BDRAF - Bombardier: What's Next After Bog Surge?

Summary

- Bombardier stock has been on a roll as management tracks well on targets.

- Bombardier reduced its net debt significantly during the year and saw results improve further.

- Further upside exists as margin expansion has still to fully materialize and demand remains strong.

Bombardier ( BDRAF ) has seen a remarkable turnaround as the company focused on its business jet segment. As a diversified business previously, the company grew rather inefficient, and the company compounded debt for its C Series program, which it never really got any benefit from. The current management is tasked with bringing the debt down and optimizing the business, and they are doing that well, as I show in this report discussing the full year results for Bombardier.

Bombardier Stock: Impressive Share Price Return

Share price performance Bombardier (Seeking Alpha)

The turnaround plan of Bombardier has been rather simple, optimize and expand the business and use the proceeds to deleverage. The big question, of course, was will the company be able to execute. Even more so given the fact that its previous turnaround plan was a rosy one but ultimately fell apart. So, I'd say that some hesitance was built into the share price and as management kept on delivering that hesitance dissolved resulting into significant share price appreciation.

{kind=link}

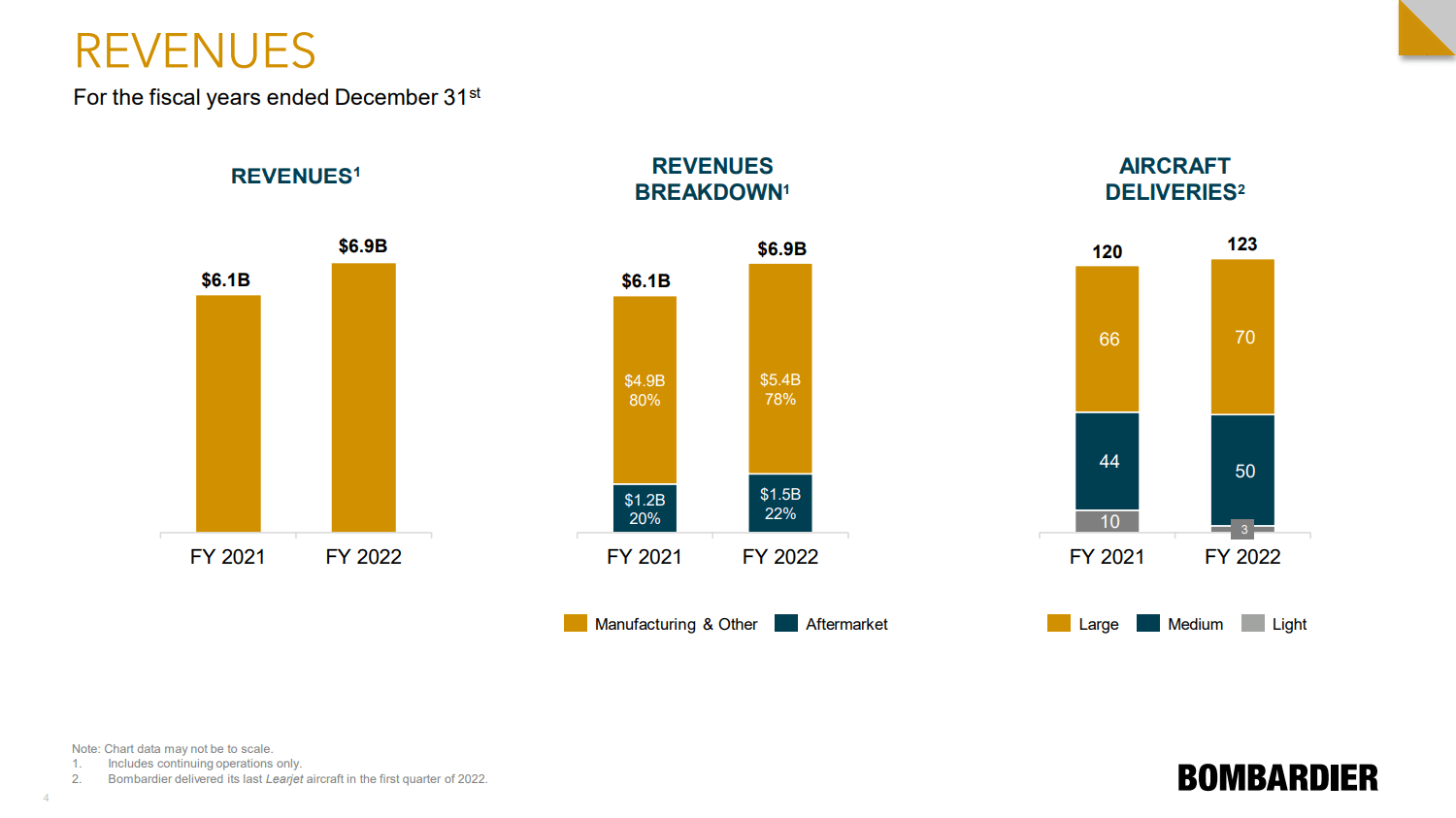

From a revenue perspective, we see that things have been significantly better year-over-year, with a 14% growth in revenues. That was achieved while delivering only three aircraft more compared to 2021. However, aftermarket sales had a significant contribution with sales growth of 22% while manufacturing sales grew by 10%. Obviously, a lot of the aftermarket sales were driven by a significant improvement in flight hours and that also means that, just from a flight-hour perspective, there is a limit to how much sales can further improve. However, Bombardier has significantly expanded its services footprint with opening new MRO facilities globally over the course of 2022. A few examples are facilities in Miami and London, with more to come in 2023. Those facilities take up to 18 months to ramp up, so we are seeing that the foundation for higher services sales has already been laid, and with more to come, the company is also positioning for the future to capture a bigger market share for after-sale services.

On manufacturing, the big positive is that the company has shifted its focus to large- and medium-sized business jets, which obviously bring in higher revenues. So part of the improvement in deliveries is also driven by an improved delivery mix.

{kind=link}

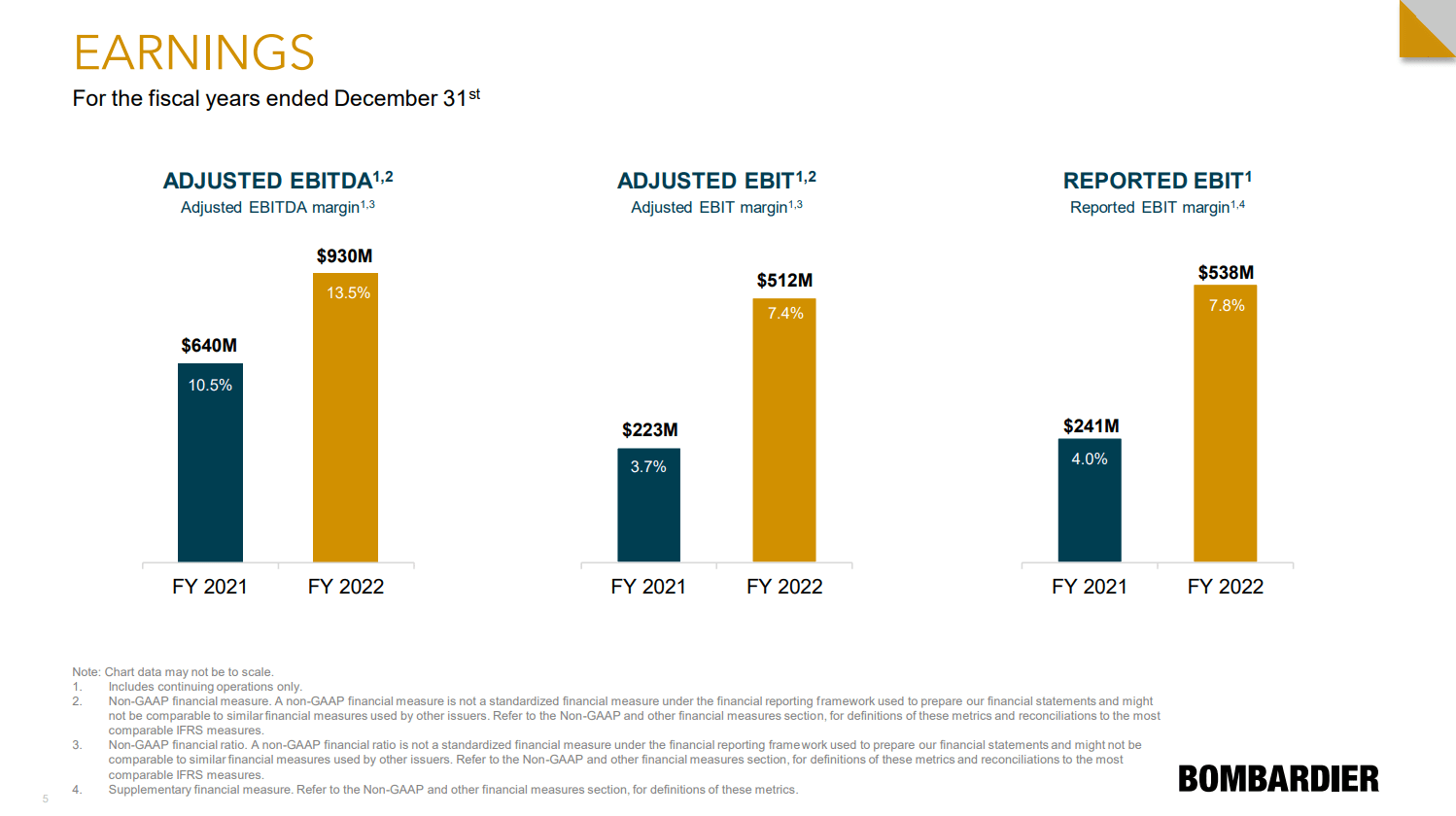

What I can appreciate about Bombardier's turnaround is that they went from not being able to look ahead a few quarters at a time at most to being able to make investments for the future and, overall, the company's strategy is also on display in the results with earnings growth outstripping revenue growth. Adjusted EBITDA grew by 45%, while adjusted EBIT grew by 130% and reported EBIT grew by 123%. While there was solid topline growth, we also see that margins improved significantly year-over-year, reflecting business optimization. In March 2021, Bombardier provided adjusted EBITDA target margins of around 20% by 2025, and we see that the company is already at 13.5% now despite labor cost and material billing headwinds.

Putting Cash To Good Use

{kind=link}

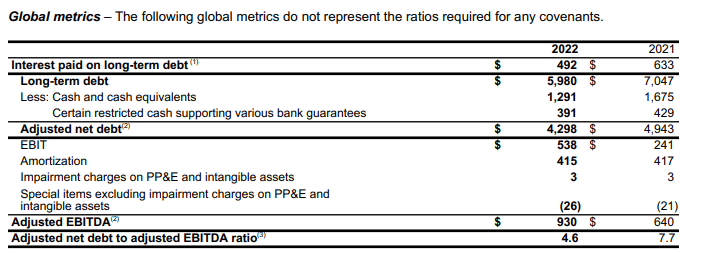

Year over year, available liquidity went down, but I don't consider it a bad thing at all. During the year, Bombardier generated $735 million in cash compared to $100 million a year earlier, allowing the company to retire $1.1 billion in debt. Furthermore, in January of this year, the $391 million in restricted cash came available due to two bank guarantees expiring without being drawn. This excess cash can be deployed to bring the debt down further.

{kind=link}

As mentioned, the liquidity going down is not a bad thing for Bombardier. Previously, the company was paying interests that exceeded the free cash flow and that basically did not allow the company to pay off any debt. That is different now. Interest payments are now lower than the free cash flow, and scheduled interest payments have declined from $524 million to $442 million. Since 2020, annualized interest costs savings due to paying off debt and retiring debt early with cash available and cash from operations has come down by over $300 million. So, the liquidity might be down for the year but that is because Bombardier is retiring debt and saving on interest costs which can be used to retire even more debt.

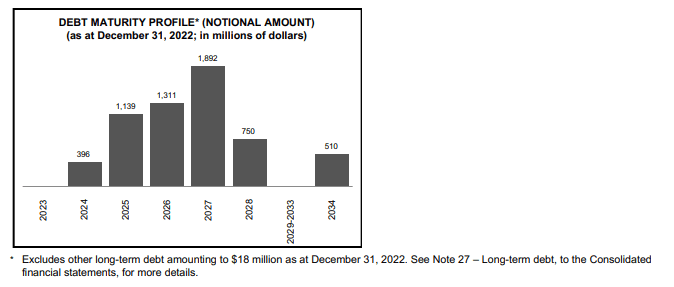

Bombardier has no debt maturing in 2023 and while the company does not have the two-year debt-free runway I am looking for, there is no reason for concern at all. The current available liquidity covers the debt requirements as of December 31, 2022 for 2024-2025 and then some. More importantly, while interests have been rising, Bombardier has been able to refinance some debt at stable rates. That debt is now due in 2029 and the proceeds will be used to retire the 2024 debt and Senior Notes up to $354 million due in 2025. So, we are seeing that Bombardier is reducing debt, but it is also able to refinance at attractive terms.

Guidance And Longer-Term View

{kind=link}

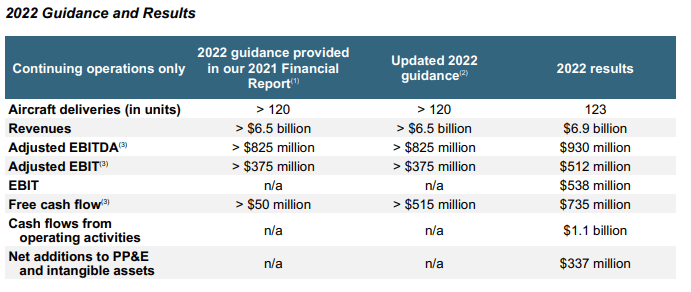

Looking at 2022, we see that Bombardier met its guidance. Net additions to property were a bit higher than what the company unofficially guided for, but on all other metrics, we saw results exceeding the minimum amount significantly. In some way, it is quite unfortunate that the company only provides a lower bound in the guidance. Especially, for free cash flow, we see that $50 million was guided for and $735 million was achieved. This was driven by strong business performance and very strong order intake.

{kind=link}

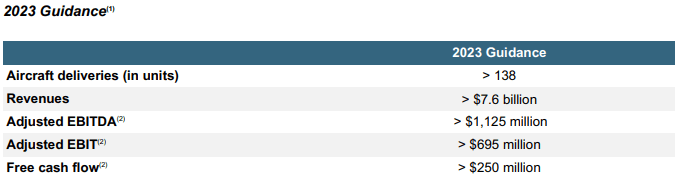

For 2023, Bombardier guides for more than 138 deliveries, which currently is primarily capped by supply chain challenges. Revenues should come in at $7.6 billion, with $1.6 billion to $1.7 billion or around 22% coming from aftermarket sales. With the 2025 target of $2 billion in aftermarket sales, things are looking good for Bombardier with more facilities ramping up, increased flight hours, and market share expansion. The free cash flow guide of higher than $250 million is lower than what Bombardier achieved in 2022, but it should be noted that last year the company guided for a free cash flow of $50 million at the start of the year. Bombardier will need a strong order intake to replicate last year's free cash flow, but I believe we should be able to at least expect around $650 million in free cash flow calculated from the adjusted EBITDA guidance with higher additions to PP&E and higher residual value guarantees payment this year. While I do appreciate Bombardier not providing rosy pictures just to please investors like it did in the past, my feeling is that the current guidance has way too much wiggle room, and the company is not providing sufficient sight on sensitivity of the free cash flow guide to certain dynamics such as order intake.

Nevertheless, the guidance suggests 10% revenue growth with 21% adjusted EBITDA growth and 36% growth in adjusted EBIT. So, I don't see a reason to be less optimistic on Bombardier's trajectory, even though one might note that the year-over-year growth is tapering.

Deleveraging Is Going Fast

{kind=link}

The goal of Bombardier is to deleverage. It set itself the goal to have 3x net debt to EBITDA. Net debt came down by $645 million year-over-year. There is no target for adjusted net debt for 2023, but if the company's net debt does not improve, it is still set to improve its leverage to 3.8x for 2023. Assuming that net debt reductions of 2022 can be replicated, the leverage could even be as low as 3.3x. So, the way things stand now with a growing services footprint, better business jet delivery mix, and business optimization, I do believe that Bombardier is able to deliver on its 2025 target and possibly achieve those goals earlier than anticipated.

Conclusion: Upside Remains For Bombardier Stock

After share prices have surged more than 200%, you might wonder what is left for Bombardier. While year-over-year growth rates might be tapering somewhat, I believe that based on the current leverage shares should be trading at $57 providing at least 17.5% upside. Furthermore, with the targets in place, this company could grow to $1 billion in free cash flow by 2025. So, there is still a lot of value that can be generated.

While the company previously took its company to the chopping block to reduce debt, it is now not in that position, and it has not impaired its product or ability to develop a product to improve the financial metrics. As a result, the company is able to deleverage and, at some point, it can consider deploying cash for a new business jet product if the market demands it, or it can return the cash to shareholders. The company also does not require additional investments for new production facilities if it wants to increase production. In fact, it has the footprint to produce up to 200 jets if the market demands it, and we see that with investments in an Abu Dhabi bases service facility, the company is positioning itself for growth beyond 2025.

For further details see:

Bombardier: What's Next After Bog Surge?