BDNNY - Boliden - Starting To Look More Interesting After 20%+ Drop

2023-07-04 09:51:39 ET

Summary

- I previously rated Boliden as overvalued, and since then, the company has lost 26.37% of its value, confirming my stance.

- I advised against buying Boliden due to its overvaluation, which turned out to be the correct decision.

- The recent decline in Boliden's valuation may now make it a more viable investment option, which I intend to explore further.

Dear readers/followers,

When I last reviewed Boliden ( BDNNY ), I came in at a pretty sanguine rating for what I viewed to be a massively overvalued mining business. Since that particular, the company has gone exactly the way I expected it to go - albeit somewhat faster than I expected it to go. Boliden has lost 26.37% of its value since my last article, or the following even with dividends compared to over 7% from the S&P500 in the meantime.

Seeking Alpha Boliden RoR (Seeking Alpha)

Now, obviously, my stance regarding Boliden and not to "BUY" it in overvaluation was the correct one. That last article was published back in April 2023 - and in this, I'm going to be updating my article for the company. The fact is that this decline in valuation has brought Boliden to a point where it may actually be invested in.

At least, that is what I intend to show you here.

Boliden - Plenty to like about the valuation and what the company offers here

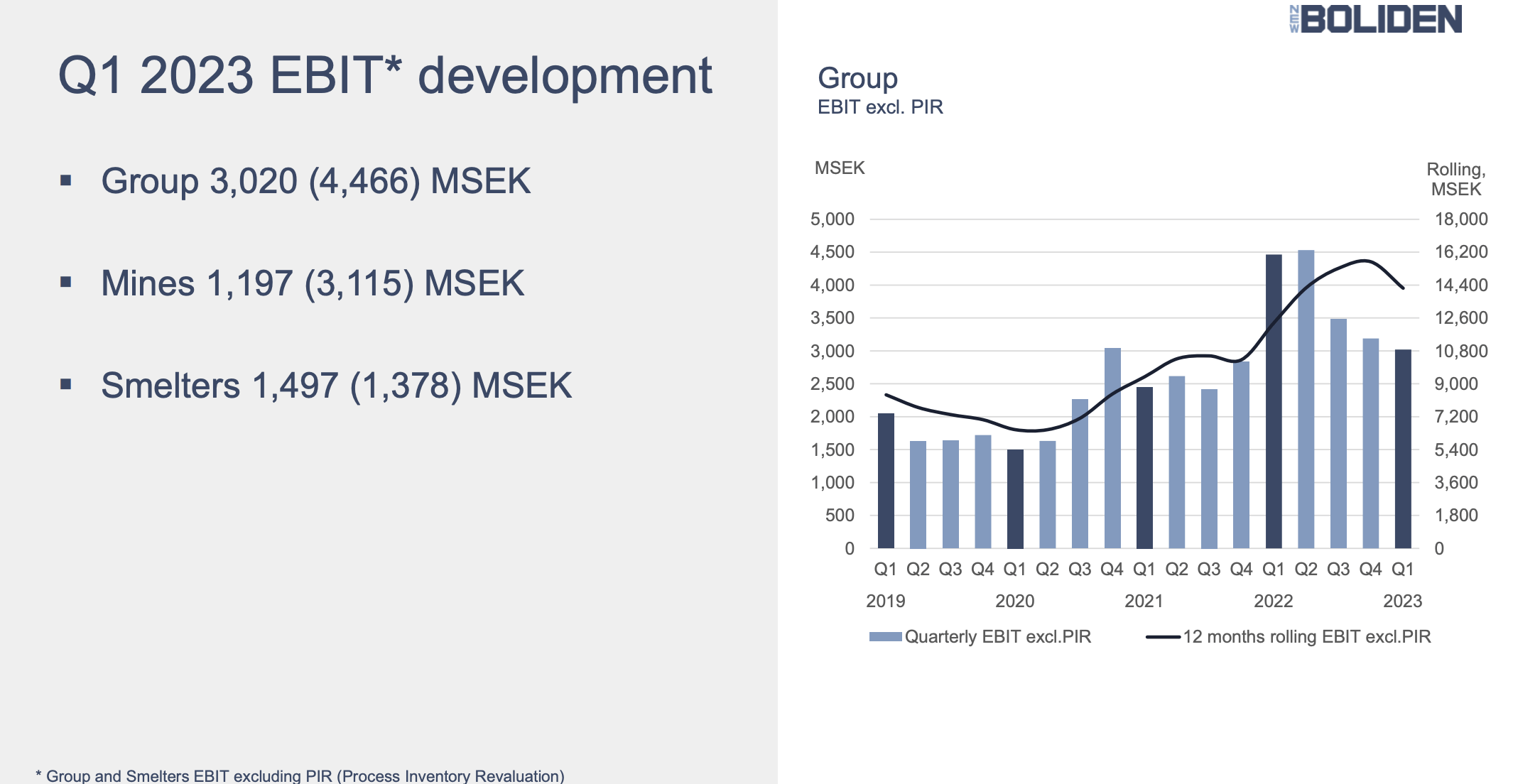

What we have for Boliden is the 1Q23, which details the introductory reason as to why we're starting to see declines in Boliden here. Record-level prices for metal are sooner or later going to make way for a decline - and that decline in pricing has begun here.

Boliden compounds these issues by also experiencing some production issues in some of its assets - namely lower overall production and overall disruptions, together with inflation, labor costs, logistical cost increases, and other issues which really aren't Boliden-specific, but which nonetheless are impacting the company here.

EBIT for the company is at 3B SEK for the quarter - but that's 1.5B SEK lower than the YoY period. FCF went negative at -46M, compared to almost 650M FCF YoY, and CapEx is double what we saw YoY.

In short, every indicator in the financial performance overview goes the "wrong" way, if that's how you want to view it.

{kind=link}

Viewed over longer-term periods, it's clear to me that what we're seeing here is really just a reversal from an ATH sort of level. So it's not that much of an issue - at least, it wouldn't be if we weren't valuing the company at what are essentially record-level valuations here.

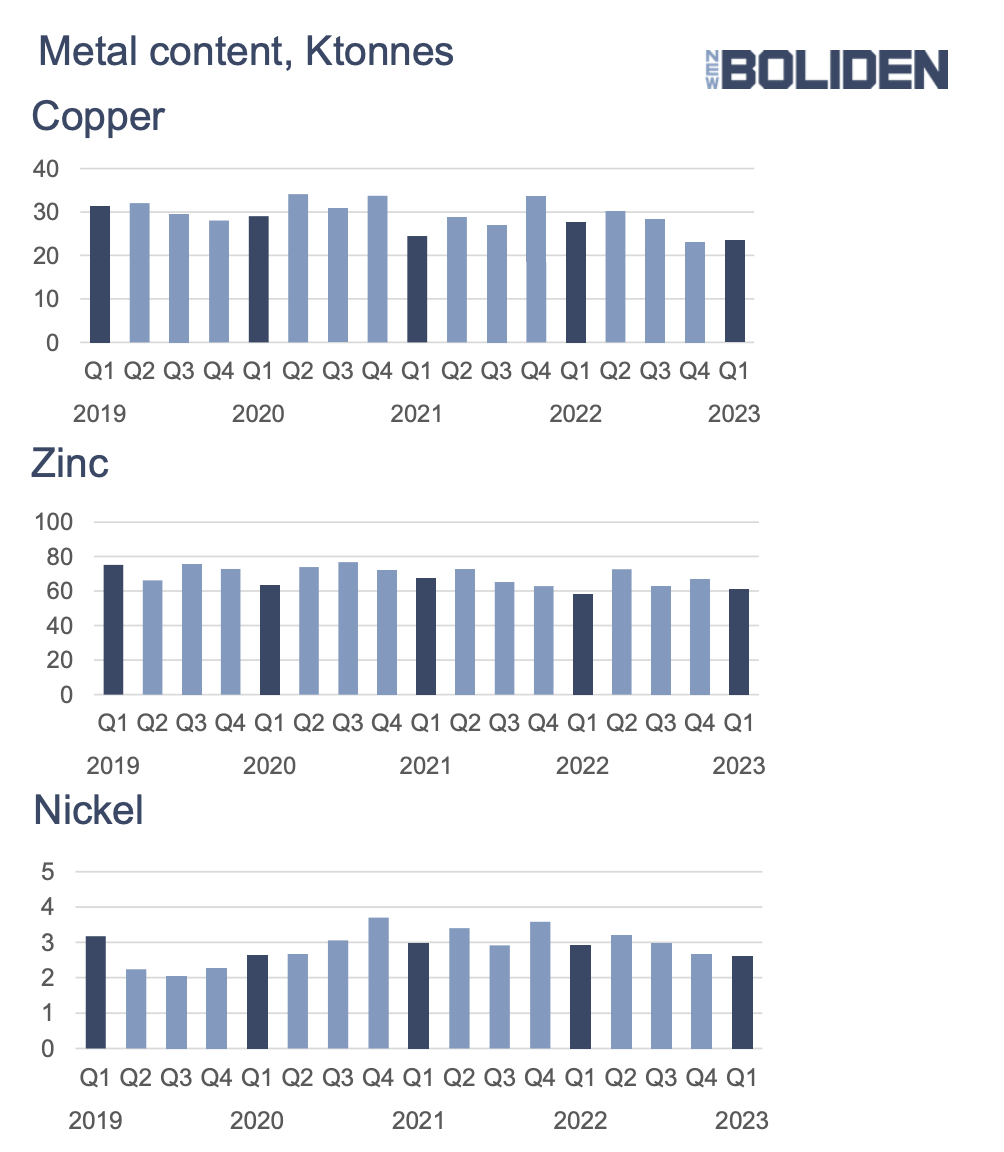

This is then added to by trends in metal pricing - negative ones, with stronger USD. The worst part though, is mine production. Boliden saw significant production decreases on a YoY basis, due mostly to lower crusher availability, unplanned maintenance outages, and something as relatively simple as conveyor belt disruptions, or even just "challenging winter conditions", which for a company like Boliden should really be part of normal business operations given where their assets are located.

{kind=link}

Lower mine production results in mostly lower smelter production, especially for copper. Several of the company's assets here saw process disturbances, unfavorable feed mixes, logistical issues, and other headwinds. Other than that - reduced electricity prices from ATH have at least resulted in some positives here.

The high-level picture is simple. The company is reversing from its ATH and is moving towards a typical downcycle - especially in the mining portion. On the positive side, the company has used the significantly positive years to improve its capital position and debt. The current net debt is at 0.1x, with a 0% net debt/equity, with an average interest rate of 3.5%.

I know Boliden quite a bit more than other mining companies - because, in my work both on the corporate and private side, I often have direct contact with the company and its personnel. Not only do I have contact, I've shared booths and groups in recruitment and marketing events, and I've been in frequent contact with their IR, and even parts of management. I've been analyzing the company for years - and for over a year now, I'm actually living close to one of the company's regional headquarters.

It's a timeless company - provided you understand and can play the ups and downs. Very few investors can. That's why I sold my meager position at the highs during 2022, knowing that eventually things would go back down, and we could once again invest profitably in the company.

We're starting to see this here. The company is a margin leader in its segment - miners - excepting the gross margins, but with a double-digit 12%+ net margin - also, superb return metrics on RoE, RoA, and ROIC. Even better net margins for 2022 - though again, these likely won't be repeated in the near term.

{kind=link}

The company has been left cash-heavy due to the massive upside for the past few years - leaving it with more cash than actual debt (explaining its net debt), and despite its downturn currently, the company has plenty of profitability, even with funding costs rising here.

It's my intent to "play" the ups and downs of this particular company. Though I expect, based on pandemic trends, that the company will not go down quite as deeply as before - also due to macro. Even though China is not demanding as much base metals with its infrastructure and construction industry in a very different position than years ago, the global demand for copper remains at a relatively high level.

Boliden is, in many ways, perhaps my favorite mining company around, because it combines many of the attractive and safety considerations I typically find in much larger companies. It's small with only 6,000 people, but at the same time, it's listed on OMX's large cap. It's local, with strong ties to communities where they operate, but at the same time, it sources a global network of smelters and resources. It's conservative, preserving what it can in terms of culture and operations, but at the same time, very few mining businesses in the world have managed to integrate technology to the degree that Boliden has. It does what it does very well, almost as some would argue, one of the best companies in all of Europe.

In the end, however, Boliden like any miner and smelter remains a company highly correlated to the market prices of specific metals. We're starting to see a reversion in the favorability for this, which is why I'm getting excited when the market reacts as strongly as we're seeing here. Because it means that we might see Boliden go cheap fairly soon.

I actually wrote my first cash-secured puts on the company not long ago. The strike for this particular set of contracts is at 285 SEK - I don't expect them to go through, but if they do, you won't see me complaining in the least. If you recall, that's very close to my price target (more on that later).

The thing I'd watch closely with Boliden is metal prices. Once those turn comparatively sour, a company like Boliden doesn't have the same positive circumstances to actually generate any sort of positive profit. Boliden's results will likely see a significant YoY downtrend compared to 2022 - and this was expected. That does not make the company bad in any way - only correlated.

We also want to keep an eye on happenings in the company. For Boliden, there was a fire at Rönnskär not that long ago - the electrolytic refinery was completely destroyed. All other production lines are expected to be reopened in July - but copper production will be made in anodes instead of cathodes, which affects the business model of the company, alongside that Boliden's production lines may have to operate at limited capacity.

Also, the company laid off 190 people. So things like this can and do have impacts - and are contributing factors to the downturn. More can be read about this here.

Let's look at the company valuation and what sort of upside we have at ~320 SEK per share.

Boliden's valuation - my sub-300 SEK price target remains, but the upside is "close"

As I've alluded to in previous articles, I don't change my price targets lightly, and I don't establish my price targets without logic and long-term consideration. Because of that, just because Boliden drops double digits in less than 5 months, doesn't mean I change my PTs. That decline was already included in my consideration.

My case for Boliden is relatively simple. If we consider that over the past 20 years, the company has averaged nearly 20% CAGR, and investors in Boliden have made nearly 19% per year, almost 2.5x the S&P500, that means that this company is attractive. However, the time to buy it is when metal prices and valuation are relatively low, not high. A 9-11x P/E is usually fair for this business, and we're currently on an 8.16x normalized P/E here.

However, for this year, a 27% EPS decline is expected - I consider 25-40% likely given trends and current macro. After that, the company is expected to grow by FactSet analyst forecasts - I would say it is possible, but it's more conservative to expect a flat development as opposed to growth.

If you're willing to forecast at 10-11x P/E, you can now get a double-digit upside close to 14-15% based on these forecasts, or almost 40% until 2025E. That's not bad, but it's also a target I consider too positive.

{kind=link}

The reason I target a PT closer to below 300 SEK/share is that at that point, we can see potentially double-digit upside without requiring the company to grow much from its 2023 lows - it can even decline quite a bit more without seeing negative RoR from a 9-10x P/E.

For those reasons, a sub-300 SEK PT for the company is one I consider to be pretty solid. That's also why I sold those cash-secured puts at below 290 SEK - it's the first time in a very long time that I've been able to sell attractive options at that level. The current S&P Global targets come to a range of between 270 SEK and 495 SEK, a massive spread with an average PT of 351 SEK. However, today only 1 analyst out of 17 is at a "BUY" rating, with the majority (14) being at "HOLD". This expresses what I view as an accurate assessment here - it's a good time, still, to wait for the company to go cheaper before buying.

Therefore, my thesis for Boliden here is as follows.

Thesis

- Boliden is a class-leading mining and metals company with an attractive overall upside if bought at the right price. It has the sort of solid fundamentals you want in an investment such as this and operates primarily in Northern Europe.

- Since COVID-19, the company has seen a significant expansion of profit and share price due to macro and pricing for metals - however, that is now slowly turning around, and a combination of cost and inflation pressures as well as a declining market will, I believe result in the company trading down over the next 3-4 years, not up.

- As of 1Q23, we've seen a beginning of this trend, with the company going down.

- For that reason, I consider Boliden around fairly valued at this price with very little upside - a "HOLD", at best, with a PT of below 380 SEK, but even that gives you only a conservative upside of around 8% per year. I'd wait for a price closer to 300, where I also put my Boliden long-term PT - at 300 SEK or below.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

I would not consider Boliden to have a realistic upside at this time, or to be cheap, meaning I call it a "HOLD".

For further details see:

Boliden - Starting To Look More Interesting After 20%+ Drop