ABNB - Booking Holdings: Well-Positioned For Profitable Travels

2023-12-26 16:38:17 ET

Summary

- The online travel services industry is bouncing back after the disruptions caused by Covid-19, with Booking Holdings as the market leader.

- The industry is expected to continue growing, but at a more moderate pace, yet the online transition is becoming more rapid.

- Booking delivered a record year in 2022, with growth expected to persist.

Thesis

Bouncing back stronger after the worldwide Covid-19 disruptions, the online travel services industry appears to be improving constantly, establishing itself with consumers across the world. Booking Holdings ( BKNG ), being the market leader, has and continues to occupy a select spot with consumers' travel arrangement efforts. In this analysis, I explore the industry's prospects, as well as the company's financial performance, attributes, and valuation.

Business Model & Market Leadership

Booking's primary business model is a rather simple one; the company provides online travel reservation services on a global scale. Essentially, BKNG connects travel service providers with travelers across a range of services, with the most notable ones being accommodation, ground transportation, activities, and others. The company also earns revenue from advertising services and travel-related insurance services.

The company is the established market leader in a growing industry, recording revenues of $17.1B (2023), while competitors like Expedia ( EXPE ), Airbnb ( ABNB ), and Trip.com ( TCOM ) report revenues of $11.7B, $8.4B, and $2.6B respectively.

Covid-19 Aftermath and the Path Forward

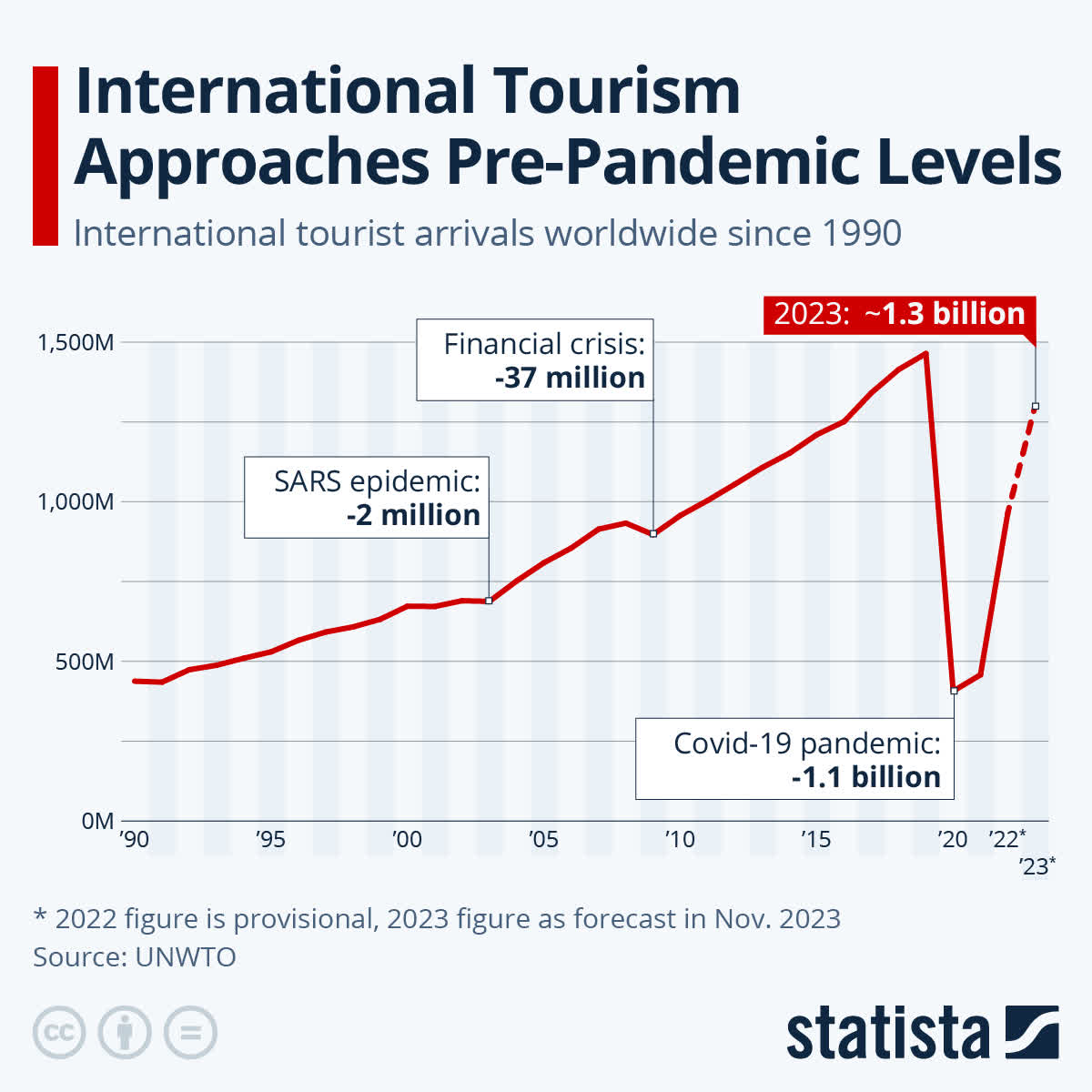

Few industries have been affected as much by the spread of the Covid-19 pandemic as the travel industry. After a couple of very tough years, however, the industry has almost fully recovered, with worldwide international tourism arrivals returning to pre-pandemic levels at the end of 2023. Given that international arrivals have tripled since 1990, it is fair to say that tourism (even with the Covid-19 disruption) has been a growing industry.

{kind=link}

Going forward, according to the World Tourism organization , growth in international tourism is expected to continue, yet at a more moderate pace, around 3% through 2030. A key obstacle that is slowing growth, is identified with higher transportation costs that increase the overall cost of travel. International tourism arrivals are expected to reach 1.8B by 2030. Emerging markets are expected to gradually gain a larger share of the international market, yet Europe is expected to maintain decent growth and market share.

The Online Transition

While the tourism industry recovers from the Covid-19 pandemic and is expected to grow moderately for the foreseeable future, more aggressive change is taking place when it comes to online booking services. The online travel market services have been on a mission to take over the industry, especially after 2020. According to Sphericalinsights.com , the global online travel market is expected to grow to $1.82T by 2030, compared to its value of $350B in 2021 (implying a 14.8% CAGR over 9 years). Having left Covid-19 behind and with aggressive growth projected going forward, online travel services seem like one of the best places to be positioned in as an investor.

A Record-Setting 2022 and the Path Forward

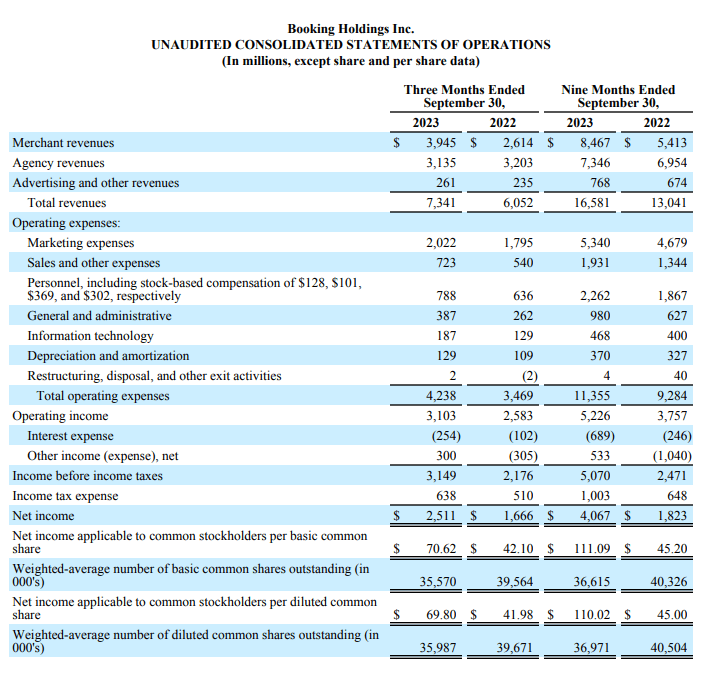

After a very tough 2020 that saw revenues cut in half and a slow-to-recover 2021, Booking has managed to set a record year in 2022. Revenues climbed to the all-time high level of $17.1B (56% YoY increase), while gross bookings increased by 58% on an annual basis. Overall, 896M room nights were booked through the platform, representing an impressive 52% increase from 2021. Net income of $3.1B in 2022 represented a 162% YoY increase, while Adjusted EBITDA came in at $5.3B.

For 2023, both management and analysts alike expect the growth trajectory to persist. The company has already delivered strong results, beating on Q1, Q2, and Q3 EPS. Revenue is expected to reach $21.3B for the full fiscal year, marking an implied 25% annual growth rate. In 2024, analysts expect revenue growth to moderate, with total revenue reaching $23.6B for the year.

Strong in the Bottom Line

Profitability has also been improving over the last few quarters, after having already established a very strong baseline in recent years. For Q3 2023, BKNG reported a 42% operating margin (relatively stable YoY) and an impressive net margin of 34% (up from 28% in Q3 2022).

{kind=link}

The online travel services market is very profitable across the board (mainly for market leaders like Booking, Airbnb, etc.), as it has yet to mature. Booking stands in a unique position, being the market leader, as its moat can dictate (to a large extent) prices and service affordability for consumers.

Balance Sheet Capability

As of the Q3 filing in 2023, Booking has also improved its balance sheet position. The company maintains a large $13.3B cash balance (increased from $12.2B in Q3 2022) and maintains a favorable current ratio of 1.44, indicating strong liquidity. Especially after taking into account the company's large cash balance, BKNG holds a rather small amount of long-term debt ($11.9B), presenting very low leverage.

Buybacks Boost Shareholder Returns

While BKNG does not pay any dividends, management has been committed to increasing shareholder value by allocating excess cash toward share repurchases. In 2022, the company repurchased $6.5B worth of shares and reduced its share count by 8% YoY. Overall, shares outstanding have decreased from 50M in 2017 to 37.4M as of the last filing. For the next couple of years, management expects buybacks to continue at similar rates.

Valuation is A Bit Overextended

After taking a look into Booking's peers, namely Expedia Group and Airbnb, we can see that BKNG trades at higher relative P/E multiples. More specifically, ABNB and EXPE trade at forward P/Es of 16.85x and 16.10x respectively, with Booking currently valued at 23.64x forward earnings. The company's strong stock price performance over the past year has even led to the current valuation gap with its peers being historically high. For reference 12 months ago, Booking traded at a forward P/E below 18x.

Despite the current valuation outlook for Booking appearing somewhat unfavorable, it is important to note that the company has the strongest profitability record compared to its peers. BKNG also trades at a 5.8x P/S and 17.4x EV/EBITDA multiples, all indicating that the stock is a bit overvalued at the moment.

Final Thoughts

After all things are considered, despite what might look like a pricey valuation, Booking is a company with a strong moat, good growth prospects, strong profitability and market share, as well as a healthy balance sheet with low leverage. Provided that Booking can continue to defend its market leader position through innovation and business expansion, profitability metrics should remain at very high levels for the foreseeable future, offering solid returns for investors. Even though a lower price point would make the stock especially attractive, still, I can see BKNG as a buy.

For further details see:

Booking Holdings: Well-Positioned For Profitable Travels