BKNG - Booking Holdings: Great But Overvalued

2023-08-16 02:17:31 ET

Summary

- Booking Holdings has capitalized on COVID to come out ahead of Expedia.

- Whether Expedia's 'technology stack consolidation' initiative constitutes a success remains to be seen.

- In contrast, Booking has a clear narrative for investors - strong growth/share gain momentum (backed by specifically identified business levers) and an investor-friendly capital allocation policy.

- While a quality company, Booking is currently trading at overvaluation.

- My rough calculation suggests that intrinsic value per share, assuming the OTA industry is no longer high growth but steady growth, is ~$2,300.

Expedia has lost market share to Booking Holdings

Booking Holdings' (BKNG) gross bookings have always been a tiny fraction less than Expedia's before the pandemic. As Covid hit, bookings for both companies plummeted, but now as the world emerges from that phase, it appears that Booking Holdings is coming out on top of its rival. Describe it however you want - maybe they're simply 'recovering more quickly' than Expedia, but either way they have gained share.

Expedia and Booking Holdings SEC Filings

What's interesting is that Booking Holdings' share gain is under the 'merchant model'. Booking Holdings itself has predominantly been an 'agency model' platform in the past, and is only in recent years that we observe an increasing contribution from the 'merchant model'. Booking Holdings CFO David Goulden explains to investors that the 'merchant model' gives OTAs better control over service delivery and consumer satisfaction (during the Q3 2018 earnings call). (The downside is working capital risk, which rare circumstances such as Covid has made clear to the market, but under normal economic conditions the working capital dynamics under the 'merchant model' are in fact favorable as OTAs receive cash first and pay back airline/hotel suppliers later). Otherwise, both models involve earning a margin / take rate for acting as an agent or merchant (i.e. middleman) in a transaction.

Booking Holdings SEC Filings

Expedia appeared to be too preoccupied with its internal transitions, giving Booking Holdings the opportunity to forge ahead

Besides battling the pandemic, Expedia appears to have spent the last 2-3 years on internal transitions, which the company prefers to describe as strategic initiatives to " simplify the company " and "focus on technology" (Q3 2021 transcript). The latter involves "re-architecting everything" and "moving from this many technical stacks to one stack on one pool of data that serves all the outcomes, all our partners, all our customers" (Q3 2021 transcript). While not the typical old-school restructuring, it appears to at least in principle be a sort of restructuring at the technology level.

When a company focuses on internal changes, it is natural for its outward expansion/momentum to stall. And this gave Booking Holdings an opportunity to take advantage.

Expedia CEO Peter Kern describes this process on the Q4 2022 earnings call :

moving the businesses on to a single technology stack and front end stack, I think hotels.com is an instructive example... As we're moving hcom across, we obviously did less to improve Hcom as a standalone entity, because all the engineers were working on moving it. So, you lose a little momentum as you're moving something. And then there is typically an uplift period where you've got to optimize the new stack and the new product on the new stack to get back to where you were, and then get all the benefits beyond that. So there is typically, if you will, a lull that takes place as you move things and some friction that you have to absorb in the numbers…

It is probably worth articulating the value proposition of this 'technology stack consolidation' beyond the technical description of the process, given the huge expense at which it is coming.

That proposition is: a unified technology stack means better AI capabilities which can support personalization, or better targeting, of customers (and vice versa, i.e. better matching of hotels, flights, other travel services according to customer preferences). This will then translate into higher volumes (bookings) and therefore revenues.

This is a perfectly legitimate proposition but also one that is difficult to validate, especially for investors. To put it this way, Expedia (despite the setbacks) has considerable industry expertise in what it does - as an OTA; but that's different from asking whether Expedia can develop Google-like AI/search capabilities.

In contrast, Booking Holdings has a clear narrative for investors

- Its core products / portfolio of platforms are registering market share gains

- It has an investor-friendly capital allocation policy that it has consistently followed and will continue to follow:

- The company believes that return of excess capital i.e. capital over and above what we need to do to support the business through organic and inorganic acquisitions is a good part of their overall value creation strategy for shareholders. This is reflected in consistent share repurchases in historical periods.

- Sidetracking a bit, this also explains the seemingly high debt to equity ratio relative to Expedia, when in fact this metric is not meaningfully comparable. Instead of retaining earnings, Booking Holdings redistributes cash back to shareholders via buybacks, resulting in an artificially suppressed equity base.

Capital IQ Capital IQ Capital IQ

{kind=link}

3. It communicates clear product and/or technological levers as business drivers, instead of broadbrush platform upgrades.

- Take for example how it emphasizes its payment piece. Both Expedia and Booking Holdings have payment processing / checkout capabilities, but Booking Holdings communicates much more clearly the role of payments in its platform ecosystem, identifying / discussing it as a specific lever that facilitates volumes, and the company's target to increase that adoption.

- While Expedia doesn't go into much detail in its annual filings beyond 'payment processing' and 'acceptance of a variety of payment methods', Booking Holdings describe this as offering alternative payment solutions to consumers even when those payment solutions may not be accepted by the travel service provider or restaurant. For example, in many markets (particularly in Asia) where credit cards are not readily available and/or e-commerce is largely carried out through mobile devices, alternative payment methods like Alipay, Paytm, and WeChat Pay that operate closed loop payments systems are the exclusive or preferred means of payment for many consumers. By enabling acceptance of these alternative payment methods, Booking Holdings' payment product helps expand the userbase by increasing conversion / on-boarding those users who may not necessarily be using credit cards and instead online payment services

- Booking Holdings' percentage of gross bookings are now running on the company's own payments platforms is ~40% , up from ~ 33% as of Dec 2021, and 15% in 2019 .

Valuation

Booking Holdings is a great company but overvalued at this point.

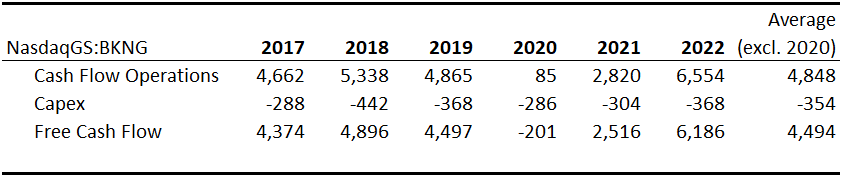

- Free cash flow to firm over the last 5 years, excluding 2020, is ~$4.5 billion per year.

Capital IQ, author's own calculation for free cash flow

{kind=link}

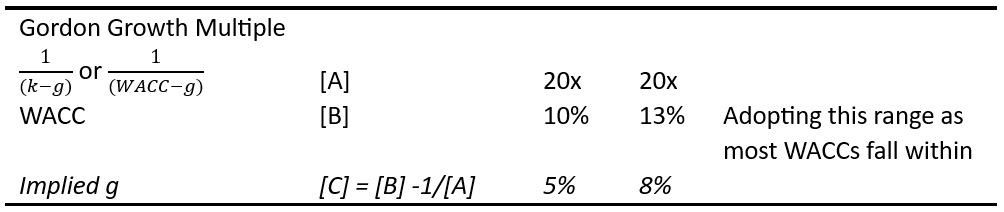

2. To capitalize this free cash flow per year, let's say we use a multiple of 20 since historically the stock's forward P/E multiple has been at that level on a relatively steady basis. Obviously, P/E and EV/unlevered FCF multiples are not the same thing, but let's say we assume that the inputs to our EV/unlevered FCF multiple is such that it produces the same multiple as P/E, that is, roughly 20x. This implies long-term growth rates of 5% to 8% - I consider these rates reasonable but would be skeptical of anything higher as the OTA industry is no longer in a high growth but a steady growth stage.

Author's assumptions and analysis

{kind=link}

3. That leaves us with:

- enterprise value of $4.5bn x 20 = $90bn.

- equity value of $90bn plus $12bn in cash less $15bn in debt (total non-current liabilities of $14.1bn plus short term debt of $0.5b)=$87bn

- $87bn / 37.65million shares = $2,310 per share, and a far cry from the ~$3,200 per share at which the stock is trading.

For further details see:

Booking Holdings: Great But Overvalued