BOOT - Boot Barn Holdings Inc.: Growth Catalysts Drive Fast-Growing Retailer's Performance

2023-05-12 10:28:13 ET

Summary

- Boot Barn is a Western lifestyle retail chain offering footwear, apparel, and accessories.

- BOOT's growth and performance catalysts are its store expansion efforts and pricing strategy.

- With its reasonably higher ROE and profits retention, the company has a high potential to continue its growth.

Investment Thesis

Boot Barn Holdings, Inc. ( BOOT ) is a lifestyle retail chain that offers Western and workwear apparel, footwear, and accessories for women, men, and children; and provides home goods and gifts. It sells its products through specialty retail stores and e-commerce websites.

Although its stock has plunged 19.24% over the last year, it remains steadfast in its growth and performance, despite economic uncertainty. Catalysts for its performance are its efforts in steadily opening new retail stores year over year and its pricing strategy, which have driven sales. Moreover, the company has a reasonably high ROE and decent earnings growth that entices investors.

The stock, however, bears the risk with respect to the company's significant amount of non-cash earnings. With its plans to open up new doors in the future and a positive growth forecast in its revenues, I am optimistic about its performance going forward, prompting me to be bullish.

Catalysts For Growth

The apparel retail industry is dynamic in the global trade, with the emerging trends and headwinds that shape it. Despite this, companies in the industry have managed to perform well, including Boot Barn Holdings, one of the fast-growing lifestyle retailers. Below are its key growth and performance drivers.

Store Expansions

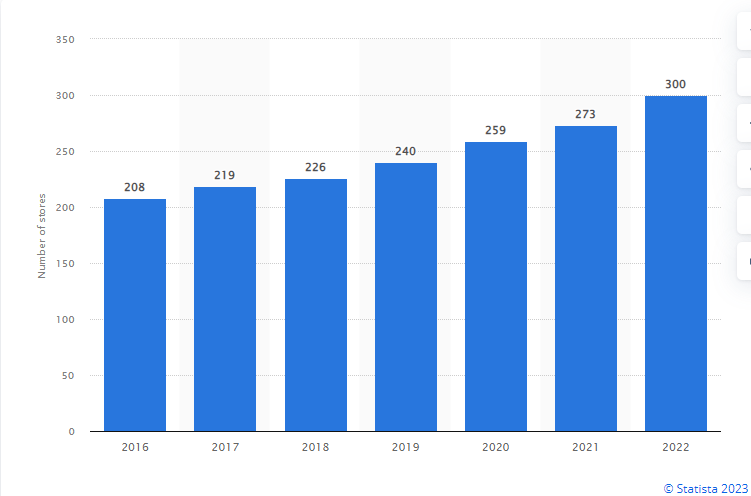

Retail store expansion is a strategy businesses approach to grow, reach more customers, and increase their market presence. When done successfully, this leads to increased sales and market share, among other positive outcomes. For the past few years, BOOT has steadily expanded its market share by increasing the number of its physical retail locations across states in the US. It had 300 operating retail stores at the end of the fiscal year 2022, including 28 new stores.

{kind=link}

The MRQ opened 12 new stores, ending the quarter with 333 stores in total in 41 states. As of April 2023, the company had a total of 347 retail stores across 43 states. BOOT anticipated opening 43 new stores at the end of the fiscal year, April 1, 2023. It is safe to say it achieved and surpassed its target with 347 stores currently compared to the 300 stores from the same previous year period. The company believes and expects to open about 800 new retail stores in the next 10 years, which I think is achievable given its current trend.

Pricing

Boot Barn Holdings has adopted selling its products at full price. This involves selling full-price products without discounts, special offers, markdowns, or promotional pricing. Case in point, despite the holidays when most retailers took on high promotional efforts to gain a competitive edge, the company maintained selling its products at full price .

Additionally, considering its exclusive brands, this pricing strategy is justified, and it is reasonable to presume that BOOT deems the full price justified by the value of the products it offers, thus no need for sales promotions or discounts. The products sell themselves. In light of this, it is plausible to say that the company uses value-based pricing to drive its sales.

The Outcome

Given the above drivers, we can only make an approximation of their outcome by deducing from their performance. These factors have driven its strong performance, which remained unwavering in the third quarter of fiscal year 2023. Revenues increased 5.9% from $485.9 million to $514.6 million in the previous year. Considering a longer period, net sales increased by 8.5% to $1.615 billion from $1.488 billion over the trailing twelve months.

BOOT's revenue is expected to grow 8.9% per year, faster than the industry (6.3%per year) and the US market (7.6% per year).

Simply Wall Street

Based on the above figures and its plans to continue opening new stores, I'm optimistic about the company's future revenues.

Return On Equity-Earnings Relationship

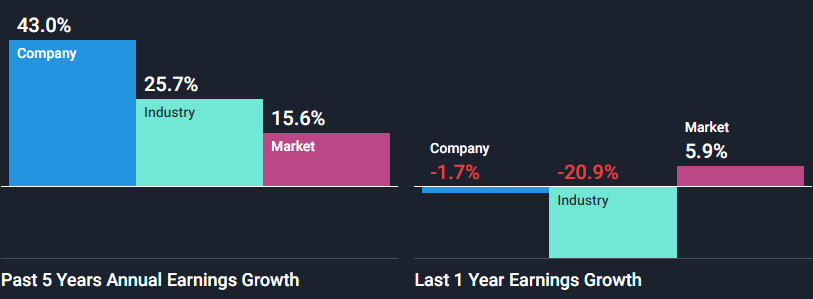

Measuring the company's profitability and ROE provides insights into how effectively it utilizes its investors' investments to generate profits. Boot Barn has a significantly high ROE of 23% and looks even better compared to the industry's average at 21%. One can argue that the strong return on equity propelled the company's stellar five-year net income growth of 43%.

{kind=link}

In determining the company's value, growth in earnings is a crucial factor. As seen above, BOOT has performed better over the past five years, as its earnings growth is higher than the industry's average. However, the company experienced a setback in its earnings growth recently. It registered negative growth in earnings, attributable to higher operational costs. Despite this, my view on the company's potential does not change.

Moreover, since the company is currently not paying dividends, this can only mean that it is reinvesting all its profits for future growth. BOOT retains all of its earnings for future expansion. It has a higher ROE, a key indicator of its growth potential, and if all variables remain constant, it will grow at a higher rate than its peers that do not possess these characteristics.

Warning Sign

Although the company has reported positive earnings, it has a high level of non-cash earnings; its profits are not backed by cash. It has registered negative free cash flows and cash flows from operations ((TTM)) at -$118.39 million and -$14.64 million, respectively. This indicates that the company consumes more cash than it generates and that its operating activities are not generating enough cash profits. This is a cause of concern, and investors should be on the lookout.

Conclusion

BOOT is one of the fast-growing lifestyle retailers in the US and has managed to perform well despite the challenges faced in the industry. Its pricing strategy and store expansion are the primary drivers of its growth and performance. As a result, the company has seen an incremental increase in its sales. The company holds that it will continue to open more retail stores. With its high ROE and high retention of profits, the company has the potential for more growth; therefore, we recommend buying to investors.

For further details see:

Boot Barn Holdings, Inc.: Growth Catalysts Drive Fast-Growing Retailer's Performance