BDNNY - Boliden: The Thesis Is Playing Out As Expected

2023-10-02 21:02:15 ET

Summary

- Boliden, a mining and metals company, has experienced a decline in share price and financial performance in 2Q23.

- The company is facing challenges such as a fire at an important asset, weaker pricing, and lower grade production.

- The company's current troubles have led to a high level of leverage and a decline in earnings, making it a "HOLD" for investors.

Dear readers/followers,

I've covered Boliden ( BDNNY ) a few times previously . I realize these articles are mostly underfollowed - but given that I've managed to get something of a 100%+ RoR from this company previously, I consider it valuable to continue covering it to be able to guide you when it's actually (according to me) time to buy it.

My overall rating on Boliden has still paid off in spades. The company has, since my last "HOLD" rating, continued to decline and seems to have found an overall bottom with around a 30% decline since my first article.

What have I done about Boliden since that time?

I've looked at doing some buy-writes, and covered calls to ensure a double-digit return at attractive share prices. I have, however, as of right now, been unable to find the proper or appealing setup for such a play - so I still remain at a "no position", or at least not a significant one, for Boliden. I was able to find some attractive CSPs, but those covered puts did not go through either, and at this time, it was some months ago.

Let's update after 2Q23 and see where this company is likely to go in the foreseeable future.

Boliden - Attractive upside from good mining operations.

The company covers every conceivable step in the first steps of mining and processing. This includes both the exploration and prospecting of new potential assets, mining, enrichments, and smelting, refining, and recycling of metals. In fact, when it comes to the recycling of metals, Boliden is one of the foremost companies in the entire world, and this is one of its fastest-growing segments. However, its main segment is of course metals, and the largest metals that Boliden is involved with in terms of revenue are Zinc and Copper.

The company also still does lead, nickel, gold, and silver as well as Cobalt - but it's mostly the ones mentioned above.

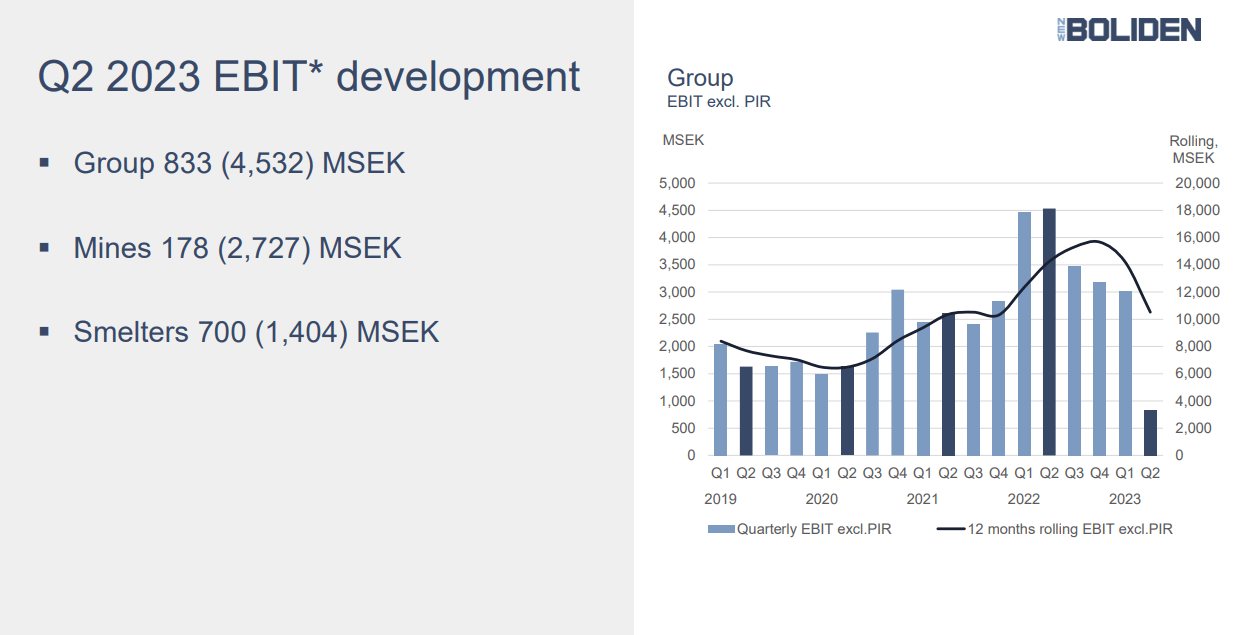

2Q23 wasn't a great quarter. It's why the share price is down as it is. We had a fire at an important asset, weaker overall pricing, the asset Tara put on care and maintenance, and lower grade production/mining results in the company's mines, as well as a planned major maintenance in Harjavtalta.

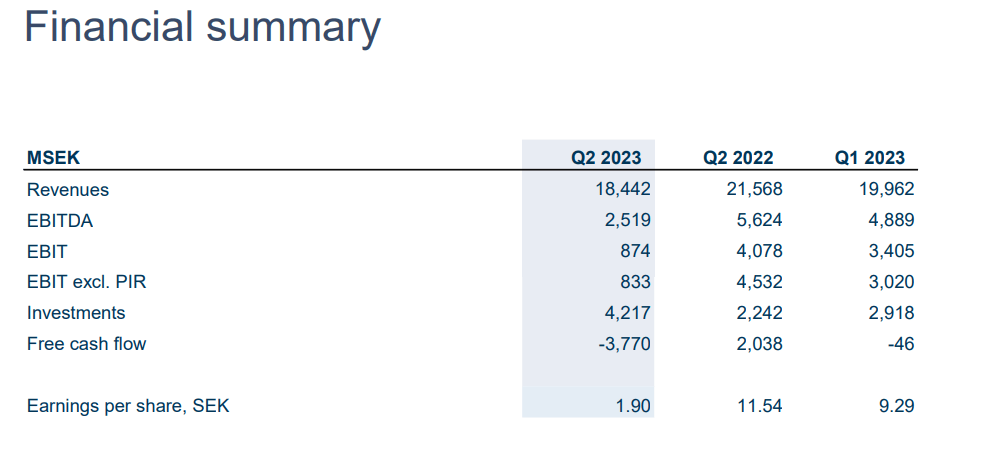

On the positive side - its projects are going according to plan - but the financial performance was fairly dismal if you compare it to YoY numbers. We're talking significant EBIT decline, a cash flow that went on an FCF basis from over 2B SEK positive to negative 3.7B SEK , and CapEx almost doubling YoY.

Basically, every financial comparison is going the wrong way. It's easy to see why the company's shares were heavily punished.

{kind=link}

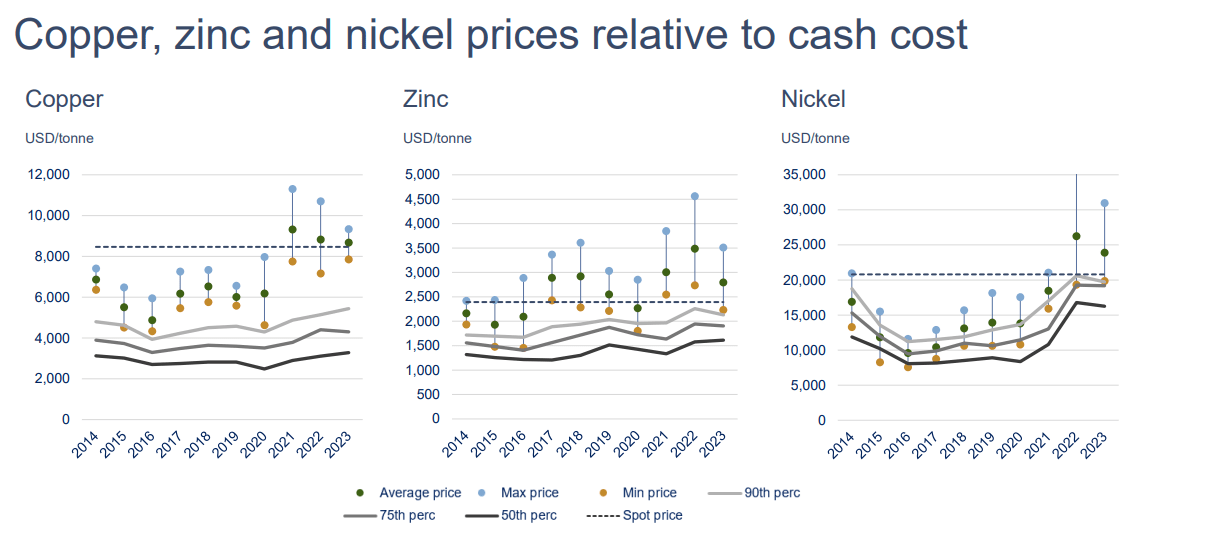

The drop-off you see here was remarkable, even in light of the expectations I had for the company. Obviously, metal prices were the major influence here. Zink especially is in a bad spot in terms of pricing - but declines in both sulfuric acid and declines in premiums, as well as the weak SEK/EUR , is putting significant pressure on a SEK-heavy business such as Boliden, which purchases a lot in EUR/USD.

Costs are increasing significantly.

{kind=link}

It's not that volumes were down massively. The mines and assets, including Aitik, Garpenberg, Kevitsa, and Boliden as well as Tara, are producing flat or at least comparable volumes. But the grades are down significantly, and the company's smelters aren't working at full capacity either due to a mix of fire and maintenance stops.

The results compared to both sequential and YoY results are so bad that one of the few upsides I see here is that it really can't get much worse in 3Q23.

{kind=link}

The macro trends are leading to a higher internal inventory not only in product but concentrates. The company, by the way, is also moving Tara into maintenance due to the negativity of current pricing.

The company's gearing/leverage level, as a result of this, is obviously also through the roof at current levels, higher than at any time during the last 4 years.

Boliden IR (Boliden IR)

The combination of these various factors affecting comparability are the company being in a worse/more negative situation than we've seen for many years. I expected further normalization from the company here. The current outlook also isn't very positive for this company - coming in at a high 15B SEK CapEx for the year, with lower EBIT and overall earnings for assets as well as shutdowns.

The question that I have for the company here is if these estimates are even low enough. Between inventory buildups, and grade reductions for several metals, including its "core" metals like Zinc, I expect even worse results and declines than we're seeing here. That's because even though the company has planned replacements for the lost Tara volumes, I don't believe it will be able to fully compensate or this - especially not with the grade issues that Boliden currently seems to be facing.

The grades are the main reason why volume is down.

Those of you not versed in mining might ask - what's the reason for this exactly?

And the reasons are numerous. The most obvious one usually is a depletion of, or shift from high-grade deposits, which forces the companies to access lower-grade ores, which in turn causes higher pollution and therefore, costs. That's the main reason why low-grade mining operations are far more environmentally harmful than high-grade mining operations. Of course, metallurgical technologies are also a factor here, as we modernize production, we're able to efficiently process lower grades of ores. But the drop in quality here across the board for Boliden was very noticeable.

While we continue to watch metal pricing trends, as I guided in my last Boliden article, I also believe it is important to watch the company's near-term performance. My hope is for a further decline in the company's results, which could set off a valuation chain reaction to where this company once again declines to very attractive levels.

If that happens, I intend to load up on Boliden for the long term. The company's current troubles notwithstanding, it's a major and possibly one of the best players in all of Scandinavia and Europe. For the long term, I see only one direction for this company to go. However, these recent trends have left a deep dent in what I expect for 2023 and 2024.

I now expect at least a 45% decline in EPS , based on these recent negatives. Granted, this is from a superb earnings level of almost 44 SEK/share. Most analysts are expecting this to pick up starting in 2024E again, I'm not so sure. The current forecast of 25%+ adjusted EPS growth for the business is one where I would say I could see it at 5-10%, and I'd want to see the next 2-3 quarters before going "deeper" here.

Boliden is not exactly expensive here, but given the recent set of troubles, I could see the business going down even more than we saw a few months and weeks back.

Let's look at valuation and see the upside for Boliden.

Boliden - The valuation upside does exist.

I deliberated for some time before deciding not to change my long-term PT for this stock. My last PT was below 300 SEK - I keep it at 300 SEK/slightly below at this time, despite the short-term trends potentially justifying a bit of a cut. If these troubles we're seeing here show themselves as persisting further, then I will cut my PT here.

Remember, my strike prices for my options are at the 265-285 SEK/level. That's where I consider the "sweet spot" for current investing in the company.

However, I don't kid myself into thinking the company can't drop further.

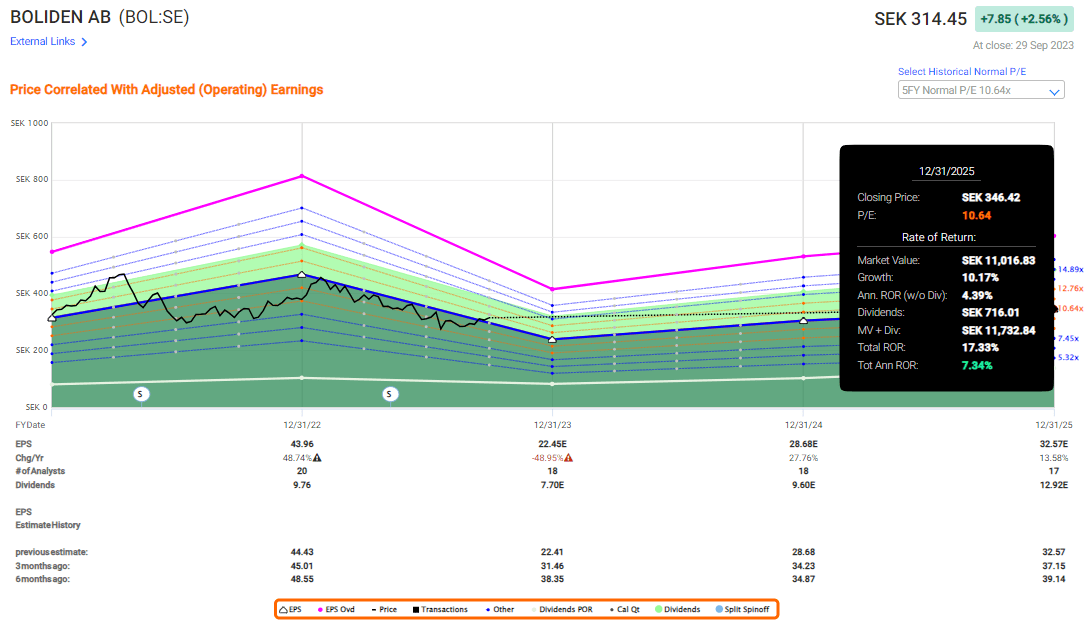

Boliden valuation comes to a high of 380 and a low of 257 SEK, with an analyst average of 310 (Source: S&P Global). However, out of 16 analysts, only 2 are at a "BUY". I am also not at a "BUY", despite the company almost, in terms of the average PT, being attractive. I believe strongly that now is a good time to "HOLD" and wait until we see more clearly where things are going.

You could argue that at a 15x P/E, the company has an upside of around 20% per year at the current set of earnings estimates, but you would be estimating this company with confidence and based on historical positives.

I say stick to the 10-11x 5-year normalized range, in which case your upside would look something closer to this.

{kind=link}

I don't need to tell you that this is not enough for me. We're not even talking double digits, and my minimum interesting RoR on an annualized basis is closer to 15% per year. This company does not meet this under conservative estimates or circumstances.

So I say "No" here.

I say that you better wait where the company goes in the next 2-3 quarters. I will keep an eye on Boliden and give you updates here, but what I want to see before going positive is either a significant discount or significant improvement in medium-term fundamentals.

The latter is not something I view as realistic, given that it's a macro question.

So, here is my thesis for Boliden as it stands now.

Thesis

- Boliden is a class-leading mining and metals company with an attractive overall upside if bought at the right price. It has the sort of solid fundamentals you want in an investment such as this and operates primarily in Northern Europe.

- Since COVID-19, the company has seen a significant expansion of profit and share price due to macro and pricing for metals - however, that is now slowly turning around, and a combination of cost and inflation pressures as well as a declining market will, I believe result in the company trading down over the next 3-4 years, not up.

- As of 2Q23, we've seen a continuation of this trend, with the company going down even further based on significantly more short-term problems than I expected for the company, including a fire, a mine closure due to pricing problems, and ore grade issues across the entire board.

- For that reason, I consider Boliden around fairly valued at this price with very little upside - a "HOLD", at best, with a PT of below 380 SEK, but even that gives you only a conservative upside of around 8% per year. I'd wait for a price closer to 300, where I also put my Boliden long-term PT - at 300 SEK or below.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

I would not consider Boliden to have a realistic upside at this time, or to be cheap, meaning I call it a "HOLD".

For further details see:

Boliden: The Thesis Is Playing Out As Expected