BKNG - Booking Holdings: Take Some Profits On This Rally (Ratings Downgrade)

2023-11-22 02:06:35 ET

Summary

- Booking Holdings stock has surged over 50% YTD, prompting my recommendation to take profits and wait for a cheaper entry point.

- BKNG stock is trading at a slightly richer multiple than the S&P 500 and has a slightly above 1.0x PEG ratio.

- The Company has positive long-term drivers, including diversifying beyond hotels, non-leisure stays, proven co-existence with Airbnb, and merchant model growth.

- In the short term, however, BKNG is expecting bookings growth to decelerate in Q4, driven in part by the war in the Middle East.

- Downgrading Booking Holdings to Neutral.

Stocks are soaring to YTD highs, which should be a trigger for investors to re-examine their portfolios and determine which stocks still belong in them. Booking Holdings ( BKNG ), the leading online travel agency, is one stock that merits a hard re-evaluation. Now up more than 50% year to date, the market's broad rally and pivot back into growth stocks has helped Booking recoup almost all of the value it shed in the aftermath of a mixed Q3 earnings print.

I last wrote a bullish note on Booking when the stock was trading closer to ~$2,800 per share, and I've been bullish on the company for quite some time. With the stock reaching new all-time highs, however, I'm recommending that investors take profits on this upswing and am downgrading the stock to neutral.

At current share prices, I view Booking as more of a balanced bag of positive and negative drivers. While I won't call out valuation as a red flag, it's more of a "yellow flag" to me - at just shy of $3,200 per share, Booking trades at a ~20x P/E ratio vs. consensus' pro forma EPS expectations of $160.67 next year, which represents 19% y/y earnings growth. The fact that Booking is now trading at a slightly richer multiple than the S&P 500 and the stock's PEG ratio is now slightly above 1.0x is making me move to the sidelines.

The other short-term driver to be worried about: Booking is expecting a deceleration in both gross bookings and room nights in Q3, in part driven by the war in Israel - more on this in the next section. Regardless, a slowdown in Booking's thus-far excellent financials could be a downside trigger for the stock when Q4 results are due. We should note as well that Booking has an incredibly tough comp for travel demand in FY24, while consensus is still expecting double-digit growth going forward.

That being said, there are still several positive long-term drivers for Booking.com:

- Diversifying beyond hotels. Booking.com's growth in airfare bookings is exceeding room nights. In addition, the company recently rolled out a cruise feature, drawing on red-hot demand for cruise travel.

- Non-leisure stays and "work from anywhere." Airbnb ( ABNB ) has cited this as a benefit to its growth in stays: now that many companies have allowed remote work from anywhere, many travelers are opting to stay in vacation destinations for extended chunks of time, bringing their work laptops with them. This new "format" for travel has increased wallet share and spending on overall travel.

- Proven to co-exist with Airbnb. Speaking of Airbnb, now that both OTAs and Airbnb have been side by side in the market for years, we can see that there is room for both. Airbnb certainly has its uses and functions (larger homes for group trips, more localized stays in smaller towns); but so does staying in hotels (convenience of a check-in counter when needed, amenities like gyms and spas, proximity to city centers). The notion that Airbnb will kill hotels and OTAs has become antiquated.

- Merchant model growth. Booking has made progress in growing its mix of merchant bookings, which is where Booking directly handles payment from the customer rather than in the agency model, where hotels collect payments and send Booking its commission after the stay. This conversion has helped Booking secure its long-term profitability and cash flow.

The bottom line here: while I still like the Booking.com story in the long term, I think there will be a near-term opportunity to buy the stock under $3,000 again. Opportunistic investors can lock in some gains on their positions now and wait for the stock to dip a little bit before buying back in.

Q3 download

Let's now discuss Booking's latest quarterly results, and commentary surrounding expectations for Q4 performance, in greater detail. The Q3 earnings summary is shown below:

{kind=link}

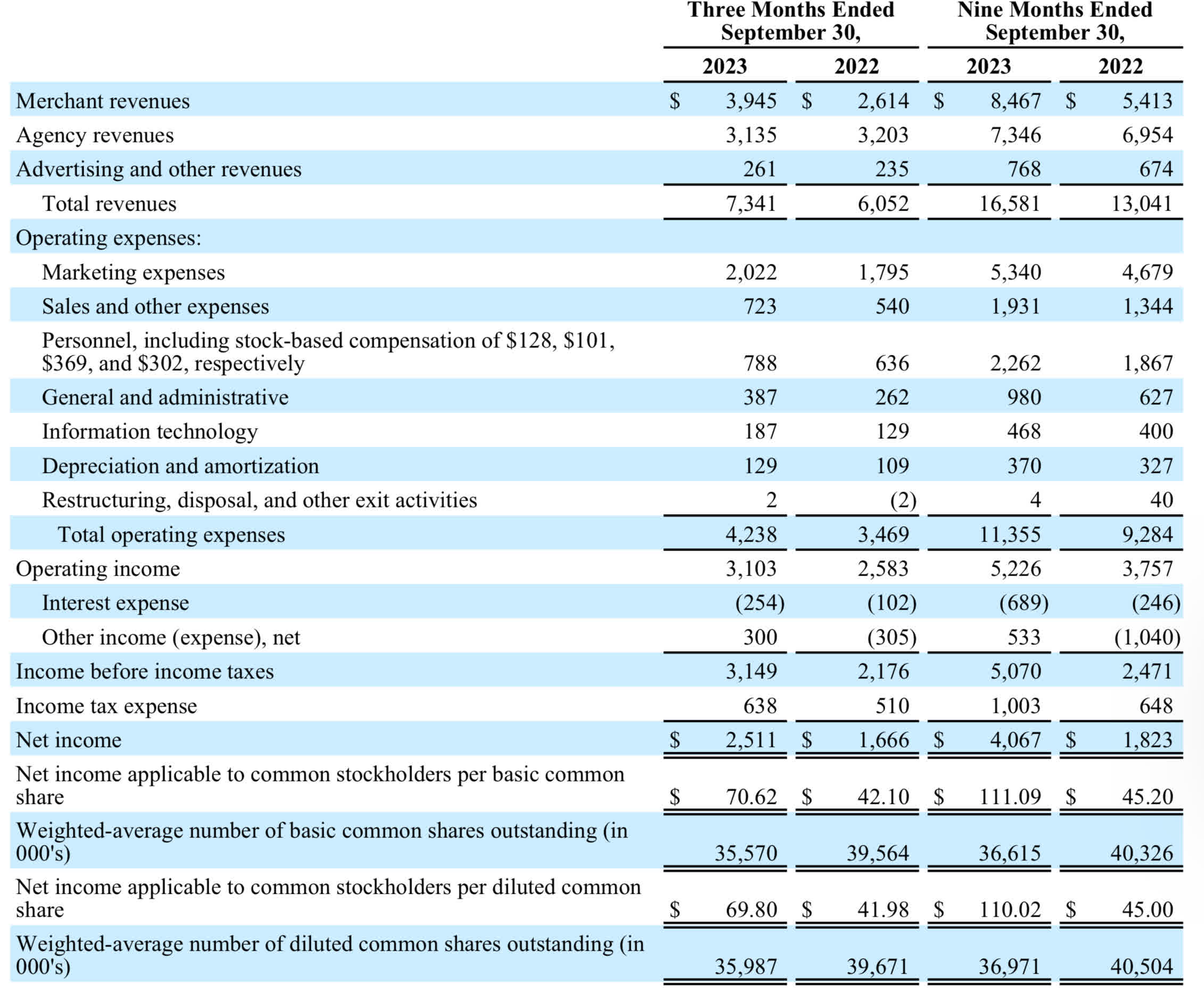

Booking's revenue grew 21% y/y to $7.34 billion, ahead of Wall Street's expectations of $7.26 billion (+20% y/y) by a slight one-point margin. Note as well that FX is now a tailwind for Booking, as the company reported that constant-currency growth would have been weaker at 18% y/y.

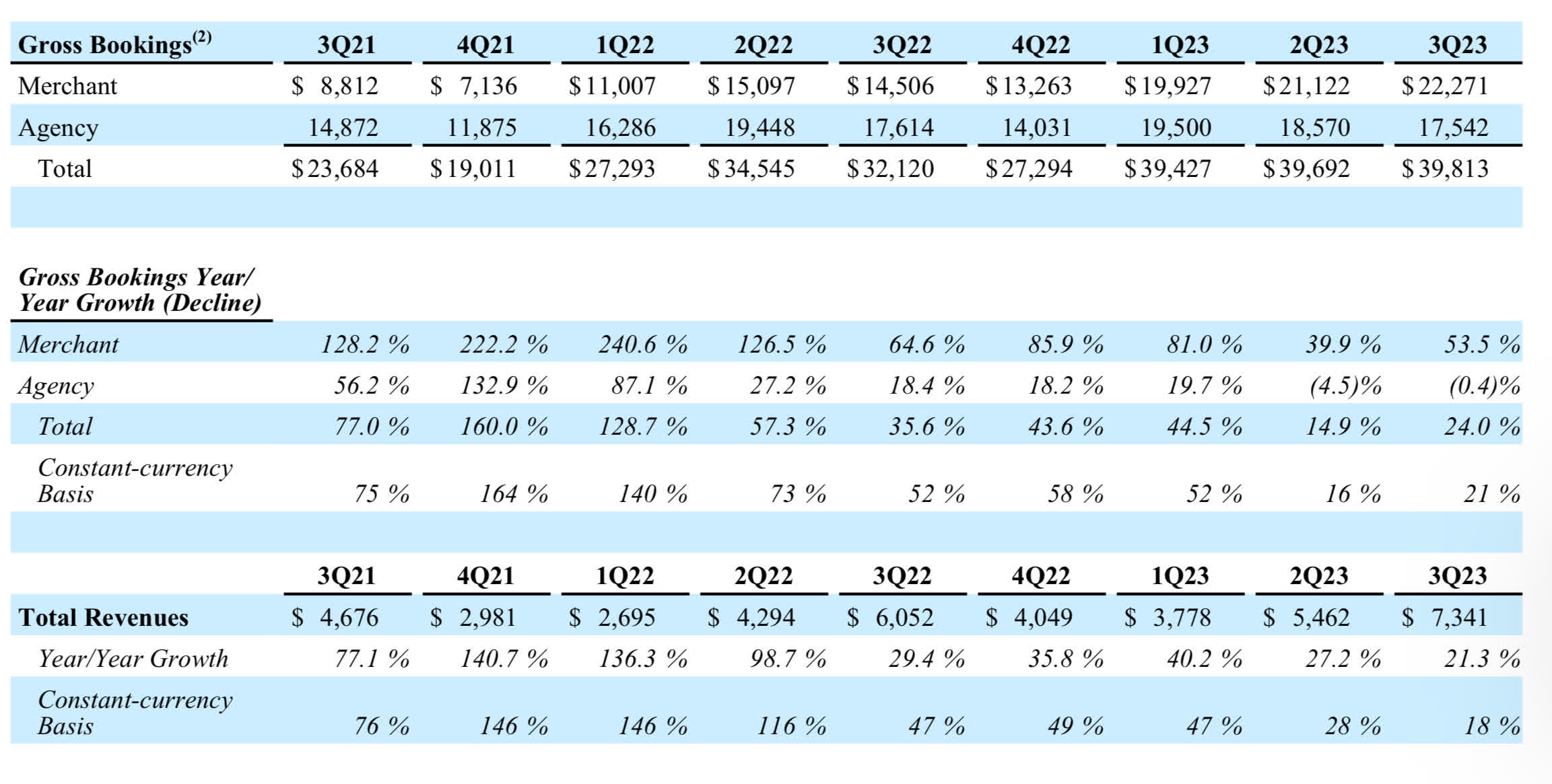

Booking.com gross bookings trends (Booking.com Q3 earnings release)

{kind=link}

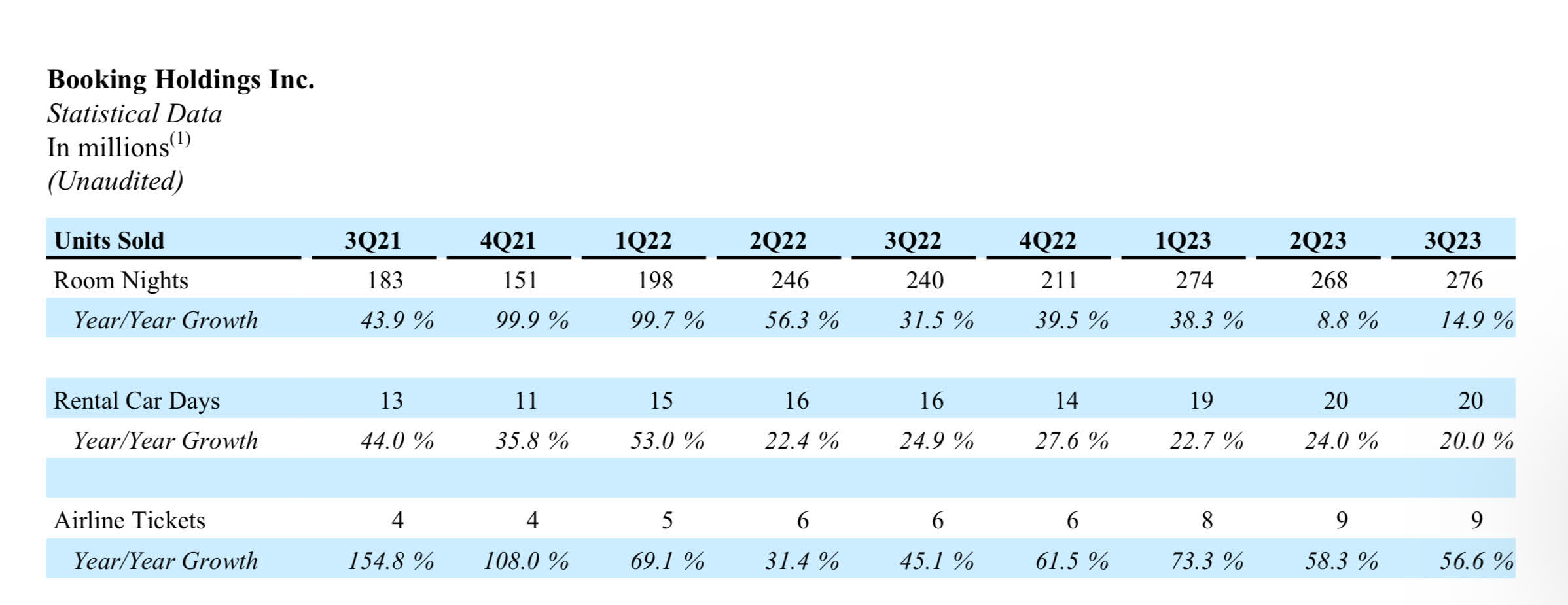

From a bookings standpoint, as shown in the chart above, booking of $39.8 billion accelerated at 41% y/y growth versus 15% y/y growth in Q2 (though this is a far cry weaker than the ~40% growth over the preceding three quarters). This was driven in large part by 15% y/y growth in room nights sold to 276 million, up from 9% y/y in Q2; while airline tickets sold of 9 million still exhibited the strongest growth category at 57% y/y.

{kind=link}

The fact that revenue growth at 21% y/y (and decelerated versus Q2), while bookings growth outpaced revenue growth at 24% y/y (accelerating versus Q2), is due to the fact that more travelers are booking early for travel in later quarters. The company expects this dynamic to unwind in Q4, where revenue growth is expected to outpace bookings growth.

It's worth scrutinizing the expectation in bookings dynamics, however. CFO David Goulden noted on the Q3 earnings call that the company is expecting a relatively sharp deceleration in room nights in Q4, extrapolating off the latest trends the company observed in October.

Now onto our thoughts for the fourth quarter of 2023. In October, we estimate year-over-year room night growth was about 8%, down from 15% in Q3 due in part to a tougher year-on-year compare, as well as the war in the Middle East. When comparing versus 2019, October room night growth was about 20%.

Excluding Israel, October room nights grew about 9% versus 2022 and about 22% versus 2019. The 22% growth versus October 2019 excluding Israel is a little lower than the 24% growth we saw in Q3 versus 2019.

Looking across our major regions, in October we saw Asia year-on-year growth of room nights without 15%, Europe up about 10%, and the U.S. and Rest of World were down slightly. The impact of the Israel-Hamas war is seen most in the Rest of World growth numbers.

Israel on a booker plus inbound travel basis is about 1% of our global room nights. The Middle East, including Turkey and Egypt, on a booker basis is about 4% of our global room nights.

Globally, we saw a slowdown starting the second week of October due to cancellations and a drop in new bookings after the start of the war in the Middle East. The cancellations we saw that started in the second week of October were concentrated in Israel, but we also saw some impact on travel trends outside of the country as people absorbed the news. We were pleased to see room night growth recover towards the end of the month."

Overall gross bookings are expected to drop to 5% growth, which is a sharp deceleration from the current quarter. While the company is blaming war in the Middle East as well as tough comps, as well as the earlier bookings exhibited in Q3, this may be a sign as well that the economy is catching up to travel demand and that we're slated to see a weaker FY24.

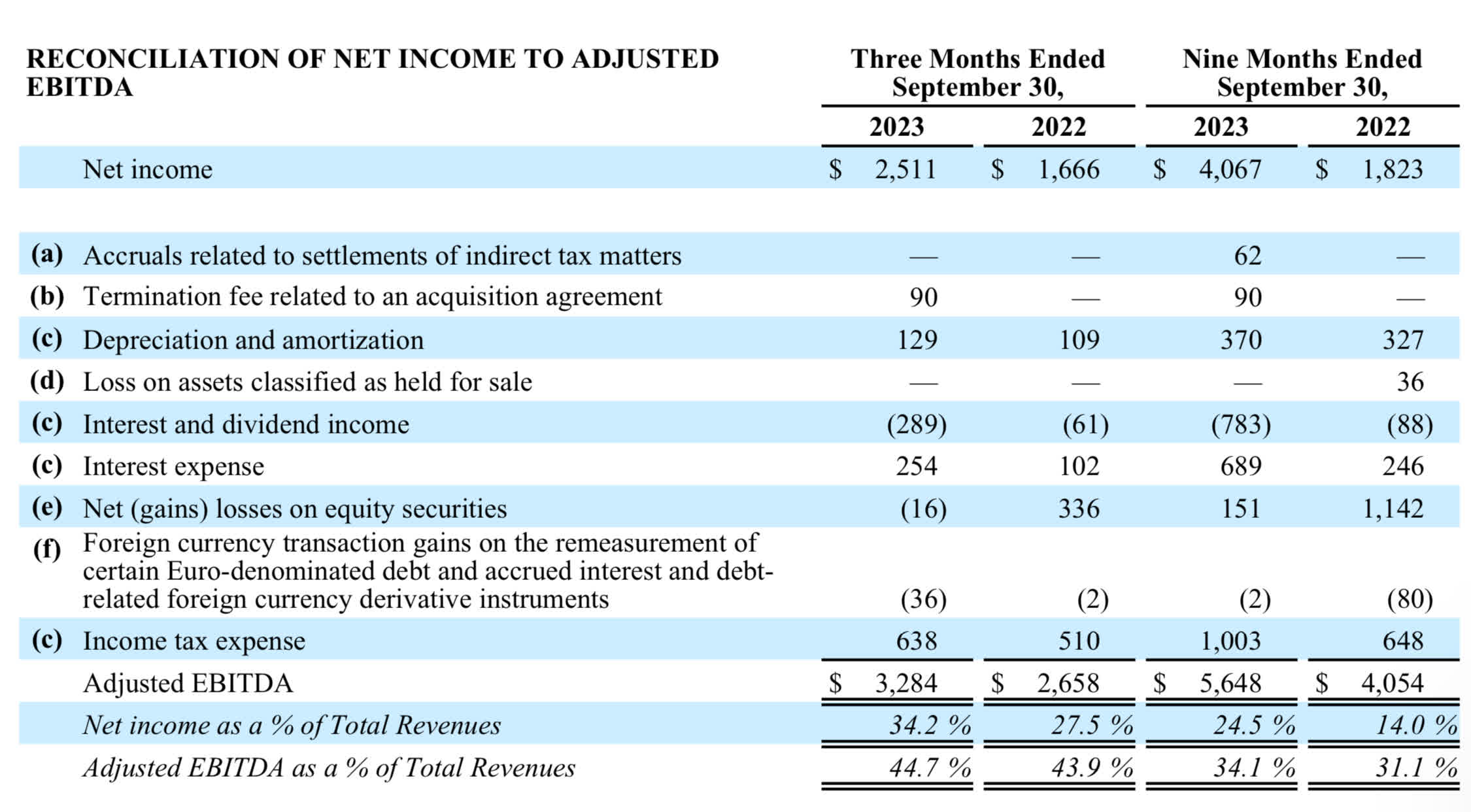

From a profitability perspective, Booking continued to deliver tremendous earnings growth. Adjusted EBITDA of $3.28 billion grew 23% y/y, while adjusted EBITDA margins of 44.7% gained 80bps of leverage versus the third quarter of FY22:

Booking.com adjusted EBITDA (Booking.com Q3 earnings release)

{kind=link}

Pro forma EPS of $72.32 also grew 36% y/y and beat Wall Street's expectations of $67.92 with 6% upside.

Key takeaways

With the recent surge in Booking Holdings stock, it's a great time to take some profits off the table and move to the sidelines until a cheaper entry point. In my view, at a ~20x FY24 P/E, Booking has exhausted most of its upside potential, especially with the deceleration expected in Q4 gross bookings. I remain positive in the long term here, but I can be opportunistic in the short term.

For further details see:

Booking Holdings: Take Some Profits On This Rally (Ratings Downgrade)