BOOT - Boot Barn Holdings: The Run Higher Isn't Over Just Yet

Summary

- Boot Barn Holdings has had a great couple of months, with rising sales pushing shares higher.

- The firm has faced continued pressure on its bottom line, but the overall picture for the firm is still appealing.

- Add in that shares are still attractively priced, and it's likely that the firm can still move higher from here.

When you make the decision to purchase stock in a company or some other asset, you should always plan to hold it for an extended period of time before realizing the return that you believe is possible. Sometimes, however, the upside that you're anticipating does not take that long to materialize. One really great example of this can be seen by looking at Boot Barn Holdings ( BOOT ), an enterprise that serves as the largest lifestyle retail chain devoted to western and work-related footwear, apparel, and accessories in the US. Since late December of last year, shares of the company have roared higher, driven by a significant amount of optimism regarding the company and in response to continued sales growth achieved by management. When you dig a bit deeper, you do see some weaknesses on the company's bottom line. But given how shares are priced at the moment, I would make the case that some additional upside is still warranted from here.

A great fit so far

On December 20th of last year, I wrote a bullish article on Boot Barn Holdings and the prospects that it offers value-oriented investors. In that article, I talked about how impressed I was at the company's track record for sales, profit, and cash flow growth over the prior few years. I acknowledged at the time that the 2023 fiscal year was looking a bit mixed. But beyond that, I didn't see anything significantly wrong with the firm. All things considered, these factors, combined with how cheap shares were, led me to rate the enterprise a 'buy' to reflect my view at the time that shares should outperform the broader market moving forward. And outperform the market shares did. Since the publication of that article, the S&P 500 has achieved an upside of 3.9%. By comparison, shares of Boot Barn Holdings have seen an upside of 36.7%.

{kind=link}

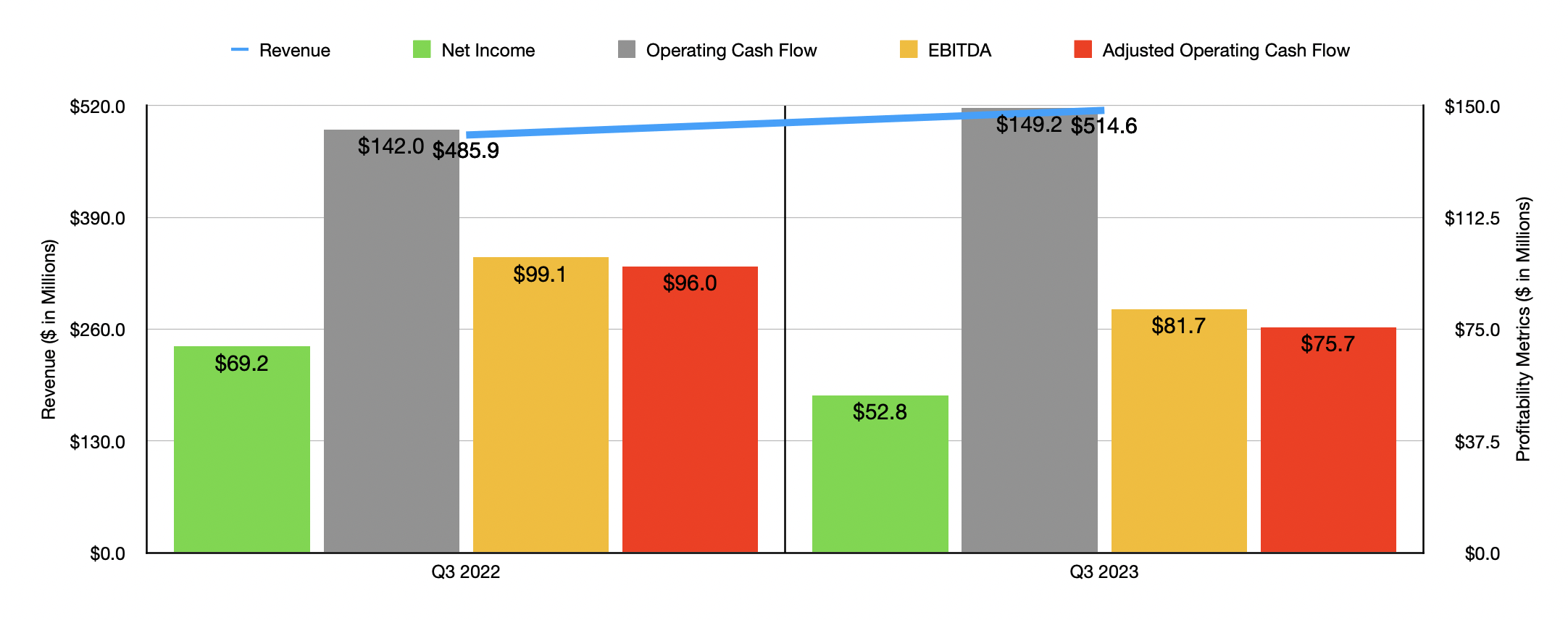

The only data that has been reported between then and now is data covering the third quarter of the company's 2023 fiscal year. For that quarter, revenue came in at $514.6 million. That's 5.9% higher than the $485.9 million reported only one year earlier. This move higher came about even as the business suffered from a 15.2% drop in e-commerce same-store sales. Excluding this decline, same-store sales for the business also managed to fall, dipping by 0.8% year-over-year. The increase in revenue during this time, then, was the result of additional store openings that the company had completed over the prior 12-month window. For context, from the start of the 2023 fiscal year through the time management reported results for that quarter, the business had opened 33 new stores. For 2023 as a whole, the company expects this number to rise to 43.

Although it was great to see the revenue increase, the company did see some weaknesses on its bottom line. Net income, for instance, dropped from $69.2 million down to $52.8 million. A big portion of this drop was associated with a decline in the company's gross profit margin from 39.4% to 36.5%. If this doesn't sound like much, consider that when applied to sales in the third quarter alone, it accounted for $14.9 million in pretax profits missing from the company's bottom line. The drop, management said, was largely due to factors like higher freight expenses, an increase in the cost of merchandise, and more. For the most part, other profitability metrics followed suit. The one exception to this involved operating cash flow, which rose from $142 million to $149.2 million. On an adjusted basis, however, it would have declined from $96 million down to $75.7 million. And finally, EBITDA for the business shrank from $99.1 million down to $81.7 million.

{kind=link}

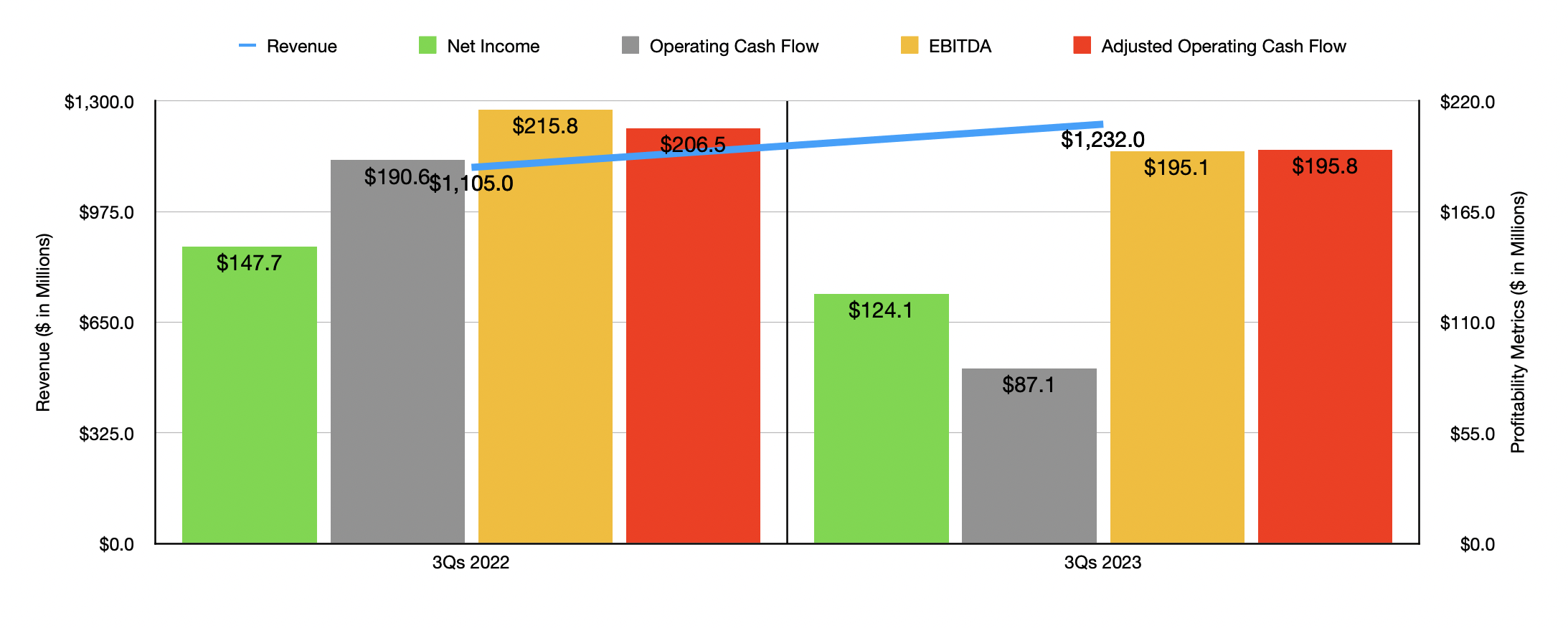

For the first nine months of the 2023 fiscal year, the picture looked very similar to what it did in the third quarter alone. Revenue, for instance, still came in higher year over year, having risen from $1.11 billion to $1.23 billion. Net income, on the other hand, declined from $147.7 million down to $124.1 million. In this case, operating cash flow did fall, dropping from $190.6 million to $87.1 million, while the adjusted figure for this declined from $206.5 million to $195.8 million. And finally, EBITDA for the company shrank from $215.8 million to $195.1 million.

When discussing expectations for the entirety of the 2023 fiscal year, management did say that revenue should come in at between $1.67 billion and $1.68 billion. That would place sales comfortably above the $1.49 billion reported for the 2022 fiscal year. For the coming years, overall same-store sales should range between an increase of 0.5% and 1%, with that number coming in even higher at between 2.5% and 3% if we ignore the drop in e-commerce sales. Overall net income for the company is expected to be between $167.2 million and $170 million. However, part of this figure includes a roughly 19 cent per share benefit from an additional $34 million in revenue that the company should generate because of an extra week in the fiscal year. Stripping this out, and using midpoint guidance for our number, we would end up with adjusted net income of $162.8 million for the year. No guidance was given when it came to other profitability metrics. But if we annualize the results experienced so far for the year, we would anticipate adjusted operating cash flow of $261 million and EBITDA of $258.3 million.

{kind=link}

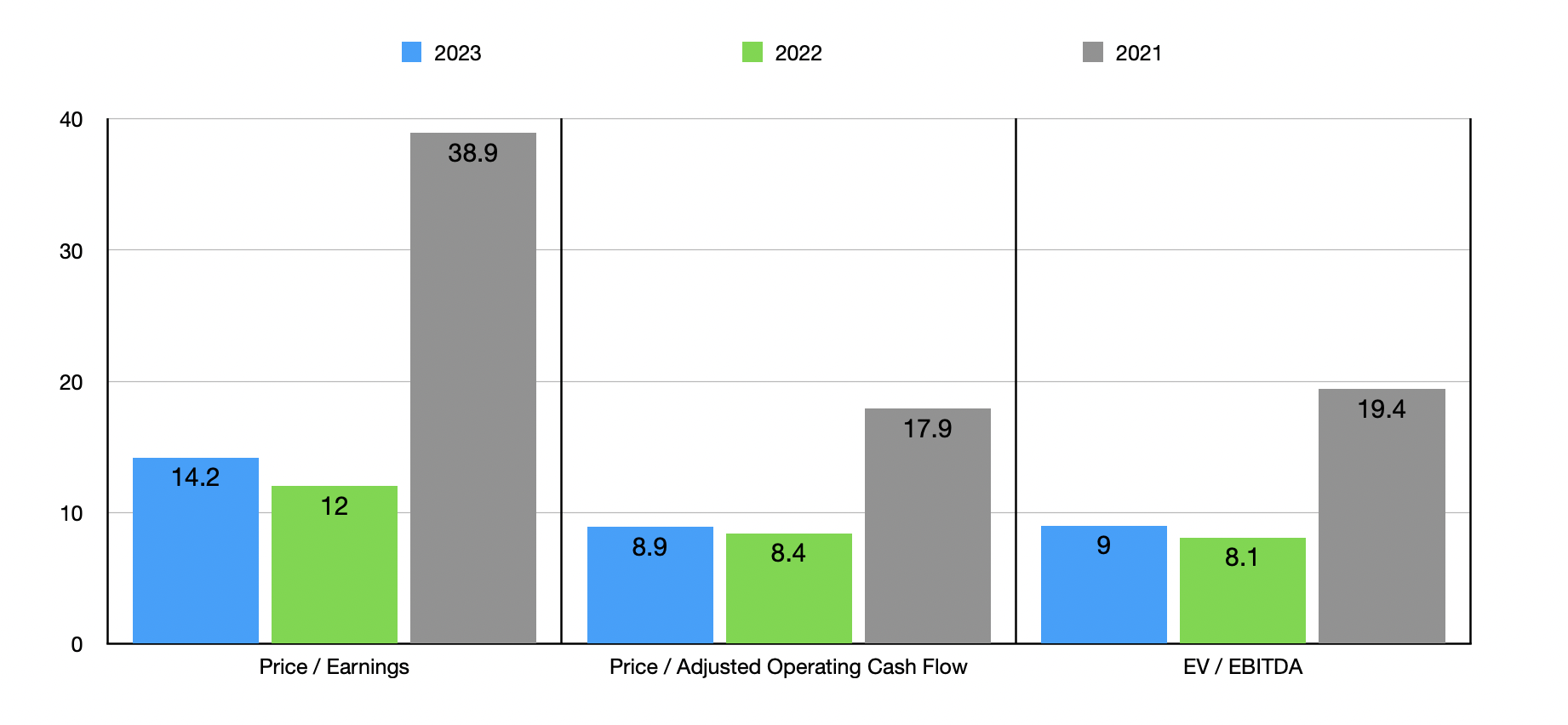

Based on the data provided, the firm is trading at a forward price-to-earnings multiple of 14.2. The price to adjusted operating cash flow multiple is quite a bit lower at 8.9, while the EV to EBITDA multiple should come in at 9. As you can see, all three of these metrics are a bit higher than if we were to use data from the 2022 fiscal year. But they are comfortably lower than what we get if we use data from 2021. As part of my analysis, I did compare the company to five similar businesses. On a price-to-earnings basis, these companies ranged from a low of 8.1 to a high of 68.4. In this scenario, we find out that two of the five companies are cheaper than our target. Using the price to operating cash flow approach, the range would be from 9 to 34.5. In this case, Boot Barn Holdings comes in as the cheapest of the group. Meanwhile, using the EV to EBITDA approach, the range would be from 5 to 6.7. This scenario is a bit different since our prospect comes in as the most expensive of the group.

| Company |

| Price/Earnings |

| Price/Operating Cash Flow |

| EV/EBITDA |

| Boot Barn Holdings |

| 14.2 |

| 8.9 |

| 9.0 |

| The Buckle ( BKE ) |

| 8.1 |

| 9.0 |

| 5.0 |

| Guess' ( GES ) |

| 11.4 |

| 13.8 |

| 5.5 |

| Abercrombie & Fitch ( ANF ) |

| 68.4 |

| N/A |

| 6.1 |

| Urban Outfitters ( URBN ) |

| 15.1 |

| 19.6 |

| 6.3 |

| American Eagle Outfitters ( AEO ) |

| 24.4 |

| 34.5 |

| 6.7 |

Takeaway

From all the data that I see, it is clear that Boot Barn Holdings stock continues to grow at a respectable clip. It is true that the growth is centered around a continued rise in store count. This is good from a structural perspective in the long run, but it is a negative to see comparable sales decline. This hit, however, can be chalked up to e-commerce operations pulling back following a couple of years of strength because of the COVID-19 pandemic. So in a sense, investors can view the comparable store sales issue as a return to normalcy. High costs are definitely a problem as well, not only for this firm but for many other companies across the economy at the moment. But those issues will eventually work themselves out as well. On top of this, the stock of the business is still cheap on an absolute basis, while being perhaps more or less fairly valued compared to similar firms. This combination of factors, though mixed in nature, does still tilt in the bullish direction in my opinion. This is not to say that upside from here will be significant. I do think that the easy money has been made. But on the whole, I think that some additional upside is still on the table.

For further details see:

Boot Barn Holdings: The Run Higher Isn't Over Just Yet