DIA - Bond Market Expectations: Slow Growth And Moderate Inflation

2023-08-16 19:22:14 ET

Summary

- Investors expect the U.S. economy to grow at a modest rate of less than 2% per year for the next five to ten years.

- Inflationary expectations in the bond market for the next five to ten years are around 2.25% to 2.30%.

- The investment community believes that the Federal Reserve will bring the inflation rate close to its target of 2.00% in the coming decade.

- But, are these numbers good enough?

It has been a while since I looked at the expectations that investors have built into the current bond prices.

The basic procedure here is to look at the nominal rate of interest and then divide this rate into what investors seem to expect in future economic growth and what the investors seem to expect of future inflation.

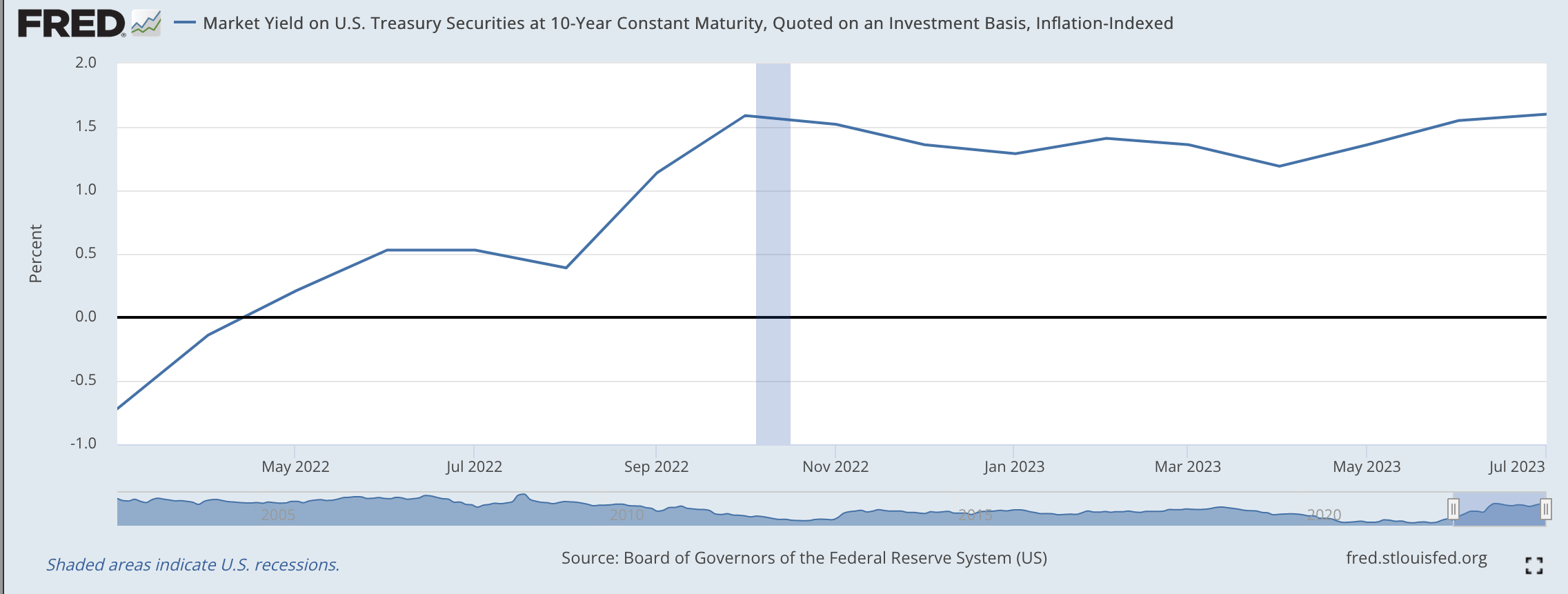

The expected rate of growth is assumed to be what the investment community foresees in the yield on the Treasury's inflation-protected securities. For example, in the first half of August 2023, the average yield on 10-year U.S. Treasury Inflation-Protected securities, or, TIPs, was right around 1.70 percent.

The average yield on 5-year TIPs was around 1.85 percent.

So, for the next five to ten years, investors imagine that the U.S. economy will grow only very modestly, somewhere less than 2.00 percent per year.

The inflationary expectations that are built into bond prices are obtained by subtracting the yield on the TIPs from the nominal yield in the marketplace.

So, for the early part of August, the nominal yield on the 5-year U.S. Treasury note (US5Y) was around 4.15 percent. Subtracting the yield on the 5-year U.S. TIPs, which as noted above was 1.90 percent, from the nominal yield, we estimate that the compound annual rate of inflation for the next five years will be around 2.25 percent or about 225 basis points.

For the 10-year Treasury (US10Y), the nominal yield, the nominal yield in early August was around 3.90 percent and the "real rate of interest," the yield on the TIPs, was around 1.60 percent, so that the compound annual rate of inflation built into the bond prices, i.e., inflationary expectations, was around 2.30 percent.

So, currently, inflationary expectations of investors in the bond market for the next five to ten years are in the neighborhood of 2.25 to 2.30 percent.

It appears as if the investment community sees the Federal Reserve maintaining a rate of inflation that is not too far above its target rate of inflation, which is 2.00 percent.

Not bad.

Expected Real Economic Growth

Let's take a look backward and see how we got here.

I am going to start this analysis in March 2022 the month that the Federal Reserve began to tighten up on its monetary policy.

In March 2022, the investment community had built into the future a period of negative real economic growth. In March 2022, the yield on the 5-year TIPs was at negative 1.30 percent and the yield on the 10-year TIPs was just around negative 0.70 percent.

Investors were seeing a recession in the future of the U.S. economy and, that the recession would be a relatively severe one to keep the compound rate of interest on these TIPs below zero for five years and 10 years.

But, things started to change.

{kind=link}

The picture here is of the U.S. economy picking up speed during this time period, but the best the economy seems expected to do over the next 10-year period is to grow at a compound rate of about 1.5 percent.

Roughly the same picture is achieved for the yield on the 5-year TIPs.

So, the investment community sees the economy growing through the next decade but growing at a very modest pace.

Note, however, that this expected performance is not that much different from the performance of the U.S. economy during the period of economic recovery following the Great Recession which ended in 2009. The compound annual growth rate from the end of the Great Recession up until the start of the Covid-19 recession was around 2.2 percent to 2.3 percent.

This rate of growth was not what was hoped for during this time period. As I have explained in many different posts , it seems as if the U.S. economy had a productivity lag during this decade and the growth of labor productivity really lagged during the time.

It seems as if this concern about the growth of labor productivity has carried over into the decade of the twenties.

Investors expect that the economic growth during the decade will be modest.

This future will be discussed at greater length in upcoming posts.

Inflationary Expectations

Investors appear to be expecting that the Federal Reserve is going to get inflation under control and bring it close to its target goal of 2.00 percent.

Here are the figures for inflationary expectations over the next five years and the next ten years as they are calculated from the market rates of interest.

Inflationary Expectations

Five-Year Expectations Ten-Year Expectations

March 2022 3.40% 3.50%.

Second Quarter, 2022 2.90% 2.70%.

Third Quarter, 2022 2.50% 2.60%.

Fourth Quarter, 2022 2.35% 2.30%.

First Quarter, 2023 2.30% 2.30%.

Second Quarter, 2023 2.30% 2.20%.

August 2023 2.20% 2.30%.

So, the investment community has moved along with the Federal Reserve's actions and talk and now seems to believe that the Fed will actually bring the inflation rate down close to the Fed's target of 2.00 percent.

Investors don't seem to feel that the Fed will get the rate all the way down to the target because these numbers are compound rates of change and not averages.

But, the important conclusion to draw from this picture is that the investment community seems to believe that the Fed will actually keep the inflation rate near the target rate for most of the next decade.

Conclusion

The conclusion one can seem to draw from these data is that the coming decade will not be much different from the decade of the 'teens.

Economic growth in the 2010s was lower than policymakers desired at came in at around a 2.2 percent compound rate of growth for the decade. In this respect, it was not a "bad" decade. It is just that we all would have liked to see a little higher rate of growth during that time.

Unemployment turned out to be the lowest in the post-World War II period. Not bad!

And, inflation, as mentioned above, came in at about a 2.2 percent compound rate of increase during the 2010s. Policymakers were very happy about this number.

So, right now investors are forecasting a future for the 2020s that is not too different from the decade of the 2010s.

I think that most, in the modern U.S. economy, would be happy if the inflation rate for the decade came in around 2.2 percent, especially with the projections people are making about the fiscal programs they see coming from the federal government.

People, however, will not be happy with an economy that is only growing at a 1.5 percent compound rate for the decade.

What will be done about this is unknown right now.

In my view, coming from the evidence of the 2010s, the economic growth problem is a supply-side problem and will require some re-education of the policymakers.

But, we will be discussing this issue a lot more over the coming months and years.

For further details see:

Bond Market Expectations: Slow Growth And Moderate Inflation