BAH - Booz Allen Hamilton: Current Overvaluation Is Making It A Hold

2023-10-20 05:48:02 ET

Summary

- Booz Allen Hamilton has seen significant growth and outperformed expectations in recent weeks.

- The company has a strong customer base and a track record of success in various sectors.

- However, the current valuation of the company is prohibitive, making it a 'Hold' rating. I don't see this rating changing easily, given the trends the company is going through.

Dear readers/followers,

So, if you follow my articles you know that I unfortunately went "HOLD" on Booz Allen Hamilton (BAH) back in 2022 in fall. The company continued to grow beyond that though, and even though I sold the remainder of my position at what I thought was a great valuation, over $100/share, the company continued climbing, and in particular in the last few weeks, really shot up quite significantly.

Regrets are not part of my M.O. - but I try to learn from mistakes that I do. Trimming Booz Allen might have been a mistake, but it also needs the consideration that what I invested in has actually gone up more than the 22% RoR we've seen since.

My last article on Booz Allen Hamilton was a long time ago - back in -22. You can find this article here .

In this article, I'm going to be updating my case on Booz Allen and see where the company goes from here on.

Booz Allen Hamilton - An Upside is harder to see here

First off, the reason why the company is up the last few weeks and since September is a number of won contracts, as well as ratings upgrades. Did I expect this to happen when I sold my position?

I expected some of this upside, but I did not expect this material improvement in valuation. If I had expected this sort of outperformance, I obviously would not have sold my position and invested different capital in the things that I bought instead.

For instance, look at what has happened to the company since one of my earlier articles back in December of -21.

Seeking Alpha BAH article (Seeking Alpha BAH article)

Obviously, I cannot take credit for that full RoR. I wish I could - but I changed my recommendation, and I also sold everything I had in the company a few weeks/months after that article, in accordance with this stance.

But I want to clarify that this is what I am looking for in my investments.

Sometimes I go out too early. Sometimes I go out just right , and go into a new investment that outperforms on its own right. The capital I invested has grown more than BAH in the same time since I sold, but a better example of in and out for me is Heidelberg Cement (HDELY). I sold everything I had back in April, and the company has not gone back above €80/share since.

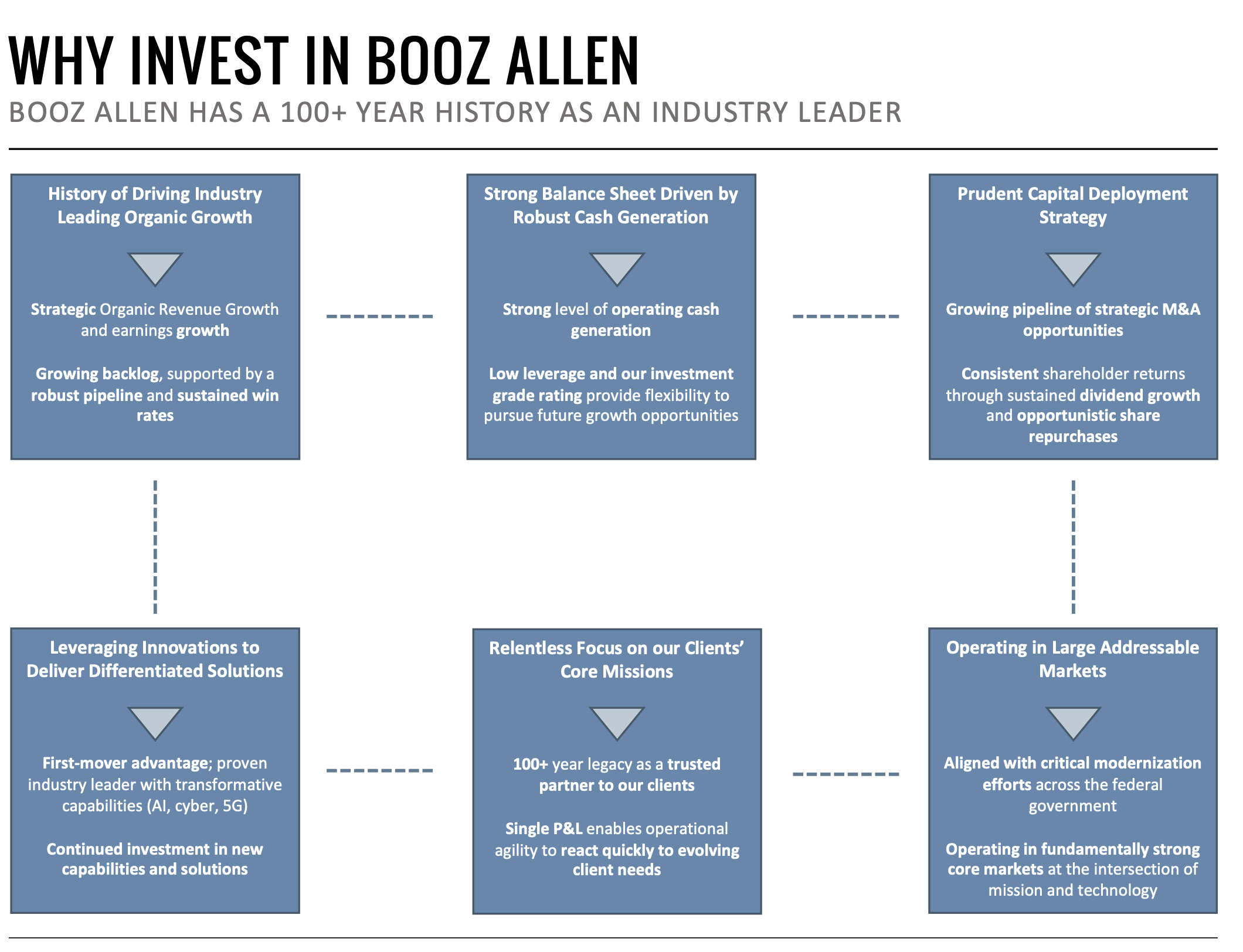

Booz Allen is an Industry leader, and some might argue this is a "Buy and hold forever" stock. It's an argument - not one I agree with, but you could certainly make it.

{kind=link}

The company consists of tens of thousands of specialists in their fields, 28% of which are military veterans, 65% of which hold security clearances, and 87% of which hold at least a bachelor's degree.

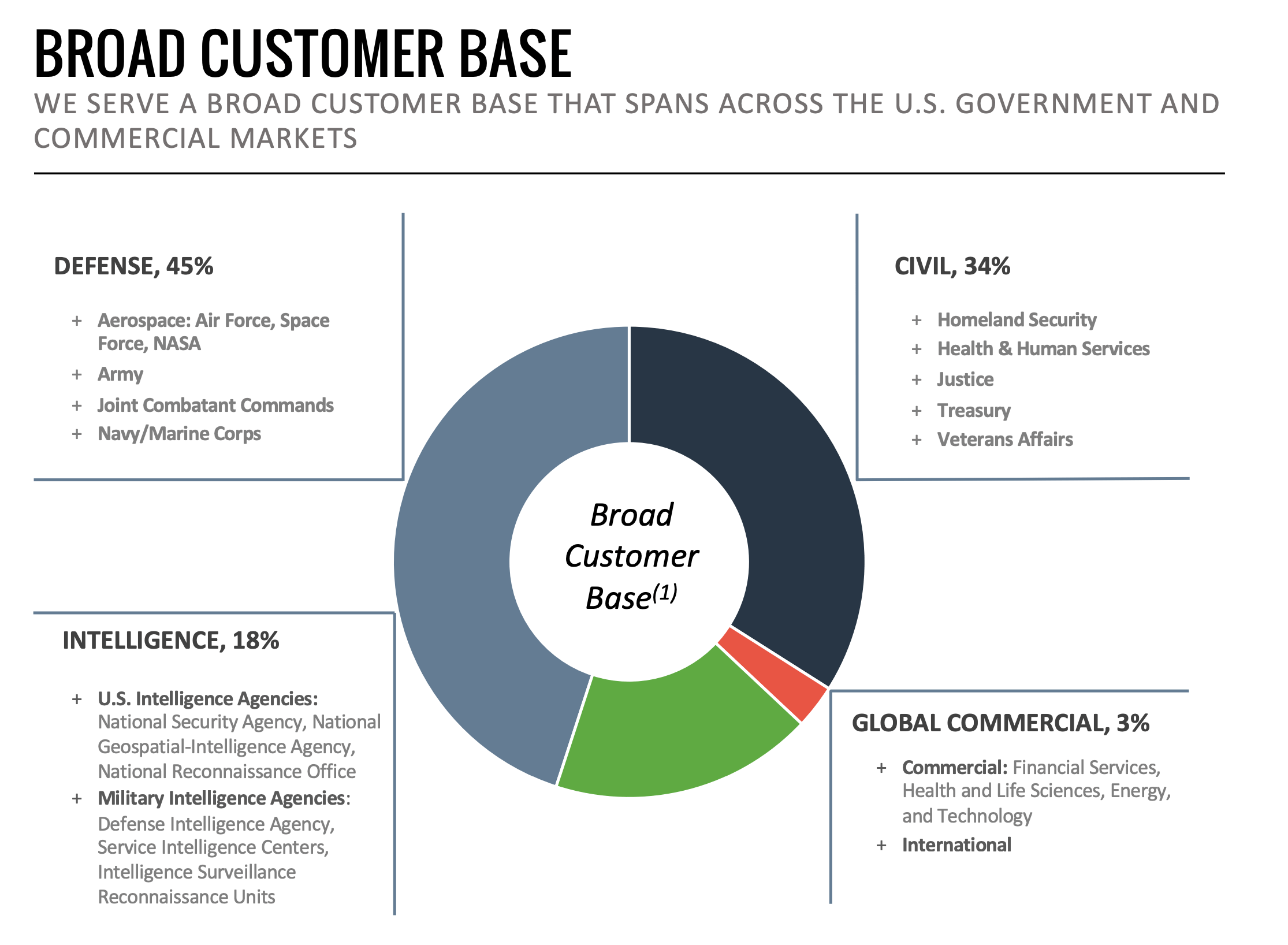

The company is a collection of specialists working to change the world using AI, Cyber, Data Science, Digital engineering, and other areas with an extremely attractive set of customers. 45% of these customers are defense, and 18% are US and military intelligence. You can hardly, as I see it, imagine a better customer base than this.

{kind=link}

The company is less cyclical than you might expect from a player in these fields depending on the defense budget and similar trends. However, most of the time, these budgets don't go down (if you account for inflation.)

Also, BAH has been around for a century. The company has been through every conceivable situation, including world wars, geopolitical turmoil, and every other situation that could impact a business like this either positively or negatively.

For the last few years, BAH has been increasingly investing capital back into its own business and also took advantage of at times low valuation to repurchase shares - most during the undervaluation of 2022, which was when I invested as well.

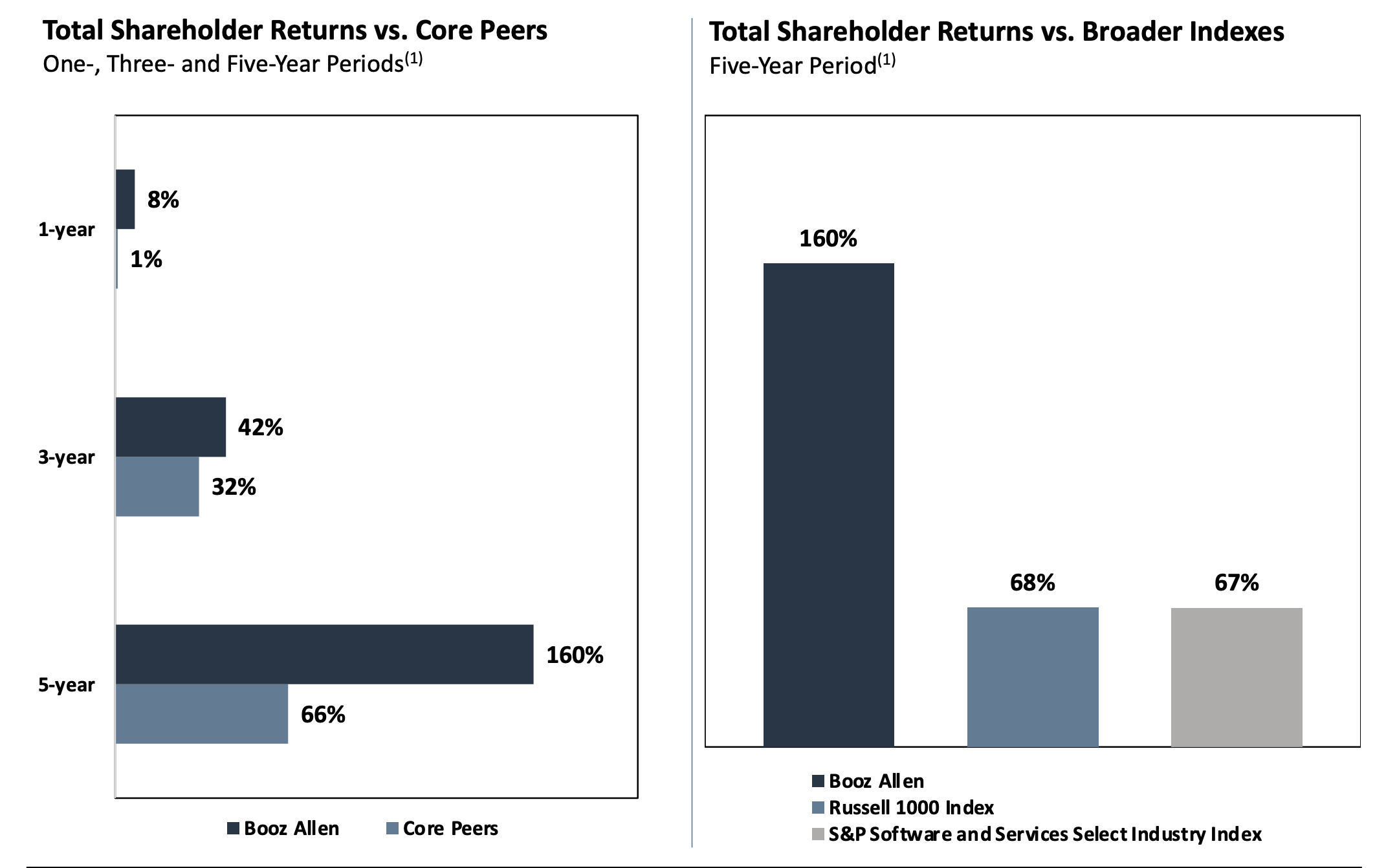

Booz Allen Hamilton not only continues to outperform peers significantly, but also the broader market.

{kind=link}

What's more, the company continues to hold a very strong overall backlog. While the book-to-bill isn't at record levels like in 2019, it remains comfortably above a 1.1x level, currently at 1.19x. The company has $42B in what it considers its qualified pipeline, and around $6B of proposals in process, around $11B worth of submitted proposals to consider.

Booz Allen has a superb win rate of 66% on new projects, and 88% on recompetes, showcasing just how high the company's expertise is in some of these sectors and segments.

The company reported its 1Q24 fiscal, which goes some ways to explain the outperformance here as well, building on an 18% YoY revenue growth and a 17% net income growth in this sort of macro environment. An EBITDA improvement of over 20% is nothing to stick under the table here, with a 30%+ improvement in adjusted diluted EPS.

The company has elected to already give us 2024E guidance, expecting revenue growth in the double digits on the high end, 11%, with adjusted EBITDA of over a billion, up to $1.1B on the high end, which comes to a diluted EPS of almost $5/share on an adjusted basis. If this was to materialize, it would be a first step towards the 2025E goal of $1.3B worth of EBITDA with a double-digit EBITDA margin and organic revenue growth towards the high single digits - it already beat this in 1Q24.

So, what I am saying is that things are going extremely well for Booz Allen. The company has shown investors that not only can it outperform in difficult environments, it can beat expectations as well.

I say this because despite what I am about to say in my valuation section, I consider this to be an extremely qualitative business.

However, it's not a business that I consider to be investable at this time.

How can those two things be said in the same article?

Simple.

Let's look at company valuation.

Booz Allen Hamilton - The valuation means we're looking at a prohibitive "HOLD" rating

You know that I invested in BAH in 2022 and 2021. The difference at that particular time was simple. The company traded at a conservative normalized P/E of below 18.5x or between 15-19x P/E.

Where does it trade today?

At a share price of almost $130/share, Booz Allen is based on current estimates trading at a P/E valuation of 27x P/E normalized. That is not a valuation where I want to see many companies or indeed would invest in a company like this.

In fact, if you look at a 10-year basis, at any time the company was at this valuation or close to it, your eventual RoR would have been sub-par in the mid-term had you invested at that time (Source: FactSet, S&P Global).

Yes, the company does not miss estimates. I do in fact believe that the company will see exactly these returns. I'm just not willing to premiumize the company in a fashion that would legitimize this valuation or an upside to it.

If you are looking for an upside here, you in fact need to estimate the company at or above that 25x P/E to see any sort of double-digit upside. If you were to estimate Booz Allen at even 20x P/E, which is the 5-year normalized P/E premium the company typically commands, your returns due to the company's yield would only be 2.5% per year. (Source: F.A.S.T Graphs).

This is not, as I see it, even close to acceptable in a 5%+ interest rate environment. We're worth more than that - and you as an investor certainly are.

I want you to realize that the company, during the last 10+ years, has never traded at this sort of valuation. Not once has this company been above 26x normalized P/E.

That's a very bad situation to go in with a high conviction unless you know exactly why you believe the company to outperform from here.

Don't get me wrong. If BAH goes back down to say, 15-18x P/E, I would throw myself over the shares like someone starving - I want shares in the business - but I only want them at a price where I would have a high conviction of having a very good rate of return.

That is not the case here.

S&P Global analysts consider the company positively and a "BUY", which does not surprise me. These analysts tend towards being fairly backward-looking and tend toward allowing, rather than questioning very high premiums, but this is not my M.O.

The current set of targets begins at $120/share and goes all the way to $145 with an average of $130/share. You should note, interestingly enough, that the same analysts gave the company no more than a $75-$80/share price when I was calling for the company to go triple digits. The feeling I get when following analysts here is that they tend to follow the share price.

I do not follow the share price - I follow fundamentals and valuation. And those show me that the company will eventually not be headed up further, but down.

For that reason, here is my thesis on Booz Allen Hamilton at this time.

Thesis

Here is my current thesis for Booz Allen Hamilton

- This company is a "HOLD" due to the only reason that I believe to matter. Booz Allen is incredibly overvalued at anything approaching a $125+ share price - yes, even with the growth rates we're seeing. You're able to get double-digit RoR at very conservative risk cases, and this investment does not, as I see it, measure up in comparison.

- That being said, Booz Allen is an extremely qualitative business with a very solid upside at the right valuation.

- The risks are relatively few and mainly focused on things like hiring, contract mix, and margins - nothing unique, and to some degree, not something the company itself can easily control of influence.

- However, I do not consider it buyable here, and consider it a very firm "HOLD". I do not believe that you will outperform the market over time if you buy here.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

The company no longer fulfills my criteria, at least not beyond 3 out of 5, and qualifies as a "HOLD" here.

For further details see:

Booz Allen Hamilton: Current Overvaluation Is Making It A Hold