BOOT - Boot Barn Is One Of The Best Growth Stories In Retail

Summary

- BOOT has a lot of store expansion opportunities ahead of it.

- The development of its own brands, meanwhile, has driven margin expansion.

- The stock looks attractively priced given its growth opportunities.

Boot Barn ( BOOT ) is one of the best retail stories out there, and has plenty of white space to continue to expand and grow its business. Success in new non-traditional markets has helped validate the company’s expansion plans.

Company Profile

BOOT is a retailer focused on western and work-related footwear, apparel, and accessories. Its stores tend to be on the larger size, averaging over 10,500 square feet and are typically either freestanding or found in strip centers. The company also sells merchandise through its e-commerce websites.

Boots take up approximately one-third of each store’s selling space. This includes both western style boots as well as work boots. On the apparel and accessory side, the company sells a variety of denim, western shirts, cowboy hats, belts and belt buckles, western-style jewelry, and accessories.

BOOT sells a variety of top-name brands, as well as its own brands. Its own brands that it has developed include Shyanne, Cody James, Moonshine Spirit, Idyllwind, Hawx, Cody James Work, El Dorado, Cleo + Wolf, Brothers & Sons, Rank 45, and Blue Ranchwear .

Opportunities

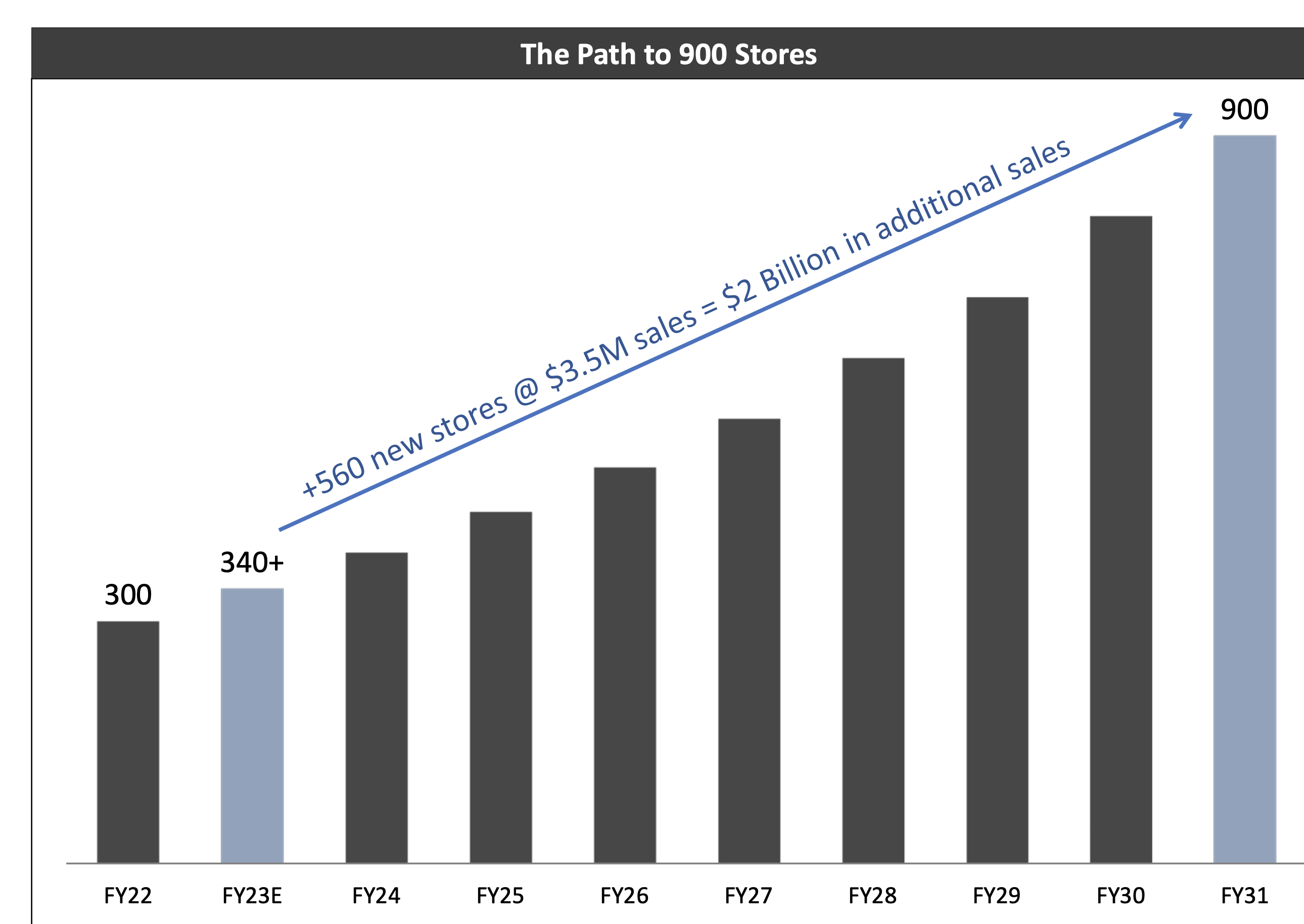

Continuing to expand its store base remains one of BOOT’s biggest opportunities. The company had 300 stores at the end of fiscal 2022 and believes it has the potential to support 900 stores across the country.

{kind=link}

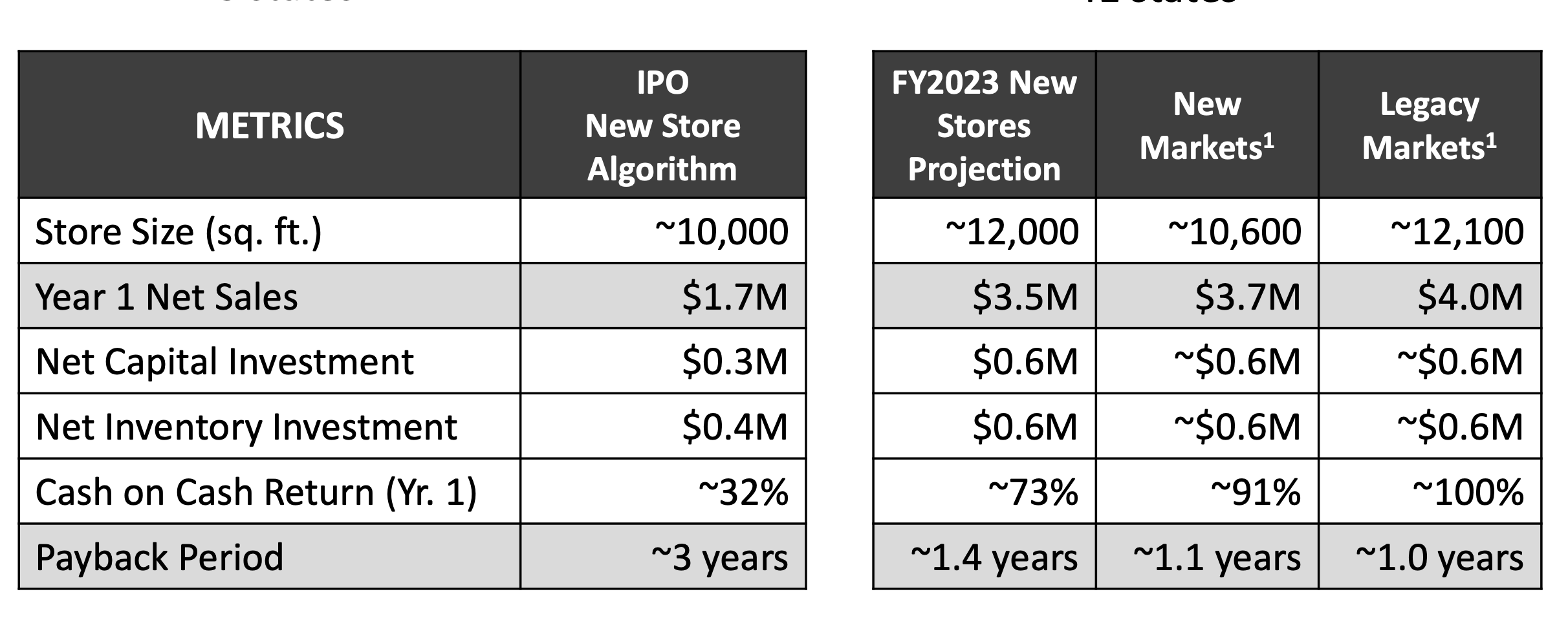

The company has done a great job of growing stores in both new and existing markets. What’s most impressive though is that new stores are getting larger and the payback period is getting shorter. BOOT’s new store payback period has gone from 3 years when it IPO’d to just over a year in fiscal 2022. For FY2023, meanwhile, the average new store size will be 20% bigger than it was at the time of its IPO, as well.

{kind=link}

With new stores averaging about $3.5 million in sales, the company projects it could add $2 billion in sales over the next 9 years. On its fiscal Q3 call, CEO James Conroy said:

“From a new store perspective, we continue to just be thrilled with the new store performance. - the number of stores that we're opening, their immediate volumes, their ability to sell western product in eastern parts of the United States, et cetera. So we are well set up to exceed our original 40 stores for this year. Our pipeline is very strong going into next year. We have the good fortune that our new stores are performing at much better than the original algorithm for sure and even better than what we're modeling them now. And that is in new markets and existing markets.

"So maybe harkening back a little bit to what we said at ICR, if we did nothing but continue to open stores for the next 6 or 7 years, we double the size of the company even if we didn't grow comps. So while we'll continue to try to look for growth in every part of the business, the new store engine is really quite compelling.”

As BOOT enters new markets, the company is also looking to expand its customer reach by broadening its assortment. BOOT has been very good with its merchandizing, and understands that styles in places like Texas can be different than in places in the Mid-Atlantic for example. Given the strong success of store openings in new markets, this has been paying off.

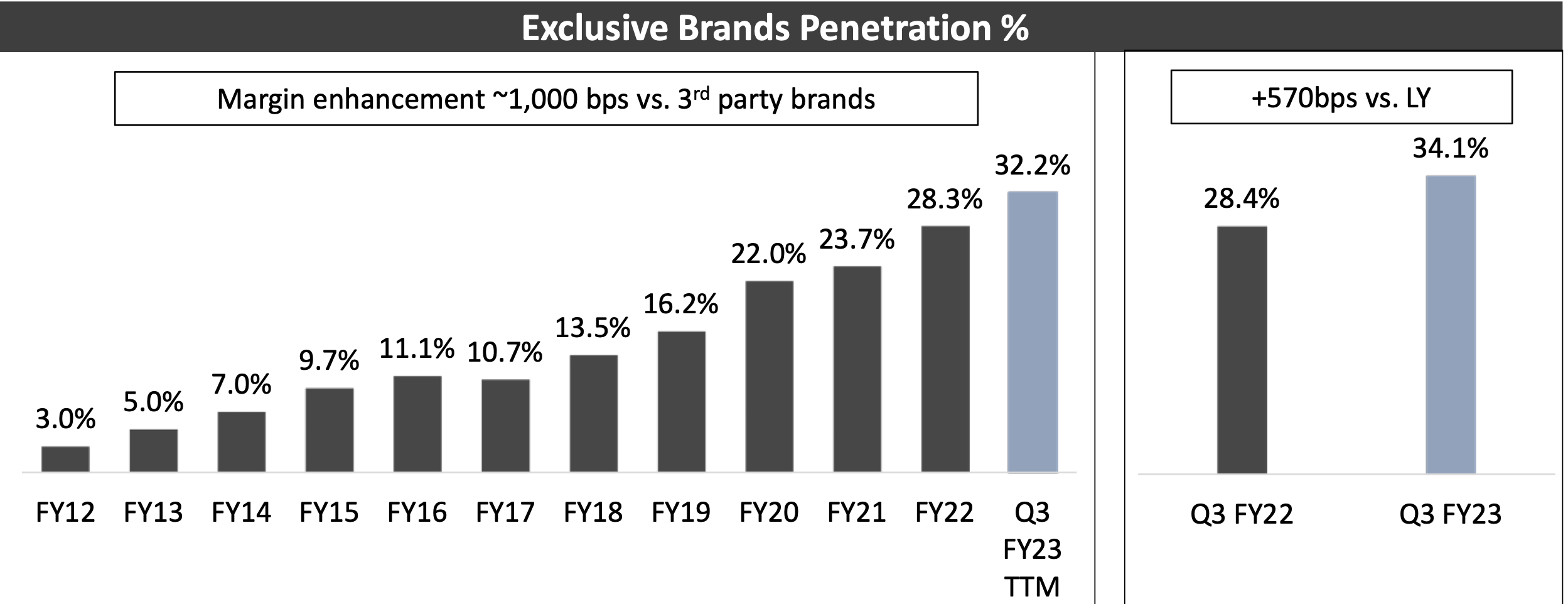

Another thing BOOT has been great with is building strong in-house brands. In fact, three of its top five selling brands are its own exclusive brands. Its own brands, meanwhile, are much more profitable than third-party brands, which has helped lead to continued margin expansion.

{kind=link}

On its FQ3 call, Conroy said:

“Our exclusive brand team continues to design excellent merchandise from both a price and quality perspective. Consistent with prior quarters, 3 of the top 5 selling brands in the third quarter were Cody James, Cheyenne and Idyllwind. We expect to drive continued growth in this area of the business with the 10 brands that currently comprise the portfolio. These brands not only provide us with competitive differentiation both in stores and online, but they are also accretive to the business by approximately 1,000 basis points of margin. The success of exclusive brands once again exceeded our original expectations. At the beginning of the year, we had anticipated expanding our exclusive brands by 300 basis points. We now are focusing -- we now are forecasting exclusive brands to grow to 33.4% of sales or approximately 500 basis points of penetration growth versus last year.”

Risks

Perhaps the biggest risk for BOOT is just how well will its stores continue to perform in non-traditional markets. So far, the results have shown the company can go into markets like the Mid-Atlantic and have the stores perform well. Meanwhile, in FQ3, its East and North regions showed the best same-store sales growth. That said, these are new markets with less history behind them, and we’ll have to see if there is a novelty effect that wears off.

BOOT also faces some fashion risk. However, it’s probably much less than most footwear and apparel retailers. About 75% of its sales come from replenishment items that are more functional in nature and need to be replaced about twice a year. These tend to be in the work and Western categories. As its grown, though, the company has added more fashion and casual country lifestyle customers, which have more fashion risk tied to them.

The macroenvironment and a stressed consumer is another risk for BOOT, as it is for most retailers. On the positive front, many of BOOT’s core markets are often tied to the energy industry, which has remained strong and likely will continue to remain strong given current supply/demand dynamics. However, its expansion into new markets and some more discretionary categories also increases its risk on the macro front as well.

It's also notable that the company saw a big jump in sales coming out of Covid lockdowns that saw its average store sales go from $2.7 million to $4.2 million. Most of this came from new customers, so there is a risk whether they will stay. Conroy addressed this phenomena at ICR in January, saying:

“The single biggest question we're getting from investors, and it's an understandable question, is your average store volume used to be $2.7 million. And then, somewhat magically, in April of '21, that $2.7 million spiked up to about $4.2 million, so more than a 50% growth in our average store volume. And the question has been, well, can you hold on to that?

“Well, there's a few proof points that would say we can hold on to that. The first is it's now been 21 consecutive months. The second is we've seen where the growth has come from, and the growth has come from new customers. So our strategy was to expand the definition of the Boot Barn brand. It seems we've successfully done that. ..

“Now the biggest question, and we're going to answer this question 100 times in the next 36 hours, is do they intend to stay? Well, we asked them, and 96% of them are either very likely or extremely likely to remain a Boot Barn customer in 2023. So from our perspective, that new level of $4.2 million is a new floor level, and we'll just build from there.”

Valuation

BOOT stock currently trades around 9x the FY 2024 (ending March) consensus EBITDA of $287.3 million and 8x the FY25 consensus of $340.1 million.

It trades at a forward P/E of 13x the FY24 consensus of $6.02.

The company is projected to grow revenue 8% in FY24 to $1.8 billion, before accelerating to 11% in FY25.

The company trades at a premium to other shoe-related retailers such as Designer Brands ( DBI ) and Shoe Carnival ( SCVL ), which trade around 5.5-6.5x EV/EBITDA. However, neither of those concepts have the white space and growth drivers as BOOT does. BOOT still has room to nearly triple its store base, which most retailers don't have the prospects of doing. It has also proven its ability to create multiple popular exclusive brands, which is also pretty unique.

While there is nothing in its space that has similar dynamics, another retailer with a lot of store growth ahead of it is Floor & Decor ( FND ). It trades at 18x 2023 EBITDA and a forward P/E of nearly 33x. It's projected to grow revenue 10% in 2023, just slightly higher than BOOT.

Conclusion

BOOT is one of the best stories in retail. It has a ton of white space ahead of it to continue to grow its store base at a double-digit clip. Meanwhile, it has been able to successfully develop its own brands to help drive margin expansion. At the same time, the concept has drawn in new customers and it's been able to successfully expand into non-traditional, new markets.

The stock looks attractively priced at current levels, and I could see it moving up to around $100 if the company continues to execute. That would put it at around a 10x multiple based on its projected FY25 EBITDA of $340 million.

For further details see:

Boot Barn Is One Of The Best Growth Stories In Retail