SPTS - Bond Ladders Look Attractive Today With TIPs

2023-09-21 09:20:24 ET

Summary

- Investors Perceive Inflation to be a Key Retirement Risk.

- TIPs are Now Priced to Generate Real Yields of Nearly 2.0%.

- The Cost of Constructing a TIPs Bond Ladder has Fallen Considerably.

- TIPs Bond Ladders Can be a Good Compliment to Social Security Income.

Interest rates remain high even as inflation abates in the US. All indications are that elevated rates will prevail well into next year. Reduced bond prices indicate yields to maturity well above expected inflation rates. That could be advantageous to retirees.

Resurgent yields among Treasury Inflation-Protected Securities (TIPs) provide an intriguing opportunity. Bond ladders have long been touted as a safe way to lock in cash flows for investors. However, systematically repressed interest rates after the Great Recession dulled investor appetite to use bonds to generate income. That situation has changed in the past 18 months. High bond returns and renewed investor concern over inflation have put bond ladders back on the table.

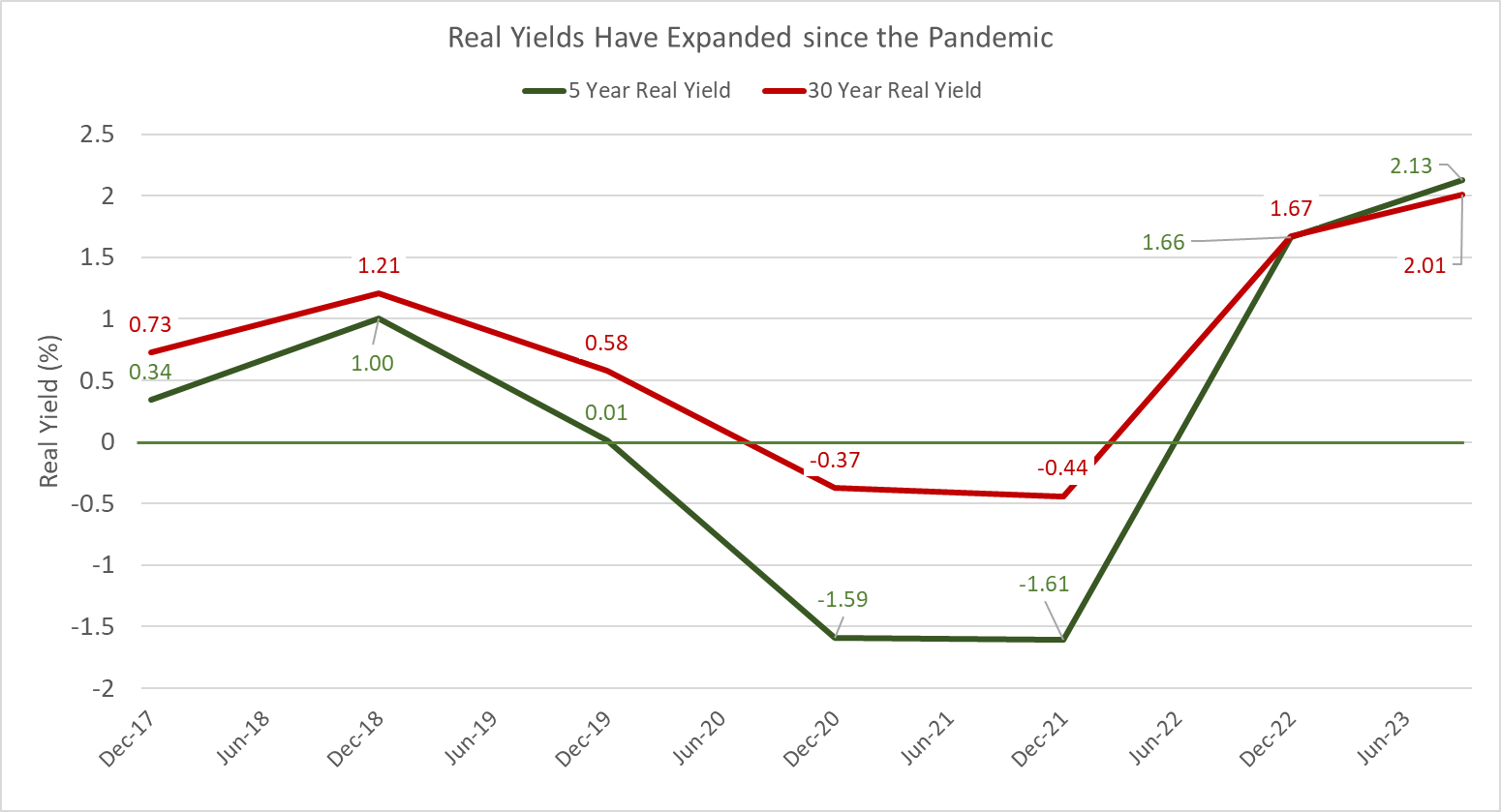

The following chart tracks the real yield offered by TIPs at the 5 year and 30 year maturities. Note that the Federal Reserve slashed rates drastically during the Pandemic. Since then, our central bank has pursued a strategy of reducing inflation through aggressive monetary policy - pushing real yields above 2.0%

{kind=link}

US Department of the Treasury

The TIPs market in the US dates only to 1997 but has grown rapidly. They are currently issued in maturities of 5, 10, and 30 years. There are nearly $2 trillion bonds outstanding - not a niche investment. Unlike regular fixed coupon treasuries, TIPs' underlying principal scales semi-annually based on measured changes in the CPI.

TIPS have often been faulted for poor near term correlation to price changes. Indeed, there is a lot of noise in short term TIPs price movements. However, the structure of individual TIPs makes them a good hedge - if they are held to maturity . Interest payments and principal adjust with the CPI every 6 months. That's not perfect but about as close as a financial security can get. Here is a simple illustration from The Balance .

Suppose the Treasury issues an inflation-protected security with a $1,000 face value and a 3% coupon. In the first year, the investor receives $30 in two semi-annual payments. That year, the CPI increases by 4%. As a result, the face value adjusts upward to $1,040.

In year two, the investor receives the same 3% coupon, but this time it’s based on the new, adjusted face value of $1,040. The result: instead of receiving an interest payment of $30, the investor receives interest of $31.20 (.03 times $1,040). In year three, inflation drops to 2%. The face value rises from $1,040 to $1060.80, and the investor receives interest of $31.82.

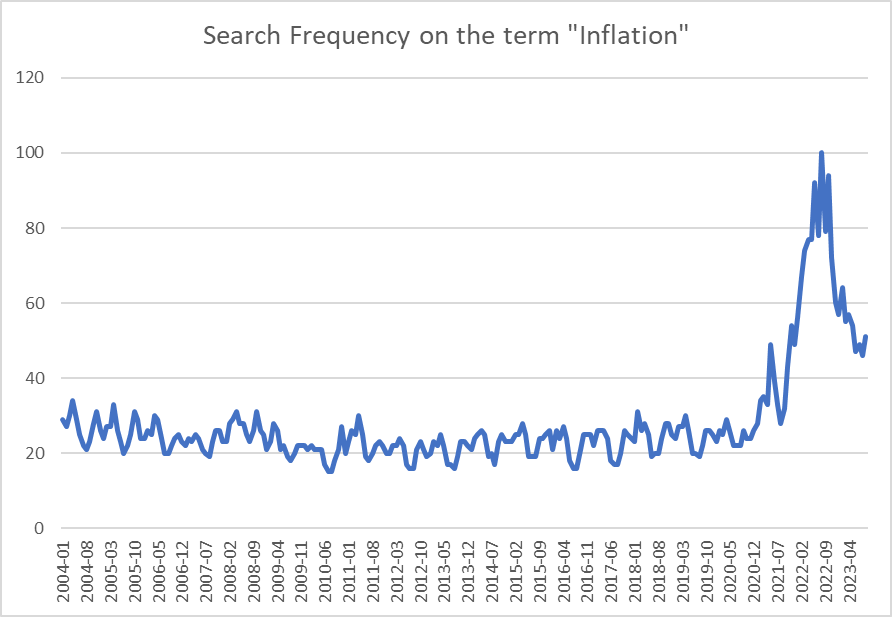

Until recently, inflation concerns were an afterthought among American investors as expectations remained anchored near 2%. Both the general level of inflation and its volatility have increased in the past 18 months. As a result, the investing public has demonstrated renewed interest in protection against price increases. Google Trends below offers a basic insight into heightened interest via the number of user searches on "inflation".

{kind=link}

Google Trends

In the 21st century, the TIPs market is quite liquid. TIPs are available today at all maturities save for a "doughnut hole" between 2034 through 2039. No thirty year TIPs were issued in the mid 2000s. The good news is that the Treasury auctions 10 year TIPs regularly. The doughnut hole in TIPs maturities will thus be filled ten years in advance via new issues.

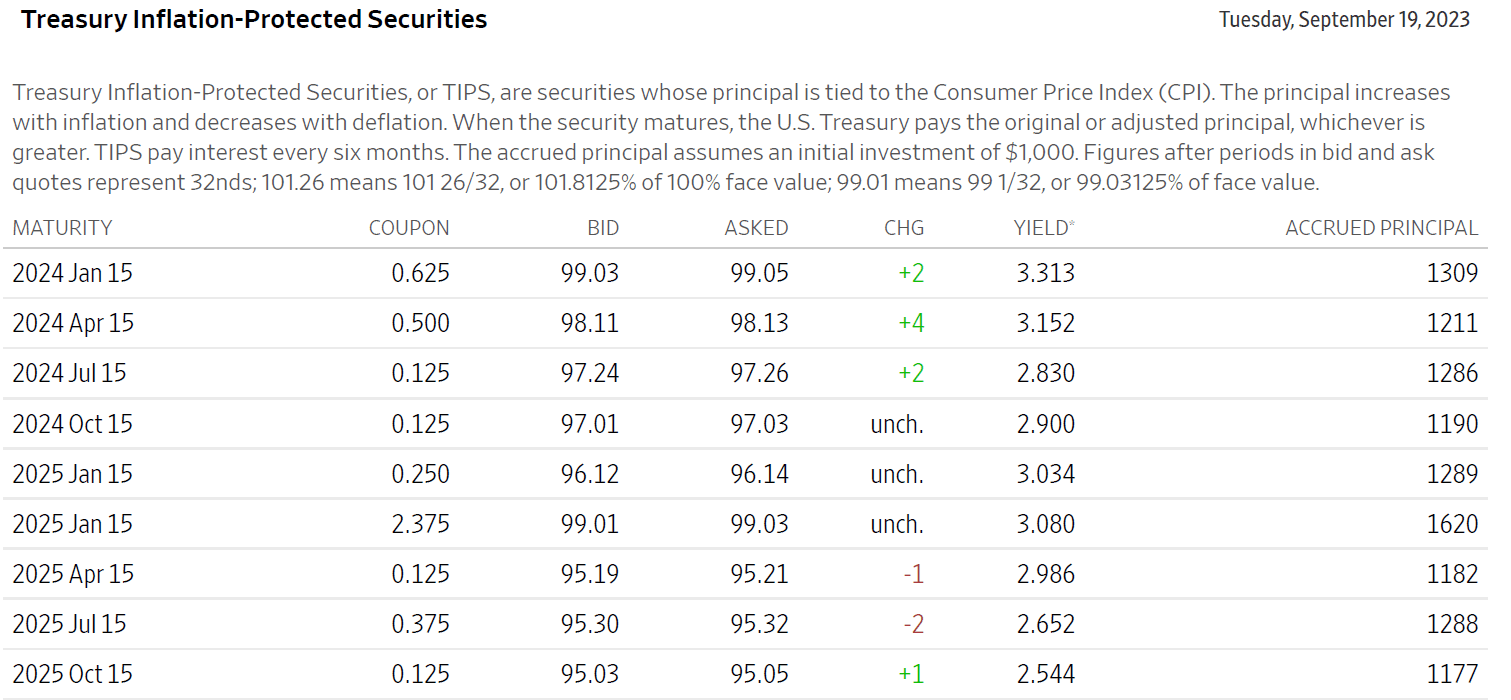

Here's an example of the near end of the TIPs market as described by the Wall Street Journal. Note that bid/ask spreads are within a 2/32 of one another and that prices are well below par value.

{kind=link}

Wall Street Journal

Assume that we want to create a bond ladder for the next 30 years, with each rung generating $10,000. We work backwards and make the simplifying assumption that interest is paid annually. Start with buying a TIPs with a current face value of $10,000 maturing in 2053. That year is pretty easy to fund. For year 29, we'll have to back out the interest generated by the first bond. Assuming that real interest rates are 2.0%, that amounts to $200. We'd only have to buy $9800 of the bond maturing in 2052. The balance of the bond ladder is implemented by continuing to work backwards.

To mitigate the risk posed by the "doughnut hole" in TIPs maturities, the investor can add TIPs positions maturing on either side of the gap (2033 and 2040) while reserving the right to redeploy as new 10 year TIPs are issued that mature during the currently barren period.

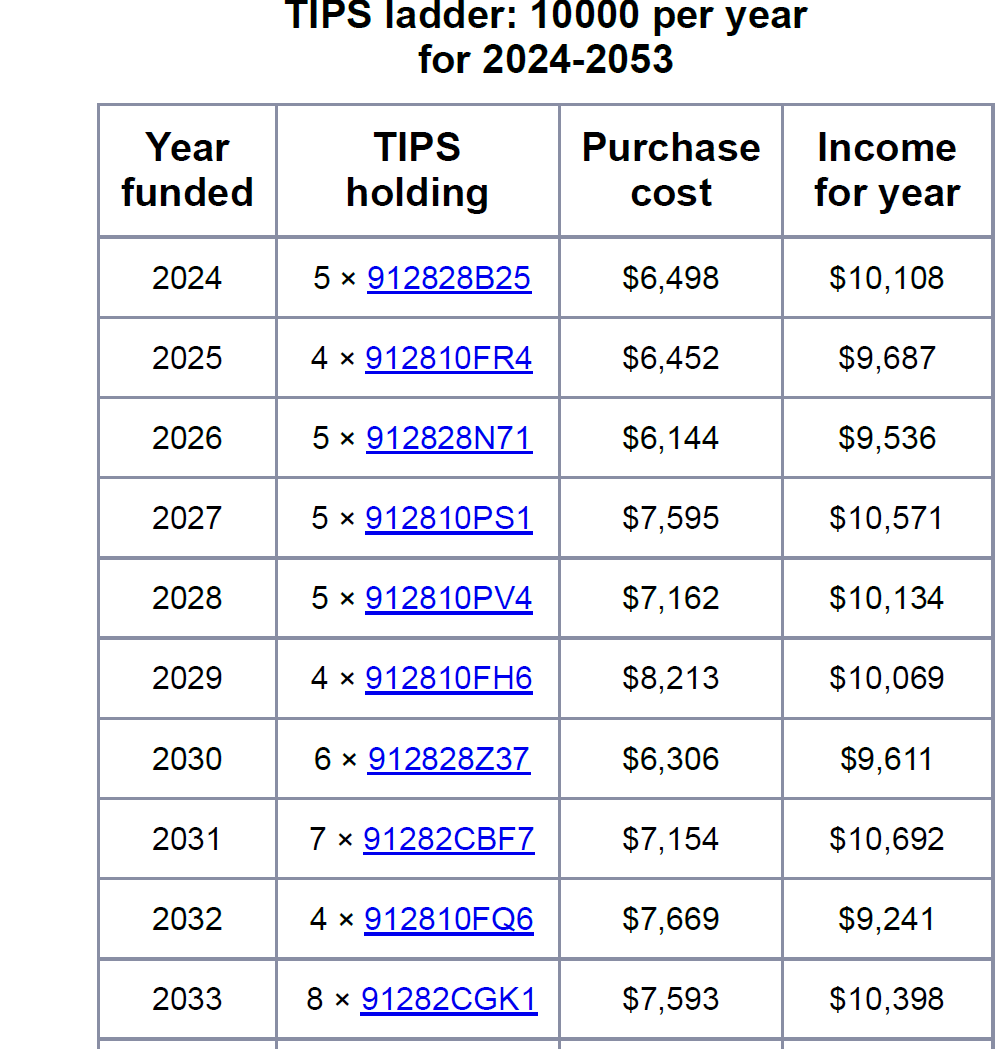

There is a free tool available at www.tipsladder.com that provides an initial draft of the TIPs you'll need to buy to fund a TIPs ladder. I ran it for the scenario above and the results indicated that the bond ladder could be funded for about $224,000.

There is some intuition here worth noting. Real yields are about 2.0% and they operate for an average of 15 years (30 years/2). The $300,000 ($10,000 x 30) aggregate outlay can be discounted by 34% (1.02^15-1). Some basic division follows ... 300,000/1.02^15 = 223,000. Pretty close. With the negative yields of about 1% that prevailed in late 2021, we can use the same intuition to reprice the bond ladder at 300,000/0.99^15 = 349,000. That's a significant increase in cost relative to today.

Here is a partial snapshot of the output. Users can obtain greater detail at the website after they input their own requirements. CUSIPs of the bonds are provided and current pricing information is utilized. Not a bad start to building the bond ladder.

{kind=link}

www.tipsladder.com

A cautionary note. The TIPs ladder is fully amortizing. There is no anticipation of any residual value once the ladder is exhausted. It doesn't pay indefinitely like social security of life annuity payments. That said, the 30 year time frame is a practical retirement horizon for many investors. Some individuals may want to fund early stages of retirement with shorter bond ladders of 10 or 20 years. The methodology is flexible.

For further details see:

Bond Ladders Look Attractive Today With TIPs