BNEFF - Bonterra Energy: I Still Expect A Dividend Restart In 2024

2023-12-18 10:30:00 ET

Summary

- Bonterra Energy plans to reinstate dividends once it reaches a certain net debt level, but the recent weakness in oil prices may delay this until at least the second half of 2024.

- In the third quarter, Bonterra reported strong financial results, with a net profit of approximately C$13.5M and an operating cash flow of C$37.7M.

- The company's 2024 guidance shows promising production and capital expenditure plans, but the reinstatement of dividends may take longer due to the drop in oil prices.

Introduction

Bonterra Energy ( BNEFF ) ( BNE:CA ) is a Canadian oil and gas producer with an average output of approximately 14,000 barrels of oil equivalent per day . The company has been working hard on reducing its net debt and once a certain net debt level has been reached, it plans to pay a dividend. Unfortunately, the recent weakness in the oil price means the timing of the dividend reinstatement is now more uncertain, and it will likely get delayed until at least the second half of 2024.

Looking back at the third quarter

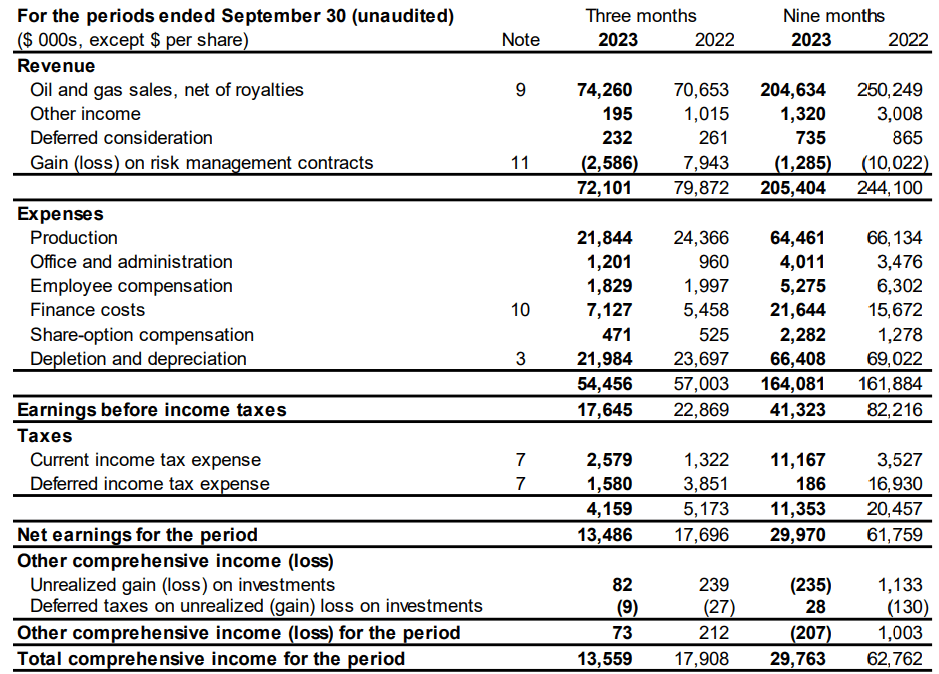

In the third quarter of the year, Bonterra produced an average of 14,300 barrels of oil equivalent per day, with almost exactly half of that consisting of light oil which was sold at an average realized price of just over C$104 per barrel. The company also produced just over 1,400 boe/day of NGLs, with the remainder of the oil equivalent production consisting of natural gas.

The total revenue generated in the third quarter was approximately C$72M, including a C$2.6M loss on hedges. The total amount of operating expenses was C$54.5M, of which almost 40% was represented by the depletion and depreciation expenses.

{kind=link}

This means the pre-tax income was C$17.6M while the net profit in the third quarter of the year was approximately C$13.5M or C$0.36 per share. A good result - thanks to the strong oil price - and the net income in the first nine months of the year came in just below C$30M or C$0.81 per share. A very respectable result based on the average realized light oil price of just under C$98 per barrel while the average realized natural gas price was C$3.27 in the first nine months of the year.

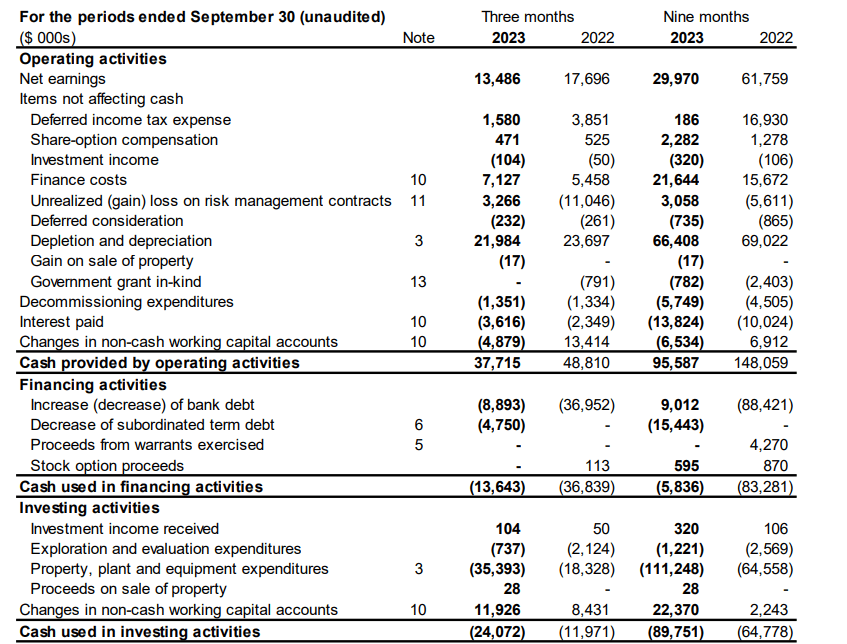

Thanks to the strong oil price, Bonterra's cash flow result was also pretty strong in the third quarter as it reported an operating cash flow of C$37.7M and approximately C$42.5M after adding back the changes in the working capital position.

{kind=link}

The total capex was also pretty high at just over C$36M if you include exploration and evaluation expenses, but keep in mind Bonterra's investment program was front-loaded. The Q4 capex will be substantially lower at just around C$15M, which means the company will likely still be free cash flow positive despite the lower oil and gas prices it will generate in the current quarter.

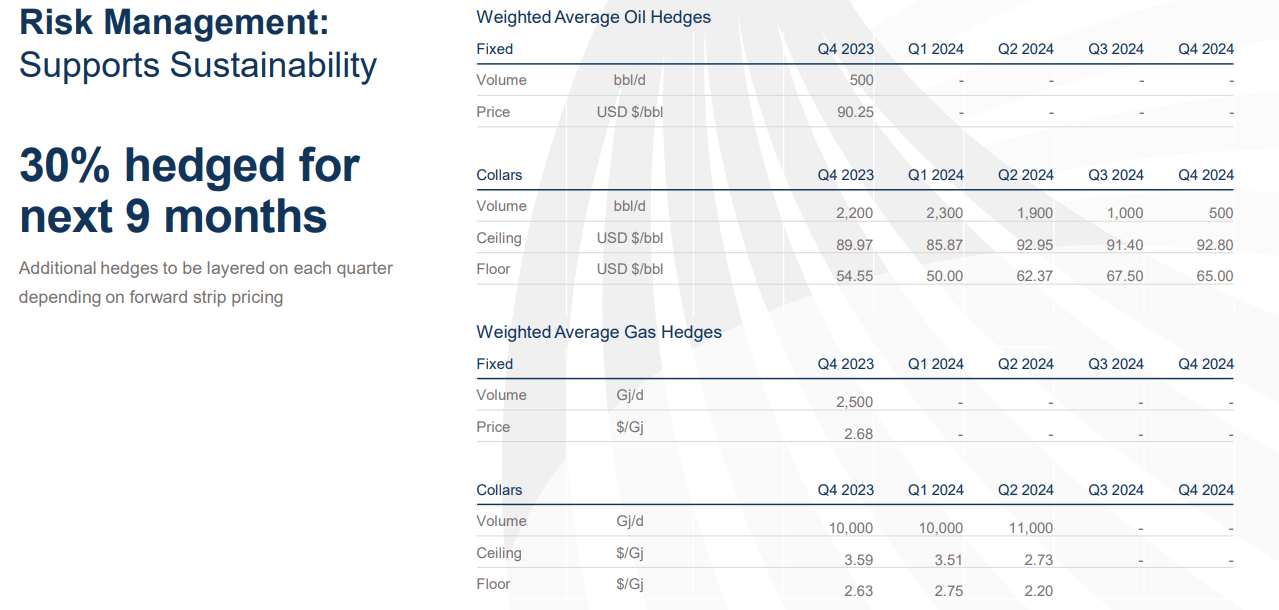

At the end of the third quarter, Bonterra had a net debt position of approximately $156M. The existing hedge book should help the company to protect its downside although the collars on the oil price won't be much help due to the large spread between ceiling and floor.

{kind=link}

The 2024 guidance is promising, but the dividend reinstatement may take longer

Last week, the company announced its official guidance for 2024 , wherein it aims to produce an average of 13,800-14,200 barrels of oil equivalent per day with approximately 60% consisting of oil and liquids. Bonterra Energy also plans to spend C$90-100M on capital expenditures, which should result in a free funds flow of C$20-25M.

I am sure this will be a disappointment to some investors who were hoping on a rapid reinstatement of the dividend. Indeed, just a few months ago I was also expecting the company to start paying dividends again in the first semester of 2024, but the substantial drop in the oil price has decided otherwise. I can't be too disappointed about that as I am satisfied to see the company's management team continue to focus on a healthy balance sheet before starting to make dividend payments again. The company has reconfirmed it wants to reduce its total net debt to C$135-145M before considering reinstating the dividend, and I can only applaud this decision.

Bonterra Investor Relations

Looking at the FY 2024 guidance (above), you see the company used an oil price of $73 and an AECO natural gas price of C$2.50 in its base case scenario. However, the sensitivity table below shows that for every C$0.10 difference in the natural gas price, the funds flow will change by C$1.2M. And for every C$1 change in the oil price, the funds flow will change by C$2.3M. So in a more upbeat scenario using US$75 WTI and C$3 AECO, the operating cash flow and free cash flow would increase by C$13M.

Bonterra Investor Relations

Of course, this sensitivity also works in the other direction. At US$70 WTI and C$2 AECO, the free cash flow would shrink to a single-digit result.

Investment thesis

I already have a long position in Bonterra Energy, but I am slowly adding to this position at the current share price. I am taking advantage of the weak oil and gas prices to increase my exposure to the sector in general, but I remain cautious as I definitely realize the oil price may remain volatile for a while.

The net debt position of Bonterra doesn't scare me as I think the company has the right priorities: reaching its desired net debt level as a first priority before even considering restarting dividend payments.

For further details see:

Bonterra Energy: I Still Expect A Dividend Restart In 2024