BKNG - Booking Holdings: Strong Competitive Position That Deserves A Premium In Valuation

2023-10-19 19:36:49 ET

Summary

- I recommend a buy rating due to BKNG's competitive position, growth potential, and strong balance sheet.

- Pre-COVID, BKNG demonstrated impressive growth, and it has since recovered and surpassed its pre-pandemic revenue levels.

- BKNG's dominant position in Europe, particularly with boutique hotels, gives it a competitive advantage and ensures high take rates.

Summary

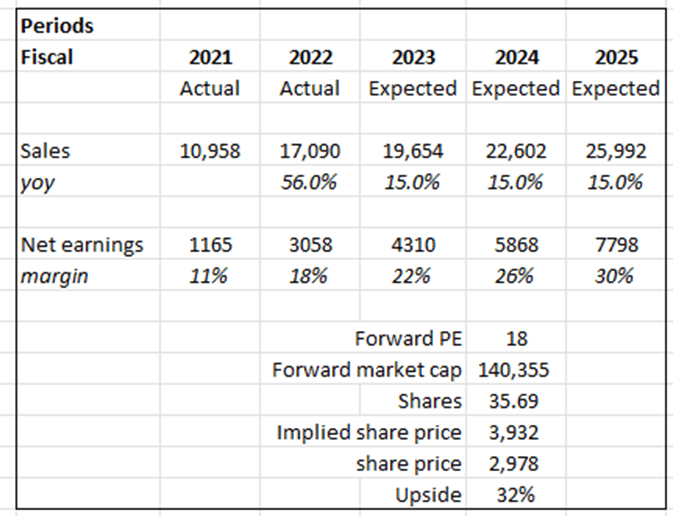

I am recommending a buy rating for Booking Holdings ( BKNG ) as I am in favor of its competitive position in the industry, growth and balance sheet profile, and long-term growth potential of its industry. With my expectations that BKNG will grow in line with the industry, I believe BKNG has a potential upside of 32%.

Business

BKNG is an online travel agency [OTA] that allows travelers to book hotels, plane tickets, car rentals, etc. There are six key brands that BKNG owns and operates: Booking.com, Priceline, Agoda, Rentacars.com, Kayak, and OpenTable. BKNG mainly derives its revenue from international sources (87% as of FY22) and 13% from the US. The key competitor that BKNG competes with is Expedia ( EXPE ).

Financials/Valuation

Pre-COVID, BKNG has demonstrated astonishing growth from $4.3 billion in FY11 to $15 billion in FY19, more than 3x growth. However, due to the nature of BKNG's business (targeting travelers), COVID was a major crisis for the business, wherein growth collapsed by 55%. However, the strength of BKNG's business and brand was well demonstrated as it was able to regain those lost revenues and has generated revenue levels way above pre-COVID level (FY19). As of LTM, the business generated $19.3 billion in revenues and $6.1 billion in EBITDA (~$100 million above FY19). BKNG also has a strong balance sheet. As of LTM, BKNG has around $1 billion in net cash, better than its peer, EXPE, which has a net debt position of $250 million.

{kind=link}

Based on my view of the business, BKNG should be able to grow in line with industry growth (15%) at the minimum. While I believe BKNG should grow faster as it is the leading player , I think it is safer to assume an industry growth rate for modeling purposes. Earnings, on the other hand, should grow faster than the top line as BKNG grows back to its historical peak net margin performance, driven by increased booking volume. For reference, in FY19, BKNG generated a net margin of 33%. I am modeling 30% to be conservative. BKNG's key competitor is EXPE, who is trading at 9x forward PE today while BKNG is at 18x. Unlike BKNG, EXPE has a much lower growth (using consensus figures, BKNG is expected to grow by 24% and 11% in FY23/24 while EXPE is expected to grow at 9.9% and 8.5%) and margin profile (BKNG has EBITDA margin of 33% while EXPE has EBITDA margin of 19%) and is in a net debt position. EXPE's competitive position in the industry (US has more chain hotels that have higher negotiating power) is also weaker than BKNG, hence deserving a discount. I expect BKNG to continue trading at 18x, which is the historical average (excluding COVID).

Comments

I expect BKNG to continue solidifying its market position as the business gets larger and larger. Being an OTA, having scale on both sides of the equation (demand and supply) is the key to winning. BKNG's dominance in Europe stems from its ability to solve the "chicken and egg" problem, whereby it has both demand from travelers and supply of hotels. Both parties use BKNG, as BKNG is the best product available. Especially in Europe, it is full of small boutique hotels that rely on BKNG as an important source of revenue. BKNG should be able to continue charging high take rates in the EU as long as the hotel supply landscape doesn't change.

Small independent boutique hotels in BKNG do not have the necessary bargaining power to negotiate for lower take rates, as BKNG is the one with leverage in this equation. Moreover, independent hotels do not have the marketing prowess to outbid BKNG and provide value loyalty programs (lack of traffic to make it economically viable anyway); as such, they rely on BKNG to market themselves. Operating an independent hotel has a significant fixed cost, and hence, the occupancy rate is extremely important, which means having traffic is key. This further weakens independent hotels' negotiating power against BKNG, as they need the traffic that BKNG can provide. The counterargument here is that a large chain hotel will have enough negotiating power as it has the ability to launch its own loyalty program (e.g., Hilton, Accor, etc.). My argument is that it is difficult to consolidate the EU hotel industry, as unlike US hotels with many rooms (hundreds per hotel), hotels in the EU typically have 10-50 rooms and are independent. This significantly lowers the risk of hotels consolidating to compete against BKNG. Because of this, it is tough for new entrants to compete against BKNG in the EU, as there is a high barrier to scale. Hotels are less likely to sign up with new entrants as the new platform does not have sufficient demand, and hotels risk pissing off BKNG.

As such, relative to EXPE, I believe BKNG has a much better competitive position in the valuation chain. BKNG brings more value in EU than US as it solves the issue of "discovery", with a myriad of independent hotels, consumers need a solution to "discover" and "find" these products, especially since travelers want to enjoy different types of experience .

Management has also been smart in ensuring it covers all possible verticals in hotel travel such that it has sufficient presence to counter or block any possible threat. The way I see it, BKNG's venture into alternative accommodations is a smart move that serves as a toehold position (increasingly becoming a value prop) that serves as both a defensive and offensive move. This ensures BKNG is able to compete with Airbnb.

Just to touch on 1 final point, I believe the risk of Google disintermediating BKNG might be overblown as 1) Google faces antitrust issues. 2) Google is earning high-margin ad revenue from BKNG (BKNG spends a lot on Google Ads to dominate the top of the funnel). In the event Google does raise ad inventory prices against BKNG, this would not be an isolated event; it would impact the entire industry, and BKNG would still be the "best man standing", Smaller players will suffer more. If Google wants to replicate BKNG, it has to hire >20,000 staff who manage the hotel partnerships and provide 24/7 customer service. These are tedious moves. All these have to happen with the antitrust overhang to make it less likely for Google to enter OTA. Over time, BKNG has managed to direct more and more traffic to its sites organically (~50% now). As BKNG continues to ramp up loyalty programs and marketing, it will rely less on Google, hence improving margins and business quality.

Risk & Conclusion

BKNG is in the travel industry, which is considered discretionary spending, and in the event of an economic downturn or recession, it would top the list of expenses to be cut. Any pandemic that would hurt the travel industry would directly impact BKNG; we can clearly see how it was impacted during COVID.

In conclusion, I recommend a buy rating for BKNG based on its strong competitive position, growth prospects, and solid balance sheet. BKNG's resilience and ability to recover rapidly from the COVID-19 crisis highlight its business strength and brand value. As it outperformed its pre-pandemic revenue levels and generated $19.3 billion in revenues, BKNG remains on a growth trajectory.

BKNG is poised to grow in line with industry, with earnings expected to outpace revenue growth due to increased booking volumes and a historical net margin of 33%. Despite its current premium valuation compared to competitors like EXPE, BKNG's dominant position in Europe, particularly with boutique hotels, ensures high take rates. The challenges of independent hotels in Europe to negotiate lower take rates and the difficulty of consolidation in the European hotel industry further bolster BKNG's competitive advantage.

For further details see:

Booking Holdings: Strong Competitive Position That Deserves A Premium In Valuation