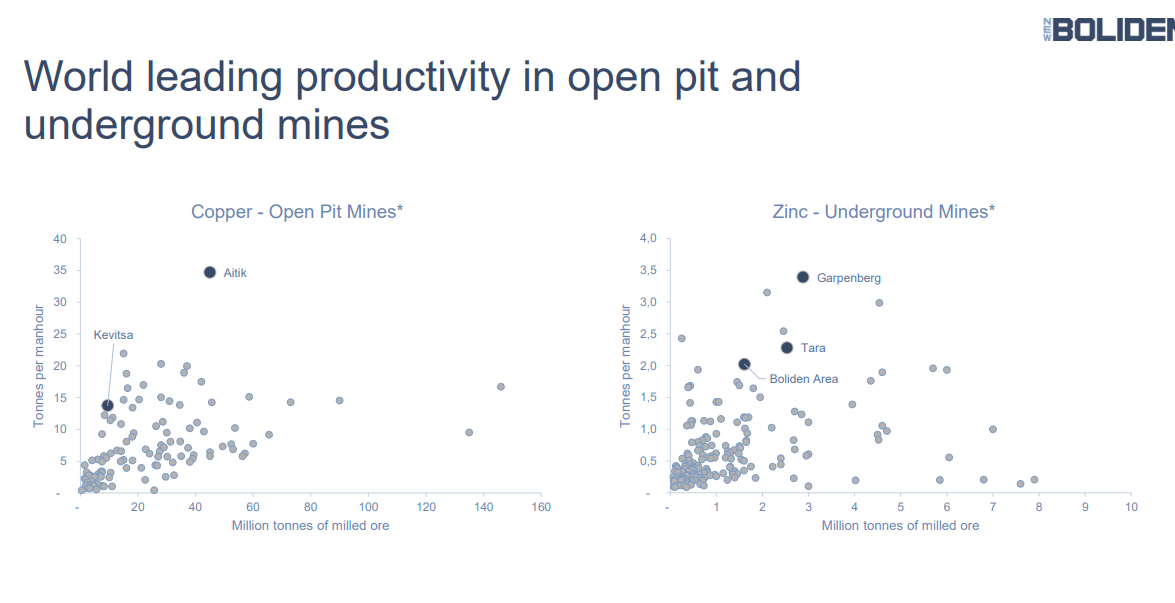

The company's mines, especially in copper and Zinc, are some of the most productive mines on earth.

{kind=link}

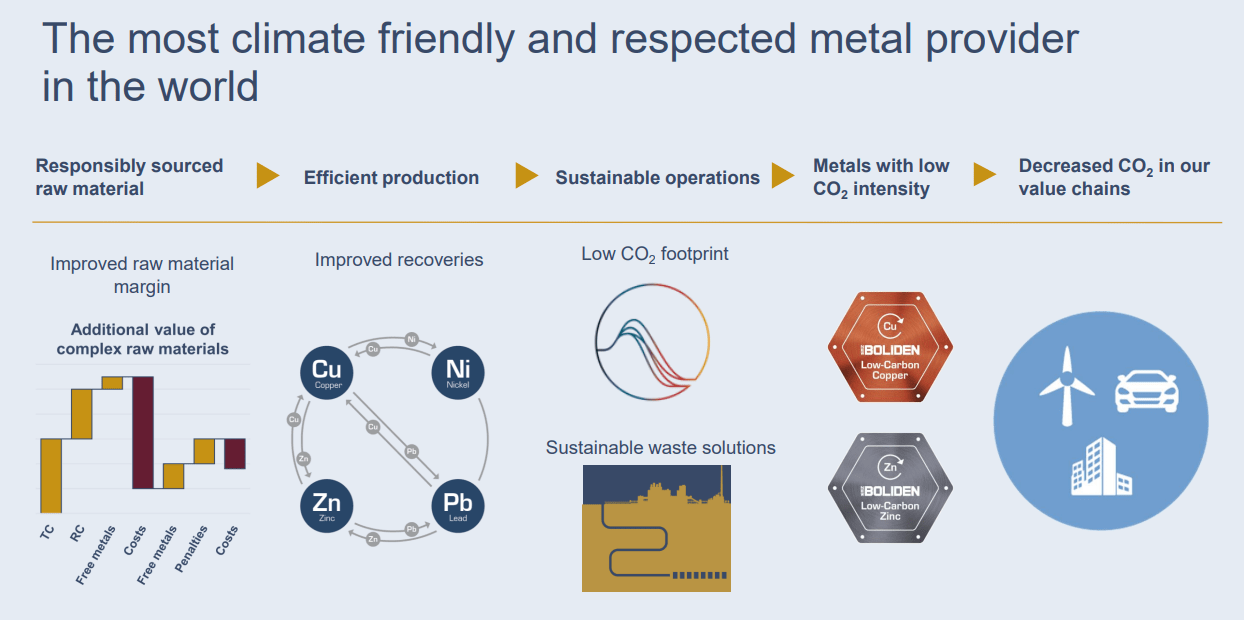

I do not believe it to be an exaggeration to say that this is a company you want to own. The company is already amongst the most world-leading in climate performance and its new pushes, including things like fossil-free mining in a new expansion, battery-powered trucks, and EV-based transport on public roads. The company is also testing Nitrate-free Co2 explores. The company markets itself as the most climate-friendly metal provider in the world.

{kind=link}

And while there are some concerns and considerations that need to be taken into account before you put money to work here, this company is not as overvalued as some of the recent peers we've been looking at.

Let's see what Boliden has going for it in terms of valuation.

Boliden - The valuation is not attractive here

Valuation for miners is always a bit tricky - even more so than for certain other types of companies. Their high CapEx and risk profile make them a "special" sort of investment, as I see it. So, I own very few - but Boliden is, and has long been one of them - albeit only at an attractive valuation.

First off, Analysts. S&P Global analysts following the company call it a "HOLD". 17 analysts follow the company, averaging 310-540 SEK with an average of 400 SEK, or an overvaluation of roughly 2%, at a P/NAV of 1.03x, meaning that 400 SEK equals around 1x or close thereto. Out of 17 analysts, only 2 are at a "BUY" here, making the stance on the company very clear as it currently is.

This is quite understandable. The problem lies in the coming dip in earnings - how deep, how long, and how consistent it'll be. If we consider the 5-year average for Boliden, the company could generate as little as 1-2% RoR even with dividends going forward, negative without the dividend. That is not an attractive prospect.

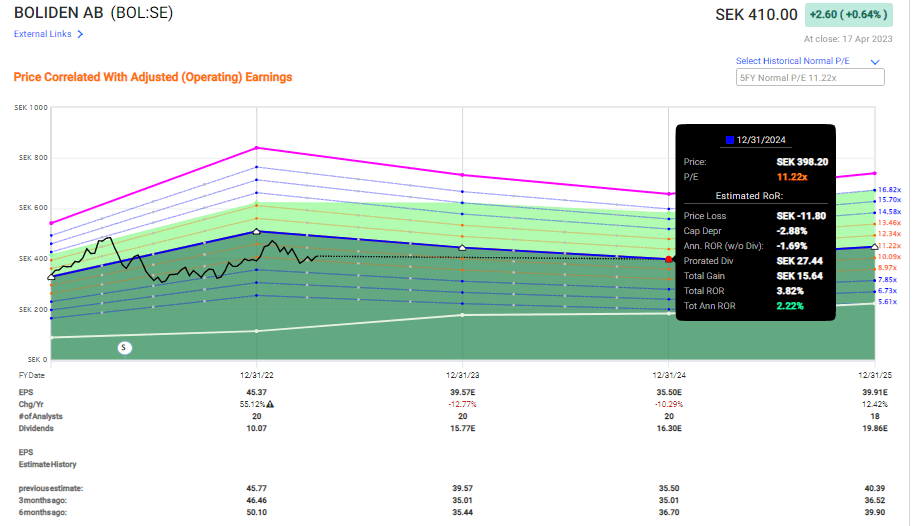

Boliden Upside (F.A.S.T Graphs)

{kind=link}

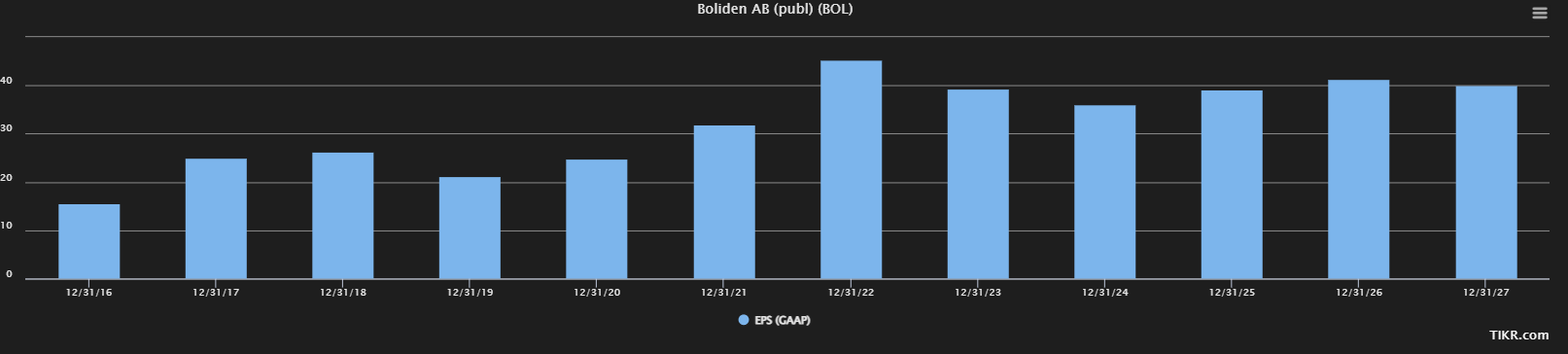

Even if we include the potential recovery from lows, to a 2025E 12% EPS growth, that still only brings about a 7% annualized RoR until then - which is lower than I would consider relevant, given that almost 4% of it is the company dividend.

So, the overall picture in terms of what we can expect or forecast here - is not all that attractive, unfortunately. FactSet is also not the only analyst forecasting an earnings decline here. The forecasts are consistent with what other people following the company see. This also includes me and to some extent the company itself, which refers to a pressured environment over the next 1-2 years. Here are the S&P Global GAAP expectations in terms of earnings.

Boliden Forecast (F.A.S.T graphs)

{kind=link}

So, combining the industry forecast with these expectations, despite the company's really superb assets and fundamentals (minus credit rating, it doesn't have an IG from S&P Global), we get a mixed picture that I would characterize as somewhat sub-optimal.

My usual cost basis when buying Boliden is closer to 300 SEK - the closer to it, or below it, the better I consider the deal. Boliden is like other European metals companies or like some fertilizer companies. In good years, the company can literally make you rich on dividends alone provided you bought enough, and at the right time, like Yara ( YARIY ). This year alone, my YoC from Yara is more than 15%. Boliden can do the same if you have the foresight to take advantage of valuation - and that's where I am trying to be people's "sherpa" here on Seeking Alpha.

You could have bought Boliden at 150 or below back in COVID-19. I had other companies in my sights at the time, but I did buy it cheaply later, resulting in an almost triple-digit RoR over time, and when I sold when the company reached above 415 SEK, which by the way happens to be my trim target here.

Boliden can technically be bought - it's fairly valued here at around 400-410 SEK but fairly valued in a market like this is not a positive. Not in any way. What you want to do in a market like this, is to quote the game, "go fish!".

This is the sort of market where I fish for undervalued, overly-qualitative opportunities in virtually every sector - but in particular, those sectors seeing pressure.

At this time, that's finance - not mining.

Scandinavian mining is still riding high from the superb years of 2021-2022 with record results and dividends for many of them. Most analysts seem to be far too slow to unwind these positives. Perhaps I am too quick to do so - but I do not believe that to be the case.

These are extremely volatile companies that, if handled incorrectly, can make sure that you earn sub-par returns on your invested capital for over a decade and more. Between 2007 and 2020, an investment into Boliden at lows would have brought about returns of less than 2.8% per year. You could literally have gotten more out of certain savings accounts.

So, my point is - buy Boliden at attractive prices to make sure you lock in that upcycle upside and yield. That could turn your invested capital into a cash-minting machine in both dividends and capital appreciation to the tune of triple digits in less than 5 years in my view.

For now, this is my thesis on Boliden AB.

Thesis

- Boliden is a class-leading mining and metals company with an attractive overall upside if bought at the right price. It has the sort of solid fundamentals you want in an investment such as this and operates primarily in Northern Europe.

- Since COVID-19, the company has seen a significant expansion of profit and share price due to macro and pricing for metals - however, that is now slowly turning around, and a combination of cost and inflation pressures as well as a declining market will, I believe result in the company trading down over the next 3-4 years, not up.

- For that reason, I consider Boliden around fairly valued at this price with very little upside - a "HOLD", at best, with a PT of below 380 SEK, but even that gives you only a conservative upside of around 8% per year. I'd wait for a price closer to 300.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

I would not consider Boliden to have a realistic upside at this time, or being cheap, meaning I call it a "HOLD".

For further details see:

Boliden: Great Company, Difficult Price