BOOT - Boot Barn's Same Store Sales Performance Seems Critical

2023-12-19 07:18:50 ET

Summary

- Boot Barn has achieved growth through store count growth with plans to open 52 new stores in FY2024 into a number of 397, and targets 900 stores by FY2030.

- Same store sales performance has driven margin growth for Boot Barn in FY2022 and afterwards, making the current decrease in same store sales concerning.

- BOOT stock seems to be priced with fair assumptions, making a hold rating constituted.

Boot Barn ( BOOT ) sells footwear, apparel, and accessories such as boots, shirts, jackets, and hats. The company’s offering is themed with a western style. Boot Barn continues to drive topline growth through new store openings and a focus on growing exclusive brands. The strategy seems to have worked very well in recent years, as the stock has returned an impressive CAGR of 36.2% in the past five years. Still, as same store sales have begun to come down after an impressive jump in FY2022, the future earnings growth has some concerns.

{kind=link}

Long-Term Growth Through Store Count Growth

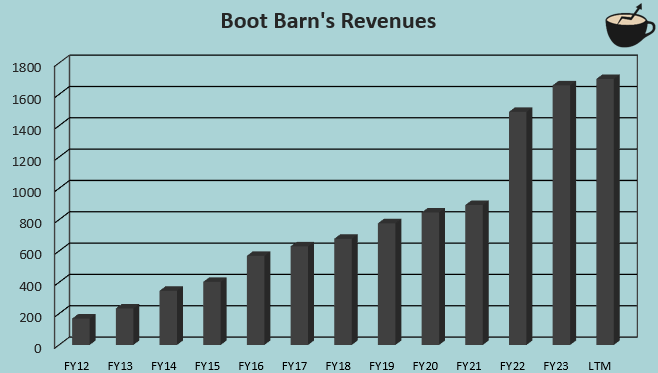

Boot Barn has sustainably grown its revenues in an organic manner. From FY2012 to current trailing figures, the company’s revenue CAGR stands at 22.2%:

{kind=link}

The overall long-term growth has been achieved through store count growth – from FY2012 to FY2023, the total store count has grown by 301% from 86 to 345, with an estimated 52 new store openings in FY2024. Boot Barn also has plans to even accelerate the store growth – for FY2030, the company targets a store count of 900. With the currently expected FY2024 store specific sales, the 900 stores would signal revenues of $3830 million for FY2030, up around 126% from the current trailing revenues of $1698 million. It must be noted that the calculation expects ecommerce scales to scale along with the brick-and-mortar revenues, though.

Store Growth (Boot Barn November Investor Presentation)

The targeted store count would signal highly accelerating store count growth – the targeted rate corresponds to average annual store openings of 84 from FY2025 to FY2030, above any figure that Boot Barn has been able to open in any single year so far. Although some acceleration seems very doable, operating a total store count of 900 could prove difficult. At the latter stages of the growth path, I would expect it to become harder for Boot Barn to find highly profitable places to open stores to.

Focus on Same Store Sales

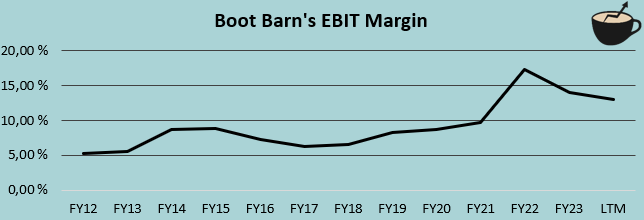

A good same store sales performance seems to be driving a great margin performance for Boot Barn – in FY2022, as the KPI increased by 53.7%, Boot Barn’s EBIT margin jumped from 9.7% to 17.4%.

Same Store Sales Performance (Boot Barn November Investor Presentation)

After the jump in same store sales in FY2022, Boot Barn’s EBIT margins have continued to stay at higher levels than in prior years; prior to FY2022, Boot Barn doesn’t have a single year with a double-digit EBIT margin, compared to a current trailing EBIT margin of 13.0%. The figure is down from the FY2022 high, mostly as same store sales have begun to fade – for FY2024, Boot Barn expects same store sales to fall by 5%.

{kind=link}

In the company’s Q2/FY2024 earnings call , Boot Barn’s management attributed the currently decreasing same store sales performance to a macroeconomic pressures, decreasing consumer spending across the United States. The company’s CEO Jim Conroy outlines that it doesn’t want to drive short-term growth in the KPI through marketing and discounts, but rather wants to drive a healthy long-term strategy.

Investors should still question the current same store sales figure’s sustainability. The FY2022 increase seems very excessive even with successful marketing including partnerships with NASCAR teams, athletes, and country music artists, as well as the partnership with The Dallas Cowboys, and the highly inflationary economic environment. The company has communicated that same store sales are at an elevated level; I believe that the same store sales will continue to come down even in FY2025. Still, the significant pressure on margins should be partly offset by operating leverage as Boot Barn continues to scale the operations with new store openings.

Valuation

{kind=link}

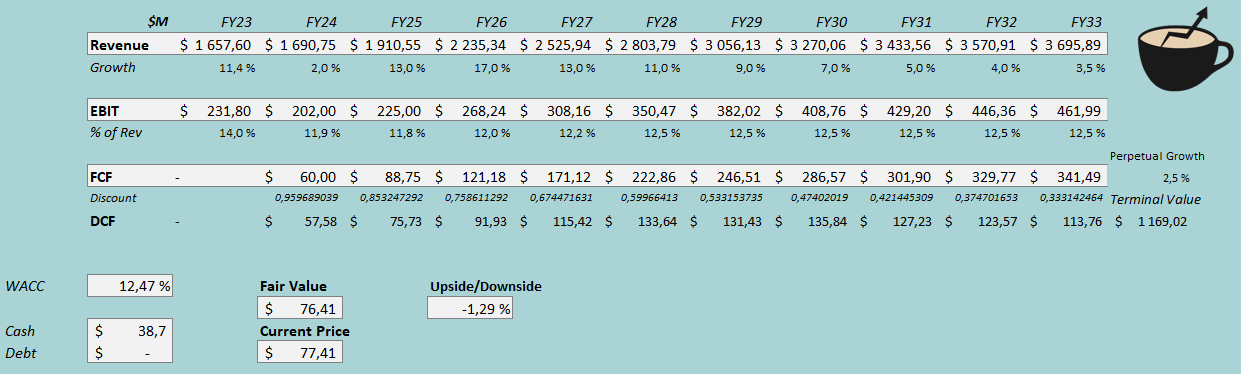

To estimate a rough fair value for the stock, I constructed a discounted cash flow model. In the model, I estimate the same store sales growth to come down in FY2024 as well as FY2025 – FY2025’s growth of 13% in the model is achieved through significant store openings. Along with the slight decrease in same store sales, I estimate the EBIT margin to come down by 10 basis points despite higher sales. After the year, I estimate Boot Barn to achieve further growth through store openings. The revenue estimate of $3270 million represents slightly lower same store sales than in FY2024, and a store count between 700 and 800. In addition, I expect operating leverage with the higher level of operations, scaling the EBIT margin from 11.8% in FY2025 to 12.5% in FY2028 and forward. As Boot Barn’s growth slows down within the years, I estimate the cash flow conversion to improve in steps.

With the discussed estimates along with a cost of capital of 12.47%, the DCF model estimates Boot Barn’s fair value at $76.41, very near the stock price at the time of writing. I believe that the stock is priced for fair baseline assumptions, although a higher-than-expected same store sales fall could signal significant underperformance for the stock, as margins would inevitably fall with the KPI.

{kind=link}

The used weighed average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

Boot Barn doesn’t seem to leverage debt in the company’s financing, and I estimate the financing structure to continue with a long-term debt-to-equity ratio estimate of 0%. For the risk-free rate on the cost of equity side, I use the United States’ 10-year bond yield of 3.96% . The equity risk premium of 5.91% is Professor Aswath Damodaran’s latest estimate for the United States, made in July. Yahoo Finance estimates Boot Barn’s beta at a figure of 2.30 . I believe that the estimate is unreasonably high – the company has demonstrated mostly a good performance in the current economic turbulence, and other companies with similar products don’t have as high betas. In addition, Boot Barn’s long-term debt-free balance sheet makes the company safer. To get a more fair beta estimate, I use the average of four mostly similar companies’ betas – with TJX Companies’ (TJX) beta of 0.88 , Dick’s (DKS) beta of 1.55 , Ross Stores’ (ROST) beta of 1.03 , and Gap’s (GPS) beta of 2.09 , the average comes up to 1.39. Finally, I add a small liquidity premium of 0.3%, crafting a cost of equity and WACC of 12.47%.

Takeaway

At the moment, Boot Barn is at an interesting point. The company’s same store sales have begun to fall after a very high jump in FY2022. A significant decrease would highly likely result in lower margins; in my opinion, the KPI is the most critical indicator for investors. As macroeconomic pressures play a part in the decrease, the current view into a sustainable same store sales level is quite clouded. Another factor to count is Boot Barn’s significant plan for store openings, going from a FY2024 estimate of 397 into a FY2030 target of 900; I believe that if achieved, the higher store count should attribute very positively to margins through operating leverage. The current stock price seems to reflect fair financial assumptions, which is why I have a hold rating for the time being.

For further details see:

Boot Barn's Same Store Sales Performance Seems Critical