FCODF - Bollore: Continued Room To Run Following Asset Sales Tender Offer

2023-04-25 12:11:00 ET

Summary

- Three years ago, I wrote about my recent investment in Bollore, which has become among the most rewarding I have made.

- Following asset sales at favorable prices, Bollore's net asset value stands at about €14, implying a remaining discount of 55%, still quite favorable compared to typical discounts of 20%-40%.

- Forward returns will likely be less than the prior three years, but all of the factors in place then are still present to produce continued compounding.

Three years ago as the pandemic was beginning to rage, I wrote about a French conglomerate Bollore ( BOIVF ). The company at the time owned among its assets a freight forwarding division, an African rail and logistics network, a European energy distribution business, some battery and other alternative energy assets, and a large stake in Vivendi ( VIVEF ). Its peculiar and complicated structure has both attracted and deterred many investors, but what first interested me was that a number of very intelligent investors had mentioned the name, including Muddy Waters, Yacktman Asset Management, Bireme Capital, and GreenWood Investors, and Woodlock House.

I first became aware of Bollore in 2018, but it took me so long to understand its complex web that I did not buy shares until 2020. That was fortuitous as the pandemic had caused shares in most all companies to sell off and presented a phenomenal entry point. In USD, shares were then trading at $2.76 and have since increased 153% to nearly $7. Ignoring dividends, that's equivalent to annual return of about 38%.

In this article, I would like to give an update on Bollore's recent moves, provide an updated view of net asset value and how much upside is still left in the shares, as well as share some reflections on the past three years of ownership.

Inching Towards Simplification

If you are not deeply familiar with Bollore, I would encourage you to read my prior article. Basically, Bollore's "Breton Pulley" structure is both pyramidal (there are a series of entities that own large stakes in each other along a chain) and circular (Bollore, for example, owns large stakes in entities upstream from it in the chain). This means truly understanding the net shares outstanding for Bollore can be quite difficult. At year-end 2022, a total of 2.93 billion shares were nominally outstanding. But, the circular ownership means that Bollore self-owns something close to 53% of itself, implying that the true, economic net shares outstanding is probably about 1.38 billion by my own estimate.

Illustration of Bollore group structure (share structure and main assets) from Bollore 2022 Results Presentation. (Bollore 2022 Results Presentation)

There has been no major simplification in the last three years in the sense that a major collapse has taken place of the pulley system. But, incremental moves towards opportunistic value creation and simplification have been happening.

Universal Music Group ( UMGNF ) may have been the first example of that. The company was sitting wholly within Vivendi and had been rapidly growing in valuation as streaming lifted the fortunes of the entire industry. Then, in two transactions in 2020 and 2021 , Tencent ( TCEHY ) entities acquired 20% of UMG for €6 billion. Bill Ackman's Pershing Square subsequently purchased another 10% for about $4 billion and UMG was listed in Amsterdam in an IPO. Today, the market cap of the company is close to $42 billion. Due to some share distributions by Vivendi as well, ownership within the Bollore structure was also shifted somewhat so that today Bollore owns 17.7% of UMG, Vivendi retains 10% ownership, and Compagnie de L'Odet ( FCODF ) owns 0.3%. The moves highlighted the tremendous value of the asset as well as freed up a lot of cash, particularly at Vivendi, whose subsequent moves I won't go into as deeply.

Outside the media assets, transportation was the most important operation for Bollore a few years ago. But, both the African transport and logistics business and the European freight forwarding business have now been or are in the process of being sold. The sale of the African assets was completed to MSC Group at an enterprise value of €5.7 billion last December and just recently an agreement to sell the freight forwarding business was completed with CMA CGM for €5.0 billion.

All the while, Bollore has been buying back some shares in various ways throughout the pulley system. This has been most noticeable at the Odet entity, which now owns about 67% of Bollore, up from 64% at the time of my first article. Prior to announcement of the sale of the freight forwarding business, Bollore announced a tender offer of its own shares at €5.75 per share for up to about 9.8% of all shares outstanding. The offer has since been revised so that an additional €0.25 per share will be paid if the deal with CMA CGM is completed.

Quite obviously, the new tender offer is extremely bullish for shares of Bollore (shares are already trading higher than potential €6 per share payout), but the benefits to shareholders will depend a great deal on how many shares are actually tendered. Following Odet's 67% ownership of Bollore, the largest shareholders are Yacktman Asset Management (with about ~7% of shares) and Orfim SAS (~5% of shares). It is my understanding that Odet, Yacktman, and Orfim are all not participating in the tender offer. That would imply that close to half of remaining shareholders would need to tender shares for the offer to be fully subscribed. Given where shares are trading today, that will not happen. Still, as the very smart Fox Castle Holdings recently posted on Twitter, this may not be the worst thing in the world.

Updated Net Asset Value

The tender offer has also come with a fairness opinion by an independent expert. You can review that document here .

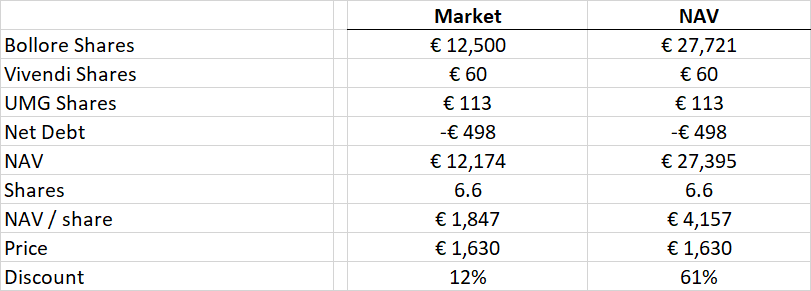

Although different scenarios are presented, the opinion produces a net asset value for Bollore of about €9 per share, but this is far too conservative. The primary reason is that Bollore's circular shareholding in Odet is valued at its market price, despite the fact that the shares it holds in Bollore trade at a discount to net asset value and that Odet itself trades at an additional discount. Using many of the assumptions that the independent expert uses (with some tweaks noted below) and removing the value of "controlled holding companies" and instead using the estimated net shares outstanding, I estimate current net asset value at about €14.

Bollore estimated net asset value. Figures are in millions, except shares outstanding (in billions) and per share amounts. (Author)

A similar calculation can be done for Odet, both using the Bollore market price and the Bollore net asset value to find the current discount.

Compagnie de L'Odet net asset value versus current share price. Values are in millions except shares outstanding (in billions) and per share amounts. (Author)

{kind=link}

When I first wrote about Bollore three years ago, I estimated the net asset value discount to be 70% and the net asset value to be €8.28 per share. That means that some of the gains over the prior three years have come from a narrowing of the discount, but a very large percentage of them have come from increases in net asset value itself, which has compounded at about 19% per year in euros.

A 40% discount to net asset value today for Bollore today would produce a share price of €8.44, upside of 33% to the current price. Odet shares would need to rise 53% to get to that mark.

Reflections On Ownership

The shareholder base of a company is an often overlooked factor in the success of an investment and the company. Lawrence Cunningham wrote a book a few years ago about this fact called Quality Shareholders: How the Best Managers Attract and Keep Them.

Aside from the fact that a quality shareholder base can help reinforce a company's culture, it can also help make the ownership experience more enriching and rewarding. The quality shareholders of Berkshire Hathaway over the years have been one of the appealing aspects of that investment, not only in reinforcing the culture that Warren Buffett wanted to build, but in the community of investors that share a desire to compound knowledge over time and share a set of common values.

In a similar sense, I have found the other investors in Bollore entities to be intellectually curious, attracted to how the puzzle has been and will be put together and also driven by a shared sense of intelligent investing and a huge amount of generosity in sharing research and perspectives. The experience has certainly reinforced my feeling that the quality of the shareholder base is an important factor in selecting an investment.

The other important reflection noted above is the source of returns over these past few years. Three years ago, I said the following:

The biggest risk of a Bollore investment is that precisely that continues to happen much longer into the future and investors capture nothing but the fluctuation in net asset value. As far as downside risks go, this one is not that large.

Despite building a significant part of the thesis on a narrowing of the net asset value discount, a little less than half of the returns have come from that narrowing. More than half, meanwhile, has come from the compounding of net asset value. Bollore thus far has been the kind of dual threat investment that investors are always looking for - extremely strong and opportunistic capital allocation driving double digit returns and priced dramatically less than its true value. But, as time goes on it is the capital allocation and growth in net asset value that will matter so much more to Bollore shareholders than a narrowing of the discount.

Three years on, the story is still somewhat similar. Although I am skeptical that the €6 per share tender offer will result in many shares being bought back, I think it does provide something of a floor under the stock. Although Vincent Bollore is incredibly patient, recent moves to buy back shares and make opportunistic asset sales also seem to validate the thesis that ever so slowly he is moving towards greater simplification, unlocking the remaining value within its unique structure.

For further details see:

Bollore: Continued Room To Run Following Asset Sales, Tender Offer