BOND - BOND: Reiterate Buy On Bullish Outlook For Bonds

2023-12-28 13:12:55 ET

Summary

- The PIMCO Active Bond ETF has outperformed passive bond ETFs with a 2.0% total return since the previous article vs. 1.7%.

- The BOND ETF has reduced credit exposure and increased exposure to mortgage-backed securities due to attractive mortgage spreads and unattractive credit spreads.

- The Fed's shift to a dovish stance and potential rate cuts provide a favorable outlook for the BOND ETF.

A few months ago, I wrote a positive review of the PIMCO Active Bond Exchange Traded Fund ETF (BOND), noting that the BOND ETF has a history of modestly outperforming passive bond ETFs. Since I was bullish on the prospects for bonds following the regional bank crisis in March, I rated the BOND ETF a buy.

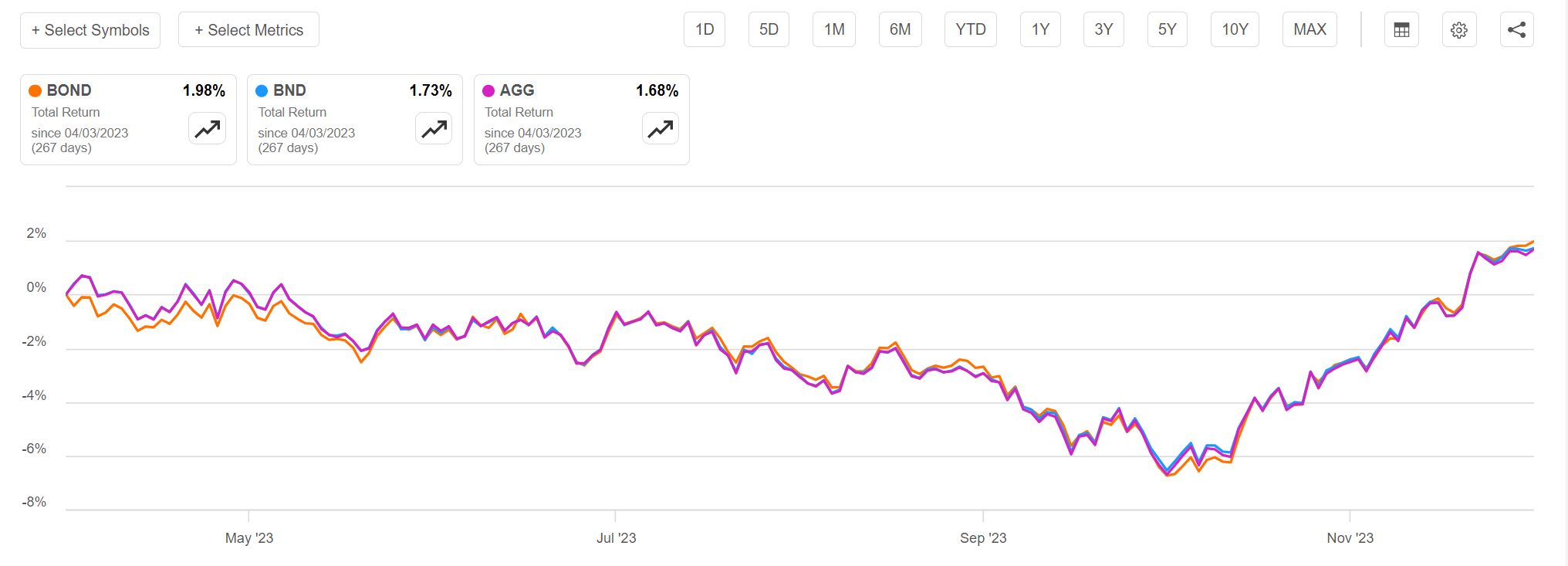

Measured from the date of my article, the BOND ETF has delivered 2.0% in total returns, modestly ahead of aggregate bond ETFs like the Vanguard Total Bond Market Index Fund ETF (BND) and the iShares Core U.S. Aggregate Bond ETF (AGG) at 1.7%, so the BOND ETF has definitely lived up to my expectations (Figure 1).

Figure 1 - BOND has outperformed BND and AGG as expected (Seeking Alpha)

{kind=link}

As we close the chapter on 2023, I want to take the opportunity to refresh my thesis on bonds and the BOND ETF going forward.

Brief Fund Overview

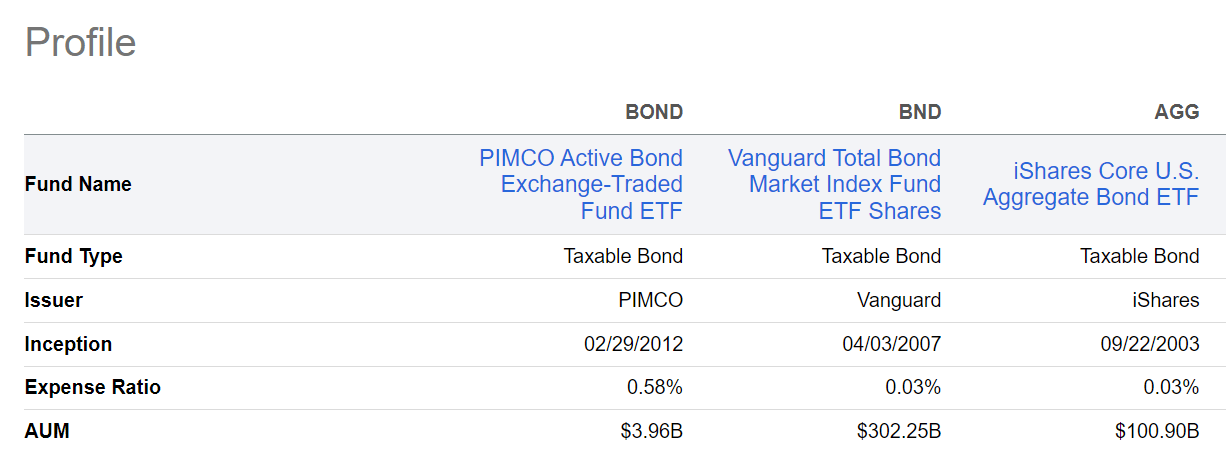

The PIMCO Active Bond ETF is an actively managed bond fund with a flexible mandate, allowing the seasoned fund managers at PIMCO to invest outside of the benchmark assets to earn higher risk-adjusted returns.

The BOND ETF is considered a higher risk but with commensurately higher potential returns within PIMCO's ETF offerings (Figure 2).

Figure 2 - BOND overview (pimco.com)

However, investors also have to pay for the privilege, as the BOND ETF charges a relatively expensive 0.58% expense ratio, far higher than the passive BND and AGG ETFs (Figure 3).

Figure 3 - BOND ETF charges far higher expenses (Seeking Alpha)

{kind=link}

Portfolio Holdings

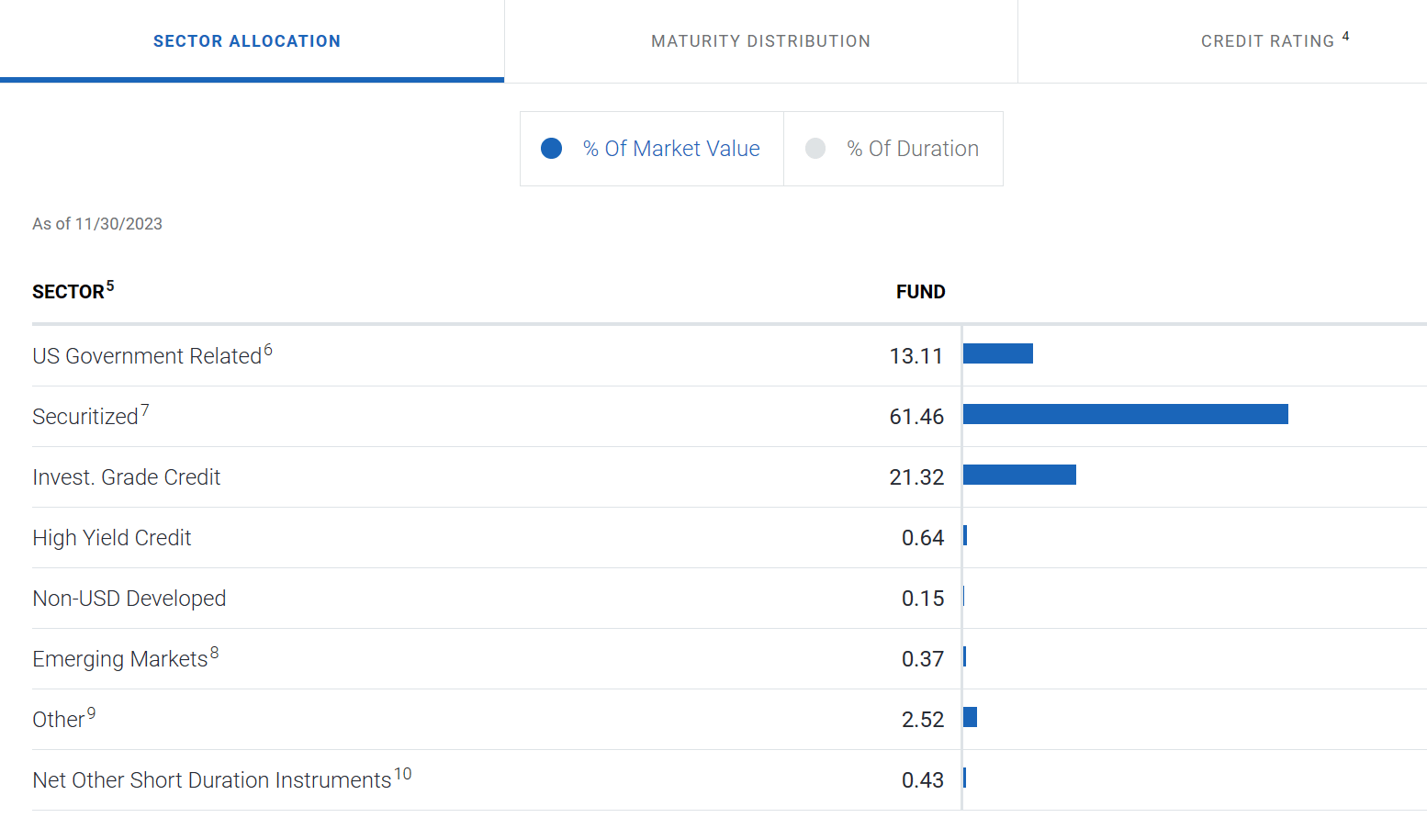

The BOND ETF holds over 1,100 securities with a portfolio effective duration of 5.6 years as of December 26, 2023. Figure 4 shows the BOND ETF's sector allocation. The BOND ETF currently has 13.1% allocated to U.S. treasuries, 21.3% invested in investment grade ("IG") credit, and 61.5% invested in securitized securities like Agency mortgage-backed securities ("MBS"), non-Agency MBS and commercial mortgage-backed securities ("CMBS").

Figure 4 - BOND sector allocation, November 30, 2023 (pimco.com)

{kind=link}

Trading Credit For Convexity Risk

Relative to my prior article in April, we can see some subtle changes to BOND's portfolio, with treasuries decreasing from 17.9% to 13.1%, IG credit decreasing from 25.9% to 21.3%, and securitized securities increasing from 51.7% to 61.5% (Figure 5).

Figure 5 - BOND sector allocation, February 28, 2023 (pimco.com)

BOND's move to overweight securitized securities makes sense, as I have noted in a recent article on the Simplify Mortgage MBS ETF (MTBA).

Historically, the mortgage spread on MBS securities traded in line with the credit spread of IG securities. However, as interest rates have risen in the past few quarters, mortgage spreads have widened as well, as prepayment risks increase (Agency MBS securities are considered backed by the U.S. government and have very little credit risk; however, they do have prepayment risk as mortgage borrowers can choose to refinance their mortgages when mortgage rates decline).

According to Simplify's data, this spread between MBS and credit is currently over 100 bps and is the widest in years, compensating investors for this convexity/prepayment risk (Figure 6).

Figure 6 - Mortgage spread the most attractive in years (Simplify.us)

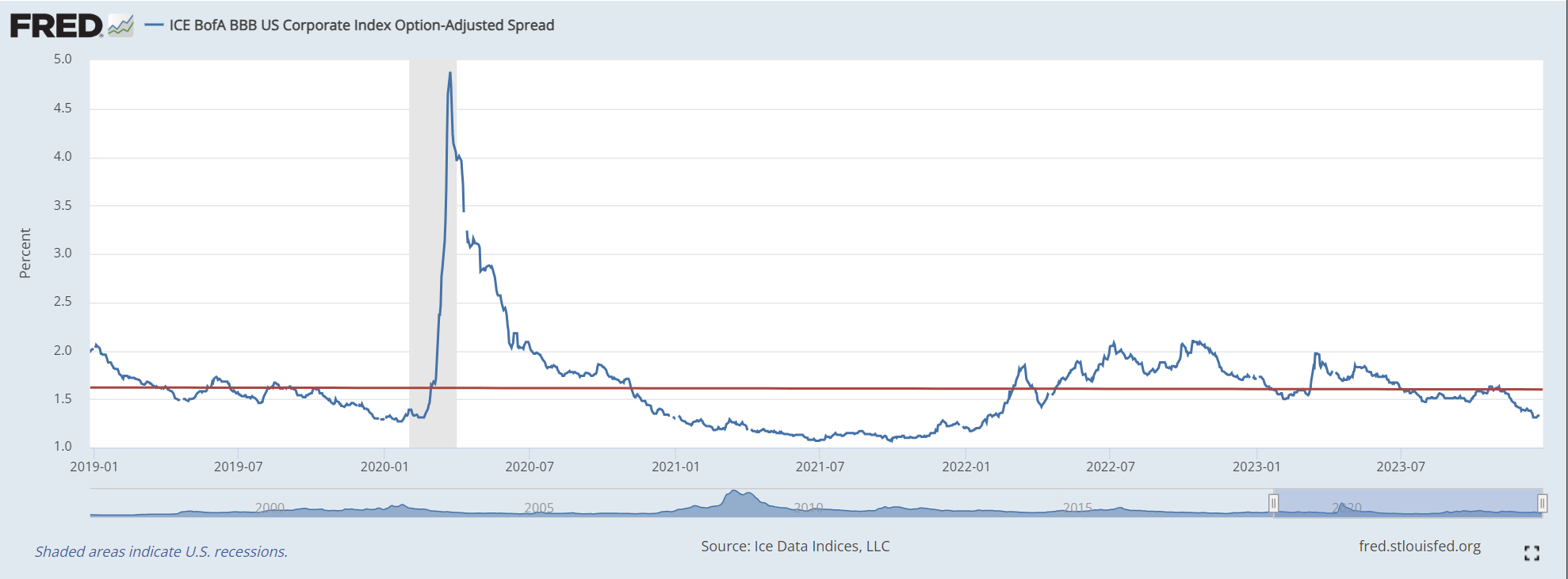

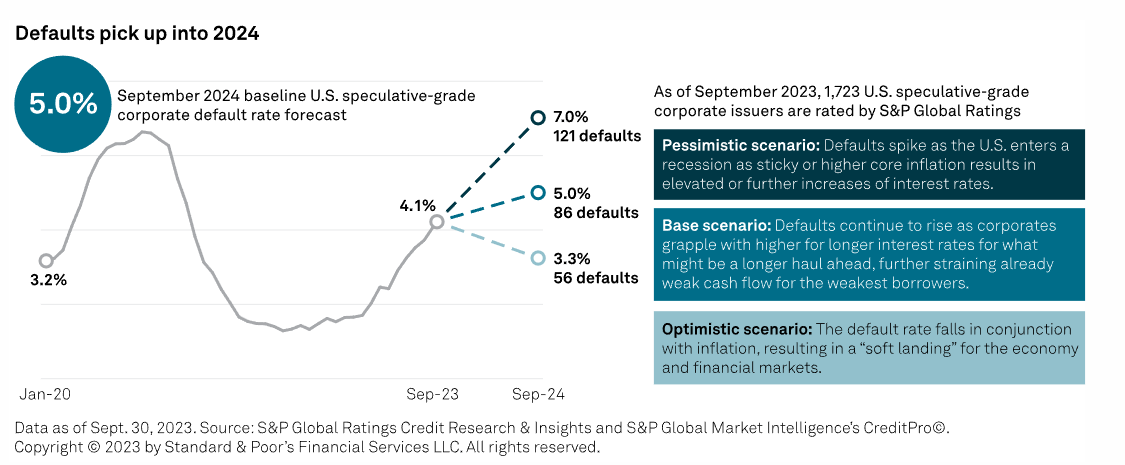

At the same time, despite a heightened risk of economic weakness in the coming quarters, credit spreads are at their tightest in years (Figure 7) and are in stark contrast to analysts' expectations for elevated credit defaults (Figure 8).

Figure 7 - IG credit spreads are the tightest in years (St. Louis Fed) Figure 8 - In contrast for expectations for heightened defaults (S&P Global)

{kind=link}

{kind=link}

Therefore, it also makes sense that the BOND ETF has been reducing its credit exposure from corporate bonds in exchange for attractive priced convexity risk from MBS securities.

End Of Rate Hikes Bullish For Bonds

Following the recent string of FOMC meetings where the Federal Reserve chose to hold interest rates steady, it appears market participants have fully bought into the Fed Chair Powell's assessment that interest rates "are likely at or near the peak rate for this cycle" as the Fed has achieved a 'soft landing'.

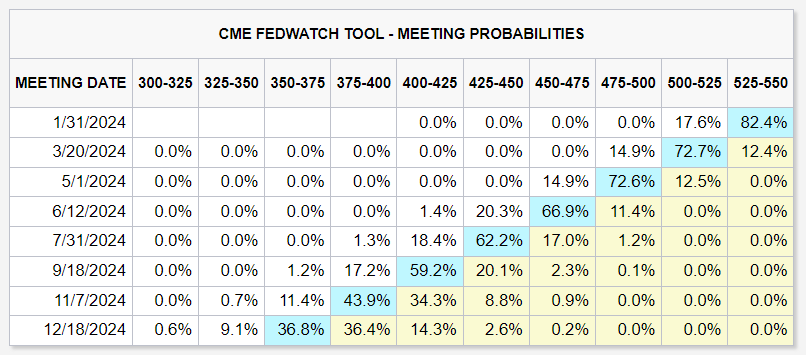

In fact, looking at the Fed Funds futures market, traders expect the Fed to start cutting interest rates as soon as March, with 7 cuts priced in for 2024 versus the Fed's forecast for 3 rate cuts in the latest Summary of Economic Projections (Figure 9).

{kind=link}

While I think traders are far too aggressive to expect 7 rate cuts, it is undeniable that the Fed's stance has shifted away from 'higher for longer' to 'soft landing' and that policy rates are set to decline in 2024. Declining policy rates will act as a tailwind for bonds (just as they were a headwind for most of 2022 and 2023), so I believe the BOND ETF will perform well in the coming year.

Upside Risk From Recession

Furthermore, there remains a significant risk that the Fed's past interest rate hikes are still working their way through the economy and will eventually tip the economy into a 'hard landing'.

This is because many businesses refinanced their debts in the 2020/2021 era at ~2% yields. As those debts come up for renewal in the coming year (corporate bonds are usually issued for 5 years and refinanced within the year of maturity), renewal rates will be in the 5-6% range, dramatically increasing debt service costs for those businesses.

If I am correct with respect to a hard landing, then the Fed may have to cut interest rates rapidly to stimulate the economy (and thus justify the 7 cuts priced into the markets), and the BOND ETF should benefit from capital appreciation as long-term interest rates decline.

Conclusion

As expected, the PIMCO Active Bond ETF has modestly outperformed aggregate bond ETFs like BND and AGG. In recent months, the BOND ETF has reduced its credit exposure while increasing MBS exposure, as credit spreads are currently too tight relative to the state of the economy.

Looking forward, the Fed's shift to a dovish stance should provide a tailwind for the BOND ETF in a 'soft landing' scenario. In the event that the economy worsens materially into a 'hard landing', the Fed has ample room to cut policy rates aggressively and the BOND ETF should benefit from capital appreciation.

I reiterate my buy recommendation.

For further details see:

BOND: Reiterate Buy On Bullish Outlook For Bonds