BKNG - Booking.Com: 18x P/E For This Growth Champion Riding Travel Tailwinds

2023-10-18 17:31:34 ET

Summary

- Booking.com is experiencing strong double-digit growth on the top and bottom line, fueled by strong travel demand.

- Management notes that trends have accelerated after the close of its most recent quarter.

- The company's business model has been proven to co-exist alongside Airbnb.

- Trading at just an ~18x multiple of FY24 earnings, Booking.com is very reasonably valued for its outsized prospects.

Amid moderating stock-market gains over the past few months as investors have shifted more money out of equities and into cash in response to higher interest rates, I’ve continued to advise that investors keep their eyes peeled for “growth at a reasonable price” stocks that are both high-quality and reasonably valued. In the case the market continues to go south, an existing low valuation protects from substantial downside, while stellar growth metrics can continue to support rallies if the market flies from here.

Booking.com ( BKNG ) is an excellent choice to look at in this regard. The online travel agent leader is up more than 40% year to date but has ratcheted back some of its recent gains, making it an excellent time to consider buying into this name.

I last wrote on Booking in July . Since then, the company has released incredibly strong Q2 results while pointing to the fact that it is seeing an acceleration in booking trends, keeping me quite bullish on the name. Clearly, consumers’ pinched wallets amid this economic slowdown have not impacted the propensity to spend on travel. Heightened travel demand also comes at a time that hotels are raising room rates while still maintaining high occupancy rates: delivering substantial gains to Booking.com's financials.

As a reminder to investors who are newer to this stock, here is my full long-term bull case on Booking.com:

- Red-hot travel demand- After a quiet COVID season, travelers are catching up on lost vacations. Picking up on strong end-customer demand, airlines and hotels have also raised rates, which benefits Booking's commission model.

- Work from anywhere- Airbnb ( ABNB ) has cited this as a benefit to its growth in stays: now that many companies have allowed remote-work from anywhere, many travelers are opting to stay in vacation destinations for extended chunks of time, bringing their work laptops with them. This new "format" for travel has increased wallet share and spending on overall travel.

- Proven to co-exist with Airbnb- Speaking of Airbnb, now that both OTAs and Airbnb have been side by side in the market for years, we can see that there is room for both. Airbnb certainly has its uses and functions (larger homes for group trips, more localized stays in smaller towns); but so does staying in hotels (convenience of a check-in counter when needed, amenities like gyms and spas, proximity to city centers). The notion that Airbnb will kill hotels and OTAs has become antiquated.

- Merchant model growth- Booking has made progress in growing its mix of merchant bookings, which is where Booking directly handles payment from the customer rather than in the agency model, where hotels collect payments and send Booking its commission after the stay. This conversion has helped Booking secure its long-term profitability and cash flow.

- Diversity of brands- With each of Booking's key subsidiaries being individually well known (including OpenTable, which gives Booking exposure to the dining space as well), the company is well-positioned to grow long-term market share.

The best part: all of this strength comes at a very reasonable price. At current share prices near $3,000, Booking.com trades at just an 18x P/E versus Wall Street's consensus FY24 pro forma EPS expectations of $162.53 (data from Yahoo Finance; representing 18% y/y earnings growth on 11% y/y expected revenue growth). For a company with a premium growth rate, it's refreshing to not have to pay a premium multiple over the S&P 500 - and with so many secular tailwinds under its belt, Booking.com remains a top-choice buy.

Q2 download

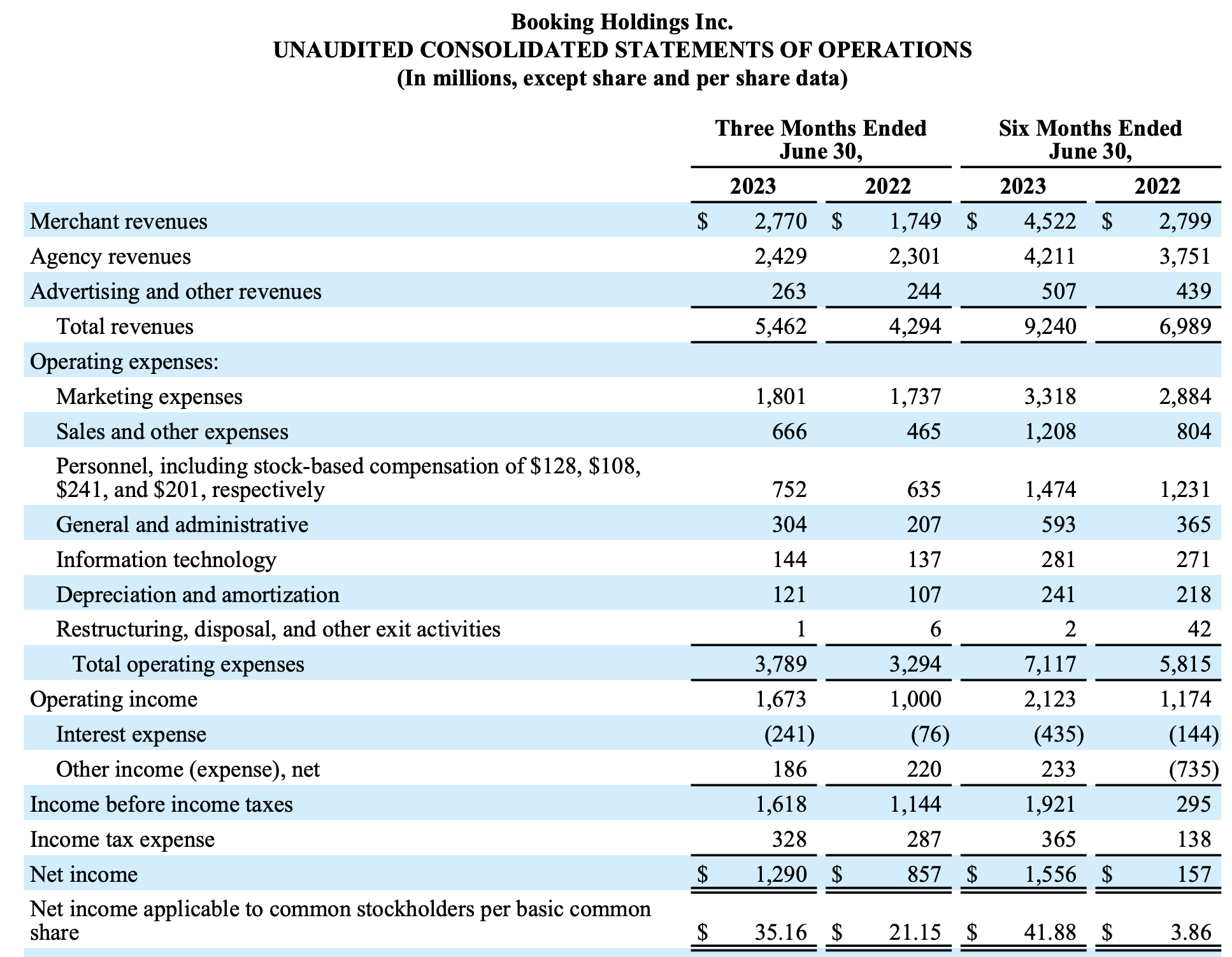

Let's now go through Booking's latest quarterly results in greater detail. The Q2 earnings summary is shown below:

{kind=link}

Booking's revenue grew 27% y/y in the quarter to $5.46 billion, beating Wall Street's expectations of $5.17 billion (+20% y/y) by a huge seven-point margin. Growth was driven primarily by Booking's merchant model, which is now roughly half of the business - and as a reminder, also helps stabilize and front-run the company's cash flow by speeding collections from customers' hotel bookings.

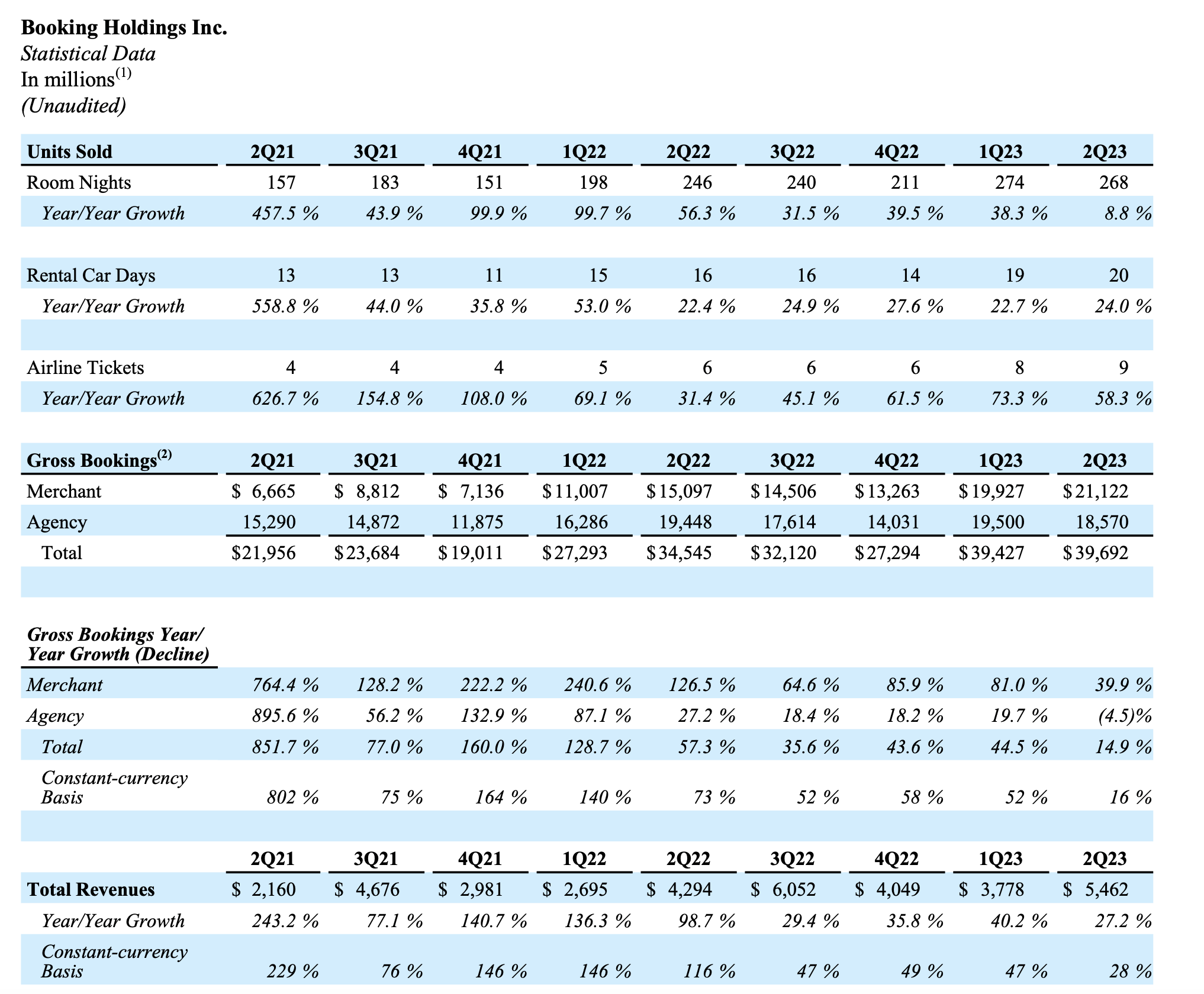

On a booking basis, the company sold 268 million room nights in the quarter, up 9% y/y. Gross bookings of $39.7 billion grew 16% y/y on a constant-currency basis, as shown in the chart below:

{kind=link}

Of course, we do note that top-line trends have seen marked deceleration (relative to 50%+ constant-currency bookings growth over the past several quarters). This is largely, however, a function of tougher comps as we start to lap the resurgence of travel demand in the back half of 2022.

Management noted that after the close of Q2, the company has seen trends continue to re-accelerate. Per CEO Glenn Fogel's remarks on the Q2 earnings call:

Looking at the month of July we have seen an acceleration in year-over-year room night growth relative to the 9% growth we reported for Q2. We estimate July room nights increased by about 20% year-over-year benefiting from the easier comparison to July 2022.

Overall, we have been very pleased to see our strong performance in the first half of the year which has benefited from the continued strength and resiliency of overall travel demand. Our solid start to the year combined with what we currently believe will be a new all-time high for Q3 summer travel period results and an improved outlook for the full year"

Also of note is the fact that Booking.com is starting to build AI into its suite of products. As part of Priceline's Summer Release of new features, the company rolled out a new generative AI trip assistant, which helps customers with a visual list of potential destinations and helps them to choose recommended accommodations and complete their reservations.

Booking achieved strong top-line results despite very limited growth in marketing spend, up only 4% y/y. As a percentage of gross bookings, marketing expense declined by 60bps.

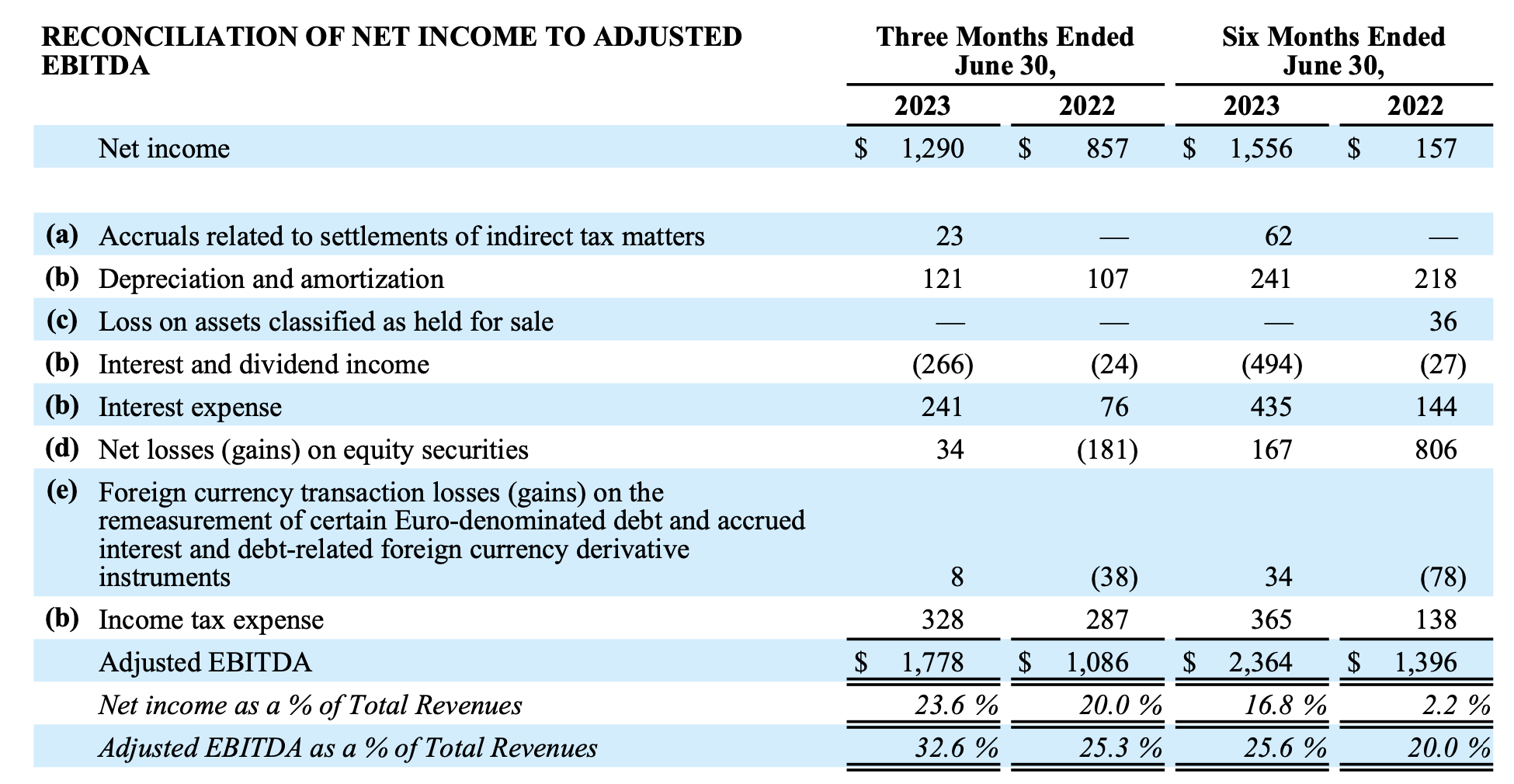

This discipline in spend helped Booking generate $1.78 billion of adjusted EBITDA in the quarter (+64% y/y), representing a massive 32.6% margin: 790bps richer than the year-ago Q2.

{kind=link}

Key takeaways

There's a lot to like about Booking.com: strong booking trends, continued optimism in the travel sector, a rich margin profile and aggressive bottom-line expansion. Stay long here and use dips as a buying opportunity, especially at Booking's current modest P/E ratio.

For further details see:

Booking.Com: 18x P/E For This Growth Champion Riding Travel Tailwinds