MGA - BorgWarner: An Electrifying Future Up For Grabs At A Huge Discount

2024-01-06 00:33:20 ET

Summary

- BorgWarner is a well-positioned automotive company with a wide economic moat and a focus on innovation in the EV parts and solutions market.

- The company has a strong financial situation, with positive returns and solid profitability despite multiple acquisitions and a difficult macro environment.

- BorgWarner's valuation suggests that its shares are heavily undervalued, potentially to the tune of 56%.

- Despite a potentially recessionary market environment in 2024, I find it difficult to see how much further valuations could realistically fall in the long run.

- Strong Buy rating issued.

Investment Thesis

BorgWarner ( BWA ) is an automotive company that produces a wide range of ICE and EV components, solutions and parts. The firm has a wide economic moat thanks to significant intellectual properties, switching costs and tangible cost advantages.

A mostly positive Q1-Q3 of FY23 appears to have gone ignored by investors with share remaining heavily discounted both according to valuation metrics, an absolute analysis and according to The Value Corner's proprietary intrinsic value calculation.

Overall, I believe BorgWarner is well positioned to take advantage of a growing EV marketplace thanks to continuous innovation and unique designs. When combined with a potentially massive 65% discount in shares, I rate BorgWarner a Strong Buy.

Company Background

BWA FY23 Q3 Presentation

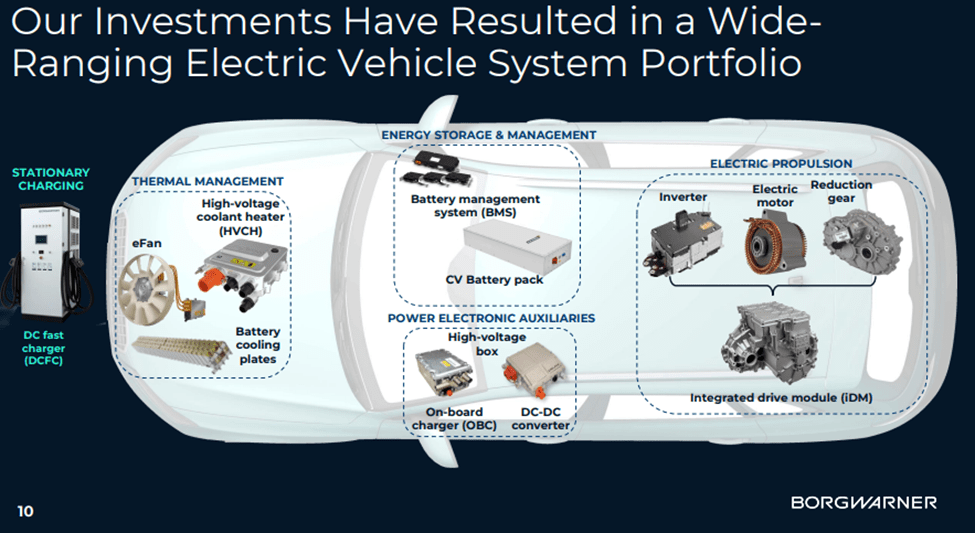

BorgWarner is an automotive company specialized in the manufacture of solutions for ICE, hybrid and electric vehicles. The firm manufactures a range of products from traditional combustion turbochargers, eBoosters for electric motors along with a host of other automotive components such as emissions systems, ignition technology, heaters, battery packs and even automotive software.

The firm has continuously innovated their product range to ensure a prosperous future and strong position within the automotive industry despite the transition away from ICE vehicles to more HEVs, BEVs and alternatively fueled vehicles.

BW’s diversification into eBoosters and eTurbos along with the provision of many other automotive components still required in electric vehicles (such as bearings, rotating components, control modules and torque-management products) has not only allowed the firm to remain relevant in today’s market, but to actually expand the moatiness of their business as a whole.

BWA FY23 Charging Forward Presentation

As of Q3 FY23, BW has over 61 manufacturing locations across 19 countries and employs more than 38000 people including 7500 engineers.

The firm recently spun-off their Fuel Systems and Aftermarket segment as PHINIA in order to unlock more value that BW believed was present in these two business segments.

BorgWarner is headed today by Frédéric B. Lissalde who took over the helm of the company back in 2018. Previous to his appointment to CEO, Lissalde served in multiple management positions including COO, Vice President and General Manager of BorgWarner Turbo Systems LLC.

Lissalde has an extensive set of industry experience and education within the field of automotive engineering while his primary experience at BorgWarner itself further suggests he is well suited for the role of CEO.

Economic Moat – In Depth Analysis

BorgWarner has a huge amount of industry knowledge when it comes to automotive solutions manufacturing and development with the firm overall harboring a wide economic moat.

Since the late 1990s, BorgWarner has continued to innovate within the automotive technology industry by developing new products, solutions and technologies to meet automaker demands. The last 30 years has seen most governments push for a huge shift in environmentally oriented policies which has forced automakers to extract more efficiency and power from their engines.

BW has responded to this long-term trend by increasingly focusing on efficiency-oriented solutions such as turbochargers, integrated drive modules and even hybrid power systems in order to retain supplier relationships with the large automakers.

The firm has also acquired multiple businesses over the last decade in order to rapidly develop their e-power oriented product lineup. The most recent acquisitions of Eldor Corporation’s Electric Hybrid Systems Business and Hubei Surpass Sun Electric Charging business are only the latest developments in what has become a core element of BW’s future enterprise.

BWA FY23 Charging Forward Presentation

The year 2021 saw BW launch the Charging Forward 2027 strategic initiative which the firm hopes will allow BorgWarner to become an integral element of the EV automotive scene. In total, BW hopes to gradually reduce manufacturing volumes for their ICE related components and solutions while rapidly increasing the amount of electric power-oriented products available to automakers.

{kind=link}

BW has rapidly begun to invest in electric vehicle related technologies to ensure this seismic shift in automotive solutions technology does not result in the firm becoming obsolete. To avoid this reality from synthesizing, BW already offers what can only be considered as a holistic portfolio of EV related technologies, components and solutions.

Fundamentally, I believe the clear goals set of BW along with tangible progress already being made towards achieving the goals set forth in the Charging Forwards 2027 initiative should allow BW to remain an integral element of the automotive industry.

The overall industry knowledge beheld by BW helps generate a narrow economic moat for the firm as the capital and time required for a competitor to match the R&D and innovation rates present at BW would be astronomical.

BW also generates significant moatiness from their supplier contracts they strike with the automotive OEMs. Traditionally in the automotive segment, OEM manufacturers contract entire engine, drivetrain and emissions programs to suppliers such as BorgWarner.

In the case of drivetrains and engines in particular, many of these supply contracts are agreed for time periods of up to a decade. This lengthy contract period ties the OEM closely to BorgWarner which ultimately helps sure-up revenues and total production volumes while also allowing BorgWarner to benefit from huge switching costs facing the OEM.

During contract cycles it is almost entirely unviable for an OEM to switch away from BorgWarner as a supplier as the change would essentially require a complete redesign of the firm’s engine or drivetrain. These switching costs also apply in new engine designs as OEM’s tend to reuse or build upon existing designs (which would still rely on BorgWarner components) when creating new engine or drivetrain designs.

These switching costs and close supplier ties between BW and the OEMs help generate significant moatiness for the firm as the threat of BW’s customers switching to new components manufacturers is decreased significantly.

BorgWarner most likely also benefits from a cost advantage arising from the aforementioned lengthy supply contracts forged with the OEMs. Longer contracts allow BW to supply a constant stream of products already developed and tested with little to no further R&D being required. This allows the firm to maximize the efficiency of production of these components which ultimately helps increase the margins BW is able to extract from their manufacturing processes.

Fundamentally, it is exactly these long-term supply contracts that allow BW to generate significant margins on their operations thus permitting the firm to reinvest a portion of their revenues back into R&D in preparation for the next set of contract and supply negotiations.

Overall, I believe the massive industry knowledge held by BW, their close ties with automotive OEMs and the cost advantages arising from lengthy supply deals generate a wide economic moat for the firm.

Financial Situation

From an operating performance perspective, BorgWarner is a relatively successful and profitable company.

BW has 5Y (FY22-FY18) average ROA, ROE and ROIC of 5.63%, 13.31% and 8.99% respectively. These returns are quite positive indeed with the firm tangibly outpacing inflation with their returns on both equity and invested capital.

While these returns are contracted by around 5-6pp compared to the figures generated in 2010-2013, it must be noted that BW is currently engaged in a relatively capital-intensive redesign of their business structure to suit the growing demand for EVs.

Considering this seismic shift in automotive product demand, the ability for BW to continue generating healthy profits despite a massively changing market environment further bolsters my thesis that the firm is accurately meeting OEM demand for automotive products.

BW’s WACC is currently around 7.07% which illustrates that BW continues to generate higher returns on their investment than it costs the company to raise the capital needed for said investment.

Furthermore, when compared to industry competitors such as Magna International ( MGA ) and Vitesco Technologies ( OTCPK:VTSCY ), BW’s ROA, ROE and ROICs are around 5pp and 9pp higher respectively.

BW also has 5Y average (as measured from FY22-FY18) gross, operating and net margins of 19.69%, 10.20% and 5.74% respectively. The relatively high and unchanged gross margin in particular illustrates that BorgWarner’s fundamental business model is profitable and healthy.

{kind=link}

FY23 has been a relatively profitable year for the firm with around 12% revenue growth in Q1 being slightly offset by flatline figures in Q2 . Q3 saw BW grow their net sales by 12.5% thanks to solid growth in the automotive segment fueled by cooling cost inflation and increased demand in North America, Europe and China for “e”-related products.

BorgWarner signed agreements with a major North American, European and one Asian OEM to supply multiple different e-related solutions which represent huge successes for the firm.

Furthermore, the North American and European OEMs are noted as being “premium” automakers which often result in slightly more profitable agreements that with more margin-pressured general automakers.

Gross profits increased 7.4% in Q3 thanks to COGS growth of 11.5% being outpaced by the 12.5% growth in net sales. The excellent cost control being exhibited by BW is welcomed and suggests the management team is focused on not only growing the firm’s range of EV related offerings but simultaneously maintaining solid profitability at the firm.

{kind=link}

SGA expenses have been essentially flatline in FY23 while the firm has seen some minor restructuring expenses as a result of the acquisitions made by BW throughout 2023.

{kind=link}

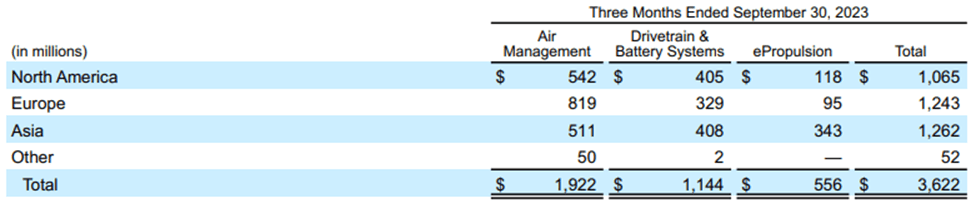

BW’s Air Management business segment continues to generate the majority of revenues for the firm while the drivetrain & battery systems and ePropulsion segment continue to grow at a healthy pace of around 22% and 25% YoY respectively.

Geographically BorgWarner has achieved excellent diversification in their revenues with their North American, European and Asian segments all producing essentially a third of revenues for the firm.

This helps isolate BW from any localized economic underperformance while simultaneously increasing the firm’s ability to mitigate the impacts of geopolitical surprise events.

Adjusted operating margins for Q3 increased by 1.6% YoY to 10.1% as the firm’s net sales handily outgrew the rise in COGS. This increase in profitability has come despite a $10M increase in 2023 eR&D expenses which the firm believes are paramount to ensuring their Charging Forward 2027 strategic goals are achieved.

{kind=link}

Seeking Alpha’s Quant calculates a “ B+ ” profitability rating for BW which I believe to be an accurate relative evaluation of the firm’s current fiscal situation.

Nonetheless, it must be reiterated that BW has witnessed a slight contraction in their gross profit margin, net income margin and ROA compared to their 5Y averages as a result of a highly inflationary macroeconomic environment increasing COGS and slightly softening demand for their range of products.

Of course, BW’s long-term contracts help increase the stability of the firms’ revenues while the significant development of EV oriented products should allow BW to remain competitive for at least the next 15 years.

When considering BW’s balance sheet, it is clear that the firm is a well-managed enterprise from a capital allocation perspective with management maintaining a conservative approach despite their acquisitive streak.

The firm has $5.9B in total current assets while total current liabilities amount to just $3.57B. This solid short-term liquidity leaves BW with an excellent quick ratio of 1.21x and a current ratio of 1.65x.

These liquidity metrics are particularly impressive when compared to Magna’s quick and current ratios of just 0.72x and 1.11x respectively or Vitesco’s of 0.71x and 1.12x.

Total assets for BorgWarner amount to $14.1B with total liabilities just $8.1B. The firm has $5.77B in total shareholders’ equity. This leaves the firm with an excellent debt/equity ratio of 0.67x and a financial leverage ratio of 2.35x for FY22.

{kind=link}

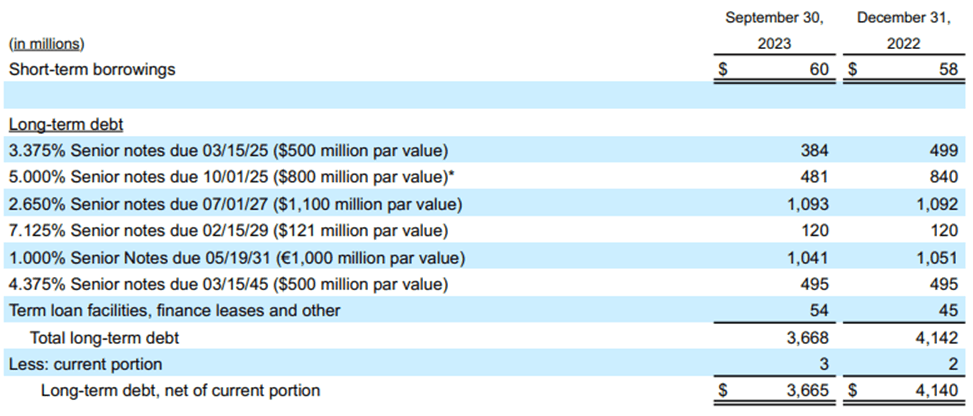

At the end of Q3 FY23, BorgWarner had $3.67B in long-term debt. Their staggered debt profile consisting of mostly fixed-rate notes illustrates management's conscientious approach to growth.

However, While the senior notes at 7.125% are a relatively small sum at just $141M par value, it is regrettable in my opinion to see such a high interest rate loan on the firms balance sheets.

Nonetheless, the relatively low rates on their other maturities illustrate that BW has acquired their newest businesses with well-planned finances and once again suggests that management is focused on maintaining a conservative approach to the firm’s capital allocation.

The recent streak of EV product related acquisitions has left BW with $2.94B worth of goodwill on their balance sheet. While this sum is over $1B higher than what the firm had in FY19, I do believe that most of this is soundly accounted for.

In many of these acquisitions, BW has specifically paid for the intellectual property these companies held with regards to various different forms of automotive technologies. Therefore, I am not overly concerned about the significant amount of goodwill and believe it accurately represents the value of these technologies.

Moody’s credit ratings agency affirmed a Baa1 credit rating for BorgWarner’s senior unsecured domestic notes while assigning a P-2 rating for the firm’s domestic commercial paper. The outlook remains stable. Moody’s classifies “Baa1” credit ratings as being of the highest “speculative grade”, due to some speculative elements being present in their rating.

{kind=link}

To further sweeten the deal for investors, BW also pays a reasonable dividend . The firm has consistently paid a dividend for 9 years with a dividend yield FWD of 1.28% and an annual payout FWD of $0.44.

While an acute economic downturn as seen in 2008 would almost certainly lead to BorgWarner pausing or decreasing their dividend, I believe management’s fundamental desire to reward shareholders is excellent to see.

I eagerly await the Q4 earnings report which will hopefully provide investors with more guidance regarding FY24 expectations and further data regarding BorgWarner’s success in meeting the goals set out in their Charging Forward business plan.

Valuation

{kind=link}

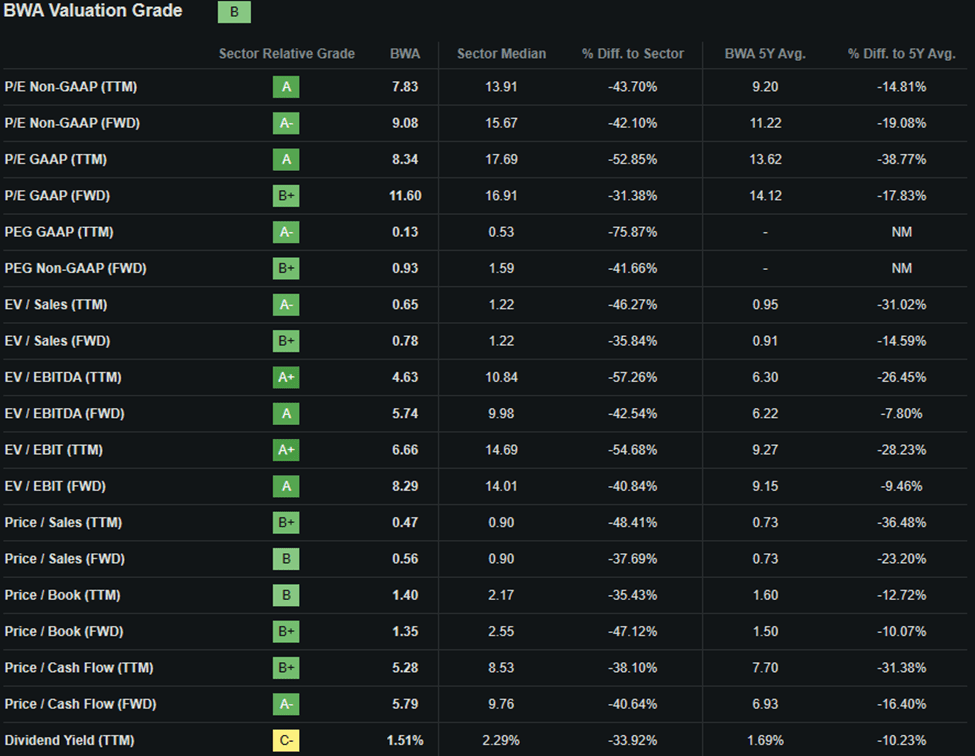

Seeking Alpha’s Quant assigns BorgWarner with a “ B ” Valuation grade. I believe even this letter grade is an excessively pessimistic representation of the value present within the firm’s stock and illustrates how very accurate relative quant ratings can sometimes poorly represent the absolute value present in a company’s shares.

The firm currently trades at a P/E GAAP TTM ratio of 8.34x. This represents a 39% decrease in the firm’s GAAP P/E ratio compared to their running 5Y average.

BorgWarner’s P/CF TTM of just 5.28x is reasonable while their TTM EV/EBITDA of just 4.63x is very low. The firm’s Price/Sales TTM of 0.47x is excellent and illustrates just how cheaply shares are currently trading.

To emphasize this metric, BorgWarner is currently trading at just half the value of their total sales in the TTM. Their Price/Book TTM of 1.40x is also very low especially when compared to the sector median of 2.17x.

Considering these basic valuation metrics alone I believe BorgWarner should already start to appear heavily undervalued given the stock’s historic averages.

{kind=link}

From an absolute perspective, BW shares are trading at a significant discount relative to previous valuations with current share prices of around $34.30 representing significant 30% contraction relative to the high’s seen in July 2023.

BW shares have also been soundly outperformed by the S&P500 index over the last five years with the popular SPY ETF outperforming BW by over 78%.

The relative valuation provided by simple metrics and ratios along with the absolute comparison already allow for a basic understanding of the value present in BorgWarner shares to be obtained. However, a quantitative approach to valuing the stock is still essential.

The Value Corner

By utilizing The Value Corner’s specially formulated Intrinsic Valuation Calculation, we can better understand what value exists in the company from a more objective perspective.

Using the firm’s current share price of $34.30, an estimated 2023 EPS of $3.78, a realistic “r” value of 0.08 (8%) and the current Moody’s Seasoned AAA Corporate Bond Yield ratio of 4.74x , I derive a base-case IV of $77.20. This represents a significant 56% undervaluation in shares.

When using a more pessimistic CAGR value for r of 0.03 (3%) to reflect a scenario where a globally spanning recession causes BW’s revenue growth to flatline while COGS remain roughly constant, shares are still valued at around $45.70 still suggesting a 25% undervaluation in the stock.

Considering the valuation metrics, absolute valuation and intrinsic value calculation, I believe that BorgWarner is soundly trading in deep-value territory.

In the short term (3-12 months), I find it difficult to say exactly what may happen to the firm’s valuation. Any acute recession in the U.S. or sudden shock to the economy could see shares tumble in the automotive supplier.

Still, it is difficult to understand how much further shares can realistically tumble given the massive discount already present in shares.

In the long-term (2-10 years), I believe BorgWarner will continue to be one of the most influential and critical automotive components suppliers in the industry thanks to their holistic Charging Forward strategic initiative.

Further expansion into the EV market should allow BorgWarner to harness significant growth and market share while their R&D initiatives could supply BW with an even greater intellectual advantage compared to competitors.

Risks Facing BorgWarner

BorgWarner faces some acute threats arising particularly from the cyclical demand environment for automobiles and the ensuing volatility present in demand for automotive parts by OEMs.

While contracts are usually agreed for around 10 years at a time, it is the current standard within the automotive industry for suppliers to reduce contract prices over time. This means BorgWarner must continue to work hard on the efficiency of their production processes to ensure their margins and returns are not overly affected by these price reductions.

However, I do believe that the EV revolution will supply BorgWarner with slightly larger pricing power compared to the mature ICE marketplace thanks to the uniqueness of BW’s product offerings.

Of course, this hypothesis relies on the assumption that BW continues to spend significant amounts of R&D to ensure their pace of innovation does now slow. Any reduction or complacency on behalf of BorgWarner could see their competitors come out ahead in a rapidly developing EV component race.

{kind=link}

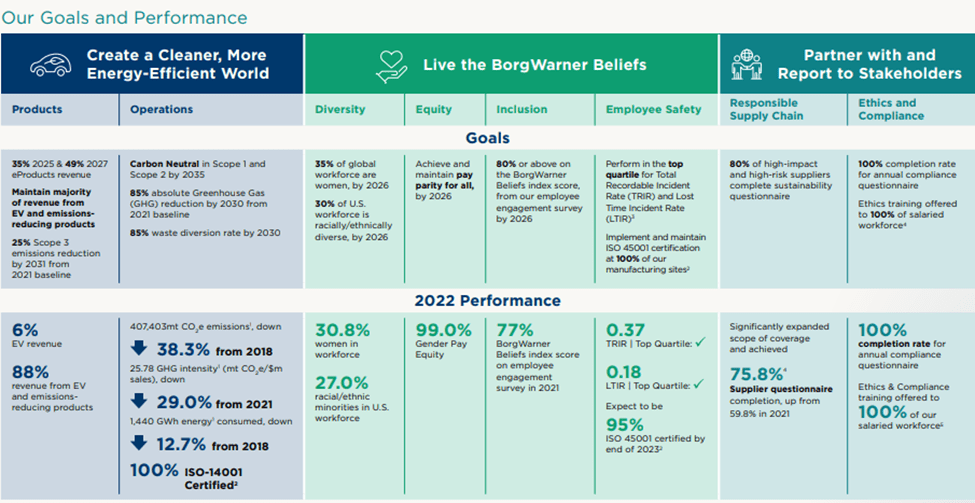

From an ESG perspective, BorgWarner faces little tangible threats. The firm has made it clear in their ESG report that the company as a whole is committed towards helping the globe transition towards a cleaner and less carbon-dependent future.

BW is also proud of their 9.0% gender pay equity and that the firm employs over 30% women in the workforce. BorgWarner is also committed to maintaining a dialogue with relevant governing bodies to ensure their business aligns with any and all applicable regulations.

The overall lack of any major environmental, societal or governance concerns suggest to me that BorgWarner may be a good choice for the more ESG conscious investor.

Of course, opinions may vary with regards to ESG material and I implore you to conduct your own ESG and sustainability research before investing in BW if these matters are of concern to you.

Summary

BorgWarner is an automotive parts and solutions supplier that for years appears to have been neglected by investors. The year 2023 in particular has seen the firm generate healthy earnings reports while simultaneously inking new supply deals and succeeding at innovating within the EV parts marketplace.

Despite this mostly positive FY23 so far, share prices appear to have stagnated in the supplier with a valuation gap suggesting a whopping 56% undervaluation in shares having emerged.

Even in my worst-case scenario analysis, BorgWarner is trading at roughly a 25% undervaluation which for me is a very healthy margin of safety when analyzing shares from a value perspective.

Considering the clarity and quality by which BW has not only presented their Charging Forward 2027 strategic initiative, but also begun to produce results from suggests to me that BorgWarner is well placed from a qualitative position to continue growing into the future.

Therefore, I rate BorgWarner a Strong Buy especially from a deep-value perspective and believe shares are heavily undervalued. To me, BorgWarner appears like a real fat-pitch idea.

For further details see:

BorgWarner: An Electrifying Future Up For Grabs At A Huge Discount